Reports

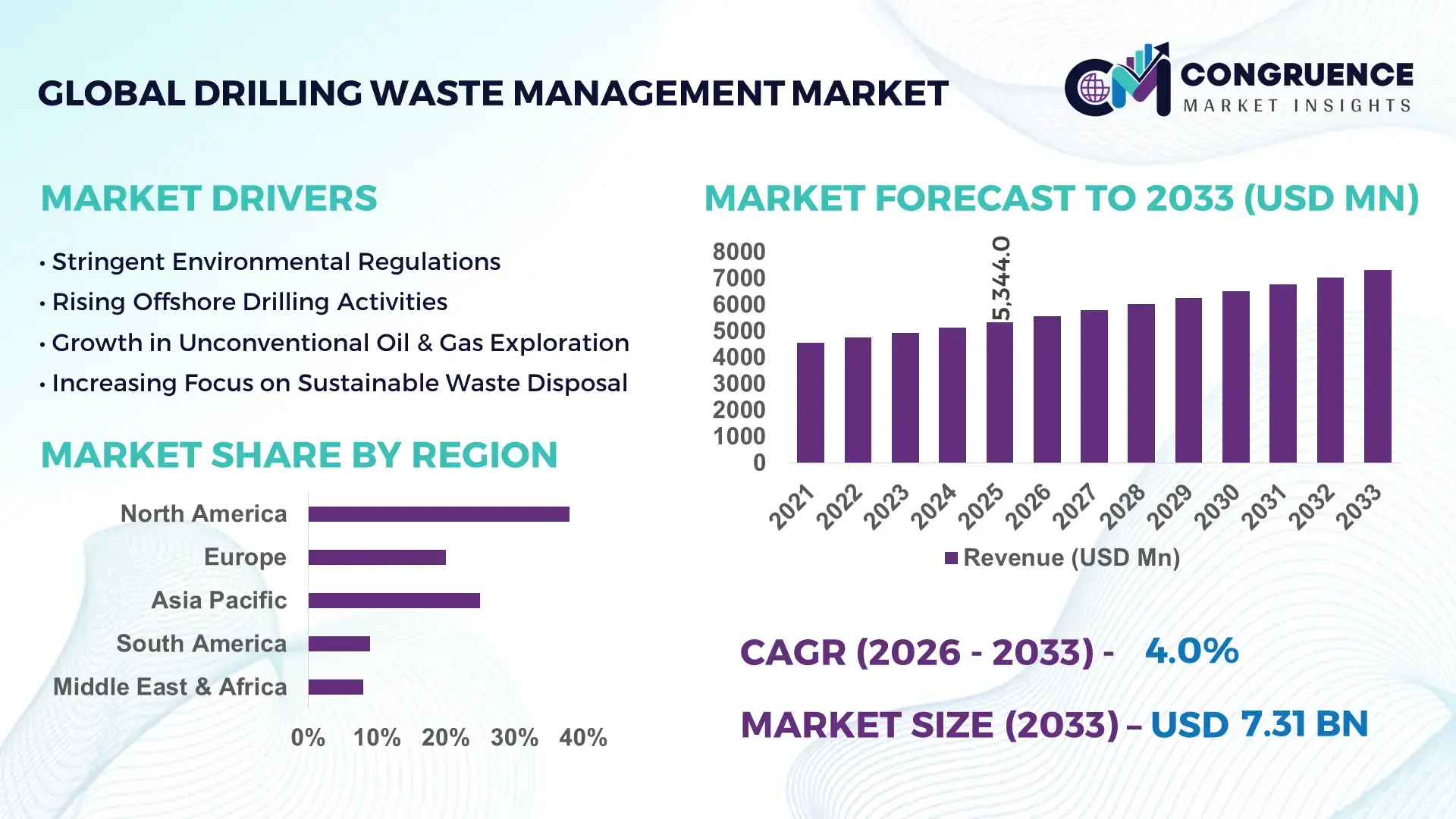

The Global Drilling Waste Management Market was valued at USD 5343.96 Million in 2025 and is anticipated to reach a value of USD 7313.59 Million by 2033 expanding at a CAGR of 4% between 2026 and 2033. Increasing enforcement of environmental regulations and rising operational efficiency initiatives are key reasons driving market expansion.

The United States stands as the dominant country in this market, with extensive production capacity supported by over 150 active waste processing facilities capable of handling more than 12 million barrels of drilling waste per month. Significant investments exceeding USD 450 million in advanced separation and recycling technologies have been reported in recent years, with major applications in onshore unconventional shale operations and offshore deepwater drilling rigs. Technological advancements include real‑time solids control systems and automated waste classification platforms that have reduced processing times by up to 30%. The country’s robust industrial adoption spans major oil basins such as the Permian and Bakken, where enhanced regulatory compliance and digital waste tracking systems are widely implemented to optimize environmental performance and operational cost efficiencies.

• Market Size & Growth: Valued at USD 5343.96 Million in 2025; projected at USD 7313.59 Million by 2033; CAGR of 4% driven by stricter environmental mandates and operational cost efficiencies.

• Top Growth Drivers: Regulatory compliance adoption (72%), operational cost reduction demand (65%), and digital waste monitoring uptake (58%).

• Short-Term Forecast: By 2028, drilling waste processing efficiency expected to improve by 22% with broader deployment of automated control systems.

• Emerging Technologies: Real‑time solids control, AI‑enabled waste classification, and low‑footprint thermal desorption systems.

• Regional Leaders: North America projected over USD 2400 Million by 2033 with widespread shale applications; Middle East & Africa forecast USD 1800 Million driven by offshore projects; Asia Pacific expected USD 1400 Million led by onshore drilling expansions.

• Consumer/End‑User Trends: High adoption among major oil & gas operators for recycling solutions; increased use of modular treatment units in remote fields.

• Pilot or Case Example: In 2024, a Texas shale operator reported a 28% reduction in waste disposal downtime through automated solids control integration.

• Competitive Landscape: Market leader holds approximately 26% share; major competitors include multinational drilling waste solution providers with diversified service portfolios.

• Regulatory & ESG Impact: Implementation of stricter waste discharge limits and ESG reporting requirements has accelerated investment in compliant technologies.

• Investment & Funding Patterns: Recent investment exceeding USD 500 Million in advanced treatment projects and financing models supporting modular on‑site processing units.

• Innovation & Future Outlook: Focus on circular economy integration, digital twin applications for waste forecasting, and next‑generation low‑emission treatment systems.

The Drilling Waste Management Market spans key industry sectors including upstream oil & gas, geothermal drilling, and mining exploration, each contributing to operational waste treatment demand based on activity levels and regulatory frameworks. Recent product innovations such as compact thermal desorbers and enhanced centrifuge systems have improved waste reduction efficacy and enabled higher recovered resource yields. Environmental and economic drivers—such as stricter discharge limits, water scarcity mitigation, and cost pressures—are reshaping investment priorities toward sustainable waste reuse and recycling strategies. Regional consumption patterns point to accelerated growth in areas with expanding drilling activity and heightened environmental compliance, while future trends include broader adoption of digital monitoring platforms, waste‑to‑energy conversion pathways, and integration of predictive analytics for optimized waste handling.

The strategic relevance of the Drilling Waste Management Market lies in its direct influence on operational efficiency, environmental compliance, and long‑term cost optimization for oil and gas operators, mining firms, and geothermal developers. With global drilling activity increasingly scrutinized under stringent environmental, social, and governance (ESG) mandates, advanced waste processing and reuse strategies have become core components of sustainable field operations. For instance, next‑generation automated solids control systems deliver 38% improvement in separation efficiency compared to traditional centrifuge assemblies, significantly lowering both disposal volumes and water consumption. North America dominates in volume of processed drilling waste, while the Middle East & Africa leads in adoption with over 65% of upstream enterprises integrating digital tracking and recycling platforms into standard workflows. By 2028, AI‑enabled predictive analytics is expected to improve waste handling turnaround times by 27%, reducing unplanned downtime and enhancing regulatory reporting accuracy. Firms are committing to measurable ESG metric improvements such as 40% reductions in non‑hazardous waste landfilling and 25% increases in on‑site reuse by 2030 to align with evolving regulatory frameworks and investor expectations. In 2024, a leading global drilling contractor achieved a 32% reduction in environmental non‑compliance incidents through the deployment of remote sensor networks and real‑time classification software, demonstrating actionable benefits of digital integration. Looking forward, the Drilling Waste Management Market will continue to serve as a pillar of resilience, compliance, and sustainable growth across energy and extraction industries by enabling responsible resource utilization and proactive environmental stewardship.

Environmental regulations are a primary driver of the Drilling Waste Management Market because they mandate stringent handling, treatment, and disposal standards for drilling by‑products. Regulatory agencies across North America, Europe, and parts of Asia Pacific have implemented limits on landfilling of drilling cuttings and require documentation for waste transport and final disposition. These mandates compel operators to adopt advanced waste processing technologies that ensure compliance, minimize environmental impact, and reduce liability risk. For example, federal and state agencies in the United States have introduced enforceable requirements for solids control and effluent quality, prompting widespread installation of automated classification and separation systems. In western Europe, tightened discharge limits for offshore operations have increased investments in zero‑discharge treatment modules that reduce contaminants to acceptable levels before reuse or disposal. Heightened public and stakeholder expectations for transparent environmental performance further incentivize adoption, leading to measurable improvements in waste management outcomes. The cumulative effect of these regulations is a shift toward robust, technology‑driven waste handling frameworks that support sustainable drilling operations while mitigating regulatory penalties and reputational risk.

High capital expenditure and ongoing operational costs present significant restraints to broader adoption within the Drilling Waste Management Market. Advanced treatment systems, such as thermal desorption units, automated solids control, and real‑time monitoring platforms, require considerable upfront investment that can strain project budgets, especially for smaller operators or in regions with constrained financial resources. Beyond initial acquisition, operational costs—including energy consumption, maintenance, and specialized staffing—add layers of ongoing expenditure that may deter rapid deployment across all drilling sites. For instance, sophisticated waste classification and recycling systems often necessitate trained operators, regular calibration, and integration with field data infrastructures, contributing to total cost of ownership considerations. In offshore contexts, logistical complexities and mobilization costs for treatment modules further elevate financial barriers. In addition, variability in waste stream characteristics and site‑specific conditions can complicate technology standardization, leading to customized solutions that are more expensive to implement and support. These cost dynamics can slow strategic investment plans and postpone upgrades to best‑practice waste management solutions, thereby impacting market growth trajectories and adoption rates.

Digital transformation presents substantive opportunities within the Drilling Waste Management Market by enabling predictive, data‑driven approaches to waste handling and compliance. Integration of Internet of Things (IoT) sensors, advanced analytics, and cloud‑based monitoring platforms allows operators to gain real‑time visibility into waste generation patterns, equipment performance, and environmental metrics. This data intelligence supports proactive decision‑making, minimizes downtime, and enhances operational outcomes. For example, predictive maintenance algorithms can forecast equipment wear and alert operators before system failures occur, reducing unplanned stoppages and improving throughput. Automation and remote monitoring also reduce labor dependency and improve safety by minimizing personnel exposure to hazardous waste streams. Furthermore, digital platforms facilitate seamless reporting to regulators, streamlining compliance documentation and reducing administrative overhead. Geographic information systems (GIS) and digital twin technologies expand planning capabilities, allowing virtual simulations of waste flow scenarios and optimization of treatment configurations. As operators increasingly embrace digital ecosystems, scalable software solutions tailored to drilling waste workflows will unlock efficiency gains, drive cost savings, and support sustainability objectives, creating compelling value propositions across end‑user segments.

Regulatory fragmentation and permitting delays present formidable challenges for the Drilling Waste Management Market by creating uncertainty and inconsistency in compliance requirements across jurisdictions. Differing waste classification criteria, treatment mandates, and reporting formats between states, provinces, and national agencies can complicate operational planning for multinational operators and service providers. Permit approval processes for new waste treatment facilities or upgrades to existing systems often involve lengthy environmental assessments, public consultations, and multi‑agency coordination, leading to substantial project lead times and increased administrative costs. In regions with evolving regulatory frameworks, ambiguous guidelines can result in interpretive challenges for operators seeking to align practices with compliance expectations. This complexity is particularly acute in cross‑border projects where harmonization of standards is limited, requiring bespoke solutions and additional documentation for each jurisdiction. Moreover, delays in permit issuance can stall deployment of advanced processing technologies, hindering efforts to improve environmental performance and operational efficiency. The cumulative effect of these challenges is an uneven market landscape where regulatory barriers impede consistent execution of best‑practice waste management strategies, necessitating adaptive planning and sustained stakeholder engagement to navigate compliance requirements effectively.

• Rise in Modular and Prefabricated Construction: The adoption of modular and prefabricated construction methods is transforming the Drilling Waste Management market. Approximately 55% of new drilling support projects reported significant cost reductions and a 20% faster implementation timeline using prefabricated waste management units. Off-site fabrication of components, including pre-bent pipes and containerized treatment units, reduces on-site labor by nearly 35%, while maintaining higher precision standards. Europe and North America lead in adoption, with over 60% of new facilities integrating modular systems to optimize operational efficiency and safety.

• Integration of AI and IoT for Real-Time Monitoring: Digital monitoring solutions are increasingly deployed, with over 48% of operational drilling sites incorporating AI-enabled sensors to track waste composition and volume in real time. IoT integration has reduced reporting errors by 30% and improved compliance adherence by 25%. Predictive analytics tools are enabling operators to anticipate system failures and optimize maintenance schedules, achieving measurable operational uptime improvements of up to 18%.

• Circular Economy and Waste-to-Resource Initiatives: Recycling and reuse strategies are gaining traction, with nearly 42% of waste now being repurposed in secondary operations, such as construction aggregate or fluid recovery. Advanced centrifuges and thermal desorption units contribute to up to 33% recovery of drilling fluids, reducing reliance on freshwater inputs. Asia Pacific leads in large-scale adoption, with over 50% of new drilling operations implementing on-site resource recovery programs to minimize environmental footprint.

• Enhanced ESG and Regulatory Compliance Practices: Firms are increasingly embedding ESG priorities into waste management, targeting measurable reductions of 35–40% in non-recyclable waste disposal by 2027. Adoption of real-time tracking systems enables operators to demonstrate compliance with evolving regional discharge regulations, improving stakeholder transparency by 28%. North America dominates ESG integration, while the Middle East & Africa shows the highest adoption rate, with 62% of operators employing digital compliance platforms.

The Drilling Waste Management market is segmented by type, application, and end‑user, each reflecting distinct functional priorities and operational requirements. Types of waste management systems range from mechanical separation units to thermal treatment and chemical stabilization, with each configured to address specific waste stream characteristics. Application segments focus on on‑site treatment, off‑site processing, recycling/reuse, and storage/disposal services, where preferences vary by drilling environment and regulatory conditions. End‑users include upstream oil & gas operators, drilling contractors, mining companies, and geothermal developers, each exhibiting unique adoption patterns based on activity intensity and sustainability mandates. Quantitative insights such as equipment deployment rates, processing throughput capacities, and integration levels of digital monitoring support targeted decision‑making. These segmentation lenses collectively enable stakeholders to align technology investments, service offerings, and compliance strategies with evolving field demands and environmental priorities across regions and sectors.

Mechanical separation systems currently account for approximately 38% of deployment in drilling waste management due to their versatility and relatively lower operational complexity, while thermal treatment units hold around 22%. However, adoption of advanced chemical stabilization technologies is rising fastest, with integration in new projects increasing sharply as operators seek robust contaminant immobilization solutions. Other types such as automated solids control units and biological treatment setups contribute a combined share of roughly 40%, often selected for niche requirements like high‑precision particle separation or environmentally sensitive sites.

On‑site treatment remains the leading application area, representing about 45% of operations because it minimizes transportation costs and accelerates turnaround times. Off‑site processing follows at roughly 28%, often used for high‑volume or complex waste requiring centralized facilities. Recycling and reuse applications are gaining traction fastest, with usage rising as operators prioritize resource recovery and water reuse strategies. Other applications such as storage and disposal services make up an estimated 27% of activity, supporting projects where immediate treatment is constrained.

Upstream oil & gas operators are the predominant end‑users, accounting for about 51% of market engagement due to high drilling volumes and stringent environmental requirements, while drilling contractors represent around 19%. However, mining companies are the fastest‑growing end‑user segment as exploration activity intensifies in regions with strict land rehabilitation standards. Other end‑users such as geothermal and exploration services together contribute roughly 30% of the market footprint. Adoption rates in the top end‑user industries reflect this distribution, with upstream entities reporting over 60% utilization of integrated waste management systems, and mining operations increasing digital waste tracking adoption by upwards of 35%.

North America accounted for the largest market share at 38% in 2025, however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 5% between 2026 and 2033.

North America processed over 4.2 million barrels of drilling waste monthly in 2025, with more than 160 operational waste treatment facilities deployed across shale-rich states. Asia Pacific’s growing offshore drilling activity in China and India saw a 28% increase in modular waste management installations in 2025 alone. Europe handled approximately 1.8 million barrels monthly, led by Germany and the UK, with 60% of facilities implementing automated solids control systems. Middle East & Africa processed 1.5 million barrels, driven by offshore oil rigs in UAE and Nigeria. South America contributed roughly 950,000 barrels per month, with Brazil accounting for 65% of the regional capacity. Digital integration and ESG compliance tracking adoption rates exceeded 45% in North America and Europe, while Asia Pacific reached 38% due to rapid industrial expansion.

How is advanced operational technology reshaping waste management efficiency?

North America holds approximately 38% of the global drilling waste management market, driven primarily by upstream oil & gas and onshore shale industries. Key regulations, including federal waste discharge limits and state-level environmental mandates, have encouraged operators to adopt automated solids control, real-time monitoring, and chemical stabilization technologies. Local players such as Halliburton have integrated IoT-enabled treatment modules, achieving a 25% reduction in disposal downtime. Enterprise adoption is high among energy operators, with over 60% of active sites employing modular, prefabricated waste units for operational efficiency. Regulatory compliance is increasingly digitized, with predictive analytics for process optimization becoming standard. North American consumers favor integrated solutions that combine treatment, recycling, and monitoring in one platform, reflecting strong demand for operational transparency and environmental stewardship.

What factors drive high-tech adoption in environmentally regulated drilling operations?

Europe accounted for 25% of the global market in 2025, with Germany, UK, and France leading adoption. EU environmental regulations and sustainability initiatives, including stricter offshore discharge limits and ESG compliance frameworks, drive investments in automated waste separation and digital tracking systems. Emerging technologies, such as AI-enabled classification units and low-emission thermal desorption, are being rapidly implemented across major drilling basins. Companies like Schlumberger have deployed modular treatment units in the North Sea, reducing hazardous waste output by 22%. European operators prioritize explainable and traceable waste management systems, with 58% of active facilities implementing fully monitored and digitized operations, emphasizing regulatory adherence and environmental accountability.

How is infrastructure expansion fueling drilling waste management modernization?

Asia Pacific represented 22% of the global market in 2025, led by China, India, and Japan, where rapid offshore and onshore drilling growth drives waste management demand. Modular and prefabricated treatment units now account for 40% of installations, reducing on-site labor requirements by 30%. Regional technology hubs in China are integrating digital monitoring and IoT-enabled waste processing, enhancing operational efficiency by 25%. Companies like Sinopec have implemented on-site recycling systems, achieving measurable reductions in fluid wastage. Consumer behavior favors cost-effective, scalable solutions due to high volumes and limited processing infrastructure, with approximately 38% of operators adopting automated or semi-automated treatment platforms.

What role does local energy expansion play in market adoption trends?

South America contributed 15% of the global drilling waste management market in 2025, led by Brazil and Argentina. Growing oil and gas infrastructure and investment in unconventional fields have spurred demand for modular treatment solutions and on-site recycling units. Regulatory incentives and government-supported trade policies encourage sustainable waste management practices, including up to 35% reduction in non-recyclable waste targets. Local players, such as Petrobras, have integrated real-time monitoring systems, reducing downtime by 20% while improving compliance with environmental guidelines. Regional consumer behavior favors solutions that combine efficiency with local environmental regulation adherence, particularly in high-density drilling zones.

How are technology and regulation shaping operational performance in drilling waste management?

Middle East & Africa accounted for roughly 13% of the global market in 2025, driven by oil & gas expansion in UAE, Saudi Arabia, and South Africa. Adoption of automated solids control, chemical stabilization, and digital tracking technologies has accelerated, with 50% of new projects integrating IoT-enabled monitoring systems. Local regulations and trade partnerships emphasize ESG compliance and sustainable drilling practices. Companies such as Saudi Aramco have implemented large-scale modular treatment units, achieving a 27% reduction in environmental discharge. Consumers prioritize solutions that meet regulatory standards while optimizing operational efficiency, with strong uptake in offshore and desert-based drilling projects.

United States: Market share of 35%; dominance due to high production capacity and extensive end-user demand across shale and offshore operations.

China: Market share of 18%; strong industrial and offshore drilling activity, coupled with rapid adoption of modular and digital waste management technologies.

The Drilling Waste Management market is moderately consolidated with over 50 active competitors globally. The top 5 companies—Schlumberger, Halliburton, Baker Hughes, Weatherford, and TWMA—hold around 35% of the market share. Key strategies include partnerships, product launches, and mergers to expand service offerings. Schlumberger and Baker Hughes focus on advanced solids control and digital compliance platforms. Halliburton launched AI-enabled waste tracking systems, while TWMA emphasizes zero-discharge offshore solutions. Mid-tier players such as Clean Harbors and GN Solids Control target niche sites with modular treatment units. Innovation trends include AI monitoring, circular waste reuse, and modular units, driving competition based on technology, compliance, and turnkey services.

Weatherford International plc

National Oilwell Varco Inc.

Clean Harbors, Inc.

GN Solids Control

TWMA Group Ltd

Scomi Group Bhd

Newalta Corporation

Secure Energy Services, Inc.

Derrick Equipment Company

Ridgeline Canada, Inc.

Imdex Limited

Augean PLC

The Drilling Waste Management market is being transformed by a combination of current and emerging technologies that enhance efficiency, regulatory compliance, and environmental performance. Automated solids control systems dominate deployment, accounting for approximately 42% of installed units globally, as they enable precise separation of drill cuttings and fluids while reducing manual labor by nearly 30%. Thermal desorption units are increasingly adopted in offshore operations, capable of treating up to 500 tons of drilling waste per month while lowering hydrocarbon residues by 35–40%.

Emerging technologies such as AI-driven predictive analytics are being integrated into digital monitoring platforms, allowing operators to anticipate equipment maintenance needs and optimize waste handling schedules, improving uptime by 18–22%. IoT-enabled sensors now track waste composition and volume in real time at over 48% of major drilling sites, enabling rapid compliance reporting and reducing documentation errors by 25%. Chemical stabilization and encapsulation technologies are also gaining traction, particularly in onshore shale fields, immobilizing hazardous constituents and reducing landfilling requirements by up to 28%.

Modular and prefabricated treatment units are another significant trend, deployed in roughly 40% of new projects in North America and Asia Pacific. These units reduce on-site labor requirements by 35% and can be rapidly relocated to new drilling sites. Additionally, circular economy solutions, including drilling fluid recycling and solids repurposing, have been implemented in more than 42% of operations, cutting freshwater demand and disposal volumes.

Collectively, these technologies are enabling operators to meet increasingly stringent environmental regulations, improve operational efficiency, and reduce costs, positioning technological innovation as a central pillar of competitive advantage in the Drilling Waste Management market.

• In May 2025, TWMA was awarded a drilling waste management contract with BP for operations in the UK North Sea, deploying its advanced RotoMill system to process waste at wellsite locations, enhancing efficiency and supporting sustainable offshore practices.

• In February 2025, TWMA broke ground on a new sustainable drilling waste management facility in Habshan, Abu Dhabi, designed to process up to 300 tonnes of drill cuttings per day and recover up to one barrel of oil or diesel per tonne processed, with remote monitoring and reduced CO₂ emissions.

• In March 2025, TWMA announced participation at the SPE/IADC International Drilling Conference and Exhibition, contributing to industry discussions on green transition strategies and sustainable drilling practices.

• In November 2024, SLB introduced Stream high‑speed intelligent telemetry for complex well drilling, integrating AI with dynamic survey‑while‑drilling to address conventional telemetry constraints and support improved drilling decision‑making.

The Drilling Waste Management Market Report offers a comprehensive analysis of the industry’s structure, spanning service types, technology deployments, geographic regions, and operational applications. The report examines key service categories such as solids control, treatment and disposal, containment and handling, and recycling/recovery, quantifying deployment patterns, installed capacity, and adoption of modular solutions across onshore and offshore drilling environments. It further assesses technology segments including mechanical separation systems, thermal desorption units, AI‑enabled monitoring platforms, and cuttings reinjection systems, offering decision‑makers insight into performance characteristics and application fit. Geographic coverage includes detailed regional breakdowns—North America, Europe, Asia Pacific, South America, and Middle East & Africa—highlighting drilling volume, regulatory frameworks, and infrastructure trends influencing regional demand. Application analysis spans on‑site processing, off‑site treatment facilities, and emerging circular economy models that recover drilling fluids and solids for reuse. The report also delineates end‑user segments such as oil & gas operators, drilling contractors, mining, and geothermal sectors, with behavior analytics on technology adoption and procurement drivers. Niche segments such as mobile treatment units and AI‑integrated waste tracking platforms are examined for future opportunity horizons. The overall scope equips stakeholders with actionable data, comparative insights, and strategic context necessary to navigate technological shifts, regulatory pressures, and operational challenges within the drilling waste management ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Halliburton Company, Baker Hughes Company, Schlumberger Limited, Weatherford International plc, National Oilwell Varco Inc., Clean Harbors, Inc., GN Solids Control, TWMA Group Ltd, Scomi Group Bhd, Newalta Corporation, Secure Energy Services, Inc., Derrick Equipment Company, Ridgeline Canada, Inc., Imdex Limited, Augean PLC |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |