Reports

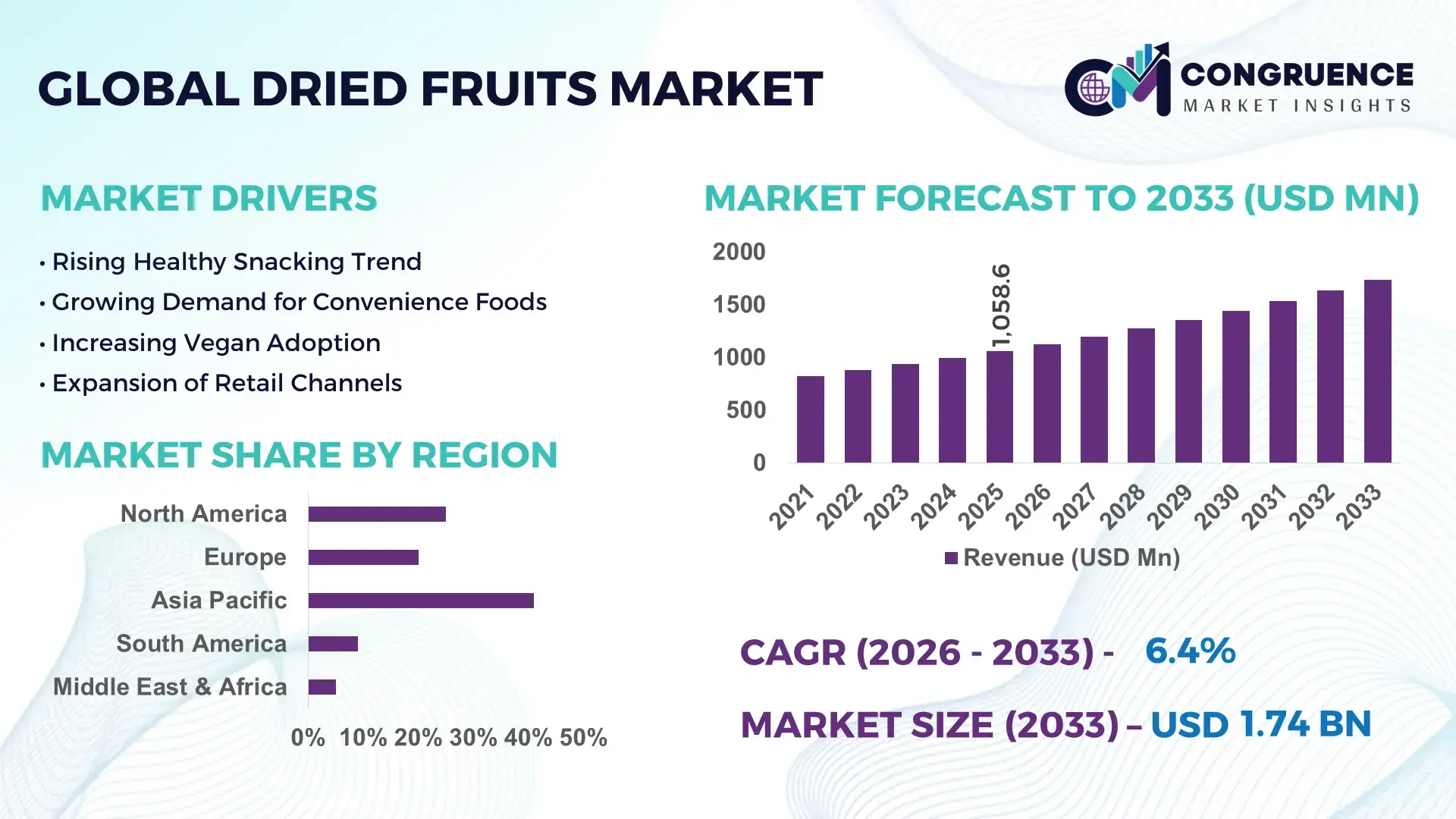

The Global Dried Fruits Market was valued at USD 1058.62 Million in 2025 and is anticipated to reach a value of USD 1738.89 Million by 2033 expanding at a CAGR of 6.4% between 2026 and 2033.

Market expansion is being directly influenced by advancements in dehydration technologies such as vacuum drying and freeze-drying, which improve nutrient retention by over 20% while reducing processing time by nearly 15%. Between 2024 and 2026, supply chain restructuring driven by trade realignments and climate variability has reshaped sourcing strategies, particularly impacting raisin and apricot exports from key producing regions.

China remains the dominant producer and processor, accounting for approximately 28% of global dried fruit output, supported by large-scale agricultural capacity and over USD 1.5 billion in recent food processing investments. The country’s integration of automated sorting and AI-based quality grading systems has increased export-grade yield by nearly 18%, positioning it ahead of traditional producers such as Turkey, which holds close to 20% share but relies more heavily on labor-intensive methods. This technological gap translates into a cost efficiency advantage of 10–12% for China in bulk export markets.

For stakeholders, this signals a clear shift toward technology-led competitiveness and geographically diversified sourcing strategies to mitigate supply volatility and maintain pricing stability.

Market Size & Growth: USD 1058.62M (2025) to USD 1738.89M (2033), CAGR 6.4%, driven by automated processing improving output efficiency by 15%.

Top Growth Drivers: Health-conscious consumption (+22%), processed food integration (+18%), export demand expansion (+16%).

Short-Term Forecast: By 2027, processing costs expected to decline by 12% due to energy-efficient drying systems.

Emerging Technologies: AI-based sorting, vacuum drying, and smart packaging adopted by over 35% of large processors.

Regional Leaders: Asia-Pacific (~USD 650M) driven by production scale; Europe (~USD 420M) via premium demand; North America (~USD 310M) through health snack adoption.

Consumer Trends: Over 48% of urban consumers prefer dried fruits as daily snack alternatives due to convenience and shelf stability.

Pilot Example: In 2025, a large-scale Turkish processing facility implemented AI grading, reducing waste by 14% and improving export quality compliance by 11%.

Competitive Landscape: Top player holds ~17% share; key companies include global exporters and vertically integrated processors dominating supply chains.

Regulatory & ESG Impact: Sustainability certifications increased adoption by 26%, driven by stricter EU import regulations on pesticide residues.

Investment & Funding: Over USD 2.3B invested globally in processing infrastructure and cold-chain upgrades between 2024–2026.

Innovation & Outlook: Shift toward organic and fortified dried fruits growing at 19%, aligning with premiumization and health-driven product positioning.

The market is structurally anchored by food processing (45%), retail packaged snacks (30%), and bakery and confectionery applications (25%), reflecting diversified end-use demand. Innovation is advancing through nutrient-enhanced variants and sugar-free processing techniques, improving product appeal by nearly 18%. Regionally, Asia-Pacific leads with over 40% consumption share, while Europe shows a 12% rise in organic dried fruit demand amid tightening food safety standards. A notable trend is the integration of traceability technologies to address supply chain disruptions linked to climate variability. These shifts position the market toward value-added, quality-driven expansion, setting the stage for strategic realignment across sourcing, processing, and product innovation.

The dried fruits market is rapidly transforming into a strategic battleground for global food companies as demand shifts toward shelf-stable, nutrient-dense products that align with modern consumption patterns and export resilience. With over 48% of urban consumers integrating dried fruits into daily diets, the category is no longer ancillary but central to high-growth snack and ingredient portfolios. This acceleration is further reinforced by the rising role of dried fruits in functional foods and clean-label product lines, where manufacturers are optimizing formulations to meet premium health standards. A critical shift is emerging from supply chain restructuring and stricter global food safety regulations, particularly across Europe and North America, forcing producers to upgrade processing standards and traceability systems. Freeze-drying technology improves nutrient retention efficiency by 25% while reducing processing cost by 14% compared to traditional sun-drying methods, fundamentally transforming product quality and scalability. Regionally, Asia-Pacific leads in volume with over 40% share, while Europe leads in innovation adoption with nearly 32% of processors implementing advanced grading and packaging technologies.

In the next 2–3 years, processing efficiency is projected to improve by 15%, while waste reduction initiatives are expected to lower raw material loss by 10%, directly enhancing margin structures. ESG compliance is emerging as a competitive lever, with sustainable sourcing and energy-efficient drying systems reducing operational costs by up to 12% while unlocking premium export markets. A 2025 case from a Middle Eastern processing hub demonstrated a 13% increase in export-grade output through AI-enabled sorting systems. Capital allocation is visibly shifting toward automation, regional processing hubs, and vertically integrated supply chains, as companies prioritize control over quality and cost. The market is no longer driven by volume alone but by the ability to optimize efficiency, ensure compliance, and capture premium positioning, making strategic investment in technology and supply chain resilience the defining factor for long-term competitiveness.

The primary growth engine is the convergence of rising health-conscious consumption and rapid advancements in processing technologies, which is accelerating both demand and supply-side transformation. Over 52% of consumers now actively seek natural, preservative-free snacks, directly increasing demand for dried fruits with clean-label positioning. Simultaneously, adoption of advanced dehydration methods has improved production efficiency by nearly 18%, enabling higher throughput and consistent quality. A key global trigger is the post-2024 supply chain restructuring, where producers are diversifying sourcing beyond climate-sensitive regions, reducing dependency risk by approximately 12%. This shift is forcing companies to invest aggressively in localized processing units and integrated supply networks. In response, leading players are expanding capacity through automated facilities and forming strategic partnerships with regional growers, ensuring stable raw material access while optimizing cost structures. The result is a synchronized expansion across production, processing, and distribution, reinforcing long-term market scalability.

The market faces significant constraints driven by raw material dependency and climate-induced supply volatility, which directly impact pricing and operational continuity. Approximately 65% of dried fruit production relies on a limited set of geographies, increasing exposure to weather disruptions that have caused yield fluctuations of up to 20% in recent cycles. Additionally, energy-intensive drying processes contribute to nearly 30% of total production costs, creating margin pressure in energy-volatile regions. Regulatory tightening, particularly on pesticide residues, has increased compliance costs by 10–15% for exporters targeting premium markets. These structural challenges are constraining scalability and delaying expansion timelines. To mitigate risks, companies are actively diversifying sourcing regions, entering long-term procurement contracts, and investing in alternative technologies such as solar-assisted drying systems. These measures are reducing dependency risk and stabilizing cost structures, but require significant upfront capital and strategic alignment.

High-impact opportunities are emerging at the intersection of advanced processing technologies, premium product innovation, and expansion into high-growth emerging markets. The adoption of AI-driven sorting and grading systems is improving product quality consistency by over 20%, enabling access to premium export segments. Meanwhile, demand for organic and fortified dried fruits is increasing at a rate exceeding 18%, creating new value-added product categories. A forward-looking innovation shift is the integration of smart packaging with moisture control and traceability features, enhancing shelf life by up to 25% and strengthening brand differentiation. Non-obvious upside lies in leveraging underutilized fruit varieties in emerging markets, unlocking cost advantages of nearly 15% compared to traditional sourcing. Companies are positioning for dominance by increasing R&D investments, expanding into untapped regions, and building ecosystem partnerships with agri-tech firms, ensuring long-term supply security and innovation leadership.

Execution challenges are increasingly centered around infrastructure limitations, scalability constraints, and the complexity of maintaining consistent quality across global supply chains. Nearly 40% of producers in developing regions lack access to advanced processing infrastructure, limiting their ability to meet international quality standards. Additionally, logistics inefficiencies contribute to post-processing losses of up to 12%, particularly in regions with inadequate cold-chain systems. A critical real-world pressure is the rising cost of energy, which has increased operational expenses by approximately 15% in key processing hubs. These barriers are constraining long-term growth consistency and limiting the ability to scale efficiently. To remain competitive, companies must invest in modern processing infrastructure, adopt energy-efficient technologies, and establish strategic logistics partnerships. Without these interventions, the gap between high-efficiency producers and traditional players will continue to widen, reshaping competitive dynamics and market access.

Automation adoption rises 35%, reducing sorting errors by 18% and processing time by 12%. Advanced AI-enabled grading and optical sorting systems are being deployed across large processing units, particularly in Asia and the Middle East. This shift is optimizing quality consistency and export compliance while lowering labor dependency amid rising workforce costs. Companies are scaling automated lines and integrating real-time monitoring to maintain throughput stability.

Energy-efficient drying technologies cut operational costs by 14% and energy use by 20%. Solar-assisted and hybrid dehydration systems are increasingly replacing conventional thermal drying, especially following energy price volatility triggered by global supply disruptions. This transition is reshaping cost structures and improving sustainability metrics. Producers are restructuring facilities and forming technology partnerships to accelerate adoption and meet regulatory efficiency benchmarks.

Premium and organic product lines expand 22%, with shelf-life improvements reaching 25%. Demand for chemical-free, traceable dried fruits is pushing companies to adopt advanced packaging solutions such as modified atmosphere systems. This shift is enhancing product longevity and supporting premium pricing strategies. Businesses are repositioning portfolios toward high-margin SKUs while aligning with tightening import regulations in developed markets.

Regional sourcing diversification increases by 17%, reducing supply risk exposure by 12%. Climate variability and geopolitical trade adjustments are forcing companies to shift procurement strategies beyond traditional supplier regions. This operational change is improving supply continuity but adding complexity to logistics networks. Firms are investing in multi-region sourcing contracts and localized processing hubs to stabilize input availability and maintain consistent output quality.

The dried fruits market is segmented across types, applications, and end-users, with demand concentrated in high-volume staple products and shifting toward value-added, premium segments. Raisins, dates, and apricots dominate supply due to scalability and cost efficiency, collectively accounting for over 60% of total demand. Applications are heavily anchored in snacks and food processing, representing more than half of consumption, while emerging categories such as dairy and cereals are expanding due to health-driven product innovation. End-user demand is led by the food and beverage industry, though retail and household consumption are gaining momentum with increasing preference for convenient, nutrient-dense foods. This segmentation highlights a clear transition from bulk commodity usage to differentiated, high-margin applications, prompting companies to realign production, diversify product portfolios, and target evolving consumption channels with precision.

Raisins dominate the segment with approximately 34% share, driven by their cost efficiency, long shelf life, and seamless integration across multiple food applications. Their scalability and established supply chains make them the preferred choice for bulk processing and export markets. In contrast, berries are the fastest-growing type, expanding at over 19%, fueled by rising demand for antioxidant-rich and premium snack options. This marks a structural shift from volume-driven consumption toward value-added, health-oriented products. Dates, holding close to 18% share, maintain strong regional dominance due to cultural consumption patterns and increasing use in natural sweeteners. Apricots and figs collectively account for around 28%, serving niche but high-value segments such as confectionery and specialty foods. The comparison between raisins and berries highlights a clear transition from cost leadership to premium differentiation. Companies are responding by expanding berry processing capacity and investing in product innovation, while maintaining raisin volumes for stable revenue streams. This shift signals a dual strategy: defend high-volume categories while aggressively capturing premium growth segments.

Snacks lead the application segment with approximately 38% share, driven by strong consumer preference for convenient, ready-to-eat healthy options. This dominance is reinforced by retail expansion and product diversification in urban markets. Food processing is the fastest-growing application, increasing at over 17%, as manufacturers incorporate dried fruits into functional foods, energy bars, and plant-based formulations. The comparison between snacks and bakery & confectionery reveals a shift from traditional indulgence-based consumption toward health-driven, multi-functional usage. Bakery and confectionery, along with dairy products and breakfast cereals, collectively contribute around 62%, maintaining steady demand due to established consumption patterns. However, dairy and cereal segments are gaining traction as companies innovate with fortified and protein-enhanced offerings. Businesses are adapting by scaling production for processed ingredients, reformulating products, and targeting health-conscious consumers. This evolution highlights a clear transition toward integrated food applications, where dried fruits serve both nutritional and functional roles.

The food and beverage industry leads with approximately 44% share, driven by large-scale procurement, consistent demand, and extensive application across product categories. Its dominance is rooted in high-volume usage and integration into processed food supply chains. Households are the fastest-growing end-user segment, expanding at over 18%, fueled by increasing health awareness and direct retail accessibility. Comparing the food and beverage industry with households reveals a shift from industrial consumption toward decentralized, consumer-driven demand. The retail sector, hospitality industry, and foodservice providers collectively account for around 56%, reflecting diverse consumption channels and growing reliance on packaged and ready-to-use products. Companies are responding by customizing packaging sizes, optimizing pricing strategies, and strengthening retail distribution networks. Partnerships with e-commerce platforms and retail chains are further enhancing market penetration. This shift underscores the importance of targeting both bulk buyers and end consumers, enabling companies to capture demand across multiple touchpoints.

Asia-Pacific accounted for the largest market share at 41% in 2025 however, Europe is expected to register the fastest growth, expanding at a CAGR of 7.1% between 2026 and 2033.

Asia-Pacific leads in production scale and consumption volume, driven by over 45% of global output capacity, while Europe captures nearly 28% share through premium, compliance-driven demand. North America holds approximately 18%, supported by high per capita consumption and strong retail penetration. Growth is accelerating in Europe due to stricter food safety regulations and rising organic demand, while Asia-Pacific continues to dominate supply. A key structural shift is the diversification of sourcing beyond climate-sensitive regions, reducing supply concentration risk by 12%. Companies are prioritizing Asia-Pacific for scale, Europe for innovation compliance, and North America for high-margin consumption.

What is driving premium consumption and operational transformation in high-value food markets?

North America holds approximately 18% of global demand, driven by strong consumption in packaged snacks and functional foods. Over 52% of consumers prefer clean-label and preservative-free products, accelerating demand for high-quality dried fruits. A key structural force is stricter labeling and traceability requirements, pushing companies toward transparency and quality assurance. Execution is shifting toward automated packaging and AI-based quality checks, improving operational efficiency by nearly 14%. A notable strategic move includes large-scale retail expansion, increasing shelf presence by 11% across major chains. Consumer behavior is premium-focused, prioritizing health benefits and convenience. This positions the region as a high-margin market where companies invest to capture value through quality differentiation and brand positioning.

How are regulatory standards and sustainability mandates reshaping product quality and supply chains?

Europe accounts for nearly 28% of the global market, led by countries such as Germany, France, and the UK. Stringent regulations on pesticide residues and sustainability compliance are increasing operational costs by 12–15%, forcing companies to upgrade sourcing and processing standards. Over 34% of producers have adopted certified organic and traceable supply chains to meet regulatory requirements. Operational shifts include advanced packaging and traceability systems, improving compliance efficiency by 16%. A key strategic move is the expansion of organic product lines, growing adoption by 21% among premium retailers. Consumer behavior is quality-first and compliance-driven, making this region a benchmark for innovation and regulatory alignment, compelling global players to adapt their standards.

Why is large-scale production and rapid consumption expansion redefining global supply leadership?

Asia-Pacific dominates with over 41% market share, supported by countries such as China and India, which lead in production and consumption. The region benefits from strong agricultural infrastructure and low-cost processing, contributing to over 45% of global supply. Execution is shifting toward mass automation and digital quality control, improving processing efficiency by 18%. A major strategic move includes capacity expansion projects increasing export output by 15% across key hubs. Consumer behavior prioritizes affordability and volume, while urban markets are shifting toward packaged and branded products. This makes Asia-Pacific critical for scale-driven strategies and global supply chain stability.

How are emerging consumption patterns balancing growth potential with structural limitations?

South America contributes approximately 7% to the global market, with Brazil and Chile as key players. Demand is driven by increasing urban consumption and export-oriented production, with consumption rising by 14% in key markets. However, infrastructure limitations and logistics inefficiencies increase supply chain costs by nearly 12%, constraining scalability. Execution is shifting toward localized processing and export-focused operations, improving efficiency by 10%. A strategic move includes investment in regional processing facilities to enhance export quality. Consumer behavior remains price-sensitive, favoring affordable bulk products. This positions the region as a high-potential but operationally constrained market requiring targeted investment.

What role do infrastructure investments and resource advantages play in shaping market transformation?

The Middle East & Africa region holds around 6% share, with demand concentrated in countries such as Turkey, Saudi Arabia, and the UAE. The market is driven by strong cultural consumption patterns and increasing use in foodservice and hospitality sectors. A key transformation driver is investment in modern processing infrastructure, improving production efficiency by 13%. Execution is shifting toward advanced sorting and packaging technologies, enhancing export quality standards. A notable strategic move includes regional partnerships expanding export capacity by 11%. Consumer behavior emphasizes traditional consumption with growing demand for packaged products. This positions the region as an emerging strategic hub with strong export potential.

China – 28% share in the Dried Fruits Market: Dominates due to large-scale production capacity and advanced processing infrastructure.

Turkey – 20% share in the Dried Fruits Market: Leads through strong export orientation and established global supply networks.

The competitive landscape is defined by global exporters, regional processing leaders, and vertically integrated agribusiness firms competing across cost efficiency, product quality, and supply chain control. Leading players such as Olam Group, Sun-Maid Growers, Bergin Fruit and Nut Company, Traina Foods, and National Raisin Company collectively account for approximately 42% of the market, reflecting moderate consolidation with strong regional influence. Competition is increasingly driven by technology adoption, where automated processing improves efficiency by 15%, and by supply chain optimization, reducing sourcing costs by up to 12%.

Global players compete with regional producers on scale and export reach, while smaller firms differentiate through organic and premium product lines. Strategic actions include capacity expansion, partnerships with growers, and vertical integration to secure raw material supply. A key competitive shift is the move toward technology-led processing and traceability, redefining quality benchmarks. Entry barriers are rising due to capital-intensive infrastructure and compliance requirements. Winning in this market requires control over sourcing, investment in advanced processing, and the ability to deliver consistent, high-quality products at scale.

Olam Group

Sun-Maid Growers of California

Bergin Fruit and Nut Company

Traina Foods Inc.

National Raisin Company

Lion Raisins Inc.

Del Monte Foods Inc.

Ocean Spray Cranberries Inc.

Royal Nut Company

Kiantama Oy

Paradise Fruits Solutions GmbH

Geobres Nemean Currants & Dried Fruits S.A.

Advanced dehydration technologies are reshaping processing efficiency and product quality across the dried fruits market. Vacuum drying and freeze-drying systems are now deployed by over 32% of large-scale processors, improving nutrient retention by 20–25% while reducing processing time by nearly 15%. These technologies are enabling premium-grade output and consistent quality, directly strengthening export competitiveness and pricing power. Emerging technologies such as AI-based optical sorting and automated grading are transforming operational precision. Adoption has crossed 35% among export-oriented facilities, reducing defect rates by 18% and improving yield efficiency by 12%. Integration with real-time data systems is optimizing throughput and minimizing waste. This shift is giving technologically advanced producers a clear advantage in compliance-heavy markets, where quality consistency determines access.

A key comparison highlights that freeze-drying improves product shelf life by 30% while lowering spoilage loss by 14% compared to traditional sun-drying methods. This transition is forcing a move away from labor-intensive processes toward capital-intensive, high-efficiency systems. Companies investing early in automation and smart processing infrastructure are capturing higher-margin segments, while traditional operators face declining competitiveness. Between 2026 and 2028, technology adoption is expected to accelerate further, with over 40% of processors integrating hybrid drying and smart packaging solutions. This evolution is optimizing supply chains, reducing operational variability, and enabling traceability. Acting now allows companies to secure cost advantages, meet tightening global standards, and position themselves in premium, high-growth product categories.

March 2026 – Olam Group expanded its dried fruit processing facility in Africa, increasing processing capacity by 18% and integrating automated grading systems. This move strengthens export efficiency and reduces post-harvest losses, enhancing supply reliability. [Capacity Expansion] Source: https://www.olamgroup.com

November 2025 – Sun-Maid Growers of California launched a new line of no-added-sugar dried fruit snacks, improving product shelf life by 22% through advanced packaging. This supports premium positioning and aligns with health-focused consumer demand. [Product Innovation] Source: https://www.sunmaid.com

July 2025 – Traina Foods Inc. partnered with a food-tech firm to implement AI-driven sorting, reducing processing defects by 16%. This improves quality consistency and strengthens competitiveness in export markets. [Tech Integration] Source: https://www.trainafoods.com

January 2024 – Paradise Fruits Solutions GmbH invested in freeze-drying technology, increasing production efficiency by 20% and expanding capacity for premium fruit inclusions. This enhances supply to bakery and cereal manufacturers. [Process Upgrade] Source: https://www.paradise-fruits.com

The report delivers comprehensive coverage across core segments, including types such as raisins, apricots, dates, figs, and berries; applications spanning snacks, bakery and confectionery, dairy products, breakfast cereals, and food processing; and end-users including households, food and beverage industry, retail, hospitality, and foodservice providers. It evaluates five major regions with detailed country-level insights and incorporates key technologies such as advanced dehydration, AI-based sorting, and smart packaging systems. Over 12 major companies are profiled, with segment-level demand distribution showing raisins leading with over 30% share and snacks accounting for nearly 38% of application demand.

Analytical depth is driven by measurable indicators, including adoption levels exceeding 35% for automated processing and over 40% consumption concentration in Asia-Pacific. The report also captures emerging niches such as organic and fortified dried fruits, which are expanding at double-digit adoption rates. With forward-looking coverage from 2026 to 2033, it enables strategic decision-making by identifying high-impact investment areas, supply chain shifts, and competitive positioning opportunities. This structured insight supports stakeholders in optimizing expansion strategies, aligning with regulatory changes, and capturing value in premium and technology-driven segments.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 1058.62 Million |

|

Market Revenue in 2033 |

USD 1738.89 Million |

|

CAGR (2026 - 2033) |

6.4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Olam Group, Sun-Maid Growers of California, Bergin Fruit and Nut Company, Traina Foods Inc., National Raisin Company, Lion Raisins Inc., Del Monte Foods Inc., Ocean Spray Cranberries Inc., Royal Nut Company, Kiantama Oy, Paradise Fruits Solutions GmbH, Geobres Nemean Currants & Dried Fruits S.A. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |