Reports

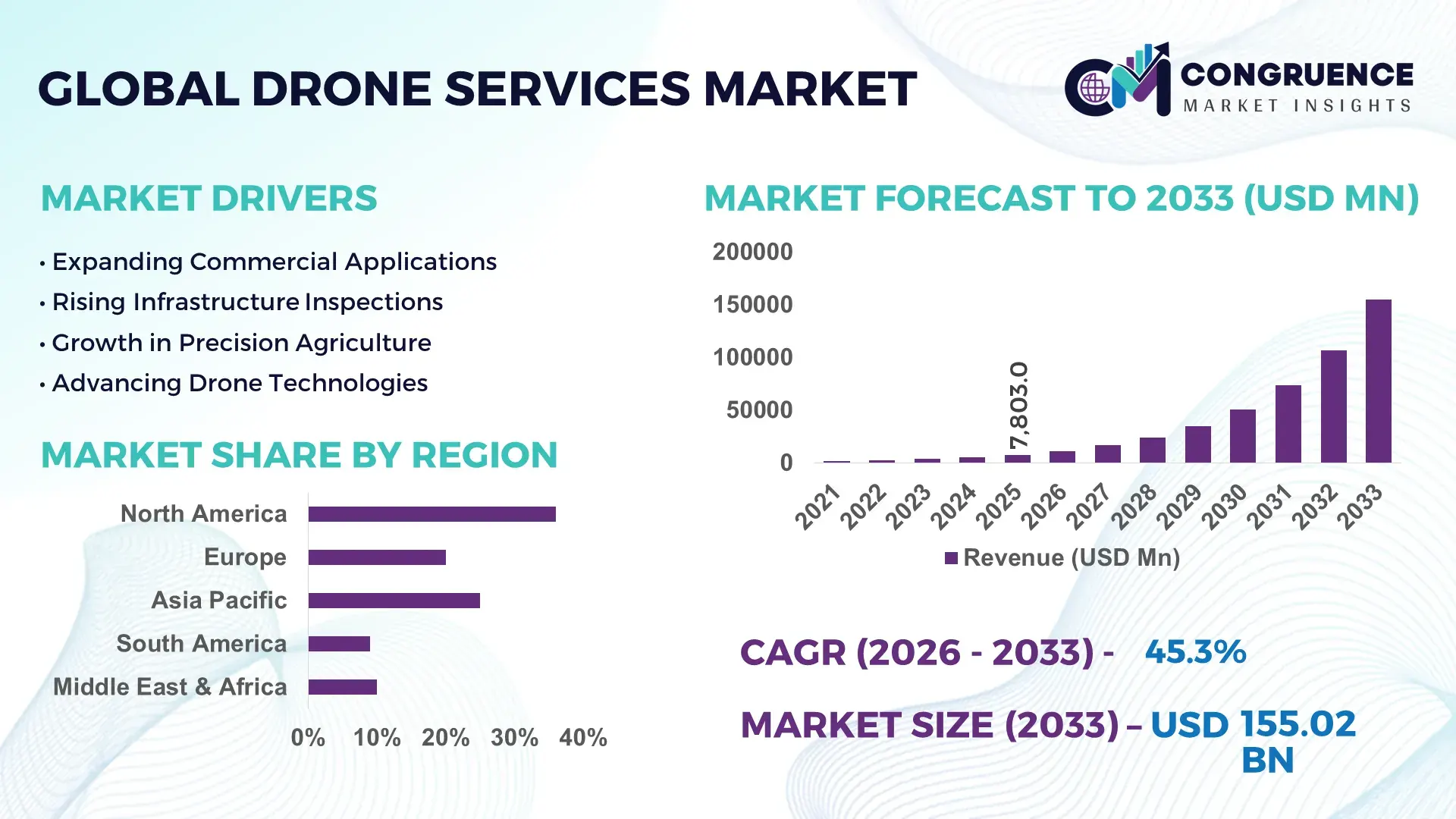

The Global Drone Services Market was valued at USD 7803.02 Million in 2025 and is anticipated to reach a value of USD 155020.13 Million by 2033 expanding at a CAGR of 45.3% between 2026 and 2033. Growth is accelerating through industrial inspection automation, precision agriculture deployment, defense-border surveillance programs, and AI-enabled aerial analytics that reduce field inspection time by over 60% across energy, mining, and infrastructure operations.

The United States dominates the advanced drone services ecosystem with approximately 34% global market share, supported by over USD 6 billion in federal and private-sector UAV modernization programs across logistics, defense, and utility inspection networks in 2026. China leads manufacturing scale with more than 70% commercial drone production capacity, while India is emerging rapidly through agriculture mapping and public infrastructure monitoring initiatives under expanded domestic drone policy reforms. Cross-border security tensions and Red Sea logistics disruptions accelerated autonomous aerial surveillance investments by nearly 28% across energy corridors and ports, strengthening enterprise adoption of high-end drone analytics platforms.

Companies prioritizing AI-integrated drone fleets, localized compliance infrastructure, and high-frequency industrial inspection contracts are positioned to secure long-term operational advantage in the high-growth global drone services market.

Market Size & Growth: USD 7803.02 Million in 2025 rising to USD 155020.13 Million by 2033 at 45.3% growth, driven by AI-enabled industrial inspection and autonomous aerial analytics adoption.

Top Growth Drivers: Precision agriculture deployment up 31%, energy infrastructure inspections up 27%, and defense surveillance integration expanding 35% globally during 2026.

Short-Term Forecast: By 2027, drone-based asset inspections will reduce operational downtime by 42% and lower manual survey costs by nearly 38% across utilities and mining.

Emerging Technologies: AI navigation systems, edge-computing drones, and BVLOS operations improve mission efficiency by 46% while increasing autonomous flight accuracy above 92%.

Regional Leaders: North America exceeds USD 28 billion through defense digitization, Asia-Pacific crosses USD 40 billion via manufacturing expansion, and Europe surpasses USD 19 billion through ESG-led infrastructure monitoring.

Consumer/End-User Trends: Nearly 58% of large construction and energy firms now integrate advanced drone services into predictive maintenance and site-mapping operations.

Pilot/Case Example: In 2026, automated offshore drone inspections in the Gulf region reduced hazardous human exposure by 49% and improved maintenance response speed by 33%.

Competitive Landscape: DJI maintains roughly 43% ecosystem influence, while AeroVironment, Parrot, Terra Drone, and Cyberhawk expand industrial drone service contracts globally.

Regulatory & ESG Impact: Updated BVLOS approvals and low-emission inspection mandates improved operational coverage by 36% across critical infrastructure and renewable energy sectors.

Investment & Funding: Global drone ecosystem investments exceeded USD 14 billion in 2026, fueled by defense partnerships, logistics automation, and regional supply-chain diversification strategies.

Innovation & Future Outlook: Autonomous drone swarms, hydrogen-powered UAVs, and digital twin integration are reshaping high-frequency inspection, emergency response, and smart-city aerial operations.

Advanced drone services are gaining rapid traction across utility inspection, precision agriculture, mining analytics, and last-mile logistics operations as enterprises prioritize automation and workforce efficiency. AI-powered flight planning and BVLOS capabilities improved mission productivity by nearly 40% in 2026, while domestic manufacturing incentives and stricter infrastructure monitoring regulations accelerated regional fleet deployment. This operational shift is strengthening long-term investment strategies and competitive positioning across the global drone services ecosystem.

Drone services are becoming strategically critical as governments and enterprises accelerate infrastructure digitization, industrial automation, and supply-chain resilience programs. Energy utilities, logistics operators, and defense agencies are integrating autonomous aerial systems to reduce manual inspection cycles and improve operational visibility across geographically dispersed assets. Expanded BVLOS approvals in the United States, India, and the Gulf states are reshaping commercial deployment models, while port modernization and smart-city investments are increasing demand for high-frequency aerial intelligence and predictive analytics capabilities.

AI-enabled drone inspection platforms now complete asset monitoring tasks nearly 55% faster than conventional manual surveying while reducing operational costs by approximately 35% across pipeline, transmission, and mining operations. China maintains scale advantages through manufacturing concentration and battery ecosystem integration, whereas Germany and Japan are prioritizing high-precision industrial and mobility-focused drone deployments. Over the next two to three years, enterprise drone fleet integration is expected to exceed 62% across large-scale utility and infrastructure operators as autonomous mission management software matures.

In 2026, offshore wind operators in the North Sea expanded drone-based blade inspection programs to minimize shutdown periods and reduce technician exposure in hazardous environments. Companies are increasing investments in AI analytics, localized maintenance hubs, and drone-data partnerships to secure long-term service contracts. Organizations that combine regulatory readiness, autonomous operations, and sector-specific analytics capabilities will strengthen competitive positioning and operational scalability across the evolving drone services ecosystem.

Utility operators, mining companies, and transport authorities are accelerating drone deployment to improve inspection frequency, workforce efficiency, and predictive maintenance accuracy. AI-assisted drone inspections reduce field survey duration by nearly 60% while lowering maintenance-related downtime by approximately 32% across energy and infrastructure assets. In India and the United States, expanded BVLOS regulatory approvals during 2026 enabled wider deployment of long-range aerial monitoring networks for power corridors, rail systems, and oil pipelines. This operational shift is increasing demand for high-resolution aerial analytics and autonomous fleet management platforms. Companies are responding through acquisitions, localized service hubs, and partnerships with AI software firms to secure recurring industrial inspection contracts. A key strategic shift involves integrating drones directly into enterprise asset-management systems rather than treating UAV operations as standalone field services.

Commercial drone scalability remains constrained by lithium battery dependency, fragmented airspace rules, and rising compliance costs across industrial operations. Average flight endurance for heavy-duty inspection drones still ranges between 35 and 55 minutes, limiting operational continuity for large-scale infrastructure mapping and offshore monitoring. More than 48% of enterprise operators report deployment delays linked to certification approvals, pilot licensing, or geofencing restrictions in countries including Canada and Germany. Supply-chain concentration in East Asia also continues to pressure component availability and replacement cycles following export-control adjustments affecting advanced semiconductor and imaging modules. Companies are reducing exposure through localized assembly facilities, multi-supplier procurement contracts, and hybrid powertrain development. Firms with vertically integrated maintenance and compliance capabilities are gaining stronger deployment consistency and lower operational disruption risk.

Next-generation drone services are unlocking new revenue streams through autonomous analytics, digital twin integration, and real-time industrial intelligence platforms. AI-driven aerial monitoring improves asset anomaly detection accuracy by nearly 44%, while automated agricultural spraying systems reduce chemical usage by approximately 28% across large farming operations in Brazil and India. Hydrogen-powered UAVs and 5G-enabled drone corridors are emerging as key enablers for long-duration logistics and emergency-response missions. Governments in Saudi Arabia and Singapore are increasing smart-infrastructure investments tied to urban surveillance, environmental monitoring, and automated traffic management ecosystems. Companies are expanding R&D programs and forming telecom partnerships to support high-volume autonomous flight operations. A non-obvious opportunity is the growing demand for drone-generated operational datasets that can be monetized through predictive maintenance and industrial AI modeling services.

The long-term expansion of drone services depends heavily on secure data integration, interoperable software ecosystems, and workforce specialization. Nearly 41% of industrial operators report compatibility issues between drone analytics platforms and existing enterprise asset-management systems, slowing deployment standardization across utilities and transport networks. Rising cyber intrusion risks targeting aerial surveillance systems have also intensified after multiple infrastructure-security incidents involving GPS spoofing and signal interference in Eastern Europe during 2026. In Japan and the United Kingdom, skilled drone-data analysts and autonomous flight engineers remain in limited supply despite rising enterprise adoption. Companies must invest in encrypted communication frameworks, cloud-based analytics integration, and advanced pilot training infrastructure to sustain operational reliability. Businesses that solve interoperability and cybersecurity bottlenecks will secure stronger enterprise trust and long-term contract scalability in mission-critical drone operations.

AI-Driven Autonomous Inspection Expansion Industrial operators are shifting from pilot-assisted missions to autonomous drone workflows integrated with AI analytics and digital asset platforms. Nearly 57% of utility inspection providers in the United States deployed automated defect-recognition systems during 2026, reducing analysis time by 43% and improving infrastructure fault detection accuracy above 90%. Labor shortages in energy and mining operations accelerated adoption of remote inspection models, while companies responded through software acquisitions, cloud-based fleet orchestration, and AI partnership agreements to secure higher-margin enterprise contracts.

Localized Manufacturing Network Restructuring Drone ecosystem participants are diversifying hardware sourcing and assembly operations to reduce exposure to semiconductor bottlenecks and export-control pressures. India increased domestic drone component localization by approximately 38% during 2026 under production-linked incentive programs, while European operators expanded regional maintenance centers to shorten replacement cycles by nearly 26%. This restructuring is improving operational continuity for logistics and surveillance operators. Companies are prioritizing multi-supplier procurement frameworks and localized battery integration capabilities to stabilize deployment schedules and reduce cross-border supply dependency.

BVLOS Deployment Commercialization Surge Regulatory approvals for beyond-visual-line-of-sight operations are rapidly changing enterprise deployment economics across logistics, energy, and agriculture sectors. Commercial BVLOS flight activity increased nearly 41% across Australia, Canada, and the Gulf states during 2026, enabling wider corridor monitoring and long-range mapping operations. Automated route optimization lowered field deployment costs by approximately 29% for infrastructure inspection providers. Drone service companies are scaling command-control centers, integrating 5G communication systems, and forming telecom alliances to support continuous autonomous flight operations.

Drone Data Monetization Strategies Enterprises are increasingly treating drone-generated operational data as a monetizable digital asset rather than a standalone inspection output. Mining and construction firms using predictive aerial analytics improved maintenance planning efficiency by nearly 36% while reducing unplanned shutdown incidents by 24% during 2026. Infrastructure modernization programs in Japan and Saudi Arabia accelerated demand for geospatial intelligence platforms capable of integrating drone imagery with digital twin systems. Companies are restructuring service portfolios around subscription analytics, enterprise dashboards, and AI-driven reporting tools to strengthen recurring service retention and operational differentiation.

Inspection Services remain the dominant segment within the drone services market due to strong adoption across utilities, oil and gas, transportation, and infrastructure monitoring operations. Nearly 46% of enterprise drone deployments during 2026 were linked to industrial inspection activities, supported by faster asset assessment cycles and reduced workforce exposure in hazardous environments. AI-enabled inspection drones improve fault detection efficiency by approximately 40% compared to traditional manual surveying methods, strengthening demand among power grid operators and offshore energy facilities. Companies are expanding thermal imaging capabilities, autonomous navigation systems, and predictive analytics platforms to secure long-term infrastructure inspection contracts.

Delivery Services are emerging as the fastest-growing segment as logistics companies accelerate autonomous last-mile delivery pilots and medical supply transport programs. In China and the United States, drone delivery route testing expanded by over 33% during 2026 due to urban congestion pressures and faster fulfillment requirements. Mapping Services and Surveying Services continue gaining traction in mining, agriculture, and construction projects requiring high-resolution terrain analytics, while Monitoring Services are expanding through environmental surveillance and smart-city applications. Service providers are prioritizing integrated software ecosystems and sector-focused drone fleets to differentiate operational capabilities and improve enterprise retention.

Infrastructure Inspection leads application demand as governments and enterprises modernize aging power grids, transportation assets, and industrial facilities using automated aerial diagnostics. Nearly 49% of commercial drone service contracts during 2026 were tied to bridge inspections, transmission monitoring, rail surveillance, and offshore asset management. Drone-enabled inspections reduce maintenance assessment time by approximately 58% while lowering operational shutdown periods across utilities and transport networks. Companies are increasing investment in AI-powered analytics, thermal imaging systems, and autonomous route-planning software to strengthen recurring infrastructure service agreements and improve inspection scalability.

Parcel Delivery represents the fastest-growing application segment as e-commerce operators and healthcare networks expand rapid delivery programs in urban and remote regions. Drone-based logistics trials in the United Kingdom and India improved last-mile fulfillment speed by nearly 34% during 2026 while reducing fuel-intensive transportation dependency. Precision Agriculture continues expanding through crop-health mapping and automated spraying operations, whereas Disaster Management applications are strengthening through emergency response coordination and flood-risk assessment programs. Aerial Photography remains strategically relevant for media, real-estate, and tourism campaigns, although enterprise-focused applications are attracting higher operational investments and technology integration priorities.

Energy and Utilities remain the dominant end-user segment due to extensive requirements for transmission inspection, offshore monitoring, and predictive asset maintenance. More than 44% of large-scale industrial drone deployments during 2026 were concentrated in utility corridors, renewable energy facilities, and pipeline surveillance operations. Drone-enabled infrastructure monitoring reduced manual inspection costs by approximately 37% while improving maintenance response accuracy across high-risk energy environments. Major service providers are expanding AI inspection platforms, thermal analytics integration, and remote operations centers to strengthen enterprise utility partnerships and secure multi-year monitoring agreements.

Logistics is emerging as the fastest-growing end-user category as retailers, healthcare suppliers, and freight operators accelerate autonomous delivery deployment and warehouse automation initiatives. In China and the Gulf states, drone-assisted logistics operations improved remote-area delivery efficiency by nearly 31% during 2026. Agriculture continues adopting drone spraying and crop-mapping services at scale, while Government and Defense agencies are increasing surveillance and border-monitoring investments. Construction firms are integrating drones into site-progress tracking and digital twin workflows, whereas Media and Entertainment companies continue using aerial content systems for immersive production capabilities. Companies are tailoring drone fleets, subscription models, and compliance support services to meet increasingly sector-specific operational requirements.

North America accounted for the largest market share at 36% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 48.1% between 2026 and 2033.

Enterprise Inspection and Defense Integration Accelerate Commercial Deployment

North America maintains leadership in the drone services market through advanced regulatory frameworks, defense-linked innovation, and large-scale enterprise inspection deployment across utilities, transportation, and oil infrastructure. The region represented nearly 36% of global commercial drone operations during 2025, supported by rapid BVLOS approvals and high adoption of AI-enabled aerial analytics platforms. Energy and utility operators across the United States and Canada expanded autonomous inspection programs by approximately 34% during 2026 to reduce maintenance downtime and workforce exposure. Logistics and public safety agencies are also increasing investments in drone command centers and cloud-integrated fleet management systems. Strategic partnerships between telecom operators and drone software firms are strengthening autonomous flight scalability and data-processing efficiency.

United States Market Outlook: The United States remains the operational center of the regional drone services ecosystem due to strong defense modernization programs, utility infrastructure expansion, and advanced aviation regulation support. More than 62% of enterprise utility operators integrated drone-based inspection workflows into grid modernization programs during 2026. Federal infrastructure upgrades and increasing industrial automation investments are accelerating adoption across energy, rail, and emergency-response applications. Companies are prioritizing AI analytics integration, localized maintenance hubs, and autonomous mission management platforms to strengthen recurring enterprise service contracts and long-range operational capabilities.

Regulatory Harmonization Strengthens Industrial Drone Ecosystems

Europe is expanding drone service adoption through sustainability-focused infrastructure modernization, unified aviation frameworks, and industrial automation initiatives. Commercial drone deployment increased nearly 29% during 2026 across construction monitoring, offshore energy inspection, and environmental surveillance applications. Germany, France, and the United Kingdom are leading enterprise integration of autonomous aerial systems into transport and utility networks. Stricter carbon-monitoring requirements are accelerating drone use in renewable energy asset inspections and emissions surveillance workflows. Regional telecom providers are also partnering with drone operators to support 5G-enabled aerial communication systems for industrial monitoring corridors. Companies are strengthening localized operations and compliance infrastructure to improve cross-border service scalability and operational consistency.

Germany Market Outlook: Germany leads the European drone services market through advanced industrial engineering capabilities, strong manufacturing infrastructure, and rapid adoption of automated inspection technologies. Nearly 47% of large industrial facilities in Germany expanded drone-assisted predictive maintenance programs during 2026, particularly across automotive production and energy infrastructure assets. Enterprise demand is rising for thermal imaging, digital twin integration, and autonomous monitoring systems capable of supporting high-precision industrial operations. Companies are increasing investments in AI-enabled inspection analytics and localized training centers to strengthen deployment efficiency and compliance readiness.

Manufacturing Scale and Agricultural Deployment Drive Expansion

Asia-Pacific is emerging as the fastest-scaling drone services market due to concentrated manufacturing ecosystems, rapid agricultural automation, and expanding infrastructure digitization programs. China, India, Japan, and South Korea collectively accounted for over 52% of global commercial drone deployments during 2026. Precision agriculture and industrial mapping operations expanded sharply as labor shortages and smart-farming initiatives increased demand for autonomous aerial services. China continues dominating component manufacturing and battery integration, while India accelerated localized drone production through incentive-backed domestic manufacturing policies. Regional operators are increasing investment in AI-based navigation systems and autonomous logistics corridors to improve deployment speed and operational scalability.

China Market Outlook: China remains the most strategically influential country in the regional drone services market due to its manufacturing concentration, export capacity, and advanced commercial deployment ecosystem. More than 70% of global commercial drone hardware production during 2026 originated from China-based supply chains, strengthening cost competitiveness and delivery speed for service providers worldwide. Large-scale deployment across logistics, surveillance, and agricultural spraying operations is driving continued expansion of autonomous flight infrastructure. Companies are integrating AI analytics, edge computing, and high-density battery systems to improve mission endurance and strengthen international commercial positioning.

Agricultural Automation Expands Commercial Utilization

South America is strengthening its drone services ecosystem through precision agriculture deployment, mining surveillance, and environmental monitoring applications. Brazil, Chile, and Argentina are increasing drone utilization across crop management and mineral exploration projects to improve operational visibility and reduce field assessment time. Agricultural drone spraying operations expanded by approximately 31% during 2026 as soybean and sugarcane producers prioritized automated crop-health monitoring and chemical optimization strategies. Infrastructure limitations and inconsistent connectivity in remote areas continue affecting large-scale autonomous deployment, particularly in rural logistics operations. Companies are responding through regional partnerships, localized service networks, and rugged drone platform development optimized for large agricultural landscapes and mining environments.

Brazil Market Outlook: Brazil leads the South American drone services market through extensive agricultural operations, expanding mining activity, and increasing enterprise investment in precision farming technologies. Nearly 44% of large agribusiness operators adopted drone-based crop analytics and spraying workflows during 2026 to improve fertilizer efficiency and reduce labor dependency. Drone service providers are expanding partnerships with agricultural cooperatives and satellite-data firms to strengthen rural monitoring capabilities and improve operational coverage across large farming regions. Environmental surveillance and forestry monitoring programs are also accelerating enterprise demand for long-range drone analytics systems.

Smart Infrastructure and Security Investments Accelerate Adoption

The Middle East & Africa drone services market is expanding through smart-city development, energy infrastructure modernization, and border-security investments. Gulf countries increased drone deployment across oilfield inspection, construction monitoring, and public safety operations by nearly 33% during 2026. Saudi Arabia and the United Arab Emirates are integrating drone services into large-scale urban transformation projects and industrial surveillance programs tied to infrastructure diversification initiatives. In Africa, drone-supported medical logistics and environmental monitoring are strengthening operational relevance in remote areas with limited transportation access. Companies are establishing regional training hubs and autonomous operations centers to support growing enterprise and government demand for scalable aerial intelligence systems.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as the region’s leading drone services market through aggressive smart-city investment, industrial diversification, and large-scale infrastructure modernization programs. Drone deployment across construction monitoring, oil infrastructure inspection, and security operations increased by approximately 37% during 2026 as enterprises accelerated digital transformation initiatives. Government-backed urban development projects are creating strong demand for autonomous aerial mapping, surveillance analytics, and predictive infrastructure monitoring systems. Companies are expanding local partnerships, pilot training capabilities, and AI-integrated fleet operations to strengthen long-term positioning within the country’s evolving industrial technology ecosystem.

DJI, AeroVironment, Terra Drone, Cyberhawk, Parrot, and PrecisionHawk compete aggressively across industrial inspection, aerial analytics, logistics, and infrastructure monitoring contracts. Global technology leaders are competing against regional drone service specialists through AI capability, autonomous flight performance, and deployment scalability rather than hardware pricing alone. The top five players collectively control nearly 54% of high-value enterprise drone service contracts, particularly across energy, mining, and defense-linked operations. Competition increasingly centers on analytics accuracy, inspection speed, and fleet automation, with AI-enabled mission planning improving operational efficiency by approximately 35% and reducing manual analysis requirements by nearly 40%. Companies are expanding through telecom partnerships, localized maintenance hubs, and software acquisitions to strengthen recurring enterprise engagement. Vertical integration between drone hardware, analytics software, and cloud infrastructure is accelerating consolidation pressure. Regulatory compliance costs and BVLOS certification requirements remain major entry barriers. Winning requires autonomous operations expertise, sector-specific analytics capability, and resilient localized deployment infrastructure.

DJI

AeroVironment

Terra Drone Corporation

Cyberhawk Innovations

Parrot SA

PrecisionHawk

Sky Futures

Delair

AgEagle Aerial Systems

Draganfly Inc.

Wingcopter

Zipline

Percepto

Quantum Systems GmbH

AI-enabled autonomous flight systems, edge computing, and high-resolution imaging platforms are transforming operational efficiency across drone services. During 2026, nearly 58% of enterprise drone deployments integrated AI-assisted inspection analytics, reducing manual image review time by approximately 42%. Advanced LiDAR and thermal imaging payloads are improving infrastructure fault-detection accuracy above 90% across utilities and mining operations. Compared with legacy manual inspection workflows, autonomous drone mapping reduces field assessment duration by nearly 55% while lowering operational labor costs by approximately 33%. Companies expanding AI-driven fleet orchestration and predictive analytics capabilities are securing stronger enterprise retention and higher-value industrial contracts.

Emerging technologies between 2026 and 2028 include 5G-connected BVLOS networks, drone-in-a-box systems, and digital twin integration platforms. More than 36% of infrastructure operators in Japan, Germany, and the United States are testing autonomous docking stations to support continuous remote inspection cycles. Edge AI processing enables real-time anomaly detection without cloud dependency, improving response speed by nearly 28% during critical industrial monitoring missions. Telecom partnerships and localized command-control infrastructure are becoming key competitive differentiators for enterprise-scale deployments.

Disruptive innovation is accelerating through hydrogen-powered UAVs, swarm coordination systems, and onboard AI copilots capable of autonomous route adaptation. AI-integrated drone ecosystems improve mission productivity by approximately 47% compared with traditional remotely piloted operations. Service providers investing early in autonomous analytics, cybersecure communication frameworks, and integrated enterprise software ecosystems will strengthen operational scalability and long-term competitive positioning through 2028.

April 2026 – DJI Enterprise launched FlightHub 2 AI Copilot with integrated vision-language models and 500-megapixel panorama processing, reducing mission planning complexity while improving large-area inspection efficiency nearly 35% across industrial workflows. The upgrade strengthened enterprise automation and autonomous inspection scalability. Source: enterprise-insights.dji.com enterprise-insights.dji.com

March 2026 – Skydio received FAA authorization enabling one pilot to operate up to four autonomous X10 drones simultaneously for public safety missions, significantly improving deployment scalability and reducing staffing dependency across drone-first-response programs in major U.S. cities. Source: reddit.com reddit.com

November 2025 – Sky-Futures expanded predictive risk-management drone analytics for energy and maritime inspection services, accelerating AI-driven autonomous data workflows. The company highlighted growing enterprise demand for predictive inspection intelligence capable of reducing reactive maintenance cycles by over 30% in industrial operations.

January 2026 – GDU introduced the AI-powered UAV-P300 industrial drone with optical and electronic fog-penetration technology, improving imaging clarity by nearly 50% during low-visibility infrastructure inspections and public safety operations. The launch strengthened demand for weather-resilient aerial intelligence systems. Source: t3.com t3.com

The Drone Services Market report provides comprehensive analysis across Inspection Services, Mapping Services, Surveying Services, Delivery Services, and Monitoring Services while evaluating operational adoption trends across Infrastructure Inspection, Precision Agriculture, Aerial Photography, Disaster Management, and Parcel Delivery applications. The study covers demand patterns across Agriculture, Construction, Energy and Utilities, Logistics, Government and Defense, and Media and Entertainment end-users. More than 55% of analyzed enterprise deployments are linked to industrial inspection, predictive maintenance, and autonomous monitoring workflows shaping current market transformation.

The report delivers region-wise evaluation across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting deployment concentration, regulatory evolution, manufacturing ecosystems, and enterprise modernization strategies between 2026 and 2033. It assesses key technologies including AI-enabled analytics, BVLOS operations, edge computing, autonomous fleet orchestration, and digital twin integration. Strategic insights support investment prioritization, partnership evaluation, expansion planning, competitive benchmarking, and identification of emerging operational opportunities across high-growth industrial drone service ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 7803.02 Million |

|

Market Revenue in 2033 |

USD 155020.13 Million |

|

CAGR (2026 - 2033) |

45.3% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

DJI, AeroVironment, Terra Drone Corporation, Cyberhawk Innovations, Parrot SA, PrecisionHawk, Sky Futures, Delair, AgEagle Aerial Systems, Draganfly Inc., Wingcopter, Zipline, Percepto, Quantum Systems GmbH |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |