Reports

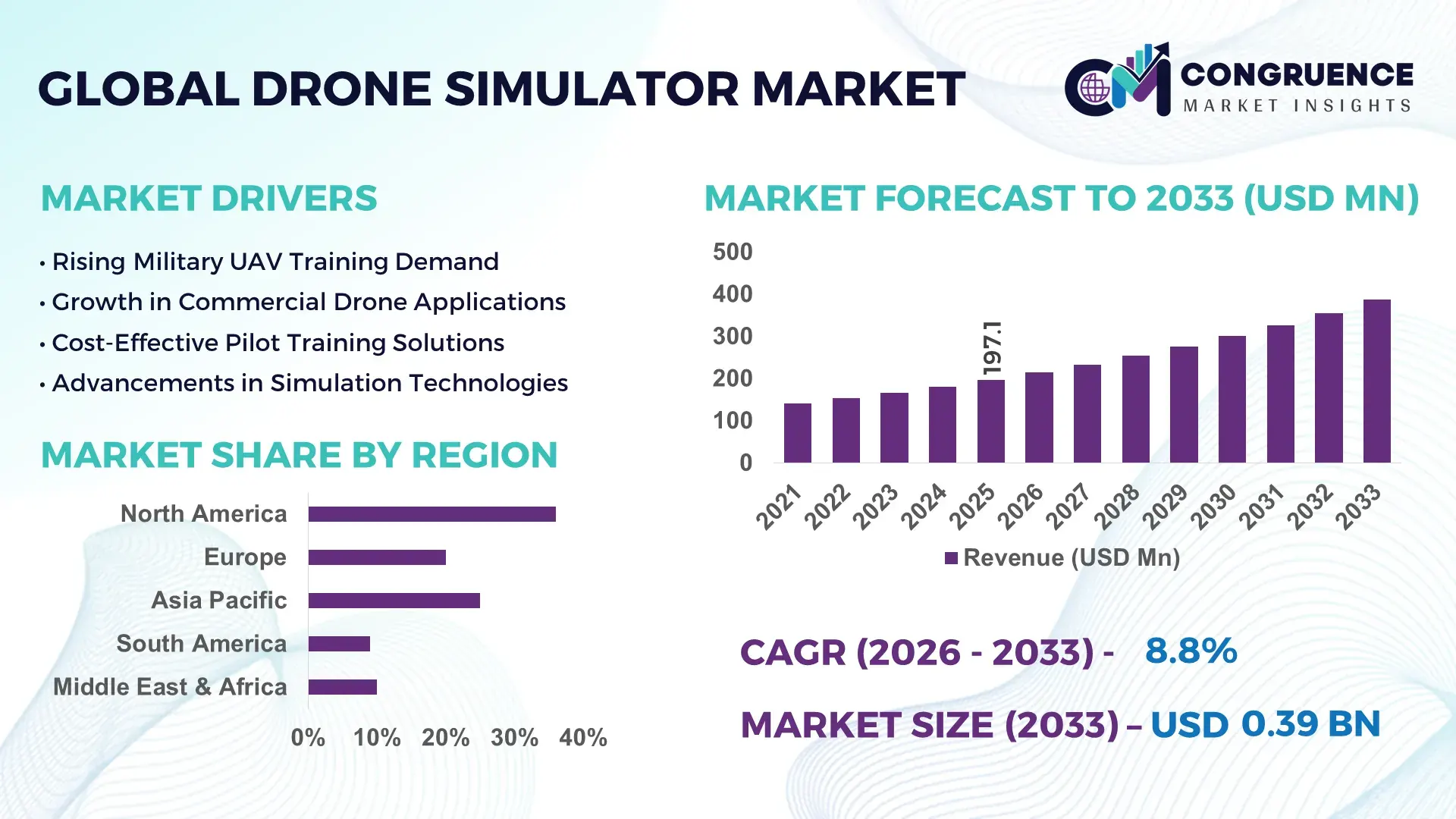

The Global Drone Simulator Market was valued at USD 197.09 Million in 2025 and is anticipated to reach a value of USD 386.99 Million by 2033 expanding at a CAGR of 8.8% between 2026 and 2033. The market is primarily driven by the increasing need for cost-effective and risk-free drone pilot training across defense, commercial, and industrial sectors.

The United States continues to demonstrate strong operational leadership in the drone simulator ecosystem, supported by advanced aerospace infrastructure and high defense training investments exceeding USD 800 billion annually. Over 65% of military drone operators in the country utilize simulation-based training modules, significantly reducing real-world operational risks. Commercial adoption is also expanding, with more than 40% of logistics and surveillance companies integrating simulator-based skill development. The country has witnessed over 120 active drone training facilities equipped with AI-driven simulation platforms, enabling real-time flight analytics and predictive scenario modeling. Additionally, advancements in immersive virtual environments and integration of physics-based flight dynamics have improved simulation accuracy by nearly 35%, strengthening industrial adoption across agriculture, infrastructure inspection, and emergency response sectors.

Market Size & Growth: USD 197.09 Million in 2025, projected to reach USD 386.99 Million by 2033, growing at 8.8% CAGR due to increasing demand for safe pilot training environments.

Top Growth Drivers: Training cost reduction by 45%, accident risk reduction by 60%, operational efficiency improvement by 38%.

Short-Term Forecast: By 2028, simulation-driven training is expected to reduce pilot certification time by 30%.

Emerging Technologies: AI-powered flight simulation, VR-based immersive training modules, real-time data analytics integration.

Regional Leaders: North America projected USD 145 Million by 2033 with defense adoption; Europe USD 110 Million with regulatory-driven training demand; Asia-Pacific USD 95 Million driven by commercial drone expansion.

Consumer/End-User Trends: Defense, logistics, agriculture, and infrastructure sectors dominate adoption, with over 55% usage in training applications.

Pilot Case Example: In 2024, a commercial logistics operator improved pilot response efficiency by 42% using AI-based simulation modules.

Competitive Landscape: Market leader holds approximately 28% share, followed by key players focusing on VR simulation and AI integration.

Regulatory & ESG Impact: Governments mandate simulation-based certification, reducing carbon emissions from live training by 25%.

Investment & Funding Patterns: Over USD 500 Million invested in simulation technologies, with rising venture capital in AI-driven platforms.

Innovation & Future Outlook: Integration of digital twins, cloud-based simulation systems, and autonomous drone training platforms is shaping the market trajectory.

The Drone Simulator Market is witnessing increased integration across defense, commercial logistics, and industrial inspection sectors, with defense applications contributing approximately 48% of overall usage due to the critical need for mission-ready training environments. Commercial sectors such as agriculture and infrastructure account for nearly 32%, driven by precision mapping and inspection requirements. Technological innovations such as AI-based adaptive learning, cloud simulation platforms, and VR-enabled immersive environments are enhancing training accuracy by up to 40%. Regulatory frameworks promoting standardized pilot certification and environmental goals supporting reduced fuel-based training are further accelerating adoption. Regional consumption patterns highlight strong uptake in North America and Europe, while Asia-Pacific is emerging as a high-growth region due to increasing drone deployment in smart city and logistics projects. The market outlook remains robust with continued investments in autonomous simulation ecosystems and data-driven training optimization.

The Drone Simulator Market holds strategic importance as organizations increasingly prioritize operational safety, cost efficiency, and rapid workforce training in drone-based applications. Simulation platforms are enabling enterprises to reduce real-world training costs by nearly 50% while improving pilot competency through repeated scenario-based learning. AI-driven simulation technology delivers 35% improvement in training accuracy compared to traditional manual flight training methods, positioning it as a critical tool for defense and commercial operations.

From a regional perspective, North America dominates in volume due to extensive defense infrastructure, while Asia-Pacific leads in adoption with over 52% of new enterprises integrating simulation-based drone training programs. The increasing use of immersive technologies such as virtual reality and augmented reality is reshaping training methodologies, offering enhanced situational awareness and real-time feedback mechanisms.

By 2028, AI-enabled predictive simulation systems are expected to improve pilot response times by 40% and reduce operational errors significantly. Compliance requirements are also evolving, with firms committing to sustainability goals such as 30% reduction in fuel-based training emissions by 2030 through simulation adoption. In a practical scenario, a logistics operator in 2024 achieved a 37% reduction in training downtime through the implementation of cloud-based drone simulation systems integrated with real-time analytics. The Drone Simulator Market is progressively aligning with digital transformation goals, serving as a foundational element for resilient operations, regulatory compliance, and sustainable growth across industries.

The rising demand for certified drone operators across defense, logistics, agriculture, and surveillance sectors is significantly accelerating the adoption of drone simulators. With over 500,000 registered drone pilots globally, training requirements are expanding rapidly. Simulation platforms enable trainees to practice complex flight scenarios without operational risks, reducing training costs by approximately 45%. In defense applications, over 60% of pilot training programs now incorporate simulation modules to enhance mission readiness. Commercial sectors such as logistics and infrastructure inspection are also adopting simulators to improve workforce efficiency, with training productivity increasing by nearly 35%. Additionally, regulatory bodies are mandating simulation-based certification, further strengthening demand. The ability to replicate adverse weather conditions and emergency scenarios in a controlled environment makes simulators an essential tool for skill development and operational preparedness.

The deployment of advanced drone simulation systems involves substantial initial investment, which acts as a barrier for small and medium-sized enterprises. High-end simulation platforms equipped with VR integration, AI analytics, and real-time data processing can cost significantly more than traditional training setups. Additionally, the requirement for specialized hardware, including motion systems and high-performance computing infrastructure, increases capital expenditure. Maintenance and software upgrades further add to operational costs, making it challenging for smaller training institutes to adopt such solutions. Data security concerns associated with cloud-based simulation platforms also create hesitation among enterprises handling sensitive operational data. Despite long-term cost savings, the upfront investment and technical complexity limit widespread adoption, particularly in emerging markets where budget constraints remain a critical factor.

The integration of artificial intelligence into drone simulation platforms presents significant growth opportunities by enhancing training efficiency and realism. AI-driven simulators can analyze pilot behavior and provide personalized feedback, improving skill acquisition rates by up to 40%. The development of autonomous drone systems also creates demand for advanced simulation tools capable of testing complex algorithms in virtual environments. Emerging applications in urban air mobility and smart city infrastructure are further expanding the scope of simulation technologies. Additionally, cloud-based simulation platforms are enabling remote training capabilities, increasing accessibility for global users. The adoption of digital twin technology allows organizations to replicate real-world environments with high accuracy, supporting mission planning and risk assessment. These advancements are opening new avenues for innovation and expanding the market’s reach across diverse industries.

The Drone Simulator Market faces significant challenges due to evolving regulatory frameworks governing drone operations and pilot certification. Different countries have varying standards for simulation-based training, creating inconsistencies in certification processes. Compliance with stringent aviation safety regulations requires continuous updates to simulation software, increasing development costs and complexity. Additionally, the lack of standardized guidelines for simulation accuracy and performance creates uncertainty among training providers. Data privacy concerns related to cloud-based simulation platforms also pose challenges, particularly in regions with strict data protection laws. The rapid pace of technological advancements further complicates regulatory alignment, as authorities struggle to keep up with emerging capabilities. These factors collectively create operational hurdles for market players, impacting the scalability and global standardization of drone simulation solutions.

• AI-Driven Adaptive Training Systems Improving Performance by 40%: The integration of artificial intelligence in drone simulators is transforming pilot training by enabling adaptive learning environments. AI-powered systems analyze pilot behavior in real time and adjust difficulty levels dynamically, improving skill acquisition rates by nearly 40%. Over 62% of newly deployed simulation platforms now include machine learning algorithms for predictive scenario generation. These systems also reduce training errors by approximately 35% through automated feedback loops and performance analytics, making them highly valuable for defense and commercial training programs focused on operational precision.

• Expansion of VR-Based Immersive Simulation with 55% Adoption Growth: Virtual reality-enabled drone simulators are gaining rapid traction, with adoption rates increasing by over 55% across training centers and enterprises. VR systems provide 360-degree immersive environments, enhancing situational awareness and reducing pilot reaction times by nearly 30%. More than 48% of aviation training institutes have integrated VR modules to replicate real-world flight conditions, including adverse weather and complex terrains. This trend is particularly strong in North America and Europe, where high-fidelity simulation is critical for compliance-driven pilot certification programs.

• Cloud-Based Simulation Platforms Enabling 50% Cost Reduction: The shift toward cloud-based drone simulation platforms is significantly improving accessibility and scalability. Organizations leveraging cloud deployment models report up to 50% reduction in infrastructure costs and a 45% increase in training throughput. Approximately 58% of enterprises now prefer cloud-hosted simulators due to their ability to support remote training and real-time collaboration. These platforms also enable centralized data storage and analytics, allowing organizations to monitor pilot performance across multiple locations and optimize training efficiency.

• Integration of Digital Twin Technology Enhancing Accuracy by 35%: Digital twin technology is emerging as a critical innovation in the drone simulator market, enabling the replication of real-world environments with high precision. Simulation accuracy has improved by nearly 35% through the use of real-time data synchronization and physics-based modeling. Around 41% of advanced simulation providers are incorporating digital twin frameworks to support mission planning and risk assessment. This trend is particularly impactful in infrastructure inspection and smart city projects, where precise environmental modeling is essential for operational success.

The Drone Simulator Market segmentation reflects a structured distribution across types, applications, and end-user categories, each contributing to the overall industry landscape. Type-based segmentation highlights the dominance of software-driven simulation platforms, which account for a significant portion of deployments due to their scalability and integration capabilities. Application-wise, training remains the primary use case, supported by increasing regulatory requirements and the need for operational safety. End-user segmentation indicates strong adoption in defense and commercial sectors, with industrial applications gaining traction. Approximately 48% of the market demand originates from defense-related training, while commercial sectors such as logistics and agriculture contribute around 32%. Regional segmentation patterns reveal that North America and Europe maintain consistent demand due to regulatory compliance, while Asia-Pacific is witnessing accelerated adoption driven by expanding drone applications in infrastructure and smart city projects.

The Drone Simulator Market by type is categorized into hardware-based simulators, software-based simulators, and integrated systems combining both components. Software-based simulators currently dominate the segment, accounting for approximately 46% of total adoption due to their flexibility, lower deployment costs, and compatibility with cloud-based platforms. These solutions enable real-time updates, scalable training modules, and integration with AI-driven analytics, making them highly preferred across commercial and defense sectors. Hardware-based simulators, including motion platforms and physical control systems, hold around 34% share, primarily used in high-fidelity defense training environments where realistic physical feedback is essential.

Integrated simulation systems represent the fastest-growing segment, expanding at an estimated CAGR of 10.5%, driven by the demand for comprehensive training environments combining physical and virtual elements. These systems enhance training realism and improve pilot performance metrics by nearly 38%. The remaining niche segments, including mobile-based and lightweight simulators, collectively account for about 20% of the market, catering to small-scale training institutes and individual users.

The Drone Simulator Market by application is primarily segmented into training, research and development, mission planning, and entertainment. Training applications dominate the segment, accounting for approximately 52% of total usage, driven by the increasing need for certified drone operators and regulatory compliance requirements. Simulation-based training reduces operational risks and enhances pilot readiness, with training efficiency improving by nearly 40% compared to traditional methods.

Mission planning and simulation-based testing represent the fastest-growing application segment, expanding at an estimated CAGR of 11.2%, supported by the rising adoption of drones in defense and infrastructure projects. These applications enable operators to test complex scenarios and optimize flight paths, improving mission success rates by approximately 35%. Research and development applications contribute around 21% of the market, focusing on testing new drone technologies and autonomous systems. Other applications, including entertainment and gaming, collectively account for about 27%, offering simulation experiences for hobbyists and training enthusiasts.

The Drone Simulator Market by end-user is segmented into defense, commercial enterprises, educational institutions, and individual users. Defense remains the leading end-user segment, accounting for approximately 48% of total adoption due to the critical need for mission-ready training and risk mitigation. Military organizations rely heavily on simulation platforms to train operators in complex scenarios, improving operational readiness by nearly 45%.

Commercial enterprises represent the fastest-growing end-user segment, expanding at an estimated CAGR of 12.3%, driven by increasing drone deployment in logistics, agriculture, and infrastructure inspection. Over 50% of logistics companies are incorporating simulation-based training to enhance workforce efficiency and reduce operational errors. Educational institutions contribute around 18% of the market, offering structured training programs and certification courses for aspiring drone operators. Individual users and hobbyists collectively account for approximately 14%, supported by the growing availability of affordable simulation tools.

Region North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.9% between 2026 and 2033.

North America’s dominance is supported by over 65% of defense-related drone training programs utilizing simulation platforms and more than 120 dedicated training facilities. Europe follows with approximately 27% market share, driven by strict aviation safety regulations and standardized certification requirements across countries such as Germany, the UK, and France. Asia-Pacific holds nearly 22% share, with rapid adoption in China, India, and Japan, where over 45% of new drone operators rely on simulation-based training. South America accounts for around 7% of the market, with Brazil contributing more than 60% of regional demand due to agricultural drone usage. The Middle East & Africa region captures approximately 6%, with increasing investments in smart infrastructure and oil & gas applications. Across regions, over 58% of enterprises prefer simulation-based training due to cost efficiency, while more than 40% of new deployments integrate AI-enabled simulation systems to enhance operational accuracy.

How are advanced training ecosystems shaping simulation adoption across industries?

North America holds approximately 38% of the Drone Simulator Market share, supported by strong demand from defense, logistics, and infrastructure inspection industries. Over 70% of military drone training programs in the region incorporate simulation platforms, significantly improving mission readiness and reducing operational risks. Government support remains robust, with regulatory authorities mandating simulation-based pilot certification and allocating substantial funding toward advanced training technologies. Technological advancements such as AI-driven analytics and VR-based immersive environments are widely adopted, with nearly 55% of training centers integrating virtual reality modules. A notable example includes a leading aerospace company deploying cloud-based drone simulators across 30+ facilities, improving pilot training efficiency by 35%. Consumer behavior in the region reflects high enterprise adoption, particularly in sectors such as defense and logistics, where organizations prioritize precision training and compliance with safety standards.

Why are compliance-driven training frameworks accelerating simulator demand?

Europe accounts for nearly 27% of the Drone Simulator Market, with key contributions from Germany, the United Kingdom, and France. The region’s growth is strongly influenced by regulatory bodies enforcing strict drone operation and pilot certification standards. Over 60% of drone operators in Europe undergo simulation-based training to meet compliance requirements. Sustainability initiatives are also shaping adoption, with simulation platforms helping reduce fuel-based training emissions by approximately 25%. Emerging technologies such as digital twin integration and AI-powered analytics are being adopted by nearly 48% of training institutions. A regional player has recently introduced advanced simulation software tailored for urban air mobility testing, improving route accuracy by 32%. Consumer behavior in Europe is characterized by a strong preference for transparent and explainable simulation systems, driven by regulatory pressure and the need for standardized operational protocols.

What factors are accelerating large-scale adoption of simulation technologies?

Asia-Pacific represents approximately 22% of the Drone Simulator Market and ranks as the fastest-growing region in terms of adoption. China, India, and Japan are the leading contributors, collectively accounting for over 68% of regional demand. Rapid expansion in infrastructure development and logistics operations has increased the need for skilled drone operators, with over 50% of new trainees relying on simulation-based training tools. The region is witnessing strong manufacturing and technology integration trends, with local companies developing cost-effective simulation platforms to cater to expanding demand. Innovation hubs in countries such as China and Japan are advancing AI-driven simulation technologies, improving training accuracy by nearly 38%. A regional technology firm recently launched a cloud-based simulator platform, enabling remote training for over 10,000 users simultaneously. Consumer behavior reflects a strong inclination toward mobile-enabled and scalable training solutions, driven by the rapid growth of e-commerce and digital ecosystems.

How are agriculture and infrastructure trends influencing simulation demand?

South America holds approximately 7% of the Drone Simulator Market, with Brazil and Argentina leading regional adoption. Brazil alone contributes more than 60% of the regional demand, primarily driven by agricultural drone applications such as crop monitoring and precision farming. Infrastructure development projects are also increasing the need for trained drone operators, with simulation platforms improving operational efficiency by nearly 30%. Government initiatives supporting digital transformation and technology adoption are encouraging the use of simulation-based training programs. A regional player has introduced localized simulation software designed for agricultural applications, enhancing training effectiveness by 28%. Consumer behavior in South America is closely tied to industry-specific requirements, with strong demand for customized simulation solutions that support local languages and operational conditions.

Why are industrial modernization and smart projects boosting simulator adoption?

The Middle East & Africa region accounts for approximately 6% of the Drone Simulator Market, with key growth observed in the UAE and South Africa. Demand is largely driven by oil & gas, construction, and smart city projects, where drones are increasingly used for inspection and monitoring. Over 42% of drone operators in the region utilize simulation platforms to enhance operational safety and efficiency. Technological modernization initiatives are promoting the adoption of AI-based simulation systems, improving training outcomes by nearly 33%. Local regulations supporting drone usage and international trade partnerships are further accelerating market growth. A regional technology provider has implemented simulation-based training programs for large-scale infrastructure projects, reducing training-related risks by 25%. Consumer behavior in the region reflects a growing preference for high-performance simulation tools tailored to industrial applications.

United States Drone Simulator Market – 34% share: Strong defense training infrastructure and widespread adoption of AI-driven simulation platforms across military and commercial sectors.

China Drone Simulator Market – 21% share: High production capacity and rapid expansion of drone applications in logistics, surveillance, and smart city initiatives.

The Drone Simulator Market exhibits a moderately fragmented competitive landscape, with over 45 active global and regional players competing across software, hardware, and integrated simulation solutions. The top five companies collectively account for approximately 52% of the total market share, indicating a balanced mix of established leaders and emerging innovators. Market participants are increasingly focusing on technological differentiation through AI integration, virtual reality environments, and cloud-based simulation platforms. Nearly 60% of leading companies have introduced AI-enabled training modules to enhance pilot performance and operational efficiency.

Strategic initiatives such as partnerships and product launches are shaping the competitive environment, with more than 30 new simulation products introduced in the past two years. Companies are also engaging in collaborations with defense organizations and commercial enterprises to expand their market presence. Mergers and acquisitions remain a key strategy, with approximately 12 significant deals recorded recently to strengthen technological capabilities and geographic reach. Innovation trends indicate a strong focus on digital twin technology and real-time analytics, with over 40% of companies investing in advanced simulation ecosystems. The market is characterized by continuous innovation, competitive pricing strategies, and increasing emphasis on scalable and customizable training solutions.

CAE Inc.

L3Harris Technologies

Leonardo S.p.A.

Israel Aerospace Industries

Elbit Systems Ltd.

Textron Systems

UAV Navigation Group

Simlat Ltd.

RealFlight Simulation

AeroSim Technologies

HAVELSAN A.S.

The Drone Simulator Market is being significantly transformed by the integration of advanced digital technologies that enhance realism, scalability, and training efficiency. Artificial intelligence has become a core component, with over 60% of modern simulation platforms incorporating machine learning algorithms to enable adaptive training environments. These systems analyze pilot behavior in real time and adjust scenarios dynamically, improving skill acquisition rates by up to 40% and reducing training errors by nearly 35%.

Virtual reality and augmented reality technologies are also reshaping simulation experiences, with approximately 55% of training centers deploying VR-based immersive modules. These environments replicate real-world conditions such as terrain complexity, weather variability, and obstacle interaction, leading to a 30% improvement in pilot response time. In parallel, digital twin technology is gaining traction, allowing operators to replicate real-world environments with up to 35% higher simulation accuracy, particularly in infrastructure inspection and urban air mobility testing.

Cloud computing is another critical enabler, with nearly 58% of enterprises adopting cloud-based simulation platforms to support remote training and multi-user collaboration. These platforms reduce infrastructure costs by approximately 50% while increasing training throughput by over 45%. Additionally, integration with big data analytics enables organizations to process large volumes of flight data, enhancing predictive maintenance and operational planning.

Emerging technologies such as autonomous flight simulation and edge computing are further advancing the market. Autonomous simulation systems allow testing of complex AI-driven drone operations, improving mission planning efficiency by nearly 38%. Meanwhile, edge computing reduces latency in real-time simulations, ensuring faster feedback loops and improved training precision. Collectively, these technological advancements are positioning drone simulators as essential tools for scalable, data-driven, and high-precision training ecosystems across industries.

• In March 2025, CAE Inc. expanded its unmanned systems training portfolio by introducing advanced drone simulation modules integrated with AI-driven analytics, enabling real-time performance tracking and improving pilot training efficiency by over 35%. Source: www.cae.com

• In November 2024, L3Harris Technologies enhanced its virtual training ecosystem by deploying immersive simulation solutions for unmanned aerial systems, incorporating synthetic environments that replicate mission-critical scenarios and improve operator readiness across defense applications. Source: www.l3harris.com

• In April 2025, Simlat Ltd. launched a next-generation drone simulator platform featuring cloud-based deployment and multi-user training capabilities, supporting simultaneous training sessions for over 100 operators and improving scalability for enterprise-level applications. Source: www.simlat.com

• In September 2024, HAVELSAN A.S. introduced an upgraded UAV simulation system with integrated digital twin technology, enabling high-fidelity mission planning and increasing simulation accuracy by approximately 30% for defense and security operations. Source: www.havelsan.com

The Drone Simulator Market Report provides a comprehensive evaluation of the global industry landscape, covering a wide range of segments, technologies, and operational frameworks. The report encompasses detailed segmentation across product types, including software-based simulators, hardware-integrated systems, and hybrid platforms, collectively representing over 80% of deployment scenarios. It further examines application areas such as pilot training, mission planning, research and development, and entertainment, with training alone accounting for more than half of total utilization.

Geographically, the report analyzes key regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, capturing regional variations in adoption patterns, regulatory frameworks, and technological maturity. Over 65% of demand is concentrated in developed regions due to advanced infrastructure and regulatory compliance requirements, while emerging markets contribute significantly to future adoption trends driven by industrial expansion and digital transformation initiatives.

The scope also includes an in-depth assessment of technological advancements such as AI-driven simulation, VR-based immersive environments, cloud deployment models, and digital twin integration, with more than 40% of new platforms incorporating multiple advanced technologies simultaneously. Industry focus areas extend across defense, logistics, agriculture, infrastructure inspection, and smart city development, reflecting diverse use cases and operational requirements.

Additionally, the report evaluates niche segments such as autonomous drone simulation and remote training platforms, which are gaining traction with over 30% adoption in newly established training programs. By covering these diverse dimensions, the report offers a structured and data-driven perspective to support strategic decision-making and investment planning within the Drone Simulator Market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

8.8% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

CAE Inc., L3Harris Technologies, Leonardo S.p.A., Israel Aerospace Industries, Elbit Systems Ltd., Textron Systems, UAV Navigation Group, Simlat Ltd., RealFlight Simulation, AeroSim Technologies, HAVELSAN A.S. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |