Reports

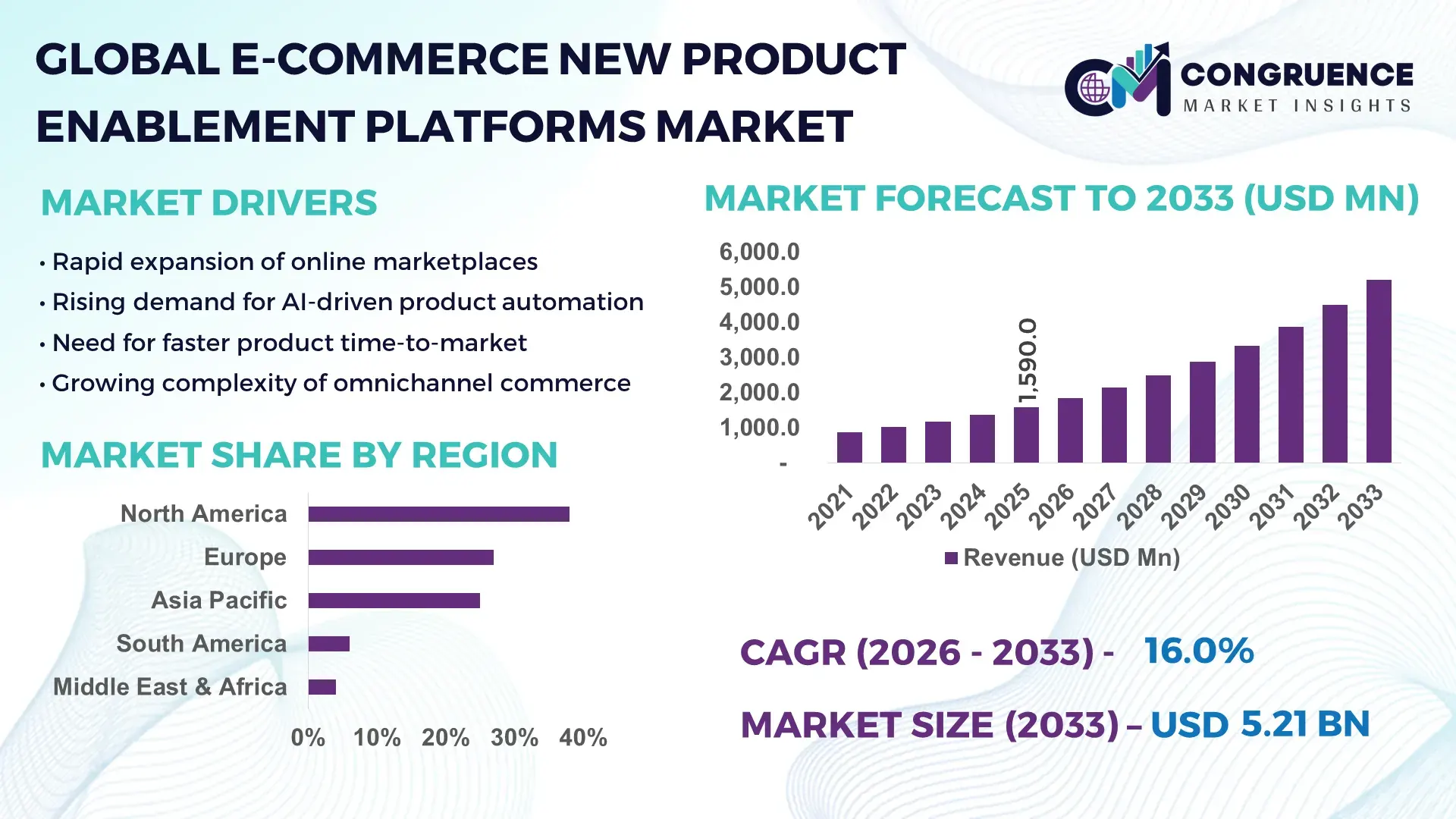

The Global E-Commerce New Product Enablement Platforms Market was valued at USD 1,590.0 Million in 2025 and is anticipated to reach a value of USD 5,212.7 Million by 2033, expanding at a CAGR of 16% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is driven by the accelerating need for faster product launches, real-time catalog synchronization, and AI-enabled content automation across omnichannel e-commerce ecosystems.

The United States dominates the global E-Commerce New Product Enablement Platforms landscape, supported by high enterprise software spending, advanced digital commerce infrastructure, and strong venture-backed innovation. Over 70% of Tier-1 U.S. retailers deploy dedicated platforms for product onboarding, enrichment, and syndication across marketplaces. Annual enterprise investment in e-commerce enablement software exceeds USD 12 billion, with significant allocation toward AI-driven product data automation, headless commerce, and API-based integrations. The U.S. also leads in SaaS platform deployment density, with more than 65% of large retailers using cloud-native enablement platforms to manage over 1 million SKUs annually. Key applications include marketplace expansion, D2C channel scaling, and rapid SKU localization, while technological advancements such as generative AI content creation and real-time compliance validation are widely embedded in commercial deployments.

Market Size & Growth: Valued at USD 1,590.0 Million in 2025, projected to reach USD 5,212.7 Million by 2033 at a CAGR of 16%, driven by accelerated digital product launch cycles.

Top Growth Drivers: Marketplace onboarding automation adoption at 48%, AI-based content enrichment improving efficiency by 42%, omnichannel expansion adoption at 37%.

Short-Term Forecast: By 2028, automated product enablement workflows are expected to reduce product launch timelines by 35%.

Emerging Technologies: Generative AI for product descriptions, headless commerce architectures, API-driven marketplace syndication engines.

Regional Leaders: North America projected at USD 2,050.0 Million by 2033 with enterprise SaaS adoption; Europe at USD 1,620.0 Million driven by compliance automation; Asia-Pacific at USD 1,180.0 Million supported by marketplace expansion.

Consumer / End-User Trends: Large retailers and brand manufacturers account for over 60% of platform usage, prioritizing speed-to-market and data accuracy.

Pilot or Case Example: In 2024, a U.S.-based omnichannel retailer reduced SKU onboarding errors by 46% using AI-enabled enablement software.

Competitive Landscape: Market leader holds approximately 18% share, followed by Adobe, SAP, Salesforce, Salsify, and Akeneo.

Regulatory & ESG Impact: Platforms increasingly embed automated compliance checks aligned with GDPR, DSA, and product traceability mandates.

Investment & Funding Patterns: More than USD 4.2 Billion invested globally in e-commerce enablement SaaS platforms since 2021.

Innovation & Future Outlook: Integration of AI copilots, real-time localization engines, and sustainability data layers is shaping next-generation platforms.

E-Commerce New Product Enablement Platforms primarily serve retail, consumer electronics, fashion, FMCG, and B2B distribution sectors, with retail contributing nearly 40% of platform deployments. Recent innovations include AI-powered product content generation, automated compliance validation, and real-time marketplace performance analytics. Regulatory alignment, cross-border commerce growth, and digital-first consumption patterns continue to shape adoption, while platform convergence with PIM and DAM systems defines the future outlook.

The E-Commerce New Product Enablement Platforms Market has become strategically critical as enterprises prioritize speed, accuracy, and scalability in digital commerce operations. These platforms enable centralized product data governance, automated enrichment, and rapid syndication across marketplaces and direct-to-consumer channels. AI-powered enablement solutions deliver up to 45% faster product launch cycles compared to traditional manual catalog management systems. Headless enablement architectures deliver 38% improvement in deployment flexibility compared to monolithic commerce platforms.

North America dominates in deployment volume, while Europe leads in compliance-driven adoption with over 58% of enterprises integrating regulatory automation into product enablement workflows. By 2028, generative AI-driven content automation is expected to improve catalog completeness KPIs by 40%, directly impacting conversion performance. Firms are committing to ESG-aligned data transparency initiatives, targeting 30% reduction in redundant product data storage by 2030 through centralized enablement platforms.

In 2024, a global consumer electronics brand achieved a 41% reduction in time-to-market by implementing AI-led product onboarding across 25 international marketplaces. Looking ahead, the E-Commerce New Product Enablement Platforms Market will function as a core pillar for operational resilience, regulatory compliance, and sustainable digital commerce growth, supporting enterprises navigating increasingly complex omnichannel environments.

The E-Commerce New Product Enablement Platforms Market is shaped by increasing SKU complexity, rapid marketplace proliferation, and growing reliance on automation to manage product data at scale. Enterprises face rising pressure to launch products simultaneously across multiple digital channels while maintaining accuracy, compliance, and localization. The convergence of PIM, DAM, and workflow automation into unified enablement platforms is redefining competitive dynamics. Cloud-native deployment models, API-first architectures, and AI-driven enrichment engines are becoming standard requirements, while integration with ERP, CRM, and analytics platforms strengthens enterprise adoption across retail and manufacturing sectors.

Retailers expanding across marketplaces, D2C platforms, and regional web stores increasingly rely on enablement platforms to manage SKU proliferation. Large retailers now manage 3–5× more active SKUs than five years ago, increasing dependency on automation. Enablement platforms reduce manual data handling by over 40%, improving launch consistency and operational efficiency. Marketplace-led commerce expansion across Asia-Pacific and Europe further amplifies demand for scalable onboarding and localization tools.

Many enterprises operate fragmented legacy systems lacking API compatibility, increasing integration costs and deployment timelines. Surveys indicate that 34% of mid-sized retailers face delays exceeding six months when integrating enablement platforms with ERP or CRM systems. Data migration challenges, inconsistent taxonomies, and limited internal digital skills continue to slow adoption, particularly among traditional wholesalers and regional retailers.

AI-enabled content generation, attribute mapping, and compliance validation unlock significant efficiency gains. Automated enrichment tools improve product data completeness by 45% and reduce human error rates by 38%. Emerging opportunities include real-time localization, sustainability data tagging, and automated regulatory updates, especially for cross-border e-commerce operations in Europe and Asia-Pacific.

As enterprises scale globally, maintaining consistent data governance across thousands of SKUs and channels becomes increasingly difficult. Over 50% of enterprises report inconsistencies in product attributes across regions, leading to listing rejections and compliance risks. Managing multilingual content, regulatory updates, and supplier-provided data at scale remains a significant operational challenge.

AI-Driven Content Automation: Over 62% of new deployments now include AI-based product description and attribute generation, reducing manual content creation time by 45% and improving listing approval rates by 30%.

Headless Enablement Architectures: Adoption of headless and API-first enablement platforms has increased by 39%, enabling enterprises to deploy product data seamlessly across web, mobile, and marketplace channels.

Marketplace-Centric Enablement: More than 55% of global retailers prioritize marketplace syndication features, supporting faster expansion into Amazon, Walmart, and regional platforms with 35% fewer onboarding errors.

Compliance and Sustainability Data Integration: Enablement platforms increasingly embed regulatory and ESG data layers, with 48% of enterprises tracking environmental attributes and compliance metadata directly within product catalogs.

The E-Commerce New Product Enablement Platforms Market is structured around distinct product types, application areas, and end-user categories that reflect how enterprises design, deploy, and operationalize digital product data at scale. Type-based segmentation differentiates platforms by their core technical approach to content generation, automation, and multimodal processing, ranging from text-first systems to more advanced video- and vision-enabled models. Application segmentation is driven by use cases such as product onboarding, marketplace syndication, catalog enrichment, compliance automation, and performance analytics, with varying levels of sophistication across industries. End-user segmentation spans large retailers, brand manufacturers, third-party sellers, and B2B distributors, each with unique requirements around speed, accuracy, and governance. Adoption intensity is shaped by SKU complexity, cross-border commerce exposure, regulatory scrutiny, and reliance on multi-channel selling, making segmentation critical for investment prioritization and platform strategy.

E-Commerce New Product Enablement Platforms can be broadly categorized into text-centric automation systems, vision-language models, video-language models, and hybrid multimodal platforms. Among these, vision-language models currently account for about 42% of adoption, as they enable automated image tagging, attribute extraction, and visual quality checks for product listings—capabilities that are now standard for major retailers managing millions of SKUs. Audio-text systems hold roughly 25%, primarily supporting voice-assisted catalog creation and supplier data ingestion workflows.

The fastest-growing type is video-language models (around 22% CAGR), driven by rising use of short-form product videos for marketplaces, automated scene summarization, and AI-generated video descriptions that improve discoverability and conversion. Adoption of video-language tools is expected to exceed 30% of total deployments by 2033 as brands increasingly require video-first product storytelling at scale.

Other types—including rule-based metadata engines, traditional PIM-centric workflows, and lightweight template automation tools—collectively represent about 33% of the market, serving niche needs such as legacy integrations, highly regulated catalogs, and low-complexity retail operations.

Key applications include product onboarding & listing automation, catalog enrichment, marketplace syndication, compliance validation, and performance analytics. Product onboarding and listing automation leads with roughly 40% share, as retailers prioritize faster time-to-list across Amazon, Walmart, and regional platforms while minimizing manual errors.

The fastest-growing application is marketplace syndication (about 20% CAGR), fueled by cross-border expansion, real-time price/attribute synchronization, and the need to manage dozens of channels from a single control layer.

Other applications—such as digital asset management integration, localization workflows, and returns data mapping—together account for about 35% of usage, supporting multi-language catalogs and supply-chain visibility. In 2025, around 37% of global retailers reported piloting AI-driven enablement tools to improve customer experience and product accuracy. Over 58% of Gen Z shoppers show higher trust in brands that use AI-enhanced product imagery, transparent attributes, and rich multimedia listings.

Large enterprise retailers lead adoption with approximately 38% share, driven by massive SKU volumes, multi-region operations, and strict governance requirements. These firms rely on centralized platforms to harmonize data across ERP, PIM, and marketplace systems.

The fastest-growing end-user segment is third-party marketplace sellers (around 21% CAGR), propelled by the professionalization of seller operations, rising competition on major platforms, and demand for automation that reduces manual listing work.

Brand manufacturers account for roughly 27%, prioritizing brand consistency, image quality, and global localization. B2B distributors, SMEs, and digital-first startups together represent about 35%, with adoption accelerating in industries such as electronics, beauty, and home goods. In 2025, about 36% of mid-sized brands tested centralized enablement platforms to unify product data across D2C and marketplace channels. Nearly 55% of U.S. omnichannel retailers reported measurable gains in listing accuracy after implementing AI-assisted enrichment tools.

North America accounted for the largest market share at 38% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 18% between 2026 and 2033.

The global E-Commerce New Product Enablement Platforms Market shows a clearly differentiated regional adoption pattern shaped by enterprise digital maturity, regulatory intensity, and e-commerce penetration. Europe follows North America with a 27% market share, driven by compliance-led digitization and cross-border commerce complexity. Asia-Pacific holds a 25% share, supported by massive marketplace ecosystems, mobile-first commerce, and rapid SME onboarding across China, India, and Southeast Asia. South America represents 6%, with growth linked to localization needs and marketplace expansion, while the Middle East & Africa accounts for the remaining 4%, driven by government-led digital transformation and retail platform modernization, reflecting a balanced yet maturity-skewed global distribution.

North America commands 38% of the global market, reflecting high enterprise adoption and advanced digital infrastructure. Demand is primarily driven by large retailers, consumer electronics brands, healthcare suppliers, and financial services platforms managing complex digital catalogs. Regulatory developments around data privacy, accessibility compliance, and digital transparency have accelerated adoption of automated product validation and enrichment tools. The region leads in AI-powered enablement, with over 65% of large enterprises integrating generative content and image-recognition capabilities into product workflows. Local players actively invest in headless commerce and API-first enablement layers to support omnichannel expansion. Consumer behavior shows higher adoption in healthcare and finance, where accuracy, compliance, and speed are mission-critical.

Europe holds 27% of the global market, with Germany, the UK, and France accounting for more than 60% of regional demand. Strict regulatory frameworks related to product labeling, sustainability disclosures, and digital services have increased reliance on structured enablement platforms. Sustainability initiatives and circular economy policies drive demand for platforms that track product origin, materials, and lifecycle data. Adoption of explainable AI and traceable content workflows is widespread, with over 50% of enterprises prioritizing compliance-ready enablement systems. Regional players focus on multilingual catalog automation and ESG-aligned data governance. Consumer behavior reflects high sensitivity to transparency and regulatory compliance.

Asia-Pacific accounts for 25% of the global market, ranking second in volume of active platform deployments. China, India, and Japan dominate regional consumption due to massive SKU volumes and marketplace-led retail models. Infrastructure investments in cloud computing and AI hubs across China and India support rapid deployment of scalable enablement platforms. More than 70% of new platform users in the region are SMEs leveraging automation to compete on regional marketplaces. Innovation hubs in China, India, and South Korea lead adoption of AI-driven localization and image-based attribute extraction. Consumer behavior is strongly influenced by mobile commerce and super-app ecosystems.

South America represents 6% of the global market, with Brazil and Argentina as primary contributors. Growth is tied to expanding e-commerce penetration and the need for Spanish- and Portuguese-language localization. Infrastructure improvements in cloud connectivity and regional data centers are enabling wider platform adoption. Government incentives supporting digital trade and SME digitization further strengthen demand. Local players emphasize catalog translation, pricing synchronization, and marketplace compatibility. Consumer behavior is closely linked to media-driven commerce and localized content presentation.

The Middle East & Africa accounts for 4% of the global market, led by the UAE and South Africa. Regional demand is influenced by retail diversification beyond oil & gas and increased focus on smart city and digital economy initiatives. Governments actively promote digital trade platforms and cross-border e-commerce integration. Retailers adopt enablement platforms to manage multilingual catalogs and compliance across diverse markets. Local enterprises prioritize mobile-ready and cloud-based solutions. Consumer behavior varies widely, with strong adoption in urban retail hubs and cross-border online purchasing.

United States – 32% Market Share: High enterprise digital maturity, large-scale SKU management needs, and strong investment in AI-driven commerce platforms.

China – 18% Market Share: Massive marketplace ecosystems, mobile-first commerce dominance, and large SME participation driving platform adoption.

The competitive environment in the E-Commerce New Product Enablement Platforms Market is characterized by a moderately consolidated landscape with numerous active players, reflecting vibrant innovation alongside established enterprise solutions. There are over 40 identified platforms competing globally, spanning legacy commerce providers, PIM/PXM specialists, cloud marketplace integrators, and AI-native automation startups. The combined share of the top 5 companies in this space accounts for approximately 55–60% of total deployments, indicating a competitive balance where large enterprises maintain influence but newer, niche innovators are rapidly gaining traction.

Leading competitors leverage distinct strategic initiatives to strengthen position and differentiation. Salsify has been recognized as a leader in product experience and information management for commerce, enhancing PIM capabilities with generative automation and expanded syndication coverage across 16+ Amazon Vendor/Seller markets. Legacy commerce platforms such as Adobe Commerce and SAP Commerce Cloud continue heavy investment in composable architectures, API-first tooling, and AI-enabled content workflows to support complex enterprise enablement needs. Strategic initiatives across the market include partnerships with AI and analytics providers, expanded marketplace integrations, product launches with headless enablement features, and mergers/acquisitions designed to broaden geographic reach or vertical specialization.

Innovation trends shaping competition include integration of generative AI for product content automation, API-driven real-time marketplace syndication, and advanced visual product recognition and metadata extraction. Smaller, AI-focused entrants also attract venture funding, supporting rapid development cycles and niche capabilities. Overall, the market is dynamic: top firms pursue ecosystem alliances and new product releases, while challengers focus on specialized automation, AI agents, and multi-channel operational support, creating a robust competitive environment that informs strategic decision-making for enterprise adopters.

Salesforce Commerce Cloud

Akeneo

Contentserv

InRiver

Pimcore

Bloomreach

Oracle CX Commerce

Shopify Plus

BigCommerce

Magento (Adobe)

Commercetools

Algolia

Elastic Path

Episerver – now Optimizely

Current and emerging technologies are rapidly transforming how enablement platforms support product onboarding, enrichment, and digital commerce operations. Artificial intelligence (AI) and generative AI (genAI) are now core components, automating tasks such as product description generation, attribute tagging, visual recognition, and image enhancement. Adobe’s commerce offerings continue to expand native AI capabilities, including generative content assistants and workflow automation agents that reduce integration effort by up to 50% for complex ERP and CRM connections. SAP Commerce Cloud’s CX AI Toolkit introduces cloud-native generative and visual search features that convert structured data into more engaging product experiences, enhancing shopper interaction and personalization.

Headless and composable architectures are reshaping platform design, enabling decoupled front-end experiences while maintaining centralized enablement logic. This modularity allows enterprises to rapidly deploy new product features, integrate marketplace syndication, and support omnichannel operations without costly monolithic upgrades. These architectures often include robust API layers that facilitate real-time synchronization between product master data and external sales channels. Visual search and image-based navigation tools are growing more prevalent, allowing customers to use photos or screenshots to find products directly within digital storefronts. Additionally, tools integrating agentic commerce experiences seek to unify product discovery, fulfillment, and AI-influenced shopping journeys within a cohesive platform, reducing friction across the purchase funnel.

Another important trend is the application of AI agents and autonomous workflows for operational tasks like automated alert triage, catalog consistency monitoring, and product set enrichment, driving down manual effort and operational costs. Research also highlights emerging frameworks for AI-generated synthetic product data, which can substitute for real datasets to train models that handle complex attribute relationships with high accuracy. Hybrid solutions combining structured and unstructured data intelligence are gaining favor, enabling better governance, compliance, and enriched consumer experiences across global markets.

• In March 2025, Salsify was named a Leader in the IDC MarketScape: Worldwide Product Information Management Applications for Commerce 2024-2025, underscoring its robust PIM/PXM platform and generative AI capabilities recognized among 18 global competitors. Source: www.salsify.com

• In 2024, Adobe Commerce expanded its composable development tools and AI-powered personalization features, including enhanced ERP integration starter kits to streamline product and customer data workflows for retail and B2B commerce implementations. Source: www.business.adobe.com

• In Q3 2024, Salsify expanded Amazon marketplace content support to include additional Vendor and Seller Central countries, enabling content syndication to 16 and 14 markets respectively and advancing Omni API support for richer supplier participation. Source: www.salsify.com

• In 2025, Perplexity partnered with Firmly.ai to introduce Agentic Commerce integration, creating a seamless product discovery-to-transaction pathway that enables merchants to maintain merchant-of-record status while enhancing user experience across the commerce funnel. Source: www.powercommerce.com

The scope of this E-Commerce New Product Enablement Platforms Market Report encompasses a comprehensive assessment of technology, applications, regional dynamics, and industry trends that influence how enterprises implement and scale product enablement solutions. The report covers product types ranging from text-centric automation systems and vision-language models to advanced video- and multimodal enablement platforms, delineating their functionality in catalog enrichment, metadata automation, marketplace syndication, and compliance workflows. It also analyzes application areas such as digital catalog management, launch acceleration, customer experience enhancement, and real-time analytics, offering insights into demand drivers across retail, consumer goods, and B2B distribution sectors.

Geographically, the report examines adoption patterns and strategic variations in key regions — North America, Europe, Asia-Pacific, South America, and Middle East & Africa — with an emphasis on enterprise digitization, regulatory frameworks, and local consumer behavior. It identifies emerging technologies affecting the market, including AI automation agents, headless architectures, visual search, and API-driven integrations that enable scalable commerce operations. Insights into competitive strategies — such as partnerships, platform ecosystem expansions, and innovation pipelines — equip decision-makers with an understanding of both established solutions and disruptive entrants reshaping enablement ecosystems. The report further highlights industry focus areas such as omnichannel readiness, compliance automation, and multilingual support, as well as specialized segments like marketplace optimization and AI governance frameworks, ensuring a full view of opportunities and operational complexities in today’s digital commerce landscape.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,590.0 Million |

| Market Revenue (2033) | USD 5,212.7 Million |

| CAGR (2026–2033) | 16.0% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Salsify, Adobe Commerce, SAP Commerce Cloud, Salesforce Commerce Cloud, Akeneo, Contentserv, InRiver, Pimcore, Bloomreach, Oracle CX Commerce, Shopify Plus, BigCommerce, Magento (Adobe), Commercetools, Algolia, Elastic Path, Episerver – now Optimizely |

| Customization & Pricing | Available on Request (10% Customization Free) |