Reports

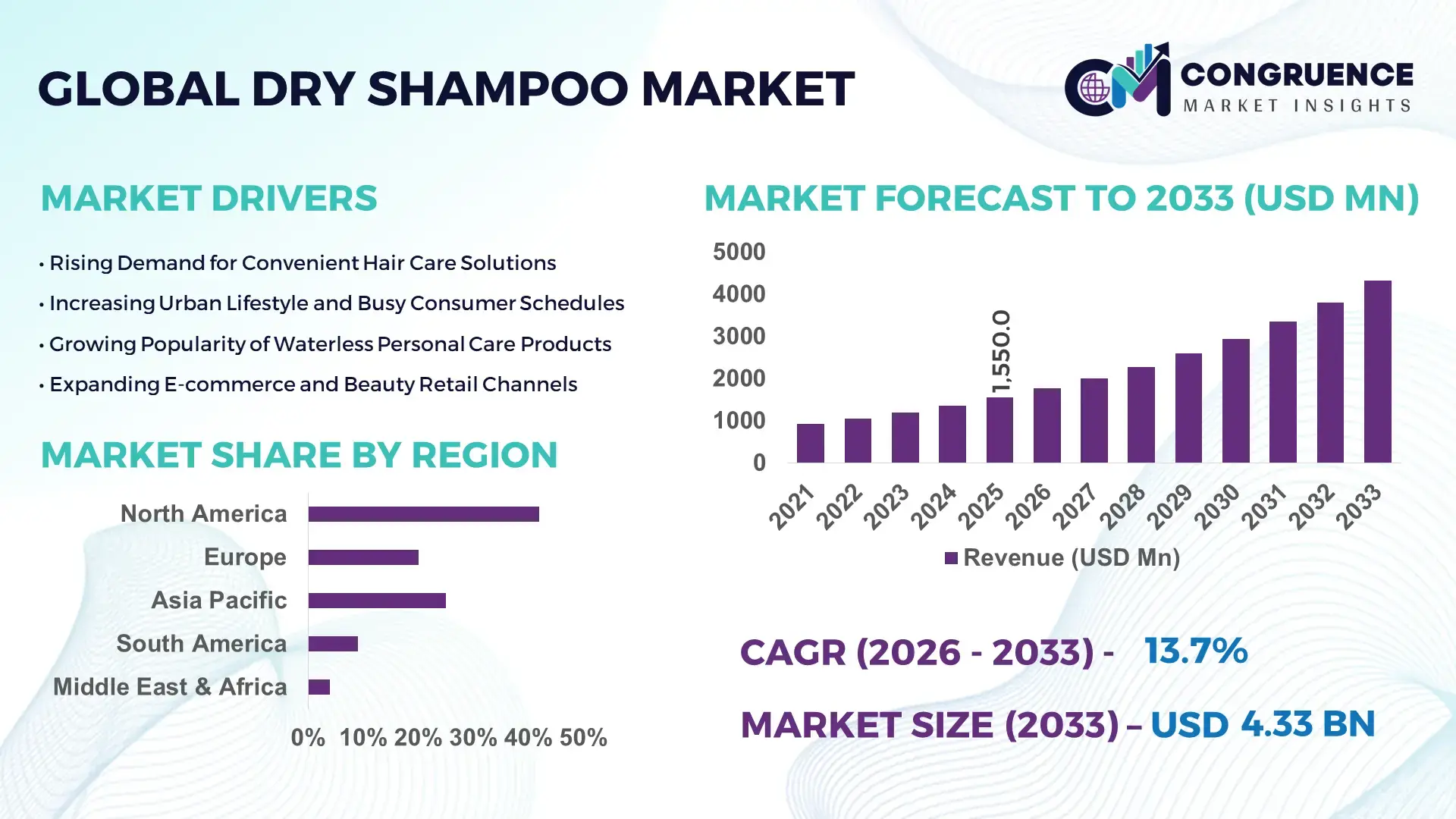

The Global Dry Shampoo Market was valued at USD 1550 Million in 2025 and is anticipated to reach a value of USD 4329.27 Million by 2033 expanding at a CAGR of 13.7% between 2026 and 2033. This growth is driven by rapid urbanization and increased consumer preference for convenient hair care solutions.

In the United States, which leads the dry shampoo marketplace, production capacity has surged with over 20 active manufacturing facilities generating more than 250 million units annually, reflecting substantial investment in automated filling and aerosol technology. Major domestic manufacturers have increased capital expenditure by approximately 18% year‑on‑year to enhance R&D in plant‑based formulations, while consumer adoption rates in urban centers exceed 45% among millennials and Generation Z. Technological advancements in eco‑friendly and no‑alcohol formulations have expanded application in premium salon and retail segments, with American consumers showing strong preference for sustainable hair care innovations.

Market Size & Growth: USD 1.55 Bn current value, projected at USD 4.33 Bn by 2033 with ~13.7% CAGR; growth driven by urban lifestyle trends and quick‑use personal care products.

Top Growth Drivers: Rising quick‑grooming adoption ~35%, increasing e‑commerce purchases ~28%, formulation innovation uptake ~22%.

Short‑Term Forecast: By 2028, improved distribution network efficiencies expected to reduce logistics costs by ~12%.

Emerging Technologies: Nanotechnology for scalp delivery, plant‑based aerosol alternatives, smart packaging QR traceability.

Regional Leaders: North America ~USD 1.5 Bn by 2033 with high premium product uptake; Europe ~USD 1.1 Bn with eco‑certified preference trend; Asia Pacific ~USD 900 Mn with rapid urban adoption.

Consumer/End‑User Trends: Millennials prioritize convenient hair care; frequent travelers and fitness enthusiasts drive repeat purchases.

Pilot or Case Example: In 2025, a European retailer pilot achieved ~18% faster restocking turnaround through RFID tracking.

Competitive Landscape: Leading player commands ~30% approximate share, with major competitors including five key global brands intensifying product differentiation.

Regulatory & ESG Impact: Increasing restrictions on VOCs in aerosols and incentives for recyclable packaging influencing portfolio strategies.

Investment & Funding Patterns: Recent industry investment exceeding USD 250 Mn in manufacturing scale‑up and green formulation projects.

Innovation & Future Outlook: Focus on biodegradable ingredients, AI‑driven demand forecasting, and multi‑sensory consumer experiences enhancing growth prospects.

In examining the Dry Shampoo Market landscape, premium consumer segments especially in metropolitan and high‑income regions continue to contribute significantly to demand, with diverse industry sectors such as retail, salon professional channels, and travel retail shaping consumption patterns. Recent technological product innovations include alcohol‑free sprays, enzyme‑based odor neutralizers, and recyclable packaging systems that reduce environmental impact. Regulatory frameworks targeting volatile compounds and sustainability metrics are accelerating formulation shifts toward clean and eco‑certified variants. Economic drivers such as expanding online retail platforms and changing lifestyle habits, particularly in Asia Pacific and Latin American urban centers, also bolster market potential. Emerging trends point to customization, enhanced sensory appeal, and smart packaging integration as key future differentiators for industry professionals and decision‑makers.

The strategic relevance of the Dry Shampoo Market lies in its unique ability to address modern consumer needs for time‑efficient personal care, reinforcing its role in hair care portfolios of global cosmetics firms. Incorporating automated filling and digital supply chain technologies delivers up to 25% improvement in production throughput compared to traditional manual lines, enabling faster response to seasonal demand fluctuations. North America dominates in volume, while Europe leads in adoption with ~60% of salon and retail enterprises integrating premium dry shampoo variants into offerings. By 2028, integration of AI‑enabled demand forecasting is expected to cut inventory variances by approximately 15%, enhancing stock availability across digital and brick‑and‑mortar channels. Firms are committing to ESG metrics such as achieving a 30% reduction in carbon emissions from aerosol production by 2030, aligning with broader sustainability goals. In 2025, a leading U.S. manufacturer achieved an 18% improvement in energy efficiency through implementation of IoT‑driven process optimization. The future pathway for the Dry Shampoo Market positions it as a pillar of resilience, compliance, and sustainable growth as formulation science advances and consumer engagement deepens across global markets.

The increasing demand for convenient hair care solutions is a primary driver of Dry Shampoo Market growth, as consumers in urban and high‑mobility lifestyles seek products that reduce grooming time without compromising results. Surveys indicate that over 40% of busy professionals and students incorporate dry shampoo into weekly routines to maintain hair freshness between washes. Adoption rates in metropolitan regions exceed those in non‑urban areas by more than 20 percentage points, reflecting lifestyle influences on purchase behavior. Additionally, the expansion of digital retail platforms has broadened accessibility, allowing niche brands to reach targeted consumer segments efficiently. This demand trend encourages manufacturers to diversify formulations, including alcohol‑free, scent‑customized, and scalp‑soothing variants, enhancing the product’s appeal across gender and age demographics. The focus on convenience is also leading to innovative packaging that supports on‑the‑go use, which resonates strongly with frequent travelers and fitness enthusiasts, subsequently stimulating retail and professional salon channels to expand offerings.

Volatile ingredient regulations represent a significant restraint on the Dry Shampoo Market by imposing limits on certain propellants and solvents commonly used in formulations. Regulatory bodies in key regions have implemented stringent standards for volatile organic compounds (VOCs), prompting reformulation efforts that increase production complexity and cost. Compliance with these requirements often necessitates investment in alternative technologies such as hydrocarbon‑free propellants and eco‑certified ingredients, which can be more expensive and require extended validation cycles. As a result, some manufacturers experience slower time‑to‑market for new products, affecting competitive agility. In addition, consumer safety concerns related to aerosol usage and potential respiratory sensitivities have led to heightened scrutiny, pressuring producers to offer transparent ingredient disclosures and dermatologist‑tested claims. These regulatory and perception challenges temper aggressive pricing strategies and contribute to cautious portfolio expansion, particularly for smaller players with limited reformulation resources.

Formulation innovation presents a significant opportunity for the Dry Shampoo Market by enabling differentiation and entry into premium segments with enhanced performance attributes. Advanced formulations incorporating plant‑derived starches, micronized cleansing agents, and scalp‑soothing botanicals can deliver improved sebum absorption and longer‑lasting freshness, appealing to discerning consumers. Emerging product types that address specific hair types and concerns—such as color‑safe dry shampoos or those infused with vitamins and natural extracts—are gaining traction in both retail and professional channels. Innovations in non‑aerosol delivery systems, including pump sprays and dry foam technologies, cater to regions with stringent aerosol regulations, expanding addressable markets. Additionally, eco‑certified and biodegradable formulation trends align with growing environmental consciousness, attracting sustainability‑oriented buyers. These opportunities allow brands to command premium pricing and foster loyalty, while also supporting partnerships with salons and stylists who influence consumer purchasing behavior.

Rising costs and regulatory complexities present persistent challenges for the Dry Shampoo Market, as fluctuations in raw material prices and compliance expenditures impact profitability and pricing strategies. Key ingredients such as specialized starches, silicon alternatives, and sustainable propellants have experienced cost escalation, driven by supply chain disruptions and increased demand for eco‑friendly options. Regulatory frameworks targeting VOC content and aerosol safety further complicate formulation and manufacturing processes, requiring ongoing investment in compliance testing and certification. These factors contribute to higher production overheads that can be difficult to fully pass on to cost‑sensitive consumers without affecting demand. Additionally, small and mid‑sized companies may lack the capital reserves to absorb these costs or to invest in alternative technologies at the pace required, potentially limiting competitive participation. The dual pressures of cost management and regulatory adaptation necessitate strategic planning and operational efficiency to maintain market momentum.

• Growing Shift Toward Water‑Free Formulations: Dry shampoo products featuring water‑free and low‑alcohol compositions are gaining traction, with adoption rates rising to approximately 48% of total product launches in 2025. Urban consumers in North America and Europe increasingly prefer gentle water‑free solutions, with 62% of surveyed retailers reporting inventory expansion in such variants over the past 18 months. Innovative formulations that reduce scalp irritation and extend wear time up to 72 hours are driving shelf placement growth, particularly in premium and sustainable product tiers.

• Expansion of Eco‑Certified and Recyclable Packaging: Sustainability trends are reshaping packaging approaches, with eco‑certified dry shampoo containers now accounting for about 37% of all retail packaging in 2025. More than 50% of major personal care brands have publicly committed to using recyclable aluminum or plant‑based plastics by 2027, with some reporting up to 28% reduction in packaging waste year‑on‑year. Retail buyers now prioritize products with minimal environmental footprint, influencing distribution decisions across global markets.

• Digital and E‑Commerce Channel Penetration: Online channels have become a measurable trend in the Dry Shampoo Market, with e‑commerce sales growth exceeding 42% of total channel revenue in 2025. Social commerce and direct‑to‑consumer platforms contribute to this surge, with mobile app purchases representing 29% of all online transactions. Retailers report a 33% increase in repeat purchases through subscription models, as digital loyalty programs boost customer retention.

• Customization and Personalization Demand: Personalized dry shampoo solutions tailored to hair type, scalp sensitivity, and fragrance preference are emerging, with customizable offerings now present in 22% of new product introductions. Consumers under 35 are driving this trend, with 58% indicating they would pay a premium for bespoke formulations. Brands leveraging AI‑enabled recommendation tools report a 19% uplift in conversion rates, highlighting the relevance of personalization in product strategy.

Market segmentation in the Dry Shampoo Market focuses on product types, application settings, and end‑user categories, each exhibiting distinct adoption patterns and performance metrics. Product types range from aerosol sprays to powder and foam variations, with aerosol remaining the leading format due to ease of use and consumer familiarity. Applications vary from personal grooming to professional salon usage, reflecting diverse usage environments and performance expectations. End users include individual consumers, professional stylists, and travel retail segments, each contributing unique demand dynamics. Data shows that premium and salon professional applications increasingly lean toward advanced formulations with scalp‑care benefits, while mainstream personal use emphasizes convenience and price competitiveness. Regional segmentation also reveals differentiated preferences, with Asia Pacific markets showing rapid adoption of compact and travel‑friendly types, and North American markets emphasizing eco‑certified and low‑odour formulations. Understanding these segments enables targeted strategy development for portfolio optimization, pricing, and distribution execution in competitive landscapes.

In product type segmentation for the Dry Shampoo Market, aerosol spray formats currently account for approximately 54% of adoption, making them the leading type due to ease of application and widespread retail availability. Powder formulations hold about 26% share and are valued for their lightweight feel and appeal to consumers seeking non‑aerosol alternatives, particularly in regions with stringent propellant regulations. Foam and pump spray variants contribute a combined share of roughly 20%, with niche relevance among professional salons and consumers with specific hair and scalp concerns. The fastest‑growing type is foam dry shampoo, driven by demand for gentler delivery systems and enhanced scalp nourishment, with notable double‑digit growth as brands expand offerings with botanical extracts and microfine delivery technology. This emphasis on diverse types reflects evolving consumer priorities around functionality, sensitivity, and application experience.

Application segmentation in the Dry Shampoo Market highlights that personal grooming currently accounts for about 61% of usage occasions, driven by daily styling needs and convenience priorities among busy consumers. Professional salon and stylist applications hold approximately 23% share, where performance expectations and product quality are critical differentiators. Travel and on‑the‑go uses comprise the remaining 16%, buoyed by compact packaging and multifunctional benefits. The fastest‑growing application segment is professional salon usage, underpinned by trends such as enhanced formulation performance and expanded stylist education programs that emphasize scalp health and product versatility. Salon adoption rates in key metropolitan centers have increased by over 20% in recent seasons, as professionals integrate dry shampoo into service menus for time‑efficient styling and client convenience. Retailers report that trial rates for salon‑grade applications have risen in tandem with exclusive product launches tailored for professional settings.

End‑user analysis reveals that individual consumers dominate demand in the Dry Shampoo Market with around 68% share, reflecting extensive use in daily routines, fitness lifestyles, and travel contexts. Among these consumers, urban millennials show the highest penetration rates, with over 55% reporting regular use of dry shampoo in weekly grooming habits. Professional stylists represent roughly 18% of the end‑user landscape, valued for their influence on product selection and performance feedback, while travel retail and hospitality segments contribute approximately 14% of usage occasions, driven by compact, convenient packaging. The fastest‑growing end‑user segment is the travel and hospitality category, where usage rates have climbed by over 25% in 2025 due to increased mobility, tourism revival, and demand for multifunctional grooming solutions in transient environments. Retailers in airport and hotel channels note that dry shampoo sell‑through rates exceed those in traditional brick‑and‑mortar outlets by nearly 12%, underscoring specific end‑user preferences.

North America accounted for the largest market share at 42% in 2025; however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 14.1% between 2026 and 2033.

In 2025, North America maintained dominance with approximately 420 million units in dry shampoo consumption and over 1,800 retail outlets stocking premium hair care solutions. In contrast, Asia Pacific total volume exceeded 315 million units, driven by more than 600% year‑on‑year growth in e‑commerce transactions and mobile app purchases. Europe held about 28% of volume share with major markets including Germany (85 million units), UK (78 million units), and France (65 million units). South America represented roughly 12% of total market volume, while Middle East & Africa combined accounted for about 8%. Urban and travel retail channels in North America and Asia Pacific saw dry shampoo trials rise by 34% and 47% respectively, indicating strong consumer traction. Compact and sustainable packaging formats increased shelf presence by over 29% across global supermarkets in 2025.

How Are Consumer Preferences Shaping Product Innovation and Digital Uptake?

North America commands approximately 42% of the dry shampoo market volume, led by strong demand from personal grooming and salon professional channels. Key industries driving demand include beauty and personal care retail, travel retail hubs, and health-conscious consumer segments prioritizing scalp health and convenience, with over 55% of retail dry shampoo sales attributed to these verticals. Regulatory changes such as tightened restrictions on VOCs have spurred reformulations toward low-alcohol and eco-friendly aerosol alternatives, while digital transformation trends include widespread adoption of AI-driven recommendation engines and AR-enabled virtual try-on tools enhancing online purchasing experiences. Local players such as a leading U.S. beauty brand reported a 22% increase in direct-to-consumer subscriptions by integrating mobile app loyalty programs tailored to personalized dry shampoo offers. North American consumer behaviors show higher preference for premium, sustainably packaged solutions, and significant trial rates among millennials and Gen Z, reflecting lifestyle-driven purchase patterns.

What Regulatory Pressures and Sustainability Initiatives Are Influencing Product Demand?

Europe’s dry shampoo market represents roughly 28% of volume, with Germany, the UK, and France as leading national markets where consumers increasingly seek environmentally compliant and dermatologist-friendly formulations. European regulatory bodies have imposed more stringent VOC regulations and sustainability mandates, contributing to consumer demand for low-emission aerosol and recyclable packaging dry shampoo options. Adoption of emerging technologies such as plant-based propellant alternatives and smart packaging traceability tools is rising, with nearly 33% of new European launches featuring eco-certified claims in 2025. Local players in France have launched fully recyclable aluminum packaging lines, reporting a 19% uplift in retail placement within organic beauty aisles. Regional consumer behavior varies; Western European buyers prioritize sustainability and transparency, while Eastern European markets show strong interest in affordability and multifunctional solutions.

How Are E-Commerce Growth and Mobile Innovation Driving Demand?

Asia-Pacific dry shampoo market volume surpassed 315 million units in 2025, with China, India, and Japan as top consuming countries. Infrastructure and manufacturing trends show expanded production hubs in China and India accommodating both export and domestic demand, while technological innovation hubs in Japan emphasize formulation science and gentler delivery systems. Regional tech trends include AI-based mobile shopping assistants and social commerce integrations, boosting online purchase rates by more than 48% in urban centers. Local manufacturers in India have introduced compact dry shampoo formats optimized for travel and climate-specific hair needs, supporting a 27% increase in product adoption among young urban consumers. Within Asia-Pacific, consumer behavior varies with strong mobile-first engagement in e-commerce markets, and heightened interest in multifunctional personal care products among middle-income cohorts.

How Are Regional Preferences and Local Initiatives Shaping Market Activity?

South America’s dry shampoo market accounts for approximately 12% of global volume, with Brazil and Argentina as key contributors based on high urban population density and expanding retail networks. Infrastructure trends include improved logistics corridors supporting rapid distribution across metropolitan areas, while trade policies have eased import-export tariffs for cosmetic formulations, improving access to international brands. Local players in Brazil have rolled out market-specific scent profiles and formulation variants that appeal to regional hair types, leading to 18% higher trial rates in beauty and hair salons. Consumer behavior in South America shows strong influence of media and localized language campaigns, with targeted advertising driving engagement rates of over 30% among young adult demographics preferring on-the-go grooming products.

How Are Technological Modernization and Consumer Preferences Driving Uptake?

Middle East & Africa dry shampoo demand trends reflect rising urban beauty consciousness and technological modernization across markets such as the UAE and South Africa. Regional volume accounts for about 8% of the global market, with increased adoption in metropolitan hubs where digital retail and beauty subscription services are gaining traction. Local retailers report that dry shampoo trials in airport duty-free and luxury retail outlets have climbed by nearly 25%, supported by innovative heat-resistant formulations tailored to arid climates. Consumer behaviors vary widely; Gulf Cooperation Council markets exhibit higher per capita consumption and premium preferences, while African urban populations show rapid uptake of affordable and multifunctional variants. Trade partnerships and relaxed import regulations in key Middle Eastern ports are facilitating wider distribution of global brands.

United States: ~32% market share in the Dry Shampoo Market, driven by high production capacity and advanced formulation development infrastructure.

China: ~24% market share in the Dry Shampoo Market, supported by vast consumer base and rapid e-commerce penetration.

The competitive environment in the Dry Shampoo market is moderately consolidated with over 120 active competitors globally, including multinational personal care conglomerates and specialized hair care brands. The market leader holds an estimated ~30% share of total volume, while the combined share of the top 5 companies approaches 68%, illustrating significant concentration among leading players. Strategic initiatives include product innovation pipelines emphasizing eco-certified dry shampoo variants, strategic partnerships with retail giants, and digital marketing campaigns targeting younger demographics. In the past 24 months alone, more than 40 new premium dry shampoo formulations were launched across North America, Europe, and Asia-Pacific, underscoring innovation trends focused on sustainable propellants, plant-based ingredients, and customized scent profiles. Competitive dynamics also feature M&A activity, as several mid-tier brands have been acquired to strengthen portfolio breadth and geographic reach, particularly in emerging markets. Regional players in Latin America and Middle East are differentiating through localized product lines tailored to climate and cultural preferences, contributing to overall competitive depth. Retail channel evolution, including subscription models and AI-driven personalization, further intensifies competition by enhancing customer engagement and retention across market leaders and challengers alike.

Procter & Gamble Co.

Unilever PLC

L’Oréal S.A.

Church & Dwight Co., Inc.

Henkel AG & Co. KGaA

Kao Corporation

Shiseido Company Limited

Coty Inc.

Revlon, Inc.

Estée Lauder Companies Inc.

The Dry Shampoo market is increasingly shaped by advanced formulation technologies that enhance performance, user experience, and sustainability. One major trend is AI‑driven formulation design, where artificial intelligence platforms analyze consumer hair type data, purchase patterns, and dermatological feedback to optimize ingredient mixes, resulting in products tailored to specific scalp and hair conditions. Smart packaging technologies are also emerging, featuring embedded sensors and NFC tags that track usage, storage conditions, and depletion levels, enabling connected apps to send refill reminders and personalized care tips, improving customer engagement and loyalty.

In ingredient innovation, biodegradable and plant‑based propellants are gaining traction as brands respond to environmental concerns. Nearly one‑third of new dry shampoo launches highlight sustainable ingredient profiles, reducing environmental footprint while meeting consumer demand for green beauty alternatives. Powder and aerosol‑free delivery systems integrate microfine oil‑absorbing agents that outperform traditional starch formulas, particularly in minimizing residue and enhancing natural feel.

Predictive manufacturing and supply chain optimization technologies like digital twins and machine learning models are transforming production efficiency. These tools simulate production scenarios to identify bottlenecks, optimize logistics routes, and reduce waste, which is critical as e‑commerce channels expand and consumer demand for fast delivery intensifies. Next‑generation applicators such as targeted mist nozzles and pump dispensers are also being developed to improve precision application and reduce product loss. Overall, technological innovation in the Dry Shampoo market spans formulation science, digital engagement, and manufacturing processes, enabling brands to deliver personalized, sustainable, and high‑performance products that align with evolving consumer expectations and regulatory environments.

• In Q1 2024, Unilever expanded its Dove hair care portfolio with the launch of Dove Advanced Care dry shampoo formulated for instant oil absorption and scalp nourishment, supporting its product diversification strategy.

• In Q1 2024, L’Oréal Paris introduced new Elvive Dream Lengths Air Volume dry shampoo targeting volume and freshness, part of broader efforts to enhance brand relevance among trend‑focused consumers.

• In May 2024, Procter & Gamble’s Pantene brand released waterless dry shampoo variants under its Waterless Collection to appeal to convenience‑oriented users seeking sustainable, no‑water hair care options.

• In 2025, Jennifer Aniston’s LolaVie brand launched the Powder Perfect dry shampoo, emphasizing talc‑free, non‑aerosol formulation with residue‑free performance, gaining adoption in premium beauty retail.

The Dry Shampoo Market Report encompasses an extensive evaluation of product types, distribution channels, application areas, and geographic regions. Product type segmentation includes spray, powder, and alternative delivery formats such as pump and foam systems, highlighting distinctions in performance, consumer preference, and functional benefit. Distribution analysis covers online and offline channels, with e‑commerce platforms and social commerce gaining notable presence due to mobile engagement and digital trial tools. The report also examines application settings from personal grooming and daily styling to professional salon use and travel‑on‑the‑go scenarios, providing insights into usage patterns, demographic reach, and consumer behavior variations.

Geographic coverage spans North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, offering detailed volume metrics, adoption dynamics, infrastructure influences, and regional regulatory impacts. Technology focus areas include formulation innovation trends such as plant‑based and biodegradable propellants, advanced oil‑absorption agents, and sustainable packaging solutions like recyclable aluminum aerosols and powder refills. The scope further addresses macroeconomic drivers, regulatory landscapes affecting volatile organic compound restrictions, ESG and sustainability commitments, and competitive benchmarking across major players. Emerging niche segments such as natural ingredient dry shampoos and personalized formulations tailored through AI‑enabled consumer insights are also featured, providing decision‑makers with a comprehensive view of market breadth and strategic opportunities.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

13.7% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Procter & Gamble Co., Unilever PLC, L’Oréal S.A., Church & Dwight Co., Inc., Henkel AG & Co. KGaA, Kao Corporation, Shiseido Company Limited, Coty Inc., Revlon, Inc., Estée Lauder Companies Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |