Reports

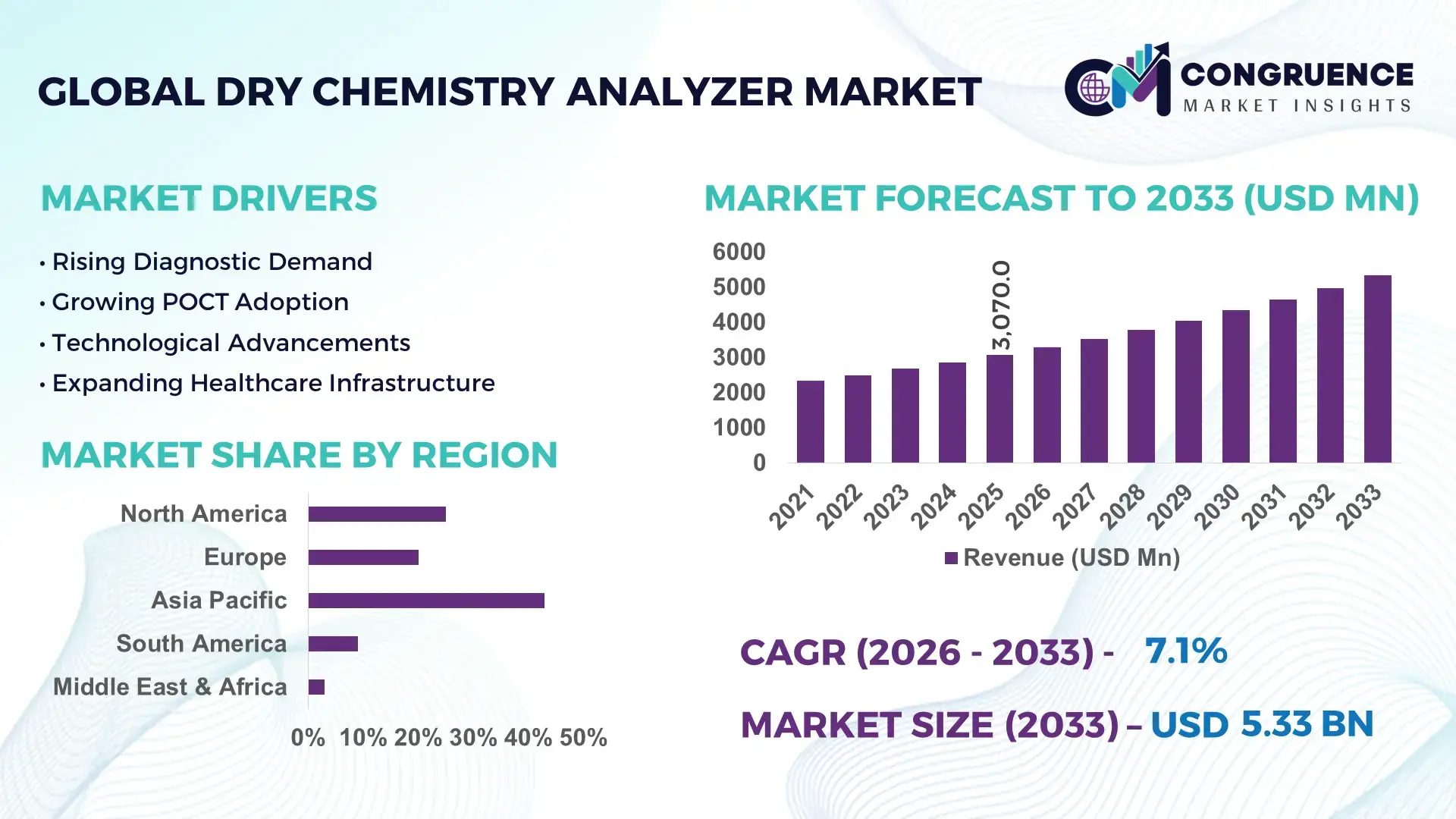

The Global Dry Chemistry Analyzer Market was valued at USD 3070 Million in 2025 and is anticipated to reach a value of USD 5334.27 Million by 2033 expanding at a CAGR of 7.15% between 2026 and 2033. Growth is being driven by expanding decentralized diagnostics, rising chronic disease testing volumes, and accelerated adoption of reagent-efficient dry chemistry platforms across hospitals, diagnostic laboratories, and point-of-care settings.

The United States leads the market with approximately 32% global demand share, supported by large-scale clinical laboratory networks, annual healthcare technology investments exceeding USD 20 billion in diagnostics modernization, and digital analyzer integration rates above 65%. In comparison, China accounts for nearly 18% of market activity, driven by hospital infrastructure expansion and domestic manufacturing capacity growth. The 2026 healthcare supply-chain resilience initiatives implemented across North America and Asia have further accelerated localized analyzer deployment, while automated testing workflows improved laboratory throughput by nearly 25% in leading facilities.

Organizations prioritizing high-throughput, reagent-stable, and digitally connected dry chemistry systems are positioned to strengthen testing efficiency, operational scalability, and long-term diagnostic service competitiveness.

Market Size & Growth: USD 3070 Million in 2025 reaching USD 5334.27 Million by 2033 at 7.15% CAGR, supported by automation-driven laboratory modernization.

Top Growth Drivers: Point-of-care testing adoption +18%, chronic disease diagnostics +14%, laboratory automation deployment +16%.

Short-Term Forecast: By 2028, laboratory processing efficiency improves by 22% while reagent wastage declines by 15%.

Emerging Technologies: AI-assisted calibration, cloud-connected analyzers, and automated quality control systems improve workflow accuracy by 20%.

Regional Leaders: North America exceeds USD 1.8 Billion, Asia-Pacific surpasses USD 1.5 Billion, Europe approaches USD 1.2 Billion, supported by digital diagnostics expansion.

Consumer/End-User Trends: More than 60% of advanced laboratories prioritize compact analyzers with integrated data management capabilities.

Pilot/Case Example: In 2026, automated dry chemistry deployment projects reported testing turnaround-time reductions of approximately 28%.

Competitive Landscape: Top manufacturers collectively hold nearly 45% share, with major competition centered on innovation, automation, and service networks.

Regulatory & ESG Impact: Energy-efficient analyzer designs reduce operational power consumption by nearly 12% while supporting compliance objectives.

Investment & Funding: Global investments exceed USD 1 Billion, driven by strategic partnerships, regional manufacturing expansion, and supply-chain diversification.

Innovation & Future Outlook: Next-generation AI-enabled analyzers and remote diagnostics platforms increase workflow productivity by over 25%, strengthening precision testing strategies.

Dry Chemistry Analyzer Market demand is expanding across clinical diagnostics, hospital laboratories, preventive healthcare screening, and decentralized testing environments. Advanced microfluidic technologies, AI-supported quality control systems, and compact multi-parameter analyzers are improving testing accuracy and workflow efficiency, with automated platforms delivering approximately 20% faster processing times. Growing localization of diagnostic manufacturing and stricter laboratory performance standards are accelerating technology upgrades, creating a strong foundation for the strategic market discussion ahead.

Dry chemistry analyzers are becoming strategically important as healthcare systems prioritize decentralized diagnostics, faster turnaround times, and laboratory efficiency under increasing testing volumes. The market is benefiting from infrastructure modernization programs, digital laboratory integration, and supply-chain restructuring initiatives aimed at reducing dependence on centralized testing models. More than 60% of newly upgraded mid-sized laboratories are incorporating automated chemistry platforms that support higher throughput with lower reagent handling requirements, strengthening operational resilience and investment attractiveness.

Technology migration is accelerating competitive differentiation. Modern dry chemistry systems deliver approximately 25% faster sample processing and reduce reagent waste by nearly 20% compared with conventional wet chemistry workflows. The United States remains focused on advanced automation and data-connected diagnostics, while China is expanding deployment through domestic manufacturing and hospital capacity upgrades. Laboratories adopting integrated analyzer platforms report workflow productivity improvements of around 18%, particularly in high-volume clinical testing environments where staffing efficiency has become a critical performance metric.

Over the next two to three years, deployment of AI-assisted quality control, remote monitoring, and compact multi-test analyzers is expected to expand across hospitals and diagnostic chains. Companies are increasing partnerships with healthcare providers, investing in localized production, and expanding service networks. Organizations that combine automation, supply security, and digital interoperability will secure stronger competitive positioning and long-term operational advantage.

The rapid shift toward decentralized diagnostics is strengthening demand for dry chemistry analyzers across hospitals, outpatient centers, and independent laboratories. Point-of-care testing utilization has increased by approximately 18%, while automated laboratory workflows have improved testing throughput by nearly 22% in large healthcare networks. In the United States, healthcare providers are expanding distributed diagnostic capabilities to reduce turnaround times and optimize workforce productivity. This operational shift directly increases demand for compact, reagent-efficient analyzer systems. Manufacturers are responding through technology partnerships, analyzer portfolio expansion, and integrated software development. A notable strategic insight is that facilities prioritizing workflow automation are achieving greater testing capacity without proportional increases in laboratory staffing, improving both operational efficiency and service scalability.

Procurement costs for advanced analyzer components remain elevated due to ongoing dependence on specialized sensors, optics, and consumables. Imported diagnostic components account for nearly 40% of critical inputs in several healthcare markets, while logistics costs remain approximately 12% above pre-disruption levels in certain supply chains. In India and other developing healthcare systems, budget constraints limit deployment beyond major urban laboratory networks. These pressures affect purchasing cycles, replacement rates, and profitability for distributors and healthcare providers. Companies are mitigating risk through localized manufacturing, long-term supplier agreements, and regional inventory strategies. An important operational insight is that supply reliability increasingly influences purchasing decisions as much as instrument performance, particularly for multi-site diagnostic organizations.

The integration of artificial intelligence, predictive maintenance, and cloud-based diagnostics is creating new value pools beyond traditional testing functions. AI-assisted quality control can reduce manual validation workloads by approximately 20%, while remote monitoring systems improve equipment utilization rates by nearly 15%. China and India are emerging as attractive deployment markets due to expanding diagnostic infrastructure and increasing digital health investments. Companies are accelerating R&D programs focused on connected analyzers capable of real-time performance monitoring and automated calibration. A less obvious opportunity lies in subscription-based service models that bundle diagnostics, software, and maintenance into unified platforms, creating recurring customer relationships while improving laboratory efficiency and equipment uptime.

Long-term market expansion depends on successful integration of advanced analyzers into increasingly digital healthcare ecosystems. Nearly 30% of laboratory modernization projects encounter interoperability challenges between analyzer platforms and laboratory information systems, while skilled diagnostic workforce shortages exceed 15% in several developed healthcare markets. As laboratories adopt AI-enabled workflows, cybersecurity and data governance requirements are becoming more stringent. These complexities affect deployment consistency, operational continuity, and technology utilization rates. Companies must invest in workforce training, interoperable software architectures, and secure data management frameworks. A critical strategic insight is that competitive advantage will increasingly depend not only on analyzer performance but also on the ability to integrate seamlessly into complex clinical and digital infrastructure environments.

• AI-Driven Workflow Optimization Laboratory operators are increasingly integrating AI-assisted calibration and automated quality control into dry chemistry workflows. Adoption among advanced diagnostic networks has exceeded 35%, while manual validation requirements have declined by nearly 20%. Persistent laboratory staffing shortages and growing test volumes are accelerating deployment. Companies are expanding software partnerships and embedding predictive analytics into analyzer platforms, improving throughput consistency and reducing operational bottlenecks across high-volume testing environments.

• Portable Testing Expansion Accelerates Portable and point-of-care dry chemistry analyzers are gaining traction beyond traditional hospital settings. Deployment across outpatient and community healthcare facilities has increased by approximately 25%, while test turnaround times have improved by nearly 30% compared with centralized workflows. Healthcare infrastructure modernization in India and China is supporting broader adoption. Manufacturers are prioritizing compact system development, battery-efficient designs, and mobile connectivity to capture demand from decentralized diagnostic networks.

• Localized Manufacturing Strategies Emerge Supply-chain resilience has become a strategic priority following recurring component sourcing disruptions. Several diagnostic manufacturers have increased localized production capacity by more than 15%, reducing procurement lead times by approximately 18%. The trend is reshaping procurement strategies, particularly among healthcare providers seeking stable consumable availability. Companies are restructuring supplier networks, expanding regional assembly operations, and securing long-term component agreements to improve operational continuity.

• Connected Diagnostics Ecosystems Advance Integration between analyzers, laboratory information systems, and cloud-based monitoring platforms is accelerating. Connected diagnostic deployments have risen by roughly 22%, while remote equipment monitoring has improved instrument uptime by nearly 12%. A less obvious shift is the growing use of analyzer performance data for predictive maintenance planning. Companies are investing in interoperability standards, digital service platforms, and enterprise-level data integration to strengthen customer retention and service differentiation.

Fully Automated Analyzers represent the leading segment due to their ability to support high-throughput testing, standardized workflows, and seamless laboratory information system integration. Large hospital laboratories and diagnostic chains increasingly favor these platforms because they reduce manual intervention and improve processing efficiency by nearly 25%. Benchtop Analyzers remain widely deployed in medium-sized laboratories where space optimization and operational flexibility are critical. Semi-Automated Analyzers continue serving cost-sensitive facilities, particularly in developing healthcare markets, although purchasing preference is gradually shifting toward higher automation levels. Companies are expanding automated portfolios and incorporating AI-enabled quality control functions to strengthen differentiation.

Portable Analyzers are emerging as the fastest-growing type as decentralized diagnostics gains momentum. Deployment in outpatient settings and remote healthcare facilities has increased by approximately 20%, supported by demand for rapid testing and mobility. Point-of-Care Analyzers are also expanding due to their ability to support immediate clinical decision-making and reduce sample transport requirements. Manufacturers are increasing investments in compact designs, wireless connectivity, and multi-parameter testing capabilities, reflecting a broader market transition from centralized testing infrastructure toward distributed diagnostic ecosystems.

Clinical Diagnostics holds the largest share of application demand because hospitals and laboratories require continuous testing for chronic disease management, metabolic assessment, and routine patient monitoring. More than 60% of analyzer utilization is linked to clinical diagnostic workflows where testing speed and consistency directly influence patient management. Blood Chemistry Testing remains a mature and essential segment, benefiting from established testing protocols and broad healthcare adoption. Companies continue expanding menu capabilities and integrating automated reporting tools to improve laboratory productivity and diagnostic accuracy.

Disease Screening is the fastest-growing application segment, driven by preventive healthcare initiatives and rising demand for early detection programs. Screening-related testing volumes have increased by approximately 18% in several healthcare systems implementing broader population health strategies. Emergency Testing is gaining strategic importance as healthcare providers seek faster diagnostic support in acute-care environments. Veterinary Diagnostics is also expanding steadily as companion animal healthcare spending rises and veterinary clinics adopt advanced testing technologies. Manufacturers are scaling deployment programs, improving analyzer portability, and integrating digital connectivity to support evolving application requirements across both human and animal healthcare settings.

Hospitals remain the dominant end-user group due to large testing volumes, advanced laboratory infrastructure, and continuous demand for diagnostic services. Major healthcare systems account for approximately 45% of analyzer deployments, supported by broad testing portfolios and integrated clinical workflows. Diagnostic Laboratories follow closely, leveraging automation and high-throughput systems to improve operational efficiency and manage increasing specimen volumes. Manufacturers are targeting these buyers through enterprise service contracts, software integration capabilities, and workflow optimization solutions designed for complex testing environments.

Ambulatory Care Centers represent the fastest-growing end-user segment as healthcare delivery shifts toward decentralized and same-day diagnostic models. Deployment of compact analyzers in ambulatory settings has increased by nearly 20%, reflecting demand for rapid testing closer to patients. Clinics are expanding analyzer adoption to improve service responsiveness, while Research Institutes continue utilizing advanced systems for biomarker and translational research applications. Veterinary Centers are also strengthening demand through modernization of animal diagnostic services. Companies are responding with customized product configurations, flexible pricing structures, and strategic healthcare partnerships that align with evolving procurement priorities across diverse care settings.

North America accounted for the largest market share at 36% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.4% between 2026 and 2033.

Laboratory Automation Driving Market Leadership

North America maintains the leading position in the Dry Chemistry Analyzer Market, supported by advanced healthcare infrastructure, high laboratory automation rates, and strong adoption of digital diagnostic technologies. The region accounts for approximately 36% of global demand, with deployment concentrated across integrated hospital systems and large diagnostic laboratory networks. More than 65% of high-volume laboratories utilize automated chemistry platforms to improve workflow efficiency and reduce turnaround times. Ongoing investments in connected diagnostics and AI-assisted quality control are strengthening operational productivity. Strategic collaborations between healthcare providers and technology vendors continue to accelerate analyzer modernization and software integration initiatives.

United States Market Outlook: The United States represents the largest national market due to extensive laboratory capacity, advanced clinical testing infrastructure, and strong healthcare technology adoption. Large healthcare systems are expanding investments in automated diagnostics to address workforce shortages and rising testing volumes. More than 70% of major diagnostic networks have implemented digital laboratory management platforms, creating favorable conditions for connected dry chemistry analyzers. Domestic innovation activity and procurement modernization continue supporting sustained deployment across hospitals and reference laboratories.

Quality Compliance and Digital Modernization Reshaping Demand

Europe remains a strategically important market driven by stringent laboratory quality standards, healthcare modernization programs, and widespread adoption of automated diagnostic workflows. The region contributes approximately 28% of global market activity, supported by strong deployment across public healthcare systems and specialized diagnostic centers. Digital laboratory transformation initiatives have increased analyzer integration rates by nearly 20% in several countries. Sustainability objectives are also influencing procurement decisions, encouraging adoption of energy-efficient analyzer platforms and optimized reagent utilization systems. Manufacturers are strengthening regional service networks and expanding compliance-focused product portfolios.

Germany Market Outlook: Germany leads the European market through its extensive diagnostic infrastructure, advanced healthcare technology ecosystem, and strong laboratory automation culture. Clinical laboratories continue upgrading testing platforms to improve operational throughput and quality assurance performance. More than 60% of large diagnostic facilities utilize advanced automated chemistry workflows. The country’s strong medical technology manufacturing base and emphasis on precision diagnostics support continued adoption of next-generation dry chemistry analyzers across healthcare institutions.

Healthcare Infrastructure Expansion Accelerates Deployment

Asia-Pacific is emerging as the fastest-expanding market due to large-scale healthcare investments, expanding diagnostic access, and increasing domestic manufacturing capabilities. The region accounts for nearly 25% of global market participation and records the highest deployment growth across hospitals, clinics, and decentralized testing facilities. Healthcare infrastructure projects have increased diagnostic equipment procurement by more than 20% in several key markets. Growing adoption of portable and point-of-care analyzers is reshaping testing models, particularly in underserved areas. Manufacturers are expanding production facilities and strengthening local distribution partnerships to capture rising demand.

China Market Outlook: China represents the most influential market within Asia-Pacific due to its extensive hospital network, domestic diagnostic manufacturing ecosystem, and healthcare modernization initiatives. Public and private healthcare providers are accelerating deployment of automated laboratory technologies to improve testing efficiency. Domestic manufacturers continue increasing production capacity while expanding technology capabilities. More than half of newly upgraded tertiary hospitals are incorporating advanced chemistry testing systems, supporting broader adoption of high-performance dry chemistry analyzers across the healthcare sector.

Diagnostic Access Expansion Supporting Adoption

South America is witnessing steady market development as healthcare providers expand diagnostic capabilities and improve access to laboratory services. The region contributes approximately 6% of global market demand, with adoption concentrated in major urban healthcare centers. Investments in hospital modernization and laboratory efficiency initiatives have increased deployment of automated analyzers by nearly 15% across leading healthcare networks. However, infrastructure disparities and procurement budget constraints continue influencing purchasing cycles. Companies are addressing these limitations through distributor partnerships, localized support services, and flexible equipment acquisition models.

Brazil Market Outlook: Brazil dominates the regional market due to its large healthcare sector, expanding diagnostic laboratory network, and increasing focus on preventive healthcare services. Private laboratory operators are investing in workflow automation and testing capacity expansion to meet growing demand. Diagnostic consolidation trends are encouraging procurement of scalable analyzer platforms capable of supporting high sample volumes. The country's broad healthcare footprint and ongoing laboratory modernization efforts continue creating opportunities for advanced dry chemistry analyzer deployment.

Healthcare Investment Programs Driving Transformation

The Middle East & Africa market is advancing through healthcare infrastructure expansion, hospital development projects, and increasing investment in diagnostic modernization. The region accounts for approximately 5% of global market activity, with deployment concentrated in major healthcare hubs. Government-backed healthcare transformation initiatives have accelerated procurement of advanced diagnostic equipment, while laboratory automation adoption has increased by nearly 12% in selected healthcare systems. Companies are strengthening regional distribution networks and establishing technical support capabilities to improve deployment effectiveness and equipment utilization.

Saudi Arabia Market Outlook: Saudi Arabia represents the leading market within the region due to substantial healthcare investment, hospital expansion projects, and ongoing digital health transformation initiatives. Healthcare providers are prioritizing advanced diagnostic technologies to improve testing quality and operational efficiency. Large healthcare facilities continue implementing automated laboratory workflows, supporting broader analyzer deployment. Strategic investments in healthcare infrastructure and technology integration are strengthening the country's position as a key destination for advanced diagnostic equipment providers.

The Dry Chemistry Analyzer Market is led by Fujifilm, Arkray, IDEXX Laboratories, Randox Laboratories, Siemens Healthineers, and Roche Diagnostics, with global technology leaders competing against regional diagnostic equipment manufacturers and cost-focused suppliers. The top five players collectively account for approximately 48% of market share. Competition centers on automation capability, analyzer throughput, consumable efficiency, digital connectivity, and service responsiveness. Advanced platforms deliver nearly 20% faster processing speeds and around 15% lower reagent consumption, creating a clear differentiation advantage. Global leaders compete through product innovation, laboratory integration software, and long-term healthcare partnerships, while regional participants focus on pricing flexibility and localized service networks. Vertical integration of consumables and analyzer systems is becoming increasingly important as supply-chain stability influences procurement decisions. The competitive landscape is shifting toward AI-enabled workflow management and connected diagnostics ecosystems. Strong regulatory requirements, validation costs, and service infrastructure investments remain significant entry barriers. Success increasingly depends on combining automation, interoperability, reliable supply, and clinical workflow integration.

Fujifilm Corporation

Arkray Inc.

IDEXX Laboratories Inc.

Randox Laboratories Ltd.

Siemens Healthineers AG

Roche Diagnostics

Beckman Coulter Inc.

Mindray Medical International Limited

Nova Biomedical Corporation

Erba Mannheim

Sysmex Corporation

Werfen S.A.

EKF Diagnostics Holdings plc

Awareness Technology Inc.

Current technology leadership is centered on fully automated dry chemistry analyzers with integrated optics, automated sample handling, and digital quality control systems. These platforms improve laboratory throughput by approximately 20% while reducing reagent waste by nearly 15% compared with conventional chemistry workflows. More than 60% of newly installed analyzers in large hospital laboratories now incorporate automated calibration and workflow management capabilities. The business impact is significant: laboratories process higher testing volumes with fewer manual interventions, improving operational efficiency and reducing staffing pressure in high-demand diagnostic environments.

Emerging technologies are focused on AI-assisted diagnostics, cloud-connected analyzers, and predictive maintenance platforms. AI-enabled quality control tools reduce manual verification workloads by around 18%, while remote monitoring systems improve equipment uptime by nearly 12%. Adoption of connected diagnostic platforms has surpassed 35% among advanced laboratory networks. Companies deploying integrated analyzer ecosystems gain stronger service differentiation, faster troubleshooting, and improved utilization rates. Strategic partnerships between diagnostics manufacturers and healthcare software providers are accelerating integration across laboratory information systems and decentralized testing environments.

Disruptive innovation is shifting toward compact multi-parameter analyzers, edge-based analytics, and point-of-care dry chemistry platforms. Compared with legacy semi-automated systems, next-generation analyzers deliver approximately 25% faster processing speeds and 20% lower operating costs. Between 2026 and 2028, deployment of AI-supported and decentralized testing systems is expected to expand significantly. Technology leaders with advanced automation, interoperability, and digital service capabilities are positioned to secure competitive advantages as healthcare providers prioritize scalable, data-driven diagnostic infrastructure.

June 2025 – IDEXX Laboratories launched the Catalyst Cortisol Test, the third Catalyst platform expansion within one year. The rollout targets an installed base exceeding 75,000 Catalyst chemistry analyzers, strengthening point-of-care endocrine diagnostics and expanding recurring consumable utilization across veterinary practices. Source: IDEXX Laboratories, Inc.

July 2025 – Fapon introduced the Shine mT8000 fully automated clinical chemistry and immunoassay system at ADLM 2025. The platform delivers throughput density of 735 tests per hour, enabling laboratories to increase output while minimizing footprint requirements and operational complexity.

October 2025 – FUJIFILM India launched the FW500 Clinical Chemistry Analyzer featuring capacity for 200 tests per hour, 95 sample positions, and 72 reagent positions. The expansion strengthens mid-sized laboratory automation capabilities and broadens the company’s diagnostics portfolio presence in India.

November 2025 – Randox Laboratories showcased the RABTA random-access analyzer at MEDICA 2025, capable of delivering up to 44 results from a single sample and processing 60 samples per hour. The innovation improves workflow continuity and productivity for high-volume diagnostic laboratories. Source:abmedica.com

This report provides a comprehensive assessment of the Dry Chemistry Analyzer Market across major product categories, including Benchtop Analyzers, Portable Analyzers, Fully Automated Analyzers, Semi-Automated Analyzers, and Point-of-Care Analyzers. The analysis covers key applications such as Clinical Diagnostics, Blood Chemistry Testing, Disease Screening, Emergency Testing, and Veterinary Diagnostics, alongside detailed evaluation of hospitals, diagnostic laboratories, clinics, research institutes, veterinary centers, and ambulatory care centers. More than 60% of current market activity is concentrated in automated and digitally integrated testing environments, highlighting a clear technology transition underway.

The study delivers region-wise intelligence across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, while examining adoption patterns, deployment strategies, competitive positioning, and innovation pipelines. Coverage includes AI-enabled diagnostics, cloud-connected laboratory systems, workflow automation, decentralized testing models, and emerging point-of-care opportunities. The report supports investment evaluation, expansion planning, product strategy development, partnership decisions, and competitive benchmarking by identifying operational priorities and technology shifts expected to shape market direction between 2026 and 2033.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 3070 Million |

|

Market Revenue in 2033 |

USD 5334.27 Million |

|

CAGR (2026 - 2033) |

7.15% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Fujifilm Corporation, Arkray Inc., IDEXX Laboratories Inc., Randox Laboratories Ltd., Siemens Healthineers AG, Roche Diagnostics, Beckman Coulter Inc., Mindray Medical International Limited, Nova Biomedical Corporation, Erba Mannheim, Sysmex Corporation, Werfen S.A., EKF Diagnostics Holdings plc, Awareness Technology Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |