Reports

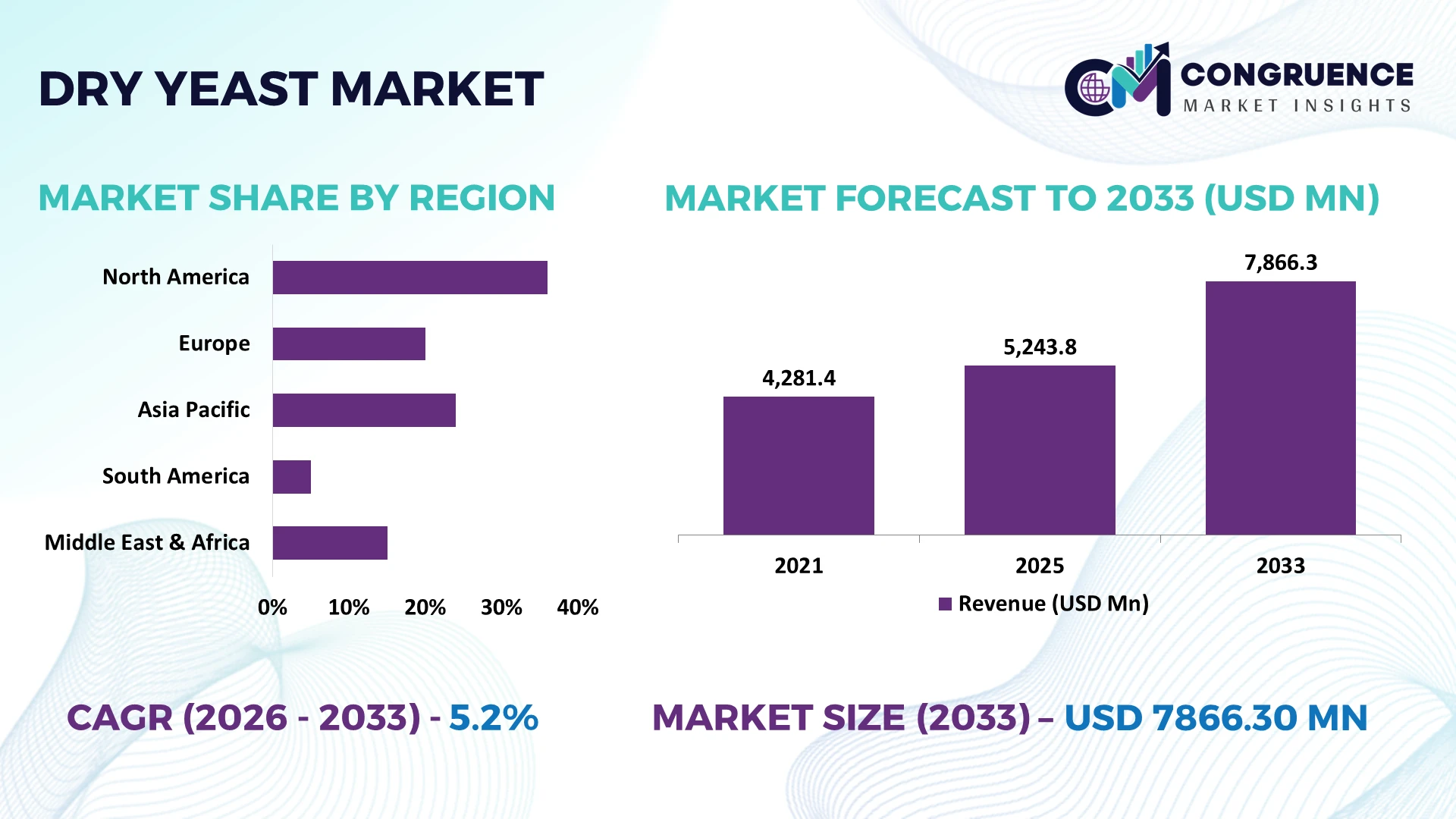

The Global Dry Yeast Market was valued at USD 5243.78 Million in 2025 and is anticipated to reach a value of USD 7866.3 Million by 2033 expanding at a CAGR of 5.2% between 2026 and 2033. Growth is driven by expanding industrial bakery production, higher demand for shelf-stable fermentation ingredients, and continuous improvements in high-activity instant dry yeast formulations that enhance processing efficiency and product consistency.

China remains the dominant production hub, accounting for approximately 32% of global dry yeast manufacturing capacity, supported by large-scale baking, food processing, and fermentation industries alongside sustained investment in automated production lines. France maintains leadership in premium baking applications through advanced fermentation expertise, while China produces over 420,000 tons annually. Trade diversification following Red Sea shipping disruptions has accelerated regional sourcing strategies across Europe and Asia.

Strategic investment in diversified manufacturing capacity, regional sourcing, and advanced fermentation technologies strengthens supply resilience while improving competitiveness across commercial baking and food processing markets.

Market Size & Growth: USD 5243.78 Million in 2025 reaching USD 7866.3 Million by 2033 at 5.2% CAGR, supported by advanced industrial bakery automation and fermentation efficiency improvements.

Top Growth Drivers: Industrial bakery output (+8%), convenience food consumption (+11%), and premium artisanal baking adoption (+9%) continue accelerating global demand.

Short-Term Forecast: By 2027, automated yeast production reduces manufacturing costs by nearly 12% while improving batch consistency by approximately 15%.

Emerging Technologies: AI-enabled fermentation monitoring, automated process control, and precision microbial optimization improve production efficiency by over 18%.

Regional Leaders: Asia-Pacific exceeds USD 3000 Million through bakery expansion, Europe surpasses USD 2200 Million via premium baking innovation, and North America approaches USD 1700 Million with automated food manufacturing adoption.

Consumer & End-User Trends: More than 60% of commercial bakeries prioritize instant dry yeast for longer storage stability and faster production cycles.

Pilot Case Example: In 2026, an automated fermentation optimization project improved yeast activity consistency by 14% while reducing processing time by 10%.

Competitive Landscape: Leading manufacturers collectively account for nearly 45% market share, supported by Lesaffre, AB Mauri, Angel Yeast, Lallemand, and Pakmaya.

Regulatory & ESG Impact: Energy-efficient production initiatives reduce operational emissions by approximately 16% while supporting stricter food manufacturing sustainability targets.

Investment & Funding: More than USD 600 Million supports capacity expansion, automation upgrades, and regional manufacturing diversification amid global supply-chain realignment.

Innovation & Future Outlook: Next-generation high-performance yeast strains, digital fermentation analytics, and precision bioprocessing strengthen production flexibility and premium bakery product development.

Dry yeast remains essential across commercial bakeries, food processing, frozen dough, and packaged convenience foods as manufacturers prioritize stable fermentation performance and extended shelf life. Advanced strain development and digital fermentation control improve production consistency, while nearly 18% higher process efficiency supports industrial operations. Regional manufacturing expansion and diversified ingredient sourcing continue strengthening supply resilience, setting the foundation for the following strategic market assessment.

Dry yeast has become strategically important as food manufacturers prioritize resilient ingredient supply, standardized fermentation performance, and efficient large-scale production. Supply-chain restructuring following recent logistics disruptions has encouraged localized manufacturing and multi-country sourcing strategies, reducing procurement risk while improving delivery reliability. At the same time, stricter food quality standards are accelerating investments in advanced fermentation control and automated quality assurance, strengthening competitive differentiation across industrial baking and processed food applications.

Modern AI-assisted fermentation monitoring improves batch consistency by nearly 15% while reducing production deviations by approximately 12% compared with conventional manual process control. China continues expanding manufacturing capacity through highly integrated production facilities, whereas France and Canada focus on premium yeast strains for artisan and specialty bakery applications with greater emphasis on product innovation than production scale. During the next two to three years, automated process adoption across commercial yeast plants is expected to exceed 40%, supported by digital production management and predictive maintenance systems.

A recent deployment of continuous fermentation technology enabled manufacturers to shorten processing cycles by around 10% while lowering energy consumption through optimized microbial control. Companies are responding by expanding regional production facilities, strengthening enzyme technology partnerships, and investing in precision fermentation research to improve product differentiation. Organizations that combine operational resilience, process automation, and diversified manufacturing networks will secure stronger competitive positioning as industrial food production continues evolving toward higher efficiency and supply reliability.

Commercial bakeries and food processors are accelerating adoption of high-performance dry yeast as automated production lines require consistent fermentation behavior and extended ingredient stability. More than 65% of industrial bakeries now prioritize instant dry yeast for standardized processing, while automated fermentation systems improve batch consistency by approximately 15% and reduce production losses by nearly 10%. China continues expanding high-capacity fermentation facilities to support domestic food manufacturing and export demand. In response, leading producers are increasing production capacity, investing in precision fermentation technologies, and establishing technical partnerships with bakery equipment suppliers. This integrated approach strengthens manufacturing efficiency, improves product quality, and creates long-term operational advantages across industrial baking ecosystems.

Molasses availability, energy pricing, and agricultural supply fluctuations continue creating structural pressure across dry yeast manufacturing. Feedstock costs account for nearly 40% of production expenses, while energy-intensive fermentation operations have experienced operating cost variations exceeding 18% during periods of market disruption. Brazil's sugar processing cycles and changing agricultural output directly influence global molasses availability, increasing procurement uncertainty for manufacturers. Companies are responding through multi-country sourcing strategies, localized inventories, and long-term supplier agreements to stabilize production planning. Strengthening procurement resilience has become a strategic priority as consistent raw material availability increasingly determines manufacturing efficiency, pricing discipline, and customer fulfillment performance.

Advanced fermentation analytics, microbial strain optimization, and digital manufacturing platforms are creating new opportunities for premium dry yeast production. AI-enabled fermentation control improves production efficiency by approximately 18%, while predictive maintenance reduces equipment downtime by nearly 20%. Japan continues investing in biotechnology innovation supporting precision microbial development for food-grade applications. Manufacturers are expanding research partnerships with biotechnology firms, integrating automated quality monitoring, and developing customized yeast formulations for frozen bakery, plant-based foods, and specialty nutrition. The strongest strategic opportunity lies in combining digital manufacturing with advanced strain engineering to deliver differentiated products while lowering operational costs and strengthening production flexibility.

Expanding manufacturing capacity without compromising microbial quality remains one of the industry's most complex execution challenges. Large-scale fermentation facilities require highly skilled technical personnel, while automated production validation increases implementation timelines by nearly 25%. Maintaining uniform yeast activity across multiple manufacturing sites also demands continuous digital monitoring, with quality deviations affecting production efficiency by approximately 12% if process controls are inconsistent. Germany's advanced food manufacturing sector demonstrates the importance of integrated automation and standardized quality systems for large-scale operations. Companies must strengthen workforce development, invest in intelligent production infrastructure, and establish global quality governance frameworks to maintain operational consistency, regulatory compliance, and long-term competitive differentiation.

Precision Fermentation Expands Industrial producers are deploying AI-assisted fermentation control, improving batch consistency by nearly 15% while reducing process deviations by 12%. Labor shortages across advanced food manufacturing hubs are accelerating automation investments. Companies are integrating predictive quality systems and digital process monitoring to shorten production cycles, improve yield stability, and strengthen large-scale manufacturing reliability.

Regional Production Diversification Supply-chain restructuring is shifting manufacturing closer to major consumption centers, with localized sourcing increasing by approximately 18% and cross-border logistics dependence declining by nearly 10%. Following global shipping disruptions, manufacturers are expanding production footprints in China, Türkiye, and Eastern Europe while establishing multi-supplier procurement models to reduce operational risk and improve delivery performance.

Specialized Product Portfolio Growth Commercial food manufacturers increasingly demand application-specific yeast formulations, with specialty product adoption rising by about 16% and frozen dough formulations expanding by 13%. Producers are responding through collaborative bakery innovation programs, customized fermentation solutions, and product differentiation strategies that improve processing efficiency while supporting premium baked goods and functional food applications.

Sustainability Through Process Optimization Energy-efficient fermentation technologies reduce processing energy consumption by approximately 14% while automated water recovery systems lower industrial water usage by nearly 11%. Environmental compliance requirements are encouraging manufacturers to modernize production infrastructure. Companies are investing in resource-efficient equipment, continuous fermentation systems, and circular manufacturing practices that strengthen long-term operational competitiveness.

Instant Dry yeast leads the market with an estimated 48% share because of its ease of use, extended shelf life, and compatibility with automated bakery operations. Its direct mixing capability eliminates rehydration, improving production speed by nearly 15% and reducing ingredient handling complexity. Active Dry yeast remains widely used in traditional commercial bakeries where established production workflows support consistent performance. Manufacturers continue enhancing both product categories through fermentation optimization, packaging improvements, and regional production expansion to improve supply reliability.

Specialty Dry yeast represents the fastest-growing segment as demand increases for premium bakery products, clean-label formulations, and application-specific fermentation solutions. Adoption has increased by approximately 17% among industrial food manufacturers seeking differentiated product performance. Fresh Dry yeast maintains relevance in selected bakery applications requiring specific fermentation characteristics but serves a comparatively smaller customer base. Companies are prioritizing specialty strain development, strategic partnerships with commercial bakeries, and expanded technical support services to capture higher-value industrial applications while balancing mature and emerging product demand.

Bread & Bakery accounts for approximately 56% of total dry yeast consumption because continuous commercial baking operations require reliable fermentation performance and high-volume ingredient availability. Automated bakery production has improved throughput by nearly 14%, encouraging greater use of standardized dry yeast products. Processed Foods represent a steadily expanding application as manufacturers incorporate fermentation ingredients into convenience products with improved texture and shelf stability. Companies continue scaling dedicated production capacity and strengthening technical collaboration with industrial bakery customers.

Nutritional Supplements are the fastest-growing application segment, supported by rising demand for yeast-derived proteins, vitamins, and functional nutrition ingredients. Adoption within nutrition-focused product development has increased by around 16%, while Alcoholic Beverages continue utilizing specialized yeast for fermentation quality and production consistency. Animal Feed remains strategically important through nutritional enrichment and livestock productivity improvements. Manufacturers are expanding specialized formulations, integrating automated production systems, and aligning product portfolios with evolving food manufacturing requirements across multiple application segments.

Bakeries remain the largest end-user group with an estimated 52% market share, driven by continuous production schedules, automated processing infrastructure, and high-volume ingredient consumption. Standardized fermentation improves production consistency by approximately 15%, making dry yeast indispensable for industrial baking operations. Food Processing companies represent the fastest-expanding buyer group as convenience foods, frozen dough products, and ready-to-eat categories require reliable fermentation ingredients. Suppliers are strengthening long-term contracts, technical services, and customized product offerings to secure enterprise customers.

Beverage Manufacturers continue investing in specialized fermentation solutions for product consistency, while the Feed Industry maintains stable demand through nutritional applications. Nutraceutical Companies are expanding purchases as functional nutrition products increasingly incorporate yeast-derived ingredients, with procurement volumes rising by approximately 14%. Manufacturers are responding through application-specific formulations, collaborative product development, flexible pricing strategies, and regional distribution partnerships to strengthen customer retention and improve competitive positioning across diversified industrial end-user segments.

Asia-Pacific accounted for the largest market share at 42% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a 6.4% between 2026 and 2033.

Advanced Food Manufacturing Drives Market Stability

North America represents a mature dry yeast market supported by highly automated commercial bakeries, integrated food processing facilities, and strong adoption of precision fermentation technologies. The region contributes approximately 24% of global demand, with industrial bakeries accounting for a significant share of ingredient consumption. Automated fermentation monitoring has improved production consistency by nearly 15%, while expanded cold-chain infrastructure strengthens distribution efficiency for packaged food manufacturers. Companies continue investing in digital manufacturing platforms, long-term ingredient supply partnerships, and production optimization programs to improve operational resilience. Enterprise demand for premium bakery products, frozen dough applications, and functional food ingredients continues supporting innovation across commercial-scale fermentation processes while maintaining high quality and traceability standards.

United States Market Outlook: The United States remains the region's operational center because of its large commercial baking industry, advanced food manufacturing infrastructure, and extensive automation deployment. More than 70% of industrial bakeries operate with highly automated production systems, encouraging widespread adoption of standardized dry yeast solutions. Manufacturers continue expanding fermentation capacity, strengthening ingredient supply agreements, and investing in digital quality control technologies to improve productivity while supporting evolving consumer preferences for premium baked and convenience food products.

Sustainability and Premium Fermentation Shape Expansion

Europe maintains a strong competitive position through advanced fermentation expertise, premium bakery production, and rigorous food quality standards. The region accounts for nearly 27% of global market activity, supported by extensive industrial bakery networks and established fermentation technology providers. Energy-efficient production upgrades have reduced manufacturing energy consumption by approximately 14%, while sustainable processing investments continue modernizing production facilities. Companies increasingly prioritize low-emission manufacturing, specialized yeast development, and collaborative innovation with bakery manufacturers to strengthen product differentiation. Premium bread, frozen bakery products, and clean-label food applications remain central to operational expansion across major manufacturing economies.

France Market Outlook: France serves as the regional innovation leader through its longstanding fermentation expertise and globally recognized baking industry. Industrial producers continue developing high-performance yeast strains tailored for artisan and industrial bakery applications. Advanced fermentation systems have improved batch precision by approximately 13%, while manufacturers expand research collaborations and production modernization programs to strengthen export competitiveness and premium product positioning across international food manufacturing markets.

Manufacturing Scale Strengthens Global Leadership

Asia-Pacific leads global dry yeast production through extensive manufacturing infrastructure, expanding commercial bakery capacity, and competitive production costs. Approximately 42% of worldwide market activity is concentrated within the region, supported by integrated fermentation facilities and rapidly growing processed food industries. China and neighboring manufacturing hubs continue increasing automated production capacity, with several facilities improving operational efficiency by nearly 18% through intelligent process control. Companies are expanding regional manufacturing networks, optimizing logistics, and investing in large-scale fermentation technologies to strengthen export capability while meeting rising domestic consumption across bakery and processed food sectors.

China Market Outlook: China remains the largest production base because of its integrated fermentation industry, abundant raw material availability, and advanced industrial manufacturing ecosystem. Large-scale production facilities manufacture more than 420,000 tons annually while increasingly deploying AI-assisted fermentation management to improve efficiency and quality consistency. Leading producers continue expanding production infrastructure, strengthening export capabilities, and investing in specialized yeast formulations supporting bakery, food processing, and nutritional ingredient applications.

Agricultural Integration Supports Industrial Expansion

South America benefits from strong agricultural resources supporting molasses availability and fermentation feedstock production, creating a competitive foundation for dry yeast manufacturing. The region contributes approximately 5% of global market activity while increasing investment in industrial bakery production and processed food manufacturing. Modern fermentation facilities have improved production efficiency by nearly 11% through equipment modernization and operational optimization. Manufacturers continue strengthening regional distribution networks and establishing strategic partnerships with commercial bakeries to improve supply reliability. Infrastructure constraints remain present in selected markets, encouraging companies to prioritize localized production and inventory management strategies.

Brazil Market Outlook: Brazil dominates the regional market through its extensive sugar processing industry, providing a stable supply of fermentation raw materials. Integrated food manufacturing and expanding bakery production continue supporting domestic dry yeast demand. Producers increasingly invest in automated fermentation technologies and long-term procurement agreements, while production optimization initiatives have improved manufacturing productivity by approximately 12%, strengthening both regional competitiveness and export opportunities.

Food Manufacturing Investments Accelerate Adoption

The Middle East & Africa market is undergoing structural transformation as governments and private enterprises expand domestic food manufacturing capabilities to strengthen food security. Industrial bakery investments, modern processing facilities, and regional logistics improvements continue supporting dry yeast adoption across commercial food production. Manufacturing modernization programs have increased processing efficiency by approximately 10%, while new food industry investments encourage localized ingredient sourcing. Companies are responding through joint ventures, regional production expansion, and technical partnerships that improve supply stability while reducing import dependence across rapidly developing food manufacturing sectors.

Saudi Arabia Market Outlook: Saudi Arabia leads regional market development through large-scale food manufacturing investments, expanding industrial bakery infrastructure, and national food security initiatives. Advanced food processing projects continue increasing demand for high-performance fermentation ingredients, while automated production technologies improve manufacturing consistency by nearly 14%. Companies are strengthening regional manufacturing partnerships, expanding warehouse infrastructure, and developing localized supply networks to support long-term industrial food production growth.

The market is led by Lesaffre, Angel Yeast, AB Mauri, Lallemand, and Pakmaya, competing directly with regional fermentation specialists and cost-focused domestic manufacturers. The top five players collectively control approximately 46% of global market share, creating a moderately consolidated structure where global technology leaders challenge regional producers on performance, while local manufacturers compete aggressively on pricing and supply responsiveness. Competition centers on fermentation efficiency, product consistency, customization, and manufacturing scale, with automated production improving batch uniformity by nearly 15% and optimized strains increasing process efficiency by around 12%. Premium suppliers differentiate through application-specific yeast solutions, whereas regional firms strengthen local distribution and shorter delivery cycles. Companies are expanding production facilities, forming bakery technology partnerships, investing in precision fermentation, and integrating upstream raw material procurement to improve supply resilience. Growing consolidation and greater control over fermentation technology raise entry barriers, requiring new entrants to combine scalable manufacturing, differentiated formulations, and dependable regional supply networks to outperform established competitors.

Lesaffre

Angel Yeast Co., Ltd.

AB Mauri

Lallemand Inc.

Pakmaya

Oriental Yeast Co., Ltd.

Ohly GmbH

Kerry Group plc

DSM-Firmenich

Leiber GmbH

Biospringer

Alltech Inc.

Traditional batch fermentation is rapidly being replaced by AI-enabled process control, precision microbial monitoring, and automated production management. Intelligent fermentation platforms improve batch consistency by approximately 15% while reducing production deviations by nearly 12% compared with conventional manual monitoring. More than 45% of newly commissioned industrial yeast facilities now integrate digital process analytics, enabling faster quality validation and improved operational traceability. Large multinational producers benefit most because standardized automation supports consistent production across multiple manufacturing locations.

Emerging technologies focus on advanced strain engineering, continuous fermentation, and predictive maintenance. Continuous fermentation shortens production cycles by nearly 10% while lowering energy consumption by approximately 14% compared with conventional batch operations. Digital twins and real-time sensor networks are increasingly deployed to optimize microbial performance and equipment utilization before operational bottlenecks occur. Companies integrating these technologies gain stronger production flexibility, reduced downtime, and faster response to changing customer specifications, strengthening competitive differentiation in industrial baking and food processing.

Between 2026 and 2028, precision fermentation integrated with machine learning is expected to become a standard capability among leading manufacturers. Automated quality inspection, intelligent resource optimization, and next-generation microbial development will improve manufacturing efficiency while supporting customized yeast formulations for bakery, nutrition, and processed food applications. Companies investing early in integrated digital fermentation ecosystems, scalable automation, and high-performance strain development will strengthen supply resilience, accelerate product innovation, and secure long-term competitive advantage against manufacturers relying on conventional production technologies.

October 2024 Lesaffre completed the acquisition of dsm-firmenich's yeast extract business, integrating 46 specialized employees and advanced yeast-processing technologies to strengthen fermentation capabilities and expand its global savory ingredients portfolio, improving product innovation and manufacturing integration.

June 2025 Lesaffre and MicroBioGen entered an exclusive global partnership to commercialize advanced yeast biotechnology across baking, food, and biochemical applications, combining complementary R&D platforms to accelerate next-generation strain development and improve industrial fermentation performance. Source: https://www.microbiogen.com

August 2025 Lesaffre announced investment in a new state-of-the-art yeast production and packaging facility in Ghent, Belgium, expanding industrial capacity to better serve global beverage manufacturers while strengthening production flexibility and supply reliability. Source: https://www.lesaffre.com

July 2026 Lesaffre welcomed the adoption of the first Codex Alimentarius global standard for baker's yeast following international technical collaboration, creating a harmonized regulatory framework that supports consistent product quality and facilitates broader international market access.

The report provides comprehensive analysis across Active Dry, Instant Dry, Fresh Dry, and Specialty Dry yeast while evaluating demand across Bread & Bakery, Alcoholic Beverages, Processed Foods, Animal Feed, and Nutritional Supplements. It further examines purchasing trends among bakeries, food processors, beverage manufacturers, feed producers, and nutraceutical companies across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. More than 40% of industry demand remains concentrated in high-volume commercial bakery operations, while specialty formulations continue expanding across premium food applications.

The assessment covers competitive positioning, manufacturing capacity expansion, precision fermentation, automation, AI-enabled process monitoring, digital quality management, and sustainable production technologies. It evaluates strategic initiatives of leading manufacturers, regional supply-chain diversification, deployment trends, and evolving customer requirements. The report supports investment evaluation, capacity planning, product portfolio optimization, partnership development, competitive benchmarking, and long-term expansion strategies while identifying emerging opportunities expected to influence market dynamics between 2026 and 2033.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 5243.78 Million |

Market Revenue in 2033 | USD 7866.3 Million |

CAGR (2026 - 2033) | 5.2% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Lesaffre, Angel Yeast Co., Ltd., AB Mauri, Lallemand Inc., Pakmaya, Oriental Yeast Co., Ltd., Ohly GmbH, Kerry Group plc, DSM-Firmenich, Leiber GmbH, Biospringer, Alltech Inc. |

Customization & Pricing | Available on Request (10% Customization is Free) |