Reports

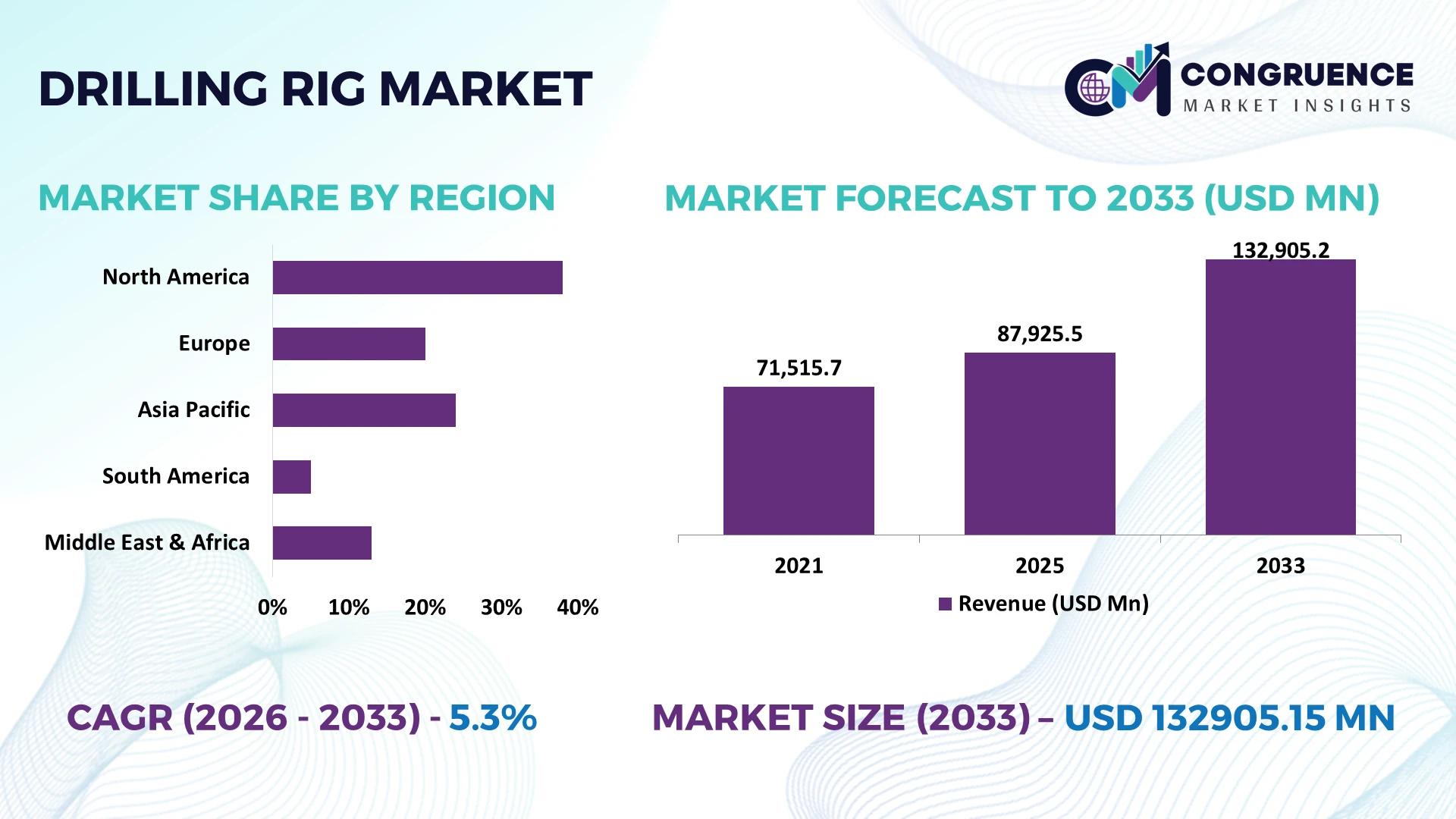

The Global Drilling Rig Market was valued at USD 87925.5 Million in 2025 and is anticipated to reach a value of USD 132905.15 Million by 2033 expanding at a CAGR of 5.3% between 2026 and 2033. Rising offshore exploration, shale development, automated drilling technologies, and expanding critical mineral extraction projects are accelerating deployment of advanced drilling rigs across global energy and mining operations.

The United States leads the global drilling rig market with approximately 28% of active drilling operations, supported by large shale reserves, offshore Gulf production, and more than 65% automated rig adoption across major operators. In comparison, Saudi Arabia continues expanding upstream capacity through strategic national investments, while geopolitical energy security initiatives have reinforced long-term drilling activity across key producing regions.

Strategic investment in intelligent, high-performance drilling fleets enables operators to improve operational resilience, optimize asset utilization, and strengthen long-term competitiveness.

Market Size & Growth: USD 87925.5 Million in 2025 is projected to reach USD 132905.15 Million by 2033 at a CAGR of 5.3%, driven by advanced drilling automation and offshore expansion.

Top Growth Drivers: Offshore drilling activity (+18%), rig automation (+22%), and unconventional resource development (+15%) continue accelerating global market expansion.

Short-Term Forecast: By 2028, drilling efficiency improves 20% while non-productive time declines 15% through predictive maintenance and digital monitoring.

Emerging Technologies: AI-powered drilling optimization, autonomous rigs, and digital twin platforms improve operational accuracy by more than 25%.

Regional Leaders: North America (~USD 42 Billion), Middle East (~USD 30 Billion), and Asia-Pacific (~USD 27 Billion) lead through offshore expansion and digital drilling adoption.

Consumer/End-User Trends: More than 60% of new drilling projects prioritize automated rigs to improve productivity and reduce operational downtime.

Pilot/Case Example: In 2025, AI-enabled drilling optimization projects reduced well completion time by approximately 18% across commercial operations.

Competitive Landscape: Leading companies hold nearly 45% market share, including SLB, Halliburton, Nabors Industries, Helmerich & Payne, and Patterson-UTI Energy.

Regulatory & ESG Impact: Low-emission drilling technologies reduce operational emissions by around 20% while supporting stricter environmental compliance.

Investment & Funding: More than USD 12 Billion supports fleet modernization, strategic partnerships, and regional expansion amid global supply-chain diversification.

Innovation & Future Outlook: Electrified rigs, remote operations, and AI-enabled drilling workflows accelerate next-generation productivity and strengthen strategic market positioning.

Drilling rig demand is expanding across offshore oil and gas fields, geothermal developments, and critical mineral exploration projects. AI-enabled drilling systems, predictive maintenance platforms, and electrified rig components are improving operational efficiency by nearly 20%, while localized manufacturing and evolving environmental regulations continue reshaping equipment procurement strategies, creating a stronger foundation for long-term strategic market development.

The drilling rig market has become strategically important as governments and energy companies prioritize supply security, domestic resource development, and operational resilience. Infrastructure modernization, increasing offshore developments, and digital drilling programs are reshaping competitive positioning, while supply-chain restructuring encourages localized manufacturing and long-term equipment partnerships. Operators are shifting capital toward high-efficiency rigs capable of supporting both conventional hydrocarbons and critical mineral exploration.

Modern AI-assisted drilling systems deliver up to 20% faster well construction and reduce non-productive time by nearly 15% compared with conventional manually optimized operations. The United States leads large-scale deployment through shale and offshore projects, whereas Norway emphasizes digitally integrated offshore platforms with lower operational emissions and higher automation intensity. Over the next two to three years, automated rig utilization is expected to exceed 70% across newly commissioned premium fleets, supported by expanding predictive maintenance capabilities.

A recent offshore deployment integrating automated pipe handling and real-time drilling analytics improved equipment utilization while reducing maintenance interventions. In response, major drilling contractors are expanding digital service portfolios, forming technology partnerships, and upgrading premium fleets to strengthen operational flexibility. Companies that integrate automation, workforce optimization, and data-driven drilling workflows will secure stronger competitive differentiation and long-term market relevance.

Automation is becoming the primary structural driver transforming drilling operations as operators target higher productivity and lower operating costs. Automated rig systems improve drilling efficiency by approximately 20%, while predictive maintenance reduces equipment downtime by nearly 15% and automated pipe handling lowers safety incidents by over 30%. The United States continues expanding digital drilling across shale basins, while Saudi Arabia accelerates intelligent rig deployment under upstream capacity expansion initiatives. These operational improvements are encouraging drilling contractors to modernize fleets through technology partnerships, software integration, and equipment upgrades. Companies investing early in intelligent drilling ecosystems are strengthening asset utilization and securing long-term service contracts in increasingly competitive energy markets.

High-value drilling components remain exposed to supply-chain disruptions, extended manufacturing lead times, and inflationary cost pressure. Delivery timelines for premium drilling equipment have increased by nearly 25% compared with pre-disruption levels, while specialized component costs remain approximately 15% higher across several supplier categories. The United States and selected European manufacturers continue facing shortages of advanced control systems and high-performance steel components, affecting fleet expansion schedules. In response, drilling companies are diversifying supplier networks, increasing local sourcing, and negotiating long-term procurement agreements to stabilize equipment availability. Strategic localization is becoming essential for maintaining deployment schedules and protecting operational profitability.

Growing investment in digital drilling platforms creates new opportunities beyond conventional oil and gas production. AI-assisted drilling optimization improves penetration rates by around 18%, while cloud-based operational monitoring increases asset utilization by approximately 20%. Australia and Canada are expanding drilling programs for lithium, copper, and other critical minerals, supported by resource security initiatives and advanced exploration technologies. Equipment manufacturers are increasing R&D spending, collaborating with software providers, and developing modular drilling solutions compatible with multiple resource applications. The convergence of automation, mineral exploration, and digital asset management is opening high-value business opportunities with stronger operational efficiency and broader equipment utilization.

The increasing sophistication of digital drilling environments is creating execution challenges related to workforce capability, cybersecurity, and integration across mixed equipment fleets. More than 40% of drilling contractors report shortages of skilled automation specialists, while connected operational systems increase cybersecurity exposure by over 30% compared with isolated legacy platforms. Norway and the United States are investing in workforce development alongside digital infrastructure to address these operational gaps. Companies must strengthen employee training, modernize legacy assets, and establish secure industrial data architectures through technology partnerships. Successfully integrating people, software, and intelligent equipment will determine long-term operational consistency and competitive leadership.

Digital Drilling Intelligence Expansion: AI-enabled drilling optimization, digital twins, and predictive maintenance are becoming standard across premium fleets. Automated drilling sequences improve penetration rates by nearly 20%, while real-time monitoring reduces unplanned downtime by approximately 15%. Driven by skilled labor shortages and higher productivity targets in the United States, contractors are expanding software partnerships and integrating cloud-connected drilling workflows to improve operational consistency and asset utilization.

Fleet Electrification and Emissions Control: Hybrid power systems, electrified rigs, and advanced energy management platforms are gaining traction as operators target lower fuel consumption. Modern electrified rigs reduce diesel usage by around 18% and operational emissions by nearly 20%, while automated power management improves energy efficiency by over 12%. Companies are accelerating fleet modernization and collaborating with equipment suppliers to meet evolving environmental requirements without compromising drilling performance.

Localized Supply Chain Strategies: Equipment manufacturers are restructuring procurement networks as supply-chain disruptions continue influencing project schedules. Local sourcing has increased by nearly 25% among major drilling contractors, while inventory planning reduces component shortages by approximately 18%. Operators in Saudi Arabia and the United States are expanding regional manufacturing partnerships and multi-supplier procurement models to improve delivery reliability and reduce operational delays.

Remote Operations Becoming Standard: Remote drilling control centers and connected field operations are transforming workforce deployment models. Remote monitoring lowers onsite staffing requirements by approximately 30% while improving operational response times by nearly 20%. Enterprise investment is shifting toward integrated communication platforms, cybersecurity, and centralized operations, allowing contractors to scale drilling activities across multiple sites with greater efficiency and workforce flexibility.

Land rigs remain the dominant segment, accounting for approximately 48% of total market deployment due to lower operating costs, faster mobilization, and extensive utilization across shale, conventional oil, and mineral exploration projects. Their modular configuration enables rapid relocation and supports high drilling frequency, particularly in the United States and the Middle East. Offshore rigs continue serving deepwater developments, while jack-up rigs remain preferred for shallow-water operations because of their cost-efficient deployment. Semi-submersible rigs deliver superior stability in harsh offshore environments, whereas drillships support ultra-deepwater exploration requiring advanced dynamic positioning capabilities.

Drillships represent the fastest-growing segment as deepwater discoveries and offshore licensing programs accelerate. Deployment of digitally integrated drillships has increased by nearly 18%, while automation features improve drilling efficiency by approximately 20%. Equipment manufacturers are prioritizing intelligent control systems, electrified power solutions, and long-term fleet modernization programs to strengthen competitiveness across offshore projects, while maintaining continued investment in high-performance land drilling platforms.

Oil exploration remains the largest application, representing approximately 52% of drilling rig utilization because of sustained upstream investment, field redevelopment, and offshore production expansion. Large-scale exploration campaigns in the United States, Saudi Arabia, and Brazil continue supporting high drilling intensity. Natural gas drilling remains strategically important as countries diversify energy supplies, while mining exploration benefits from increasing demand for critical minerals. Water well drilling maintains stable deployment across infrastructure and agricultural projects.

Geothermal drilling is the fastest-growing application as governments expand renewable energy portfolios and advanced drilling technologies reduce project complexity. Automated drilling systems improve geothermal drilling productivity by nearly 18%, while digital planning tools shorten well development timelines by approximately 15%. Equipment suppliers are introducing specialized drilling solutions, expanding engineering partnerships, and adapting rigs for multi-resource applications, allowing operators to improve utilization across conventional and emerging energy projects.

Oil & Gas remains the leading end-user, accounting for approximately 63% of drilling rig demand due to continuous upstream development, offshore investment, and unconventional resource production. High drilling intensity and extensive infrastructure requirements sustain equipment replacement and premium rig deployment. Mining remains an important buyer as exploration expands for lithium, copper, and other strategic minerals. Construction and Water Utilities maintain stable procurement for infrastructure development, groundwater access, and civil engineering applications.

Geothermal Energy represents the fastest-growing end-user segment as national decarbonization strategies encourage investment in renewable heat and power generation. Digital drilling technologies improve operational efficiency by approximately 20%, while automated rig systems reduce drilling time by nearly 15%. Equipment manufacturers are introducing customized rig configurations, expanding technology partnerships, and strengthening aftermarket service capabilities to address evolving operational requirements across both traditional and emerging end-user industries.

North America accounted for the largest market share at 38.4% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a 6.4% CAGR between 2026 and 2033.

Advanced Automation Strengthens Upstream Operations

North America maintains the largest share of the drilling rig market through extensive shale development, offshore production, and continuous fleet modernization. The United States and Canada collectively account for a significant concentration of active land rigs, while operators increasingly deploy AI-assisted drilling platforms and predictive maintenance systems to improve drilling precision. More than 65% of newly commissioned premium rigs incorporate automated drilling functions, reducing operational downtime and improving equipment utilization. Continued investment in digital oilfield infrastructure, drilling analytics, and electrified equipment supports higher operational efficiency. Enterprise collaboration between drilling contractors, software providers, and equipment manufacturers continues accelerating deployment of intelligent drilling solutions while strengthening supply-chain resilience through localized manufacturing and long-term procurement strategies.

United States Market Outlook: The United States remains the region's operational center due to extensive shale resources, offshore Gulf production, and advanced drilling technology adoption. More than 70% of premium drilling fleets deployed across major shale basins utilize digital drilling optimization and automated control systems. Leading contractors continue investing in intelligent rig upgrades, workforce digitalization, and predictive maintenance platforms, strengthening drilling productivity while improving operational safety and equipment availability.

Offshore Modernization Drives Technology Adoption

Europe continues strengthening its drilling capabilities through offshore modernization, digital asset management, and stricter environmental performance standards. Norway and the United Kingdom remain key offshore drilling hubs, where automated drilling technologies and remote operations improve productivity across mature offshore assets. Approximately 60% of new offshore equipment upgrades include digital monitoring capabilities, while hybrid power solutions reduce fuel consumption during drilling operations. Companies continue prioritizing intelligent drilling systems, integrated maintenance platforms, and equipment modernization to extend asset life and optimize offshore performance. Environmental compliance is also encouraging deployment of lower-emission drilling technologies across new and upgraded installations.

Norway Market Outlook: Norway leads regional innovation through advanced offshore operations, high digital maturity, and continuous investment in intelligent drilling infrastructure. Automated drilling technologies are deployed across a substantial share of offshore developments, improving drilling consistency and reducing maintenance interventions. National operators continue strengthening partnerships with technology providers to integrate remote monitoring, predictive analytics, and lower-emission drilling equipment into future offshore projects.

Industrial Expansion Accelerates Fleet Deployment

Asia-Pacific represents the fastest-expanding drilling rig market as governments increase domestic energy production, offshore exploration, and critical mineral development. China, India, and Australia continue investing in drilling infrastructure, while offshore licensing programs and mining exploration sustain equipment demand. Regional deployment of automated drilling systems has increased by approximately 22%, supported by expanding manufacturing capacity and technology localization. Equipment suppliers are establishing production facilities, engineering partnerships, and service networks closer to major drilling projects to improve delivery efficiency and reduce equipment lead times. Continued industrial expansion supports broader adoption of advanced drilling technologies across multiple resource sectors.

China Market Outlook: China continues expanding drilling operations through domestic energy security initiatives, offshore exploration, and strategic mineral development. Intelligent drilling systems are increasingly integrated into newly deployed rigs, with automated equipment adoption exceeding 40% across several large enterprise projects. Domestic manufacturers are strengthening research capabilities and expanding localized production to improve equipment competitiveness while reducing dependence on imported drilling technologies.

Offshore Exploration Supports Market Expansion

South America continues benefiting from offshore resource development, particularly across deepwater oil projects and expanding exploration activity. Brazil remains the regional leader through large offshore developments, while Argentina supports additional drilling demand through unconventional resource production. Offshore drilling deployment has increased by nearly 16% across key projects, encouraging investment in high-capacity drillships and digital drilling technologies. Infrastructure constraints and equipment availability remain operational challenges, prompting contractors to strengthen supplier partnerships and regional maintenance capabilities. Companies are focusing on fleet modernization and operational efficiency to improve project execution across increasingly complex offshore developments.

Brazil Market Outlook: Brazil remains the region's strongest drilling market through sustained offshore investment, advanced deepwater expertise, and large-scale production infrastructure. Digital drilling technologies continue improving offshore operational performance, while integrated maintenance systems reduce equipment downtime across major offshore fields. National operators and international contractors are expanding premium rig deployment and strengthening technology partnerships to improve long-term offshore productivity.

Strategic Capacity Expansion Drives Investment

The Middle East & Africa continues strengthening its position through upstream capacity expansion, drilling fleet modernization, and long-term energy infrastructure investment. Saudi Arabia, the United Arab Emirates, and selected African producers are increasing drilling activity to support production targets and resource development. Automated drilling technologies now support approximately 50% of newly upgraded premium rigs across leading operators, improving operational consistency and reducing drilling time. Equipment manufacturers continue expanding regional service facilities, engineering partnerships, and aftermarket support to improve equipment availability while reducing maintenance turnaround. Long-term infrastructure investment continues reinforcing drilling activity across both conventional and emerging resource projects.

Saudi Arabia Market Outlook: Saudi Arabia remains the region's largest drilling market due to extensive upstream development programs, modern drilling infrastructure, and sustained investment in intelligent drilling technologies. Large operators continue integrating automated rig controls, digital drilling analytics, and predictive maintenance platforms across expanding drilling fleets. Strong national investment priorities and long-term contractor partnerships continue strengthening operational efficiency while supporting future drilling capacity expansion.

The drilling rig market is led by SLB, Halliburton, Nabors Industries, Helmerich & Payne, and Patterson-UTI Energy, competing against regional drilling contractors and specialized offshore fleet operators. The top five players collectively control approximately 45% of the global market, creating intense competition between technology leaders and cost-focused regional providers. Premium operators compete through automation, digital drilling platforms, and integrated service offerings, while regional companies emphasize fleet flexibility and localized support. Automated drilling solutions improve operational efficiency by nearly 20%, and predictive maintenance reduces downtime by approximately 15%, making technology a stronger differentiator than pricing alone. Companies are expanding through strategic partnerships, fleet modernization, vertical integration, and digital service acquisitions to strengthen long-term contracts and asset utilization. Competitive momentum is shifting toward intelligent drilling ecosystems rather than standalone equipment ownership, increasing pressure on conventional fleet operators. High capital requirements, certification standards, and advanced software integration create substantial entry barriers. Success increasingly depends on combining automated operations, reliable service execution, digital capabilities, and scalable fleet performance.

SLB

Halliburton

Nabors Industries Ltd.

Helmerich & Payne, Inc.

Patterson-UTI Energy, Inc.

Transocean Ltd.

Valaris Limited

Seadrill Limited

Precision Drilling Corporation

KCA Deutag

Parker Drilling Company

Saipem S.p.A.

Digital transformation is redefining drilling operations through AI-driven drilling optimization, autonomous rig controls, predictive maintenance, and digital twin technology. More than 60% of newly deployed premium rigs incorporate connected monitoring systems, while predictive analytics reduces unplanned downtime by approximately 15%. Cloud-based operational platforms enable real-time performance optimization across multiple drilling sites, allowing contractors to improve equipment utilization and standardize workflows. Integrated data platforms are becoming a competitive requirement rather than an optional capability.

Compared with conventional manually optimized drilling, AI-assisted drilling systems improve drilling efficiency by nearly 20% while reducing well construction time by approximately 18%. Electrified rig power systems further reduce fuel consumption and emissions without affecting drilling performance. Large integrated contractors and offshore operators gain the greatest advantage because digital technologies improve asset productivity, strengthen maintenance planning, and support long-term service agreements across increasingly complex drilling environments.

Between 2026 and 2028, autonomous drilling workflows, edge computing, advanced robotics, and industrial cybersecurity will become core investment priorities. Remote operations, automated pipe handling, and intelligent decision-support platforms are expected to exceed 70% deployment across newly commissioned premium fleets. Companies investing early in integrated digital ecosystems, secure industrial connectivity, and intelligent fleet management will establish stronger operational resilience, higher drilling consistency, and sustainable competitive differentiation.

January 2024 SLB and Nabors Industries announced a strategic collaboration to integrate drilling automation platforms, improving interoperability between rig operating systems and accelerating digital drilling deployment across customer fleets. The integration targets broader automation adoption with platform-level compatibility improvements.

October 2024 Nabors Industries signed an agreement to acquire Parker Wellbore, expanding its global drilling, engineering, and project management capabilities. The transaction strengthened operations across more than 20 countries, enhancing integrated drilling and well construction services.

April 2025 Halliburton and Nabors completed the first fully automated surface and subsurface rotary and slide drilling execution in Oman using integrated automation technologies, delivering higher drilling consistency and lower non-productive time while earning the 2025 Digital Enabler of the Year recognition. Source: halliburton.com

February 2026 Nabors expanded its operational capabilities in Abu Dhabi through a larger technology-focused facility, strengthening regional repair, maintenance, and engineering support. The expansion increased local service capacity, improving response times and supporting faster fleet deployment across Middle East operations. Source: nabors.com

The report delivers comprehensive analysis of the global drilling rig market across equipment types, applications, end-users, and major geographical markets. It evaluates Land Rigs, Offshore Rigs, Jack-Up Rigs, Semi-Submersible Rigs, and Drillships, alongside Oil Exploration, Natural Gas Drilling, Geothermal Drilling, Mining Exploration, and Water Well Drilling applications. The assessment also covers demand across Oil & Gas, Mining, Geothermal Energy, Construction, and Water Utilities, while examining operational trends across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. More than 60% of premium fleet deployments now incorporate digital drilling capabilities, highlighting accelerating technology adoption.

The study provides strategic intelligence on automation, AI-enabled drilling, predictive maintenance, electrified rigs, remote operations, and fleet modernization. It benchmarks leading market participants, evaluates deployment patterns, competitive positioning, and technology adoption, and identifies emerging opportunities across critical mineral exploration and geothermal drilling. The analysis supports investment planning, product development, capacity expansion, partnership strategy, and long-term business decisions between 2026 and 2033 through detailed segmentation, regional comparisons, and operational performance insights.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 87925.5 Million |

Market Revenue in 2033 | USD 132905.15 Million |

CAGR (2026 - 2033) | 5.3% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | SLB, Halliburton, Nabors Industries Ltd., Helmerich & Payne, Inc., Patterson-UTI Energy, Inc., Transocean Ltd., Valaris Limited, Seadrill Limited, Precision Drilling Corporation, KCA Deutag, Parker Drilling Company, Saipem S.p.A. |

Customization & Pricing | Available on Request (10% Customization is Free) |