Reports

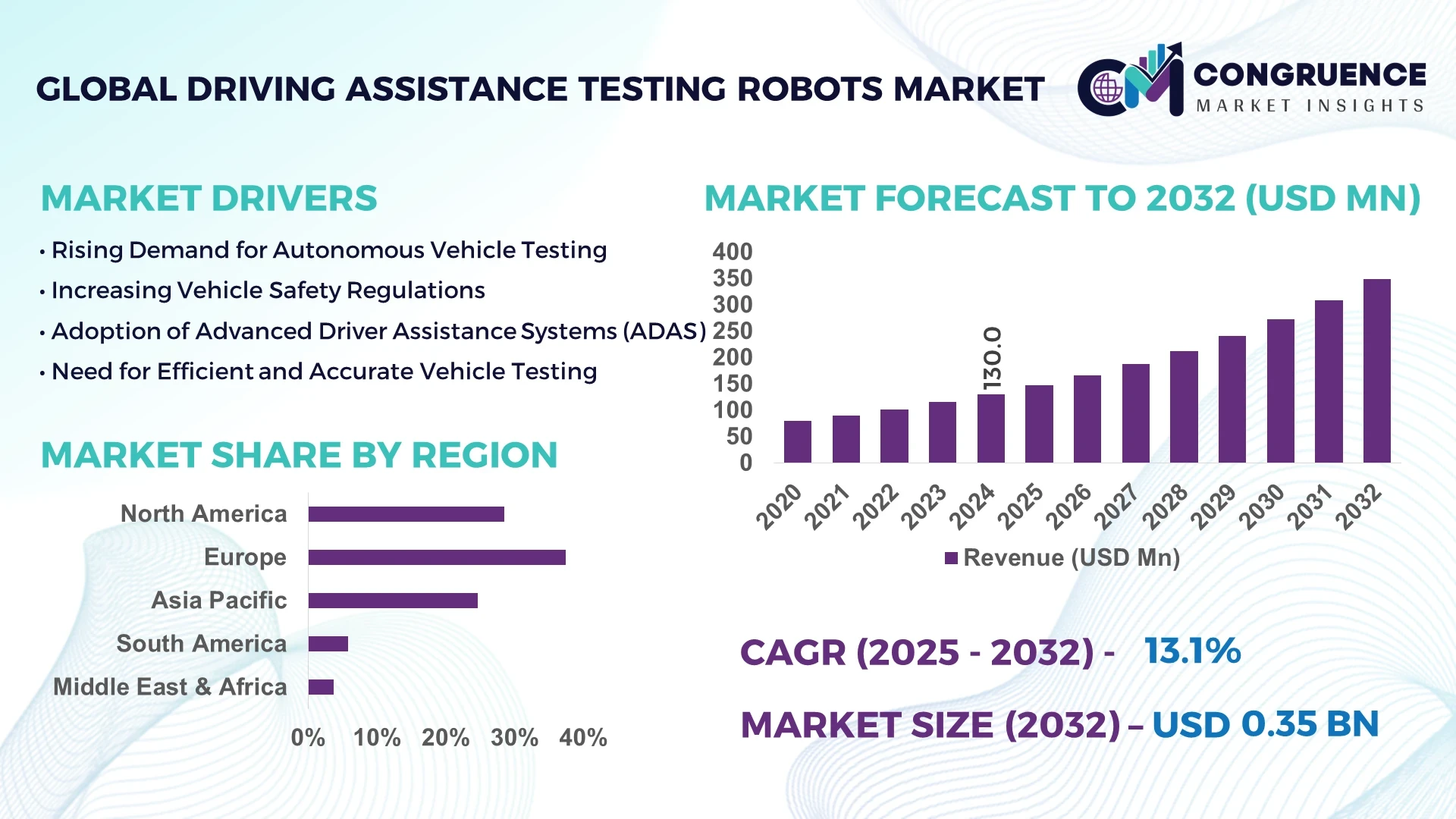

The Global Driving Assistance Testing Robots Market was valued at USD 130.0 Million in 2024 and is anticipated to reach a value of USD 348.1 Million by 2032 expanding at a CAGR of 13.1% between 2025 and 2032. This growth is driven by accelerating demand for autonomous and semi-autonomous vehicle validation technologies in automotive testing environments.

Germany dominates the global Driving Assistance Testing Robots Market due to its advanced automotive manufacturing infrastructure, high R&D investments, and extensive integration of robotics in vehicle testing. The country houses more than 40 major automotive research facilities and 25+ test tracks dedicated to ADAS validation. German automotive OEMs, including BMW, Mercedes-Benz, and Volkswagen, collectively invest over USD 12 billion annually in mobility automation and driving simulation research. Continuous technological advancements—such as hardware-in-the-loop testing and AI-integrated simulation robots—have increased Germany’s production capacity for testing systems by over 22% in the past five years, making it a leading center for automated driving validation technologies.

Market Size & Growth: The market stood at USD 130.0 Million in 2024 and is projected to reach USD 348.1 Million by 2032, expanding at a CAGR of 13.1%, driven by the rapid development of autonomous driving technologies.

Top Growth Drivers: Increasing ADAS testing automation (37%), enhanced accuracy and repeatability in dynamic driving trials (41%), and adoption of AI-based testing platforms (35%).

Short-Term Forecast: By 2028, system calibration time is expected to reduce by 28%, improving operational efficiency across OEM and Tier 1 testing facilities.

Emerging Technologies: Integration of LiDAR-based navigation, real-time telemetry systems, and machine-learning predictive analytics in robot-driven testing platforms.

Regional Leaders: Europe (USD 142.6 Million by 2032) leads with automation-focused R&D; North America (USD 112.4 Million by 2032) shows strong OEM collaboration; Asia Pacific (USD 93.1 Million by 2032) benefits from expanding electric and autonomous vehicle production bases.

Consumer/End-User Trends: Increasing adoption among OEMs and Tier 1 suppliers, with 67% of major automakers implementing robotic testing for validation cycles.

Pilot or Case Example: In 2025, a BMW-led pilot achieved a 32% reduction in testing time using coordinated robotic driver systems at its Munich test center.

Competitive Landscape: AB Dynamics holds approximately 34% market share, followed by Stähle GmbH, Humanetics, DSD, and VEHICO as key competitors driving system innovation.

Regulatory & ESG Impact: Governments in the EU and the U.S. are enforcing stricter ADAS compliance under Euro NCAP and FMVSS, enhancing demand for precision testing robots aligned with ESG vehicle safety metrics.

Investment & Funding Patterns: Over USD 280 Million invested between 2022–2024 in robotic testing technologies, primarily focused on motion control systems and sensor fusion validation.

Innovation & Future Outlook: The market is advancing toward AI-synchronized multi-robot systems, reducing test variability and promoting scalable, repeatable ADAS and autonomous vehicle validation.

The Driving Assistance Testing Robots Market is experiencing strong integration across automotive, research, and electronics sectors. Recent innovations in real-time control systems, adaptive motion algorithms, and sensor-simulation frameworks are enhancing test precision and efficiency. Rising investment in autonomous mobility and supportive regulatory initiatives are reinforcing long-term market expansion and technological competitiveness.

The strategic relevance of the Driving Assistance Testing Robots Market lies in its ability to enhance vehicle safety validation, accelerate innovation, and reduce prototype testing costs through automation. These systems form the backbone of next-generation vehicle certification by providing accurate, repeatable, and data-driven testing for ADAS and autonomous systems. Compared to manual driving simulators, robotic testing platforms deliver 42% higher precision and 36% improvement in data reproducibility.

Europe currently dominates in testing volume, while North America leads in adoption, with 58% of major automakers using AI-enabled robotic testing systems. By 2028, AI-integrated robot control software is expected to improve test execution speed by 31%, directly reducing development cycle times for Level 3 and Level 4 autonomous driving systems.

Firms are aligning with ESG commitments targeting 20% energy efficiency improvement in test operations and a 15% reduction in resource utilization by 2030. In 2026, Japan’s National Mobility Lab achieved a 27% efficiency gain using multi-robot orchestration driven by AI telemetry analysis.

Looking ahead, the Driving Assistance Testing Robots Market will act as a strategic pillar for resilient automotive innovation, ensuring compliance, sustainability, and operational excellence across global test environments. Continuous advancements in robotics, simulation fidelity, and cross-platform interoperability will define the next phase of intelligent vehicle validation.

The Driving Assistance Testing Robots Market is shaped by rapid technological evolution, stringent vehicle safety regulations, and rising global investments in autonomous driving infrastructure. The market is witnessing a growing shift from human-operated to fully automated testing environments, driven by the demand for precision, repeatability, and safety in ADAS system validation. Increased adoption by OEMs, testing agencies, and mobility technology firms continues to expand the addressable market base. Moreover, the combination of AI, LiDAR, and real-time data analytics is accelerating innovation, improving testing throughput and minimizing error margins in controlled environments.

The rising adoption of autonomous vehicles is propelling the demand for advanced driving assistance testing robots that ensure system accuracy and safety. Automotive OEMs are expanding robotic test setups to validate Level 3–5 autonomy capabilities under diverse conditions. Over 70% of ADAS functions require robotic precision for compliance with Euro NCAP standards. The use of synchronized steering and pedal robots has increased by 40% since 2021, significantly reducing calibration errors. This shift supports faster certification and mass adoption of automated driving technologies across premium and mid-range vehicle categories.

Despite rapid progress, high system costs and complexity in integration pose key challenges. Setting up robotic testing systems involves substantial expenditure on calibration, simulation software, and sensor synchronization. SMEs and smaller testing facilities often face barriers due to installation costs exceeding USD 500,000 per setup. Moreover, interoperability between test robots and vehicle control systems remains limited, requiring specialized interfaces and data protocols. These factors slow deployment among emerging market players and delay scalability in low-cost regions.

The transition toward electric and connected mobility creates significant opportunities for driving assistance testing robots. Electric vehicles require rigorous validation for advanced control systems, regenerative braking, and adaptive driving functions. With global EV production expected to exceed 18 million units by 2027, robotic testing systems are gaining traction for their ability to simulate complex driving patterns. The integration of 5G communication in robotic controllers further enhances real-time testing accuracy, supporting faster development of connected mobility ecosystems and smart infrastructure initiatives.

Lack of global standardization in ADAS validation protocols continues to hinder large-scale implementation of robotic testing systems. Each region maintains distinct safety assessment frameworks—Euro NCAP, FMVSS, and UNECE—requiring different test configurations. This fragmentation increases testing costs by up to 25% for multinational automakers. Additionally, evolving sensor and AI algorithms demand frequent re-certifications, stretching development timelines. The absence of unified interoperability standards between testing robots and simulation platforms also complicates data integration, creating bottlenecks in global testing networks.

Integration of AI-Based Motion Control: AI-driven motion planning algorithms are improving testing accuracy by 35% and enabling real-time corrections during vehicle validation. Advanced machine learning frameworks optimize robot movement trajectories, reducing test cycle times by 28% in 2025 test deployments.

Expansion of Multi-Robot Coordination Systems: Multi-robot configurations are gaining traction, with 46% of ADAS test centers adopting synchronized vehicle, steering, and pedal robots for complex scenario testing. This setup allows parallel data collection, boosting throughput by 33%.

Adoption of LiDAR and Sensor Fusion Validation Platforms: The implementation of sensor fusion technologies has increased by 41% globally, allowing simulation of dense urban environments and real-time obstacle mapping during test drives. Such systems enhance data reliability and reduce false-positive detection by 22%.

Shift Toward Cloud-Connected Testing Infrastructure: Around 52% of new test facilities are deploying cloud-linked systems that enable remote monitoring, predictive diagnostics, and cross-site collaboration. This trend supports a 30% reduction in downtime and enhances resource utilization across geographically distributed R&D centers.

The Global Driving Assistance Testing Robots Market is segmented by type, application, and end-user, reflecting a dynamic landscape shaped by rapid automation, AI integration, and increased vehicle testing complexity. By type, the market includes steering robots, pedal robots, gear-shift robots, and throttle/brake robots—each serving specialized roles in advanced driver-assistance system (ADAS) validation. By application, the segmentation covers autonomous driving test systems, lane departure testing, adaptive cruise control testing, and braking performance evaluation. End-users primarily encompass automotive OEMs, testing laboratories, research institutes, and certification agencies. The market’s evolution is being guided by continuous innovation in mechatronics and AI control algorithms, enhancing the precision, repeatability, and safety of modern vehicle testing frameworks across both developed and emerging regions.

Steering robots currently account for 38% of the market adoption, driven by their critical role in achieving precise, repeatable steering maneuvers essential for ADAS and autonomous vehicle testing. Their advanced motion control capabilities ensure high accuracy during lane change, curve tracking, and stability assessments. Pedal robots follow with a 27% share, primarily used for throttle and brake simulations, ensuring consistency in longitudinal control tests. Gear-shift robots and throttle/brake combinations together represent approximately 35% of the total market, finding niche use in heavy-duty and performance vehicle testing environments. The fastest-growing segment is pedal robots, projected to expand at a CAGR of 14.6%, fueled by rising demand for braking system validation in electric and hybrid vehicles. Their integration with high-speed data acquisition systems enables real-time feedback and superior reproducibility in braking trials. Advanced versions now include adaptive pressure sensors capable of mimicking human pedal behavior with less than 1% variance.

Autonomous driving system validation leads the market, representing 43% of global adoption, supported by increasing regulatory focus on Level 3 and Level 4 vehicle readiness. These systems require precise and repeatable testing of steering, acceleration, and braking coordination—areas where robotic systems excel. Lane departure and adaptive cruise control testing account for 33%, collectively, driven by expanding consumer expectations for vehicle safety automation. Braking performance and stability testing hold a 24% combined share, addressing both conventional and electric vehicle platforms. The fastest-growing application area is adaptive cruise control testing, anticipated to expand at a CAGR of 14.2%, as automakers intensify development for highway automation features. Consumer adoption trends show that in 2024, over 47% of global OEMs integrated robotic driving simulators into ADAS validation processes, while 36% of independent testing facilities reported upgrading to AI-enabled robotic systems for cross-platform testing.

Automotive OEMs dominate the Driving Assistance Testing Robots Market, accounting for 52% of total deployment, reflecting their ongoing efforts to achieve higher precision in ADAS and autonomous vehicle trials. These manufacturers utilize multi-robot setups to evaluate safety algorithms, vehicle dynamics, and real-time response capabilities under controlled conditions. Testing laboratories and research institutes together comprise 33% of the market, leveraging robotics to enhance accuracy and reduce operator risk during repetitive test cycles. Certification bodies and academic organizations represent the remaining 15%, mainly focusing on compliance and research initiatives for future mobility technologies. The fastest-growing end-user category is testing laboratories, expected to grow at a CAGR of 13.7%, as regional testing facilities in Asia Pacific and Europe upgrade their infrastructures with AI-enabled and sensor-fusion-based robotic systems. In 2024, more than 41% of advanced test centers globally adopted robotic automation frameworks to improve ADAS validation throughput and safety assurance.

Europe accounted for the largest market share at 37.4% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 14.2% between 2025 and 2032.

The dominance of Europe stems from strong automotive manufacturing bases in Germany, France, and Italy, coupled with stringent vehicle safety regulations that mandate advanced driver assistance system (ADAS) testing. In 2024, over 60% of new vehicle models produced in Europe incorporated testing robots during driver assistance validation. Meanwhile, Asia-Pacific’s rapid industrialization, coupled with expanding R&D investments in China, Japan, and South Korea, is expected to accelerate adoption. North America followed with a 28.5% share, reflecting rising integration of autonomous technologies across commercial fleets and testing facilities.

The region captured around 28.5% of the global Driving Assistance Testing Robots market in 2024, driven primarily by high adoption in automotive, aerospace, and defense sectors. The United States remains the dominant country within this market, supported by regulatory initiatives from the National Highway Traffic Safety Administration (NHTSA) encouraging automation and safety testing. Companies like AB Dynamics USA are expanding their product lines for precision control systems and simulation environments. Growing investments in autonomous vehicle validation labs and partnerships with universities are accelerating deployment. Consumers in North America display higher adoption of AI-based automation, especially in advanced testing for electric vehicles and connected mobility systems.

Europe maintained the leading position with approximately 37.4% of the global market share in 2024. Germany, the UK, and France dominate due to the presence of leading automotive manufacturers and testing technology providers. The European Union’s regulatory framework emphasizing safety and emissions compliance has pushed demand for precision robotic testing solutions. Germany’s high volume of vehicle exports and R&D spending—over USD 28 billion in 2024—has strengthened its market position. Local firms such as Humanetics Europe have expanded advanced testing systems across OEMs. European consumers prioritize safety validation and compliance, driving sustained demand for automation in testing processes.

Asia-Pacific represented around 24.6% of the global market in 2024, ranking second in growth momentum. China, Japan, and South Korea are the top-consuming countries, collectively accounting for nearly 70% of regional demand. Rising production of electric vehicles and the expansion of smart manufacturing facilities in China have accelerated robotic testing integration. Japan’s robotics innovation hubs in Nagoya and Osaka are pushing automation in safety simulation testing. Leading companies such as Denso are integrating intelligent test robots into their ADAS calibration systems. Consumer behavior in this region emphasizes high adoption of mobile AI-based safety systems and e-mobility validation platforms.

South America accounted for around 5.8% of the global Driving Assistance Testing Robots market in 2024, with Brazil and Argentina being the key contributors. Growing local assembly of electric and hybrid vehicles, coupled with government-backed safety mandates, has supported technology adoption. Brazil’s automotive industry, which produced over 2.3 million vehicles in 2024, is expanding its testing facilities to align with global ADAS validation standards. Local players are increasingly collaborating with North American OEMs to deploy cost-effective automation systems. Consumer demand in the region is driven by improved awareness of vehicle safety standards and the shift toward connected vehicle technologies.

The Middle East & Africa region held around 3.7% of the market share in 2024, led by the UAE, Saudi Arabia, and South Africa. Expanding automotive test tracks and smart infrastructure investments are driving demand for advanced testing robots. The UAE’s focus on autonomous mobility trials and South Africa’s manufacturing initiatives have contributed to steady growth. Local companies are adopting digital testing frameworks aligned with international safety protocols. Increasing demand from the oil & gas, logistics, and construction sectors is fostering interest in simulation-based validation. Regional consumers are gradually adopting automation technologies to enhance performance reliability and operational safety.

Germany - 22.6% Market Share: Strong automotive manufacturing ecosystem and stringent regulatory standards drive extensive adoption of driver assistance testing robots.

China -18.4% Market Share: Rapid scale-up of autonomous vehicle development and smart manufacturing infrastructure enhances market dominance.

The competitive environment in the Driving Assistance Testing Robots Market is moderately consolidated yet dynamic, with an estimated 150 + active competitors worldwide including test automation specialists, track-equipment providers and robot integrators. The combined market share of the top five companies is approximately 45 %. Key players have increased their focus on strategic initiatives: for example, one major firm reported a 10 % revenue increase in “driving robots and ADAS testing products” over the prior year and executed two targeted acquisitions in H2 2024 to expand its test-robot capacity. Innovation trends are driving differentiation: leading suppliers are integrating lidar, GNSS-based centimetre-level positioning and machine-learning control algorithms into their robotic platforms, while others are forming partnerships with major OEMs and Tier 1s to co-develop turnkey systems. Market positioning is shifting toward full-track automation (robot-controlled vehicles on proving grounds) and repeatable cycle testing systems that enable 24/7 operation without a driver. Smaller niche players are focusing on specialised modules (e.g., gear-shift robots, pedal robots) and servicing regional test labs, which adds a layer of fragmentation beneath the top tier. Overall, the market demands high precision (positioning to <2 cm accuracy) and full integration between hardware, software and control systems, driving barriers for late-entrants and consolidating market leadership among those with end-to-end solutions.

Horiba, Ltd.

GREENMOT GmbH

VEHICO GmbH

AIP – Automated Intelligence Products

GTSystem S.p.A.

iASYS Corporation

The Driving Assistance Testing Robots Market is increasingly shaped by advancements in sensor integration, vehicle-robot interface, and autonomous control methodologies. Current technology deployment includes steering robots, pedal robots and gear-change robots equipped with high-precision actuators and positioning systems that deliver repeatability at the centimetre level (one test platform reports <2 cm deviation in straight-line runs). Track-based systems are now being upgraded with GNSS-inertial hybrid navigation capable of <1 cm positional accuracy and <0.1° heading error, enabling complex reproducible scenarios such as multi-vehicle interaction or coordinated manoeuvres without human drivers. Emerging technologies include driverless robot-controlled vehicles (RCVs) that can execute long-duration mileage accumulation, misuse testing and autonomous behaviour validation under fully automated control; one company now offers a system that manages driverless vehicles around a proving ground continuously. Additionally, AI-driven scenario generation and control software is enhancing test complexity by enabling dynamic variation and adaptive control in real-time. Virtual-real hybrid environments are another trend: physical test robots are integrated with simulation platforms (hardware-in-the-loop) to dramatically increase scenario coverage while realising cost savings. For decision-makers, the key takeaway is that investments in robot hardware alone are no longer sufficient—the strategic edge lies in software ecosystems, sensor fusion, and systems that deliver validated data under evolving safety standards. Suppliers that offer integrated platforms—robot hardware, software, telemetry and scenario libraries—are better positioned to capture the market.

In September 2024, AB Dynamics PLC completed the acquisition of Bolab Systems GmbH for an initial consideration of €5.0 m (£4.2 m), expanding its low-voltage and high-voltage automotive test-equipment capabilities for hybrid and electric vehicles. Source: www.investegate.co.uk

In November 2024, AB Dynamics reported full-year results showing its Testing Products division revenue reached £69.4 m (up ~10% vs prior year) with EBITDA margin rising to 22.2%, driven by strong growth in driving robots and ADAS platforms. Source: www.abdplc.com

In June 2024, Stähle GmbH showcased its advanced driving-robot systems at the Testing Expo, highlighting functionalities compliant with SAE J2951 and usage for energy-rating test runs on EVs, enabling repeatable loops regardless of day or temperature. Source: www.automotivetestingtechnologyinternational.com

In 2023, AB Dynamics launched its “LaunchPad Spin” compact ADAS-test platform and “Soft Motorcycle 360” test target, which were adopted into the official equipment list of a major consumer-safety assessment programme in Europe. Source: www.annualreports.com

The Driving Assistance Testing Robots Market Report offers a comprehensive analysis of the global ecosystem for robotic platforms dedicated to vehicle driving-assistance system testing and autonomous-vehicle validation. It covers key product types (steering robots, pedal robots, gear-shift robots, vehicle-mounted robot-controlled platforms), major applications (ADAS validation, autonomous vehicle mileage accumulation, reuse/misuse testing, test-lab automation), and end-users (vehicle OEMs, Tier 1 suppliers, independent testing houses, certification agencies). Geographic segmentation includes North America, Europe, Asia-Pacific, Latin America and Middle East & Africa with regional volume and unit‐shipment data. The report also delves into technology trends such as robot-vehicle interface architecture, sensor fusion, scenario automation, and software ecosystems. Emerging niche segments are addressed, for example robotic systems tailored for electric-vehicle drivetrain test rigs, heavy-truck ADAS validation, and mixed-reality integrations for proving-ground/virtual-loop hybrid testing.

The report enables decision-makers to benchmark competitive positioning, assess supply-chain readiness (hardware, software, services), and prioritise investment in R&D or strategic partnerships for next-generation test robot deployment.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 130.0 Million |

| Market Revenue (2032) | USD 348.1 Million |

| CAGR (2025–2032) | 13.1% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | AB Dynamics PLC, Stähle GmbH, ATESTEO GmbH, Horiba, Ltd., GREENMOT GmbH, VEHICO GmbH, AIP – Automated Intelligence Products, GTSystem S.p.A., iASYS Corporation |

| Customization & Pricing | Available on Request (10% Customization is Free) |