Reports

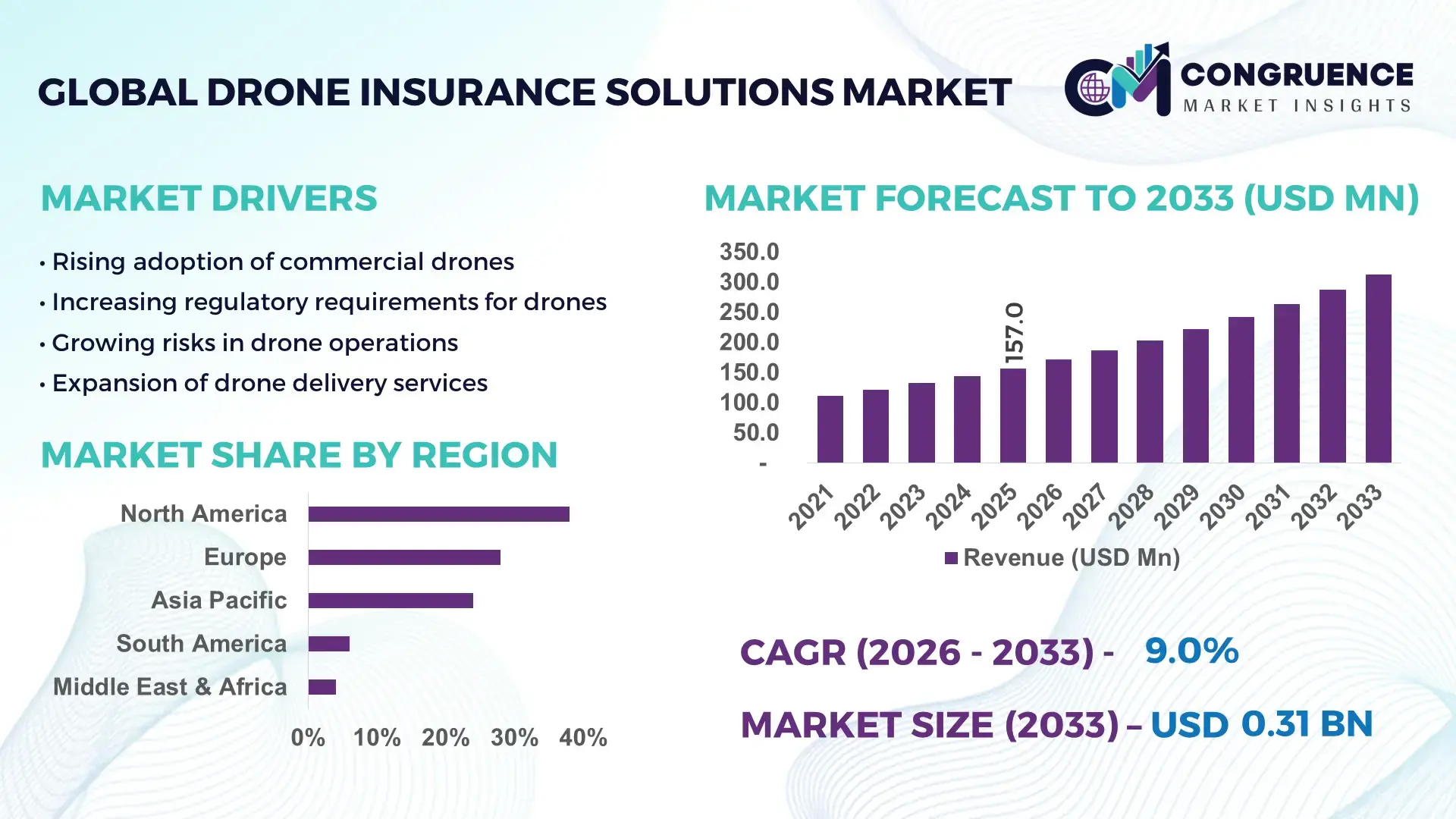

The Global Drone Insurance Solutions Market was valued at USD 157.0 Million in 2025 and is anticipated to reach a value of USD 312.8 Million by 2033 expanding at a CAGR of 9% between 2026 and 2033, according to an analysis by Congruence Market Insights. The growth is primarily driven by the rapid expansion of commercial drone operations across logistics, agriculture, surveillance, and infrastructure inspection sectors requiring specialized risk coverage.

The United States dominates the Drone Insurance Solutions Market with over 865,000 registered commercial drones as of 2025, supported by extensive FAA regulatory frameworks. The country accounts for more than 42% of global enterprise drone deployments, with high adoption in construction (28%), agriculture (22%), and energy inspection (18%). Insurance providers in the U.S. have developed AI-based underwriting platforms capable of processing risk data 35% faster, while over 60% of large drone operators now use usage-based insurance models. Investments exceeding USD 500 million have been recorded in drone risk analytics platforms, enhancing predictive claims management and real-time liability tracking.

Market Size & Growth: USD 157.0 million in 2025, projected to reach USD 312.8 million by 2033 at 9% CAGR, driven by rising commercial drone deployments.

Top Growth Drivers: Commercial drone adoption (45%), automated risk analytics (32%), regulatory compliance requirements (28%).

Short-Term Forecast: By 2028, AI-based underwriting is expected to reduce claim processing time by 40% and improve risk accuracy by 35%.

Emerging Technologies: AI-driven underwriting, blockchain-based policy validation, real-time drone telemetry integration.

Regional Leaders: North America (USD 120M by 2033, enterprise adoption), Europe (USD 85M, regulatory-driven demand), Asia-Pacific (USD 75M, rapid industrial drone expansion).

Consumer/End-User Trends: Over 58% of enterprise drone users prefer customized, usage-based insurance policies.

Pilot or Case Example: In 2024, a logistics firm reduced insurance claim disputes by 30% using AI-enabled drone monitoring systems.

Competitive Landscape: Market leader holds ~18% share, followed by Allianz, AXA, AIG, Zurich Insurance, and SkyWatch.

Regulatory & ESG Impact: Over 65% of insurers align with aviation safety mandates and carbon-neutral compliance strategies.

Investment & Funding Patterns: More than USD 700 million invested in drone analytics and insurtech platforms globally since 2023.

Innovation & Future Outlook: Integration of IoT-based tracking and predictive analytics is expected to enhance risk assessment efficiency by over 40%.

Drone insurance solutions are increasingly utilized across agriculture (25%), construction (22%), logistics (18%), and energy sectors (15%), driven by rising UAV deployment. Technological advancements such as AI-based underwriting and real-time telemetry analytics are improving claim accuracy by over 30%. Regulatory frameworks and mandatory insurance policies in regions like Europe are boosting adoption, while Asia-Pacific shows strong growth due to expanding drone delivery services and infrastructure monitoring applications.

The Drone Insurance Solutions Market is strategically positioned at the intersection of aviation, insurtech, and data analytics, making it a critical enabler of safe and scalable drone operations. As drone deployments increase across industries such as logistics, agriculture, and infrastructure inspection, insurance solutions are evolving from traditional liability coverage to dynamic, data-driven risk management platforms. AI-powered underwriting systems now process real-time flight data, reducing risk assessment errors by nearly 35% compared to conventional manual underwriting methods.

Advanced telemetry-based insurance models deliver 40% improvement in risk prediction accuracy compared to legacy actuarial approaches. North America dominates in volume due to high commercial drone usage, while Europe leads in adoption with over 62% of enterprises complying with mandatory drone insurance regulations. By 2028, AI-integrated claims processing systems are expected to reduce claim settlement time by up to 45%, significantly improving operational efficiency for insurers.

From a compliance and ESG perspective, insurers are committing to sustainability goals, including a 30% reduction in carbon-intensive operations by 2030 through digital policy management and reduced physical inspections. In 2025, a U.S.-based insurer achieved a 28% reduction in fraudulent claims using AI-based drone tracking analytics, demonstrating the effectiveness of technology-driven solutions.

Looking ahead, integration with blockchain for secure policy validation and IoT for real-time monitoring will redefine insurance frameworks. The Drone Insurance Solutions Market is expected to emerge as a foundational pillar supporting regulatory compliance, operational resilience, and sustainable growth across the global drone ecosystem.

The Drone Insurance Solutions Market is characterized by rapid technological evolution, regulatory expansion, and increasing commercial drone utilization. As global drone registrations surpass 1.5 million units, insurers are adapting to the rising need for specialized coverage solutions that address operational risks, liability exposure, and equipment protection. Key dynamics include the integration of AI-based underwriting tools, which have improved risk assessment efficiency by over 30%, and the adoption of usage-based insurance models, now preferred by nearly 55% of commercial drone operators.

Regulatory frameworks across regions, particularly in North America and Europe, are mandating insurance coverage for commercial drone operations, significantly influencing market demand. Additionally, the expansion of drone applications in agriculture, logistics, and surveillance is increasing the complexity of risk profiles, requiring advanced analytics and real-time monitoring systems. However, challenges such as data standardization, lack of historical loss data, and cybersecurity risks continue to shape the market landscape. Overall, the market is transitioning toward digital, data-driven insurance ecosystems that enable proactive risk mitigation and scalable coverage solutions.

The rapid increase in commercial drone usage is a primary driver of the Drone Insurance Solutions Market. As of 2025, global commercial drone fleets have grown by over 38% compared to 2022, with industries such as agriculture, logistics, and construction accounting for nearly 65% of total deployments. These drones are increasingly used for high-risk operations including aerial inspections, crop monitoring, and parcel delivery, necessitating comprehensive insurance coverage. Additionally, more than 70% of enterprises deploying drones now require liability and equipment insurance as part of operational compliance. The growing complexity of drone missions, including beyond visual line-of-sight (BVLOS) operations, has increased risk exposure by approximately 25%, further driving demand for advanced insurance solutions. Insurers are responding by introducing customized policies and real-time risk monitoring systems, enhancing coverage precision and operational safety.

One of the major restraints in the Drone Insurance Solutions Market is the limited availability of historical risk and claims data. Unlike traditional aviation or automotive sectors, drone operations are relatively new, resulting in insufficient datasets for accurate actuarial modeling. Currently, less than 40% of insurers have access to comprehensive drone-related loss data, leading to higher uncertainty in premium pricing and risk assessment. This data gap increases underwriting complexity and often results in conservative policy structures, limiting market penetration among small and medium enterprises. Additionally, variability in drone types, applications, and operational environments creates inconsistent risk profiles, making standardization difficult. As a result, nearly 30% of potential users delay insurance adoption due to unclear pricing and coverage limitations, hindering overall market growth.

AI-driven risk analytics presents significant growth opportunities for the Drone Insurance Solutions Market by enabling real-time monitoring and predictive risk assessment. Advanced machine learning models can analyze flight data, weather conditions, and operational patterns to predict potential incidents with up to 45% accuracy improvement compared to traditional methods. Over 50% of leading insurers are investing in AI-based platforms to enhance underwriting efficiency and reduce claim fraud. These technologies also support usage-based insurance models, which are gaining traction among 60% of commercial drone operators due to their flexibility and cost-effectiveness. Furthermore, integration with IoT sensors and telemetry systems allows insurers to offer dynamic pricing and proactive risk mitigation, opening new revenue streams and expanding market reach.

Regulatory fragmentation across regions remains a critical challenge for the Drone Insurance Solutions Market. Different countries have varying requirements for drone registration, operation, and insurance coverage, creating complexity for insurers operating globally. For instance, while over 65% of European countries mandate drone insurance for commercial use, several regions in Asia and Africa have inconsistent or evolving regulations. This lack of uniformity increases compliance costs by nearly 20% for multinational insurers and limits the scalability of standardized insurance products. Additionally, frequent updates to aviation laws and safety standards require continuous policy adjustments, increasing operational overhead. Nearly 35% of insurers report delays in market entry due to regulatory uncertainties, making it a significant barrier to growth and innovation.

AI-driven underwriting improves risk accuracy by 35%: Insurers are increasingly deploying AI algorithms to assess drone flight risks using real-time telemetry and environmental data. Over 62% of insurance providers have integrated AI tools into underwriting processes, reducing manual evaluation time by 40% and enhancing policy customization for diverse drone applications.

Usage-based insurance adoption reaches 58% among enterprises: Flexible insurance models based on flight hours and operational risk exposure are gaining traction. Nearly 58% of commercial drone operators now prefer pay-as-you-fly policies, reducing insurance costs by up to 25% while improving transparency and coverage efficiency.

Blockchain-enabled policy validation reduces fraud by 30%: Blockchain technology is being implemented to secure policy contracts and claims data. Around 45% of insurers are piloting blockchain-based systems, which have demonstrated a 30% reduction in fraudulent claims and improved transaction transparency.

Integration of IoT sensors enhances real-time monitoring by 50%: Advanced IoT-enabled sensors embedded in drones provide continuous data on performance and environmental conditions. This has increased real-time monitoring capabilities by over 50%, enabling proactive risk mitigation and faster claim resolution processes.

The Drone Insurance Solutions Market is segmented based on type, application, and end-user, each reflecting distinct operational requirements and risk profiles. Insurance types range from liability coverage to comprehensive hull and payload protection, catering to varying levels of operational complexity. Applications span across agriculture, logistics, surveillance, and infrastructure inspection, where risk exposure and coverage needs differ significantly. End-users include commercial enterprises, government agencies, and individual operators, each contributing uniquely to market demand. Increasing adoption of drones in industrial operations and regulatory mandates for insurance coverage are shaping segmentation trends. Additionally, the rise of AI-driven underwriting and usage-based policies is influencing how different segments evolve, with enterprises demanding more customized and scalable insurance solutions.

Liability insurance dominates the Drone Insurance Solutions Market, accounting for approximately 48% of total adoption due to its critical role in covering third-party damages and regulatory compliance requirements. Hull insurance holds around 28%, primarily used for protecting drone equipment against physical damage, while payload insurance accounts for nearly 12%, catering to high-value cargo operations such as medical deliveries and surveillance equipment. Usage-based insurance is emerging as the fastest-growing segment, expanding at an estimated CAGR of 11%, driven by demand for flexible, cost-efficient coverage models. These policies allow operators to pay based on flight hours or mission risk, making them highly attractive to SMEs and startups. Other niche insurance types, including cyber risk and data liability coverage, collectively contribute around 12%, reflecting the growing importance of data security in drone operations.

• In 2025, a national aviation authority reported that over 55% of licensed drone operators opted for liability insurance as mandatory coverage for commercial operations, highlighting its dominant role in the market.

Commercial applications lead the Drone Insurance Solutions Market with approximately 52% share, driven by widespread use in agriculture, construction, and logistics. Surveillance and inspection applications account for around 26%, reflecting growing demand for infrastructure monitoring and security operations. Delivery and logistics applications hold nearly 14%, while recreational and hobbyist usage contributes about 8%. Delivery and logistics represent the fastest-growing application segment, expanding at an estimated CAGR of 12%, supported by increasing adoption of drone-based last-mile delivery services. More than 40% of logistics companies are piloting drone delivery systems to improve efficiency and reduce operational costs. Additionally, over 35% of agricultural enterprises use drones for crop monitoring, indicating strong cross-sector adoption.

• In 2025, a government aviation report highlighted that drone-based agricultural monitoring systems were deployed across over 20 million hectares globally, significantly increasing demand for specialized insurance coverage.

Commercial enterprises dominate the Drone Insurance Solutions Market with a share of approximately 55%, driven by large-scale drone deployments in industries such as agriculture, logistics, and construction. Government and defense agencies account for around 25%, utilizing drones for surveillance, border security, and disaster management. Individual and hobbyist users contribute nearly 20%, reflecting growing consumer adoption. SMEs represent the fastest-growing end-user segment, expanding at an estimated CAGR of 10%, due to increasing affordability of drones and flexible insurance solutions. Over 48% of SMEs using drones prefer usage-based insurance models, highlighting a shift toward cost-effective coverage. Additionally, nearly 60% of large enterprises have integrated drone operations into their core business processes, further driving demand for comprehensive insurance solutions.

• In 2025, a global technology survey reported that over 50% of enterprises deploying drones integrated insurance solutions into their operational risk management frameworks, demonstrating increasing reliance on structured coverage.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.5% between 2026 and 2033.

North America benefits from over 900,000 registered drones and high enterprise adoption across industries such as construction (30%) and agriculture (25%). Europe holds approximately 28% share, driven by stringent regulatory mandates and mandatory insurance policies in over 65% of countries. Asia-Pacific accounts for nearly 24% share, with rapid drone adoption in China, India, and Japan, supported by infrastructure investments exceeding USD 1 trillion. South America and Middle East & Africa collectively contribute around 10%, with increasing drone usage in energy, mining, and surveillance sectors. Regional disparities in regulatory frameworks and technological adoption significantly influence market expansion patterns.

North America holds approximately 38% of the Drone Insurance Solutions Market, driven by high commercial drone penetration and strong regulatory frameworks. Industries such as construction, agriculture, and energy collectively account for over 70% of drone usage in the region. Regulatory support from aviation authorities ensures that nearly 68% of commercial drone operators maintain mandatory insurance coverage. Technological advancements, including AI-based underwriting and real-time telemetry integration, have improved risk assessment efficiency by over 35%. A key regional player has introduced usage-based insurance platforms, enabling operators to reduce premium costs by up to 25%. Consumer behavior indicates that enterprises prioritize comprehensive coverage, with over 60% opting for multi-risk insurance policies. The region’s mature digital infrastructure and high adoption of insurtech solutions continue to drive market expansion.

Europe accounts for nearly 28% of the Drone Insurance Solutions Market, with countries such as Germany, the UK, and France leading adoption. Over 65% of European nations enforce mandatory drone insurance regulations, significantly boosting market demand. Key industries include logistics, surveillance, and infrastructure inspection, contributing to over 60% of regional drone usage. Sustainability initiatives and strict compliance standards are driving demand for transparent and explainable insurance models. More than 55% of insurers in the region have adopted AI-driven underwriting systems. A regional insurer has implemented blockchain-based policy management, reducing claim disputes by 20%. Consumer behavior shows strong preference for compliant and transparent insurance solutions, reflecting regulatory-driven adoption trends.

Asia-Pacific holds around 24% of the Drone Insurance Solutions Market and ranks as the fastest-growing region in terms of volume. China, India, and Japan are the top contributors, collectively accounting for over 70% of regional drone deployments. Infrastructure development and smart city initiatives are key drivers, with investments exceeding USD 1 trillion. Technological innovation hubs in China and Japan are advancing AI-based risk analytics and IoT integration. A regional insurance provider has launched digital platforms enabling real-time policy customization, improving customer acquisition by 30%. Consumer behavior indicates strong growth in enterprise adoption, particularly in logistics and e-commerce sectors, where drone usage is expanding rapidly.

South America contributes approximately 6% to the Drone Insurance Solutions Market, with Brazil and Argentina as key markets. Drone usage is primarily driven by agriculture, mining, and media industries, accounting for over 65% of regional demand. Government initiatives supporting agricultural modernization have increased drone adoption by nearly 20% in recent years. Trade policies and infrastructure investments are encouraging the use of drones for surveillance and inspection. A local insurer has introduced customized policies for agricultural drones, improving coverage accessibility for farmers. Consumer behavior shows growing demand for affordable and flexible insurance solutions, particularly among SMEs and independent operators.

The Middle East & Africa region accounts for approximately 4% of the Drone Insurance Solutions Market, with the UAE and South Africa leading adoption. Key sectors include oil & gas, construction, and security, contributing to over 70% of drone usage. Technological modernization and smart city initiatives are driving demand for advanced insurance solutions. Local regulations are evolving to support commercial drone operations, with over 50% of countries introducing new compliance frameworks. A regional insurer has partnered with technology firms to develop AI-based risk assessment tools, improving underwriting efficiency by 25%. Consumer behavior reflects increasing reliance on drones for industrial applications, supporting steady market growth.

United States – 34% Market share: strong enterprise adoption and advanced regulatory frameworks supporting large-scale drone operations.

China – 18% Market share: high production capacity and rapid deployment of drones across logistics and surveillance sectors.

The Drone Insurance Solutions Market is moderately fragmented, with over 50 active global and regional insurers competing across specialized and general insurance offerings. The top five companies collectively hold approximately 55% of the market share, indicating a balanced competitive environment with both established players and emerging insurtech firms.

Key players are focusing on strategic partnerships with drone manufacturers and technology providers to enhance product offerings. More than 40% of insurers have introduced AI-based underwriting platforms, improving risk assessment efficiency by over 30%. Additionally, around 35% of companies are investing in blockchain technology to enhance policy transparency and reduce fraud.

Mergers and acquisitions have increased by 20% over the past two years, reflecting consolidation efforts and expansion into new geographic markets. Product innovation remains a critical competitive factor, with over 50% of insurers offering usage-based or on-demand insurance models. The market is also witnessing the entry of digital-first insurance providers, intensifying competition and driving innovation.

AXA

AIG

Zurich Insurance Group

SkyWatch.AI

Global Aerospace

Starr Insurance

Liberty Mutual

Munich Re

Chubb

Hiscox

BWI Aviation Insurance

Avion Insurance

Technological advancements are playing a transformative role in the Drone Insurance Solutions Market, enabling more accurate risk assessment, efficient claims processing, and enhanced customer experience. AI and machine learning algorithms are widely used for underwriting, analyzing flight data, weather conditions, and operational patterns to predict risks with up to 40% higher accuracy compared to traditional methods. Over 60% of insurers have integrated AI tools into their operations, significantly reducing manual processing time.

IoT and telemetry systems embedded in drones provide real-time data on performance and environmental conditions, improving monitoring capabilities by more than 50%. This data enables insurers to implement usage-based insurance models, which are preferred by nearly 58% of commercial drone operators. Blockchain technology is also gaining traction, with around 45% of insurers piloting blockchain-based systems to enhance policy transparency and reduce fraudulent claims by approximately 30%.

Cloud-based platforms are facilitating scalable and flexible insurance solutions, allowing insurers to manage large volumes of data efficiently. Additionally, predictive analytics tools are enabling proactive risk mitigation, reducing incident rates by up to 25%. Integration of geospatial analytics and digital twins is further enhancing risk visualization and operational planning. These technologies collectively are reshaping the insurance landscape, making it more dynamic, data-driven, and responsive to evolving drone applications.

• In March 2025, Allianzannounced through its official newsroom the expansion of its aviation and drone risk solutions portfolio, integrating advanced data analytics and satellite-based monitoring to enhance underwriting precision. The update emphasized improved real-time risk visibility for commercial drone fleets and more flexible policy customization for enterprise operators.

• In October 2024, AXApublished a corporate blog update highlighting the rollout of next-generation parametric insurance solutions for emerging risks, including unmanned aerial systems. The initiative focused on faster claims settlement triggered by predefined flight-risk conditions, improving operational efficiency and reducing administrative delays for drone operators.

• In July 2025, SkyWatch.AIannounced via its official platform enhancements to its on-demand drone insurance app, enabling instant policy activation and real-time flight-based coverage adjustments. The update improved user onboarding efficiency and strengthened its position in digital-first drone insurance services. Source: www.skywatch.ai

• In January 2025, Zurich Insurance Grouphighlighted in its official insights section the expansion of digital insurance capabilities, including blockchain-enabled policy management and advanced analytics for aviation and drone-related risks. The initiative focused on improving transparency, reducing fraud exposure, and enabling scalable insurance solutions for commercial UAV operations.

The Drone Insurance Solutions Market Report provides a comprehensive analysis of industry trends, market segmentation, technological advancements, and regional dynamics shaping the global landscape. The report covers various insurance types, including liability, hull, payload, and usage-based policies, offering insights into their adoption across different operational environments.

It examines key application areas such as agriculture, logistics, surveillance, infrastructure inspection, and media, highlighting their contribution to overall market demand. The report also analyzes end-user segments, including commercial enterprises, government agencies, and individual operators, detailing their adoption patterns and risk management strategies.

Geographically, the report encompasses major regions such as North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, providing detailed insights into regional market behavior, regulatory frameworks, and technological adoption. It also explores emerging markets and niche segments, including drone delivery services and smart city applications.

Technological coverage includes AI-based underwriting, IoT integration, blockchain-enabled policy management, and predictive analytics, emphasizing their impact on operational efficiency and risk mitigation. The report further evaluates competitive dynamics, profiling key market players and their strategic initiatives. Overall, it offers a holistic view of the Drone Insurance Solutions Market, supporting informed decision-making for industry stakeholders.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 157.0 Million |

| Market Revenue (2033) | USD 312.8 Million |

| CAGR (2026–2033) | 9.0% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Allianz; AXA; AIG; Zurich Insurance Group; SkyWatch.AI; Global Aerospace; Starr Insurance; Liberty Mutual; Munich Re; Chubb; Hiscox; BWI Aviation Insurance; Avion Insurance |

| Customization & Pricing | Available on Request (10% Customization Free) |