Reports

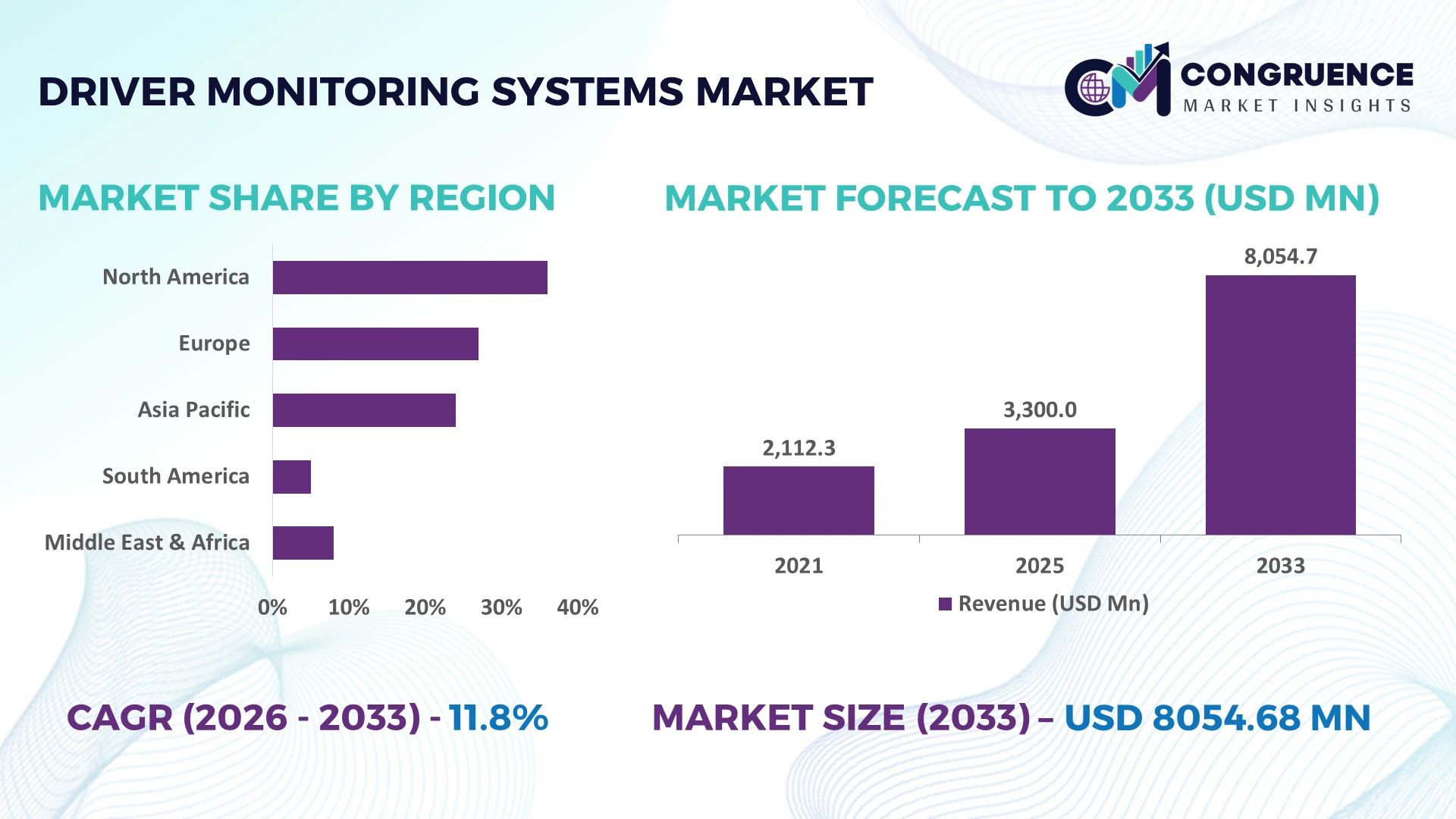

The Global Driver Monitoring Systems Market was valued at USD 3300 Million in 2025 and is anticipated to reach a value of USD 8054.68 Million by 2033 expanding at a CAGR of 11.8% between 2026 and 2033. Growth is driven by mandatory in-cabin safety regulations, AI-powered vision processing, rising integration of Level 2 and Level 3 driver assistance systems, and increasing OEM deployment of infrared camera-based occupant monitoring technologies.

China leads the global Driver Monitoring Systems Market with approximately 34% of vehicle-based system production, supported by large-scale automotive electronics manufacturing, intelligent mobility investments exceeding USD 20 billion, and rapid ADAS integration across passenger vehicles. Germany remains the European technology benchmark, with premium vehicle penetration above 70% for advanced safety features, while cross-border automotive supply-chain diversification following geopolitical trade realignments continues accelerating regional manufacturing resilience.

Automotive manufacturers prioritizing scalable AI-driven monitoring platforms and diversified regional production networks are positioned to strengthen long-term competitive advantage.

Market Size & Growth: USD 3300 Million in 2025, projected to reach USD 8054.68 Million by 2033 at 11.8% CAGR, supported by expanding AI-enabled vehicle safety integration.

Top Growth Drivers: AI vision adoption exceeds 45%, regulatory safety compliance contributes nearly 38%, and premium vehicle ADAS penetration surpasses 50%.

Short-Term Forecast: By 2028, driver fatigue detection accuracy improves over 30% while system response latency declines by approximately 20%.

Emerging Technologies: AI vision processors, infrared cameras, edge computing, and occupant sensing algorithms increase real-time detection performance by more than 35%.

Regional Leaders: Asia-Pacific approaches USD 3400 Million, Europe exceeds USD 2100 Million, and North America nears USD 1700 Million, driven by expanding intelligent mobility programs.

Consumer/End-User Trends: More than 60% of premium vehicle buyers actively prefer advanced in-cabin safety and driver attention monitoring capabilities.

Pilot/Case Example: A 2026 commercial fleet deployment reduced fatigue-related driving incidents by approximately 28% through continuous AI-based driver monitoring.

Competitive Landscape: Leading suppliers collectively account for nearly 48% market share, with major participants including Bosch, Continental, Valeo, Aptiv, and Denso.

Regulatory & ESG Impact: Advanced vehicle safety regulations improve compliant model availability by over 40%, supporting safer and more efficient transportation ecosystems.

Investment & Funding: More than USD 5 billion supports automotive AI, sensor integration, strategic partnerships, and regional manufacturing expansion amid evolving global supply chains.

Innovation & Future Outlook: Next-generation multimodal sensing, AI-powered occupant analytics, and software-defined vehicle platforms accelerate high-growth intelligent cabin transformation.

Increasing deployment across passenger vehicles, commercial fleets, and autonomous mobility platforms continues reshaping the Driver Monitoring Systems Market. AI-enabled eye tracking, facial recognition, and occupant behavior analytics improve driver awareness while reducing intervention time by over 30%. Strong regulatory alignment, localized semiconductor manufacturing, and expanding software-defined vehicle ecosystems are reinforcing product innovation and creating a solid foundation for the strategic market assessment that follows.

Driver monitoring systems have become a strategic differentiator as automakers compete on intelligent safety, software-defined vehicle capabilities, and regulatory compliance rather than hardware alone. The market is benefiting from stricter in-cabin safety mandates and digital cockpit integration, while automotive supply-chain restructuring is encouraging localized sensor and semiconductor production. More than 65% of newly launched premium vehicle platforms now incorporate advanced driver attention monitoring, strengthening product differentiation and reducing compliance risk for global manufacturers.

AI-enabled vision systems outperform conventional rule-based monitoring by improving driver distraction recognition accuracy by nearly 35% while lowering false alerts by approximately 25%, enhancing both operational reliability and user acceptance. China leads large-scale deployment through high-volume vehicle manufacturing and vertically integrated electronics ecosystems, whereas Germany emphasizes precision engineering and premium software integration for high-performance platforms. Over the next two to three years, OEM adoption of integrated cabin sensing solutions is expected to exceed 55% of new intelligent vehicle architectures, reflecting a rapid transition toward centralized computing platforms.

A practical example is the integration of infrared cameras with AI processors to detect fatigue, distraction, and occupant behavior through a single computing platform, reducing component complexity and streamlining vehicle validation. Manufacturers are expanding software partnerships, strengthening domestic semiconductor sourcing, and investing in over-the-air update capabilities to improve system lifecycle performance. Companies that combine scalable software, reliable sensing technologies, and diversified production strategies will secure stronger competitive positioning as intelligent mobility ecosystems continue to mature.

Mandatory vehicle safety regulations and the rapid adoption of advanced driver assistance technologies are reshaping deployment priorities across the automotive sector. More than 60% of newly introduced premium vehicle models now integrate driver monitoring capabilities, while AI-based attention detection improves recognition performance by around 30% compared with conventional camera systems. European safety requirements and China's intelligent vehicle initiatives are accelerating OEM implementation across multiple vehicle categories. In response, automotive technology providers are expanding AI software portfolios, investing in infrared sensing platforms, and forming strategic partnerships with semiconductor developers. The structural shift from optional safety features to standardized intelligent cabin technologies strengthens long-term product differentiation and supports higher software integration across vehicle platforms.

System integration remains constrained by the high cost of infrared cameras, AI processors, and calibration requirements, particularly for entry-level vehicle platforms. Advanced driver monitoring hardware can increase electronic system costs by 15–20%, while software validation and functional safety testing extend development timelines by nearly 25%. Dependence on specialized imaging sensors and automotive-grade semiconductor availability continues to create operational pressure, especially during global supply-chain disruptions. Manufacturers are responding by localizing component sourcing in countries such as India and Mexico, standardizing software architectures, and adopting modular hardware platforms. These measures improve procurement resilience while helping control production costs and accelerate commercialization across broader vehicle segments.

The convergence of driver monitoring, occupant sensing, and software-defined vehicle architecture is opening opportunities beyond regulatory compliance. AI-powered multimodal cabin systems improve detection accuracy by over 35% while reducing processing workloads by approximately 20% through edge computing optimization. Japan and South Korea are advancing integrated cockpit platforms combining biometric recognition, health monitoring, and personalized vehicle settings within unified electronic architectures. Companies are increasing investment in AI algorithms, cloud-connected analytics, and strategic collaborations with automotive software specialists to expand recurring software-based services. A significant competitive advantage lies in transforming driver monitoring from a standalone safety function into an intelligent in-cabin experience platform supporting future autonomous mobility.

Long-term expansion depends on validating increasingly complex AI models across diverse driving environments while protecting connected vehicle ecosystems from cybersecurity threats. More than 70% of next-generation monitoring platforms rely on continuous software updates, and AI training datasets now require millions of annotated driving scenarios to maintain detection consistency. Cross-border data governance requirements and evolving automotive cybersecurity regulations increase engineering complexity, particularly for multinational manufacturers. Companies must strengthen secure software development, cloud validation infrastructure, and strategic partnerships with cybersecurity specialists while expanding real-world testing capabilities. Organizations that establish scalable validation frameworks and resilient digital architectures will achieve stronger deployment consistency and maintain long-term competitiveness in intelligent vehicle ecosystems.

AI Vision Processing Expansion: AI-enabled driver monitoring platforms are replacing conventional image-processing architectures, improving distraction detection accuracy by nearly 35% while reducing false alerts by approximately 25%. Regulatory safety requirements and software-defined vehicle development are accelerating deployment, prompting manufacturers to expand AI partnerships and standardize scalable software stacks that shorten validation cycles and improve fleet-wide update efficiency.

Integrated Cabin Sensing Platforms: Vehicle manufacturers are combining driver monitoring, occupant detection, and interior analytics into unified sensing platforms, reducing hardware complexity by around 20% and lowering wiring requirements by nearly 15%. China-based automotive electronics suppliers are increasing vertical integration, while OEMs restructure procurement toward centralized computing architectures that simplify production and reduce long-term maintenance costs.

Infrared Sensor Optimization: Infrared imaging adoption continues to increase as low-light detection performance improves by over 30% and night-time monitoring reliability exceeds conventional camera solutions by approximately 25%. Semiconductor supply normalization has accelerated production planning, encouraging companies to expand localized sensor manufacturing, strengthen supplier partnerships, and improve production resilience across multiple vehicle platforms.

Commercial Fleet Intelligence Adoption: Fleet operators are deploying driver monitoring systems alongside telematics and predictive safety analytics, reducing fatigue-related incidents by nearly 28% while increasing compliance reporting efficiency by about 22%. Labor shortages and stricter transport safety policies are encouraging logistics companies to automate driver risk assessment, leading technology providers to scale cloud-enabled fleet monitoring services and integrated operational dashboards.

Camera-Based Systems remain the leading segment due to proven scalability, broad OEM acceptance, and relatively lower integration costs across passenger vehicle platforms. More than 55% of installed driver monitoring solutions continue to rely primarily on camera-based architectures, supported by mature manufacturing ecosystems and straightforward integration with existing ADAS platforms. Infrared Systems maintain strategic importance for premium vehicles requiring reliable low-light monitoring, while Sensor-Based Systems continue supporting complementary driver behavior detection through steering and physiological inputs.

AI-Based Systems represent the fastest-growing segment as automakers transition toward intelligent, software-defined vehicle platforms. AI-enabled monitoring improves driver state recognition accuracy by approximately 35% while reducing processing delays by nearly 20%, creating measurable operational advantages. Hybrid Systems are gaining momentum by combining cameras, infrared imaging, and AI analytics to improve redundancy and functional safety. Companies are increasing investments in AI software optimization, strategic semiconductor partnerships, and integrated sensing platforms to strengthen product differentiation and accelerate deployment across mid-range and premium vehicle categories.

Passenger Vehicles account for the largest application segment because intelligent safety technologies are increasingly becoming standard equipment rather than premium options. Approximately 65% of new premium passenger vehicle launches now integrate advanced driver monitoring capabilities, supported by stricter vehicle safety expectations and expanding digital cockpit architectures. ADAS remains closely linked with this segment, as driver attention monitoring enhances overall system reliability and supports safer semi-automated driving functions.

Autonomous Vehicles represent the fastest-growing application as manufacturers prepare vehicles for higher automation levels requiring continuous driver readiness verification. Detection accuracy improvements exceeding 30% and system response enhancements approaching 20% are accelerating deployment in advanced mobility programs. Commercial Vehicles and Fleet Management continue expanding through telematics integration, automated compliance monitoring, and predictive safety management, particularly within logistics operations. Companies are strengthening software integration, expanding AI-enabled analytics, and collaborating with fleet technology providers to address evolving operational requirements while improving deployment efficiency.

Automotive OEMs remain the dominant end-user group because they integrate driver monitoring systems directly into vehicle design, enabling optimized performance, regulatory alignment, and seamless compatibility with ADAS platforms. More than 70% of advanced monitoring deployments originate during original vehicle manufacturing, allowing automakers to standardize intelligent cabin technologies across multiple vehicle models. Automotive Suppliers play a critical supporting role by delivering AI software, imaging sensors, processors, and integrated electronic control systems that strengthen OEM development capabilities.

Fleet Operators are emerging as the fastest-growing end-user segment as commercial organizations increasingly deploy connected safety technologies to improve operational efficiency. Fleet-wide monitoring reduces driver-related safety incidents by approximately 25%, while predictive analytics improve maintenance planning and compliance reporting efficiency by nearly 20%. Commercial Transport operators continue expanding investments in integrated telematics, whereas the Aftermarket segment focuses on retrofit solutions for existing vehicle fleets. Companies are responding through subscription-based software services, strategic ecosystem partnerships, customized fleet platforms, and modular product offerings that address diverse customer requirements.

North America accounted for the largest market share at 36.2% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a 13.4% CAGR between 2026 and 2033.

Advanced Vehicle Software Integration Drives Market Leadership

North America maintains the largest share of the Driver Monitoring Systems Market through strong adoption of intelligent safety technologies, high penetration of premium vehicles, and mature automotive software ecosystems. The region accounts for over 36% of global deployment, supported by rapid integration of AI-enabled cabin monitoring into next-generation vehicle platforms. Automotive manufacturers continue expanding strategic collaborations with semiconductor and software developers to accelerate system validation and deployment. During 2026, several OEMs increased investment in centralized vehicle computing platforms, reducing electronic control unit complexity by approximately 18% while improving software update efficiency. The combination of advanced manufacturing capabilities, established testing infrastructure, and evolving vehicle safety requirements continues reinforcing the region's competitive position.

United States Market Outlook: The United States remains the regional innovation center due to its strong automotive software ecosystem, AI development capabilities, and extensive autonomous vehicle testing programs. More than 70% of domestic premium vehicle launches incorporate advanced driver monitoring functions, while technology companies continue expanding partnerships with OEMs to integrate AI vision processing, cloud-connected diagnostics, and over-the-air software updates. Continued investment in intelligent mobility infrastructure strengthens commercialization across passenger and commercial vehicle platforms.

Regulatory Compliance Accelerates Intelligent Cabin Deployment

Europe continues strengthening its market position through mandatory vehicle safety requirements, advanced automotive engineering, and rapid deployment of intelligent cockpit technologies. The region contributes approximately 29% of global demand, supported by premium vehicle manufacturing and standardized safety validation processes. Automotive suppliers are expanding AI-based driver monitoring portfolios to align with evolving vehicle safety regulations. Recent manufacturing upgrades have improved integrated sensor production efficiency by nearly 20%, enabling faster deployment across multiple vehicle segments. Strong collaboration between OEMs, electronics manufacturers, and software providers is supporting scalable implementation while maintaining high functional safety standards.

Germany Market Outlook: Germany remains the region's technology leader through its concentration of premium vehicle manufacturers, automotive electronics expertise, and advanced engineering capabilities. Integrated driver monitoring technologies are now incorporated into a significant proportion of newly developed luxury vehicle platforms, while domestic suppliers continue investing in AI software optimization, infrared imaging, and intelligent cockpit integration. Strong industrial collaboration enables rapid commercialization of next-generation safety technologies across domestic and export markets.

Manufacturing Scale Supports Rapid Deployment

Asia-Pacific is becoming the fastest-expanding regional market through unmatched automotive manufacturing capacity, semiconductor production, and intelligent mobility investments. The region contributes approximately 33% of global production, supported by large-scale electronics manufacturing and expanding ADAS deployment across passenger vehicles. AI-enabled driver monitoring installations have increased by more than 30% across major manufacturing hubs as OEMs accelerate software-defined vehicle strategies. Continued investment in localized semiconductor fabrication and vehicle electronics production strengthens supply-chain resilience while reducing production lead times. The region's vertically integrated automotive ecosystem enables faster commercialization of advanced monitoring technologies.

China Market Outlook: China dominates regional deployment through high-volume vehicle manufacturing, integrated semiconductor supply chains, and aggressive intelligent mobility investment. More than one-third of globally manufactured driver monitoring systems are estimated to originate from Chinese production facilities. Domestic automakers continue strengthening partnerships with AI software developers and sensor manufacturers, enabling rapid deployment of intelligent cabin platforms across both electric and conventional vehicle portfolios while improving production efficiency.

Fleet Safety Modernization Expands Demand

South America is witnessing gradual adoption of driver monitoring technologies as commercial transportation modernization and vehicle safety initiatives gain momentum. The region represents approximately 6% of global deployment, with demand concentrated in commercial fleets, logistics operators, and premium passenger vehicles. Fleet operators increasingly integrate driver monitoring with telematics platforms, improving operational visibility and reducing driver-related incidents by nearly 18%. Infrastructure limitations and uneven technology adoption continue influencing deployment speed, yet manufacturers are expanding regional partnerships and localized technical support to improve implementation efficiency and customer adoption.

Brazil Market Outlook: Brazil leads regional demand through its established automotive manufacturing sector, expanding logistics industry, and increasing investment in connected fleet technologies. Commercial transport operators are adopting AI-enabled driver monitoring to strengthen operational compliance and fleet safety performance. Domestic vehicle assembly facilities continue integrating advanced electronic safety platforms, while technology providers expand service networks and software support capabilities to accelerate implementation across large transportation fleets.

Infrastructure Modernization Encourages Intelligent Mobility

The Middle East & Africa market is progressing through transportation modernization, commercial fleet digitization, and increasing investment in intelligent mobility infrastructure. The region accounts for approximately 4% of global deployment, with adoption centered on premium vehicles, logistics fleets, and government-supported mobility initiatives. Fleet digitalization programs have improved operational monitoring efficiency by around 20%, encouraging broader deployment of AI-enabled driver monitoring technologies. Automotive technology suppliers are expanding regional partnerships, technical training, and system integration capabilities to support evolving transportation requirements while improving long-term deployment consistency.

United Arab Emirates Market Outlook: The United Arab Emirates remains the leading regional market due to its advanced transport infrastructure, connected mobility initiatives, and rapid adoption of intelligent fleet management technologies. Commercial operators increasingly deploy AI-enabled driver monitoring systems within logistics and public transport fleets to improve safety performance and operational oversight. Continued investment in smart mobility ecosystems and advanced transportation technologies positions the country as a regional reference point for intelligent vehicle safety deployment.

The Driver Monitoring Systems Market is led by Continental AG, Bosch, Valeo, Denso Corporation, and Aptiv, while regional electronics manufacturers compete on cost and localized integration. Global technology leaders compete with regional suppliers through AI software capability, sensing accuracy, and vehicle platform compatibility, whereas OEM-aligned suppliers challenge independent technology vendors through long-term development contracts. The top five companies collectively control approximately 49% of the market. Competition increasingly depends on AI detection precision exceeding 95%, software validation speed improving nearly 25%, and production localization reducing supply lead times by around 20%. Companies are expanding engineering centers, forming semiconductor partnerships, integrating camera and infrared technologies, and strengthening vertical software capabilities to secure multi-year OEM programs. The competitive landscape is shifting toward software-defined vehicle platforms where integrated sensing ecosystems outperform standalone hardware. High functional safety certification requirements, AI training complexity, and automotive qualification standards create significant entry barriers. Winning requires scalable AI software, resilient supply chains, rapid validation, and deep OEM collaboration.

Continental AG

Robert Bosch GmbH

Valeo

Denso Corporation

Aptiv PLC

Magna International Inc.

Smart Eye AB

Seeing Machines Limited

Cipia

Mobileye

LG Innotek

Visteon Corporation

Forvia

Veoneer

AI-powered vision systems, infrared imaging, and edge computing have become the technological foundation of advanced driver monitoring. AI-based facial analysis improves driver state recognition by approximately 35% compared with conventional rule-based image processing while reducing false alerts by nearly 25%. More than 60% of newly developed premium vehicle platforms now integrate intelligent cabin monitoring with centralized computing architectures. These technologies improve operational reliability, simplify software maintenance, and strengthen compliance with advanced vehicle safety requirements, giving leading automotive suppliers and OEMs stronger competitive differentiation.

Emerging innovation is centered on multimodal sensing that combines cameras, infrared sensors, radar, and biometric analytics into unified cabin intelligence platforms. Compared with legacy single-camera systems, integrated architectures reduce processing latency by around 20% while improving low-light detection performance by over 30%. Automotive manufacturers increasingly deploy software-defined vehicle platforms supporting over-the-air updates, enabling continuous algorithm improvements without hardware replacement. Suppliers with strong AI software expertise benefit from shorter product development cycles and greater compatibility across multiple vehicle platforms.

Between 2026 and 2028, embedded AI accelerators, 3D occupant sensing, and predictive behavioral analytics will reshape intelligent cockpit development. Deployment across next-generation vehicle platforms is expected to exceed 70% as centralized electronic architectures replace distributed control units. Companies investing early in scalable software ecosystems, secure edge processing, and semiconductor partnerships will achieve faster validation, stronger lifecycle management, and sustainable competitive advantage as intelligent mobility platforms become increasingly software driven.

November 2024: Continental AG introduced its Invisible Biometrics Sensing Display, integrating a 1.5 MP near-infrared camera behind the display for seamless driver and occupant monitoring, enhancing cabin design flexibility and advanced safety performance. Source: https://www.continental.com

March 2025: Cipia partnered with Arm to optimize its Driver Sense platform on Arm Cortex CPUs, improving AI processing efficiency while maintaining high driver monitoring performance, enabling faster integration into next-generation automotive platforms.

April 2025: Smart Eye aligned its Driver Monitoring System roadmap with Euro NCAP 2026 protocols, supporting a new 25-point safety assessment framework that strengthens OEM compliance and accelerates deployment of intelligent in-cabin monitoring technologies. Source: https://www.publicnow.com

July 2026: The European Union expanded General Safety Regulation requirements, making driver distraction monitoring mandatory for 100% of newly registered passenger vehicles, significantly accelerating OEM implementation and supplier demand across the automotive industry. Source: https://www.roadandtrack.com

The report provides comprehensive analysis of the Driver Monitoring Systems Market across Camera-Based Systems, Sensor-Based Systems, AI-Based Systems, Infrared Systems, and Hybrid Systems, with detailed assessment of Passenger Vehicles, Commercial Vehicles, Fleet Management, Autonomous Vehicles, and ADAS applications. It further evaluates Automotive OEMs, Fleet Operators, Commercial Transport, Automotive Suppliers, and Aftermarket demand across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. The study analyzes deployment trends, technology adoption patterns, competitive benchmarking, and evolving intelligent cabin architectures influencing more than 60% of new premium vehicle platforms.

The report delivers strategic insights into AI-enabled sensing technologies, software-defined vehicle integration, regional manufacturing capabilities, supply-chain evolution, regulatory developments, and enterprise investment priorities between 2026 and 2033. It supports expansion planning, competitive positioning, product portfolio optimization, partnership evaluation, and investment decision-making while identifying emerging deployment opportunities, operational shifts, and innovation priorities shaping the future of intelligent automotive safety systems.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 3300 Million |

Market Revenue in 2033 | USD 8054.68 Million |

CAGR (2026 - 2033) | 11.8% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Continental AG, Robert Bosch GmbH, Valeo, Denso Corporation, Aptiv PLC, Magna International Inc., Smart Eye AB, Seeing Machines Limited, Cipia, Mobileye, LG Innotek, Visteon Corporation, Forvia, Veoneer |

Customization & Pricing | Available on Request (10% Customization is Free) |