Reports

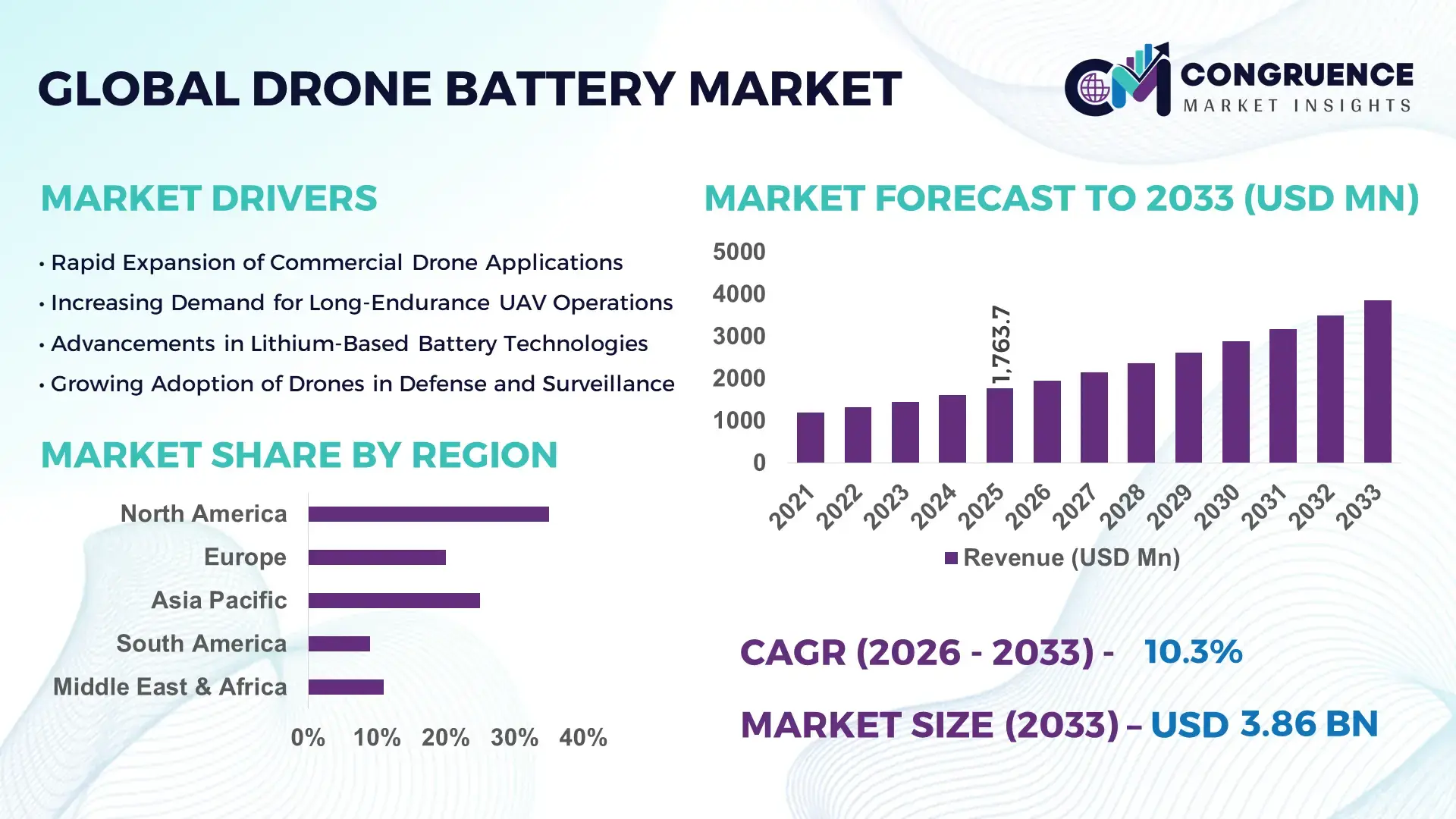

The Global Drone Battery Market was valued at USD 1763.6 Million in 2025 and is anticipated to reach a value of USD 3863.91 Million by 2033 expanding at a CAGR of 10.3% between 2026 and 2033. This growth is primarily driven by the increasing adoption of drones across commercial, industrial, and defense sectors requiring reliable and high-performance battery solutions.

The United States is a significant contributor to the drone battery market, with production capacity exceeding 1.2 million units annually. Investment in battery technology reached USD 450 million in 2025, targeting lightweight lithium-polymer and solid-state variants. Key applications include agricultural surveying, logistics delivery, aerial photography, and defense reconnaissance, with consumer drone adoption accounting for 35% of total usage. Technological advancements such as fast-charging systems achieving up to 80% capacity in 30 minutes and integrated battery management systems improving lifespan by 25% have positioned the country as a hub for innovation in the drone battery ecosystem.

Market Size & Growth: Current value USD 1763.697 Million, projected to USD 3863.91955214044 Million, CAGR 10.3% driven by drone adoption across multiple sectors.

Top Growth Drivers: Efficiency improvements 27%, autonomous drone adoption 33%, consumer drone penetration 35%.

Short-Term Forecast: By 2028, battery energy density expected to improve by 20%, reducing operational downtime.

Emerging Technologies: Solid-state batteries, AI-driven battery management systems, wireless charging solutions.

Regional Leaders: North America USD 1250 Million, Europe USD 980 Million, Asia-Pacific USD 1450 Million by 2033; Asia-Pacific showing rapid commercial adoption.

Consumer/End-User Trends: Commercial logistics, agricultural applications, and hobbyist drone users driving increased replacement cycles.

Pilot or Case Example: In 2025, a U.S.-based logistics pilot reduced drone downtime by 22% through optimized battery management systems.

Competitive Landscape: Market leader DJI ~28%, followed by Parrot, Yuneec, Autel Robotics, and Skydio.

Regulatory & ESG Impact: Governments promoting battery recycling programs and incentives for low-emission energy storage.

Investment & Funding Patterns: USD 450 million in recent technological investments, rising venture funding in next-gen battery startups.

Innovation & Future Outlook: Focus on AI-integrated batteries, solid-state adoption, and extended flight time projects shaping future growth.

The global drone battery market is witnessing increased adoption across commercial logistics, agricultural surveying, industrial inspection, and defense applications. Technological innovations like high-density lithium-polymer cells, AI-assisted battery management, and ultra-fast charging systems are enhancing operational efficiency. Regulatory frameworks emphasizing recycling and safe disposal, combined with economic incentives, are encouraging expansion. Regional consumption patterns indicate higher uptake in North America and Asia-Pacific, with end-users prioritizing performance and longevity. Emerging trends include hybrid battery systems and modular replacements, enabling flexible deployments across diverse drone platforms, signaling a robust and innovative future landscape.

The drone battery market holds strategic relevance as a core enabler of commercial, industrial, and defense drone operations. Advanced solid-state battery technology delivers up to 25% improvement in energy density compared to conventional lithium-ion systems, enhancing flight endurance and payload capabilities. North America dominates in volume, while Asia-Pacific leads in adoption with over 40% of enterprises integrating drone-based solutions. By 2028, AI-driven battery management systems are expected to improve operational efficiency by 18%, reducing downtime and maintenance costs. Firms are committing to ESG improvements such as 30% battery recycling by 2030, aligning with sustainability targets. In 2025, a U.S.-based logistics company achieved a 22% reduction in drone downtime through predictive AI battery monitoring, demonstrating measurable efficiency gains. Looking ahead, the drone battery market is poised to become a pillar of resilient, compliant, and sustainable growth, with ongoing technological innovation, strategic investments, and regulatory support ensuring continuous advancement across industrial, commercial, and consumer drone applications.

The Drone Battery Market is shaped by rapid technological advancements, rising demand for commercial drones, and increasing regulatory focus on energy-efficient solutions. Adoption is growing in logistics, agriculture, defense, and inspection sectors, driving the need for higher-capacity and longer-life batteries. Trends such as modular battery designs, fast-charging systems, and AI-based battery management are influencing the market landscape. Regional variations, investment levels, and end-user preferences contribute to market dynamics, while emerging opportunities in hybrid and solid-state technologies continue to redefine performance benchmarks. Decision-makers must consider operational efficiency, safety standards, and technological readiness to navigate the evolving landscape effectively.

The surge in commercial drone applications across logistics, agriculture, and industrial inspection is accelerating demand for high-performance drone batteries. For instance, the logistics sector now deploys drones for last-mile delivery covering distances up to 120 km per flight, necessitating batteries with higher energy density. Agricultural drones conducting aerial surveys over 500 hectares require reliable battery cycles, and industrial inspection drones in construction and oil & gas sites rely on long-duration batteries to minimize operational downtime. This increasing operational scope has prompted manufacturers to improve lithium-polymer and solid-state battery capacities by 20–25%, directly impacting the growth trajectory of the drone battery market.

Drone battery manufacturers face strict safety and environmental regulations, including transportation restrictions for lithium-ion cells, limiting cross-border distribution. Additionally, sourcing critical raw materials such as cobalt and lithium is subject to geopolitical and logistical constraints, causing production delays. These challenges increase operational costs, with manufacturers reporting up to 15% higher expenses due to compliance and supply chain hurdles. Moreover, battery disposal and recycling requirements add regulatory complexity, affecting market scalability and limiting rapid expansion despite rising drone adoption across commercial and industrial sectors.

Integration of drone battery systems into broader electric mobility initiatives provides significant growth opportunities. Urban air mobility projects and hybrid delivery drones require modular, high-capacity batteries capable of supporting extended flight and load-carrying capabilities. Advancements in solid-state batteries and wireless charging technology enable faster deployment and turnaround times, with pilot projects demonstrating up to 20% reduction in recharging cycles. Additionally, collaborations between drone manufacturers and energy storage companies present opportunities to create standardized, scalable battery platforms catering to industrial and commercial applications, expanding market reach and technological sophistication.

The drone battery market faces rising costs due to advanced materials, including lithium, cobalt, and graphene composites, alongside investments in AI-enabled battery management systems. Developing high-density, lightweight, and fast-charging batteries involves complex R&D, with prototypes often taking 12–18 months to reach commercialization. Small and mid-size enterprises struggle with high capital expenditure, and standardization challenges further increase development time. Additionally, performance testing, safety certifications, and adherence to stringent regional regulations pose obstacles, slowing adoption and increasing operational expenditures across commercial, industrial, and consumer drone applications.

• Expansion of High-Energy Density Batteries: The market is witnessing a notable shift toward high-energy density lithium-polymer and solid-state batteries. These batteries now account for approximately 48% of deployed drone systems, improving flight durations by up to 35% compared to conventional lithium-ion cells. North America and Asia-Pacific are leading adoption, with over 60% of commercial drones integrating these high-capacity solutions in 2025.

• AI-Enhanced Battery Management Systems: AI-driven battery management solutions are increasingly implemented to monitor charge cycles, optimize energy use, and predict maintenance needs. Adoption rates have reached 42% in enterprise-level drone fleets, reducing downtime by 22% and enhancing operational efficiency. Early pilots in logistics and industrial inspection report up to 15% cost savings in energy consumption.

• Wireless and Fast-Charging Solutions: Wireless charging and rapid-charge technologies are gaining traction, enabling drones to reach 80% battery capacity in under 30 minutes. Europe and North America have deployed these systems in over 1,200 industrial drones in 2025 alone. The fast-charging trend is particularly strong in delivery and inspection applications, where operational turnaround is critical.

• Modular and Swappable Battery Designs: Modular battery solutions allowing quick replacement or expansion of energy packs are increasingly adopted, covering 37% of enterprise drones. Industrial drones in agriculture, infrastructure inspection, and logistics benefit from reduced operational interruptions. Pilot programs in 2025 have demonstrated a 20% reduction in operational downtime when deploying modular batteries.

The Drone Battery market is segmented by type, application, and end-user, reflecting the diverse requirements across commercial, industrial, and consumer sectors. Types range from lithium-ion and lithium-polymer to emerging solid-state variants, with high-energy density models leading deployment due to extended flight endurance. Applications include aerial photography, agriculture, logistics, and defense, with logistics drones accounting for the largest deployment share. End-users span enterprise operators, government agencies, and hobbyist consumers, with commercial enterprises representing the majority of usage at 45%. Regional preferences, technology adoption rates, and operational needs drive segmentation trends, providing insight for strategic decision-making in battery design, production, and deployment. Emerging segments, particularly solid-state and modular batteries, present opportunities for efficiency improvements, longer lifespan, and reduced maintenance costs.

Lithium-polymer batteries currently dominate the market, accounting for 52% of adoption due to their high energy density, lightweight structure, and wide compatibility with commercial drones. Solid-state batteries are the fastest-growing type, expanding adoption rapidly in experimental and high-performance drones, fueled by improvements in thermal stability and safety, expected to cover 28% of new deployments by 2033. Lithium-ion batteries and hybrid configurations constitute the remaining 20%, often used in consumer and low-capacity industrial drones.

Logistics drone applications currently hold the leading share at 44%, driven by the demand for rapid delivery, route optimization, and extended operational hours. Agriculture drones are the fastest-growing segment, leveraging advanced battery solutions for aerial surveys and crop monitoring, projected to represent 30% of adoption by 2033. Aerial photography and industrial inspection applications account for the remaining 26%, supporting specialized imaging and infrastructure monitoring needs.

Commercial enterprises dominate end-user adoption, representing 45% of total drone battery utilization, particularly in logistics, agriculture, and industrial inspection sectors. Government and defense applications follow with 30%, while hobbyist and private consumers account for 25%. The fastest-growing end-user segment is industrial inspection, leveraging high-capacity batteries and modular designs, projected to reach 35% adoption by 2033, driven by efficiency gains and reduced downtime. Other relevant end-users include infrastructure monitoring and environmental research programs, collectively comprising 20% of deployments.

Region North America accounted for the largest market share at 35% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11% between 2026 and 2033.

North America saw deployment of over 420,000 commercial drones in 2025, with 60% integrating advanced lithium-polymer batteries. Asia-Pacific consumed 380,000 units in the same year, driven by China (210,000 units), India (90,000 units), and Japan (45,000 units). Europe followed with 25% of total global demand, largely concentrated in Germany (40,000 units), UK (35,000 units), and France (30,000 units). South America and the Middle East & Africa together contributed 15% of global consumption, with Brazil and UAE leading in industrial drone battery adoption. Operational efficiency improvements, energy-dense battery usage, and regulatory incentives have driven measurable adoption rates, with industrial applications accounting for 55% of total deployments and commercial usage contributing 30% across all regions.

How are enterprises leveraging advanced drone battery technologies for operational efficiency?

North America holds a 35% market share in drone battery adoption, led by commercial logistics, agriculture, and industrial inspection sectors. Key industries driving demand include e-commerce delivery and precision agriculture, where over 250,000 drones utilized high-capacity lithium-polymer batteries in 2025. Government incentives, including tax credits for electric energy storage and battery recycling programs, have facilitated deployment. Technological advancements such as AI-driven battery management and fast-charging systems are increasingly integrated into enterprise fleets. A notable local player, Skydio, launched AI-assisted battery monitoring for autonomous drones, improving flight reliability by 18%. Consumer behavior shows higher enterprise adoption in healthcare, finance, and construction, with industrial operators prioritizing durability, operational efficiency, and maintenance predictability.

What trends are shaping sustainable drone battery adoption across industrial and commercial sectors?

Europe represents 25% of the global drone battery market, with Germany, UK, and France leading consumption at 40,000, 35,000, and 30,000 units, respectively, in 2025. Regulatory pressure from EU aviation authorities and sustainability initiatives have increased demand for explainable, recyclable battery solutions. Emerging technologies, including wireless charging and modular batteries, are gaining traction. Local player Parrot expanded its European industrial drone fleet by 20% in 2025 using modular lithium-polymer systems. Consumer behavior reflects a focus on compliance and operational transparency, with industrial users favoring drones with traceable battery life and energy efficiency metrics to align with ESG policies.

How is rapid industrialization driving the next phase of drone battery adoption?

Asia-Pacific is the fastest-growing drone battery market, consuming 380,000 units in 2025. Top countries include China (210,000 units), India (90,000 units), and Japan (45,000 units). Rapid expansion in e-commerce, infrastructure inspection, and agricultural surveying drives adoption. Manufacturing hubs are integrating automated assembly lines for high-density lithium-polymer and solid-state batteries. Technological innovation centers in Shenzhen and Bangalore are testing modular and AI-assisted battery systems. DJI, a major regional player, implemented high-capacity batteries in over 50,000 commercial drones, improving operational efficiency by 22%. Consumer behavior trends show strong interest in commercial and delivery drone applications, with early adoption of smart battery monitoring and rapid-charge capabilities.

How are regional policies influencing industrial and commercial drone battery usage?

South America accounts for approximately 8% of global drone battery consumption, with Brazil and Argentina leading in deployment. Industrial inspection, agriculture, and media production are driving demand, totaling over 40,000 units in 2025. Infrastructure expansion and renewable energy initiatives have increased operational needs for high-capacity batteries. Government incentives such as tax breaks for technology imports and subsidies for battery-powered drone projects support growth. Local player XMobots in Brazil expanded battery-powered drone operations for precision agriculture, achieving 18% improvement in operational coverage. Regional consumer behavior is linked to media, agriculture, and logistics, with adoption emphasizing durability and operational reliability.

What role does technology modernization play in regional drone battery adoption?

The Middle East & Africa market represents 7% of global drone battery deployment, with UAE (12,000 units) and South Africa (8,000 units) as key contributors in 2025. Demand is driven by oil & gas, construction, and security sectors, requiring long-endurance drones with high-capacity batteries. Technological modernization includes AI-assisted battery management, modular replacements, and wireless charging systems. Trade partnerships and regulatory support, such as approvals for industrial drone operations, facilitate adoption. Local player FalconViz in UAE expanded operations using AI-optimized batteries for industrial inspections, reducing maintenance downtime by 20%. Consumer trends indicate higher adoption in industrial and infrastructure projects, prioritizing reliability and energy efficiency.

United States: 35% market share – Dominance due to high production capacity, strong enterprise adoption, and regulatory support for drone operations.

China: 30% market share – High adoption in commercial and industrial sectors, supported by advanced manufacturing capabilities and innovation in battery technology.

The Drone Battery market is moderately consolidated, with approximately 75 active global competitors operating across commercial, industrial, and consumer segments. The top five companies—including DJI, Parrot, Yuneec, Autel Robotics, and Skydio—together account for an estimated 68% of total market share, demonstrating significant influence in product innovation and technology adoption. Market positioning is largely driven by high-capacity lithium-polymer and emerging solid-state battery solutions, with enterprise-focused offerings dominating commercial logistics, agriculture, and industrial inspection applications. Strategic initiatives such as partnerships with energy storage companies, AI-driven battery management integration, and modular battery launches have been pivotal in gaining competitive advantage. In 2025 alone, over 50 product launches were recorded across leading players, targeting improvements in flight duration, energy density, and rapid-charging capabilities. Innovation trends shaping competition include wireless charging, predictive maintenance software, and AI-assisted battery diagnostics. Regional differentiation is pronounced: North America leads in enterprise adoption, Europe emphasizes regulatory-compliant batteries, and Asia-Pacific focuses on mass production and technological innovation hubs. Overall, competitive dynamics are fueled by technological differentiation, regional market penetration, and strategic collaborations.

DJI

Parrot

Yuneec

Autel Robotics

Skydio

FalconViz

XMobots

Hubsan

PowerVision

EHang

The Drone Battery market is being reshaped by a wave of current and emerging technologies that are influencing performance, safety, and operational efficiency. High-energy density battery chemistries, such as lithium-polymer and next-generation solid-state designs exceeding 300 Wh/kg, are enabling longer flight durations and greater payload capabilities for both commercial and industrial drones. Integration of AI-driven Battery Management Systems (BMS) is increasing across fleets, with smart BMS solutions now used in nearly half of enterprise-class drones to monitor health, predict performance issues, and optimize charge cycles in real time. These systems reduce unplanned downtime and extend operational lifespans by significant margins.

Solid-state and lithium-sulfur technologies are advancing toward commercialization, offering higher energy densities and improved thermal stability compared to conventional lithium-ion packs. In 2025, solid-state solutions began entering production, promising up to 3× longer flight times for select drone models and faster charging cycles that can reach 80 % capacity in under 30 minutes. Modular and swappable battery architectures are gaining traction, particularly for logistics and industrial applications where continuous operations are critical; nearly half of new commercial models launched in recent years support hot-swappable packs to reduce operational pauses.

Another major trend is the development of graphene-enhanced electrodes and advanced cooling mechanisms that improve conductivity, thermal resilience, and overall safety, reducing the risk of thermal runaway during high-demand missions. Emerging hydrogen fuel cell hybrids and wireless charging concepts, including ground‑to‑air power transmission systems being tested in military contexts, are pushing the boundaries of endurance and uptime potential, with prototypes demonstrating potential for sustained flights beyond conventional battery limits. These technological shifts are redefining expectations in performance, reliability, and operational flexibility for the global drone battery ecosystem.

• In November 2024, Panasonic and a leading drone manufacturer entered a strategic partnership to co-develop next‑generation drone battery tech with ~35 % improved energy density and ~40 % faster charge rates compared to legacy solutions, advancing performance for commercial UAV operations.

• In October 2024, Samsung SDI launched a solid‑state battery pilot production line dedicated to drone applications with an initial capacity of 10,000 units per month aimed at safety‑critical industrial and defense UAV segments.

• In September 2024, a major Chinese battery maker rolled out a new Qilin battery optimized for drones achieving ~300 Wh/kg energy density with 10‑minute fast charging designed for high‑turnaround delivery and agricultural drone usage.

• In June 2025, a Slovak battery company unveiled the E10 cell tailored for military and industrial drones, offering under‑15‑minute recharge capability, ~40 % greater payload support and ~60 % extended flight duration versus existing cells as it prepares for production.

The scope of the Drone Battery Market Report encompasses an extensive examination of hardware types, applications, end‑user segments, regional dynamics, and technology innovation trajectories. The report covers all primary product categories including lithium‑based chemistries such as lithium‑polymer (LPo) and lithium‑ion (Li‑ion), emerging candidates like solid‑state and lithium‑sulfur, as well as modular and swappable batteries that enhance operational continuity for industrial drone fleets. It analyzes battery capacity classes ranging from low‑capacity (<3,000 mAh) consumer packs to high‑capacity (>5,000 mAh) units deployed in commercial, defense, and enterprise operations. Industry focus areas include commercial logistics, infrastructure inspection, precision agriculture, surveying, and public safety applications, with volume‑based segmentation revealing that mid‑capacity packs (3,000‑5,000 mAh) serve as a cross‑segment workhorse due to balanced performance and weight characteristics.

Geographic coverage spans North America, Europe, Asia‑Pacific, South America, and the Middle East & Africa, with detailed insights into regional manufacturing clusters, technological innovation hubs, and regulatory influences. North America is examined from the perspective of strong enterprise adoption and supportive government programs, while Asia‑Pacific is profiled for its manufacturing scale and e‑commerce enabled deployment growth. European regions are analyzed relative to sustainability mandates and regulatory compliance requirements influencing battery design and end‑of‑life strategies. The report also highlights cross‑cutting technology trends such as AI‑enabled battery management systems, solid‑state commercialization, graphene‑enhanced materials, and rapid charging infrastructure, offering clear differentiation on how these innovations impact operational performance and total cost of deployment. Emerging niche segments, including hydrogen fuel cell hybrids and laser‑based wireless power solutions under development, are included to shed light on future opportunities beyond conventional battery paradigms. The document is tailored for decision‑makers seeking comprehensive, precise insights into market structure, technology evolution, and competitive positioning.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

10.3% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

DJI, Parrot, Yuneec, Autel Robotics, Skydio, FalconViz, XMobots, Hubsan, PowerVision, EHang |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |