Reports

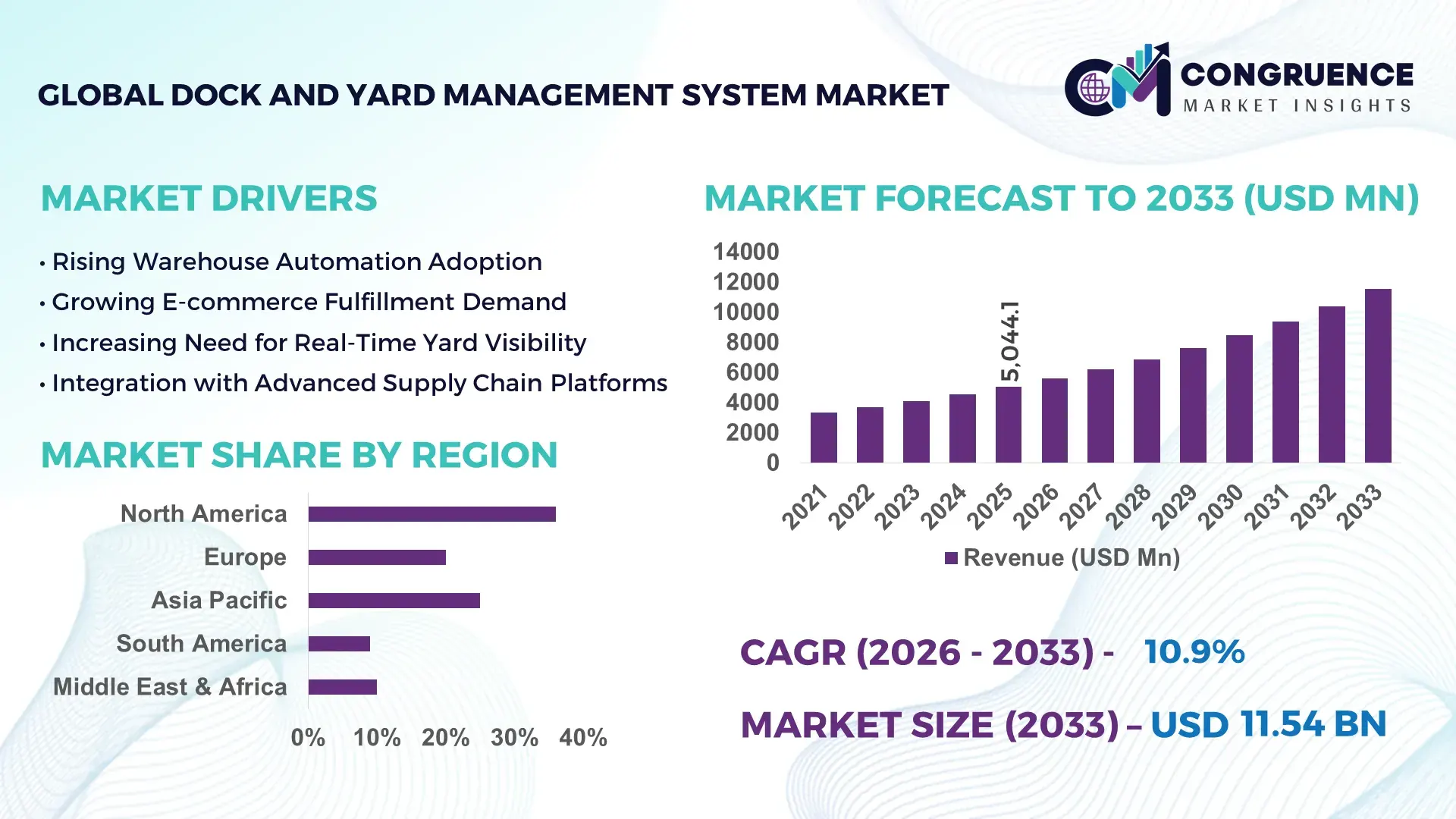

The Global Dock and Yard Management System Market was valued at USD 5044.11 Million in 2025 and is anticipated to reach a value of USD 11540.82 Million by 2033 expanding at a CAGR of 10.9% between 2026 and 2033. Growth is primarily driven by accelerating warehouse automation and rising demand for real-time logistics visibility amid supply chain disruptions.

The United States continues to dominate the Dock and Yard Management System market with extensive deployment across over 20,000 large-scale distribution centers and intermodal terminals. The country operates more than 5 million commercial trucks, generating significant yard traffic volumes that necessitate advanced dock scheduling software and yard optimization platforms. Annual logistics investments exceed USD 2 trillion, with substantial capital allocated to AI-driven warehouse management, IoT-enabled yard tracking, and RFID-based asset monitoring systems. Adoption is particularly strong in retail e-commerce, automotive manufacturing, and third-party logistics sectors, where digital dock management has reduced truck turnaround times by up to 25% and improved yard throughput by 18%. High penetration of cloud-based supply chain software and advanced telematics further reinforces technological maturity in this market.

Market Size & Growth: USD 5044.11 Million (2025) projected to reach USD 11540.82 Million by 2033 at 10.9% CAGR, driven by real-time yard visibility and digital freight optimization.

Top Growth Drivers: 42% rise in warehouse automation adoption; 35% improvement in dock utilization efficiency; 28% reduction in vehicle idle time through digital scheduling.

Short-Term Forecast: By 2028, predictive yard analytics is expected to reduce detention costs by 20% and enhance on-time dispatch performance by 18%.

Emerging Technologies: AI-powered yard orchestration, IoT-enabled asset tracking, cloud-based dock scheduling integrated with transportation management systems.

Regional Leaders: North America projected at USD 4200 Million by 2033 with strong 3PL adoption; Asia-Pacific nearing USD 3800 Million driven by port digitalization; Europe reaching USD 2500 Million with ESG-compliant smart warehouses.

Consumer/End-User Trends: E-commerce, FMCG, and automotive sectors account for over 60% of deployments, emphasizing cloud-native yard visibility platforms.

Pilot Example: In 2024, a leading global retailer implemented AI-based yard automation, reducing truck dwell time by 22% and improving gate processing speed by 30%.

Competitive Landscape: Manhattan Associates holds approximately 18% share, followed by SAP, Oracle, Blue Yonder, and Körber Supply Chain.

Regulatory & ESG Impact: Carbon reporting mandates push logistics operators to cut yard emissions by 15% through optimized routing and idle reduction systems.

Investment & Funding Patterns: Over USD 1.6 billion invested globally in logistics digitization projects during 2024, including venture-backed SaaS yard management startups.

Innovation & Future Outlook: Integration of digital twin yard modeling and autonomous yard trucks is shaping next-generation resilient logistics ecosystems.

The Dock and Yard Management System market serves key sectors including e-commerce (approx. 32% of deployments), automotive and industrial manufacturing (25%), retail distribution (18%), and third-party logistics providers (over 20%). Recent innovations include AI-driven dock door assignment, machine learning-based congestion forecasting, and blockchain-enabled shipment verification. Regulatory focus on carbon emission reduction and cross-border trade digitization is accelerating system integration across North America and Europe, while Asia-Pacific demonstrates rapid consumption growth due to port automation initiatives. Increasing demand for scalable SaaS yard platforms and integrated transportation management solutions is positioning the market for sustained digital transformation and operational resilience.

The Dock and Yard Management System Market plays a strategic role in strengthening end-to-end supply chain resilience, particularly under volatile global trade conditions and conflict-driven disruptions. Enterprises are prioritizing intelligent dock scheduling and real-time yard orchestration to reduce bottlenecks, optimize fleet movement, and mitigate detention penalties. AI-powered predictive yard analytics delivers 30% improvement in dock allocation efficiency compared to manual spreadsheet-based scheduling systems, significantly lowering congestion risks.

North America dominates in volume due to large-scale warehouse infrastructure, while Europe leads in digital adoption with nearly 55% of large logistics enterprises integrating cloud-based yard management solutions. By 2028, AI-enabled computer vision and automated gate processing systems are expected to improve yard throughput by 25% while cutting manual intervention by 40%. Firms are committing to ESG targets such as 20% reduction in yard-related carbon emissions by 2030 through idle-time monitoring and smart routing optimization.

In 2024, a major logistics operator in Germany achieved a 27% reduction in truck waiting time after deploying IoT-enabled yard sensors integrated with predictive analytics dashboards. Over the next three years, integration of digital twin yard simulations and autonomous yard tractors is projected to reduce operational downtime by 15%. As supply chains adapt to geopolitical uncertainties and compliance mandates, the Dock and Yard Management System Market is emerging as a foundational pillar of operational resilience, regulatory compliance, and sustainable logistics growth.

Global e-commerce parcel volumes exceed 200 billion annually, placing immense pressure on distribution centers and last-mile logistics networks. High shipment frequency increases dock congestion and vehicle idle time, directly impacting operational costs. Advanced dock and yard management systems streamline gate check-ins, automate dock door assignments, and provide real-time yard mapping, reducing truck turnaround time by up to 25%. Large fulfillment hubs processing over 500,000 orders daily rely on predictive yard analytics to prevent bottlenecks and enhance throughput efficiency. Integration with transportation management systems ensures synchronized inbound and outbound flows, supporting faster order fulfillment and improved customer service performance across competitive retail markets.

Deploying an enterprise-grade dock and yard management system involves integration with existing ERP, WMS, and TMS platforms, often requiring multi-million-dollar capital expenditure for large facilities. Hardware components such as IoT sensors, RFID readers, gate automation systems, and surveillance infrastructure add to upfront costs. Mid-sized warehouses operating under tight margins may delay modernization due to extended ROI timelines. Additionally, legacy IT environments create compatibility challenges, leading to longer deployment cycles that may exceed 9–12 months. Data security concerns and workforce training requirements further slow adoption, particularly in developing markets where digital infrastructure maturity remains uneven.

Smart port initiatives and autonomous logistics corridors are generating new growth avenues for dock and yard management system providers. Over 60% of major global ports are investing in digital transformation projects that include automated gate systems and AI-based yard optimization tools. Autonomous yard trucks and robotic container handling solutions enhance safety and reduce manual labor dependency. Integration of real-time weather analytics and predictive congestion modeling offers improved operational continuity. Emerging economies in Asia-Pacific and the Middle East are building greenfield logistics parks with built-in digital yard infrastructure, creating strong demand for scalable SaaS-based yard orchestration platforms tailored to high-volume freight environments.

As dock and yard management systems become increasingly cloud-connected and data-intensive, cybersecurity threats pose significant operational risks. Logistics facilities process thousands of vehicle and shipment records daily, making them attractive targets for ransomware and data breaches. A single cyber incident can disrupt yard operations for several hours, causing cascading supply chain delays. Furthermore, integration of AI modules, IoT sensors, and legacy warehouse software demands robust interoperability frameworks. Fragmented technology ecosystems across multinational logistics networks complicate standardization efforts. Ensuring secure APIs, encrypted communication channels, and continuous system monitoring remains critical to sustaining trust and long-term digital transformation initiatives within the Dock and Yard Management System market.

• AI-Driven Predictive Yard Orchestration Improving Turnaround by 25%:

Advanced artificial intelligence algorithms are being deployed to predict dock congestion, optimize gate scheduling, and allocate yard assets dynamically. Facilities using AI-enabled dock and yard management platforms report up to 25% reduction in truck turnaround time and 18% improvement in dock utilization rates. Over 60% of large distribution centers in North America have integrated predictive analytics dashboards to manage peak-hour traffic. Real-time machine learning models analyze more than 10,000 daily yard movement data points in high-volume facilities, enabling proactive congestion management and measurable reductions in detention penalties.

• IoT and RFID Integration Enhancing Real-Time Asset Visibility by 30%:

IoT-enabled sensors and RFID tracking technologies are transforming yard visibility and compliance monitoring. More than 70% of newly commissioned smart warehouses now deploy connected gate systems and GPS-enabled trailer tracking. These digital yard visibility solutions improve asset tracking accuracy by 30% and reduce misplaced trailer incidents by nearly 40%. Automated check-in kiosks integrated with RFID readers can process vehicles in under 90 seconds, compared to 4–5 minutes under manual systems, significantly accelerating throughput in high-density logistics parks.

• Cloud-Based Dock Scheduling Platforms Achieving 35% Operational Efficiency Gains:

Cloud-native dock scheduling software adoption has increased by over 50% across multi-site logistics operators seeking centralized control. Enterprises implementing scalable SaaS-based dock management systems report 35% improvement in resource allocation efficiency and up to 20% reduction in yard labor requirements. Multi-tenant cloud platforms allow real-time collaboration between carriers and warehouse managers, supporting over 1,000 concurrent booking requests daily in major retail fulfillment hubs. Integration with transportation management systems ensures synchronized inbound and outbound flow management across complex supply chain networks.

• Sustainability-Focused Yard Optimization Cutting Emissions by 15%:

Environmental compliance and ESG commitments are reshaping yard management strategies globally. Intelligent routing and idle-time monitoring solutions have reduced yard-related fuel consumption by 12%–15% in facilities deploying automated dispatch systems. Over 45% of European logistics operators now use emission-tracking dashboards integrated into dock and yard management platforms. Electrified yard tractors combined with digital scheduling systems have lowered carbon emissions per shipment by nearly 10%, supporting corporate sustainability targets and regulatory reporting requirements across developed markets.

The Dock and Yard Management System market is segmented by type, application, and end-user, reflecting diverse operational requirements across global logistics networks. Deployment models range from cloud-based platforms to on-premise enterprise systems, with cloud adoption surpassing 55% due to scalability and lower infrastructure complexity. Applications primarily include dock scheduling, yard visibility and tracking, gate management, and fleet coordination. Dock scheduling accounts for approximately 34% of total system utilization owing to its direct impact on turnaround efficiency and cost optimization.

From an end-user perspective, third-party logistics providers and large-scale retailers represent more than 50% of overall deployments, driven by high shipment volumes and stringent service-level agreements. Manufacturing and automotive sectors follow closely, integrating yard management solutions to streamline inbound raw material flows and outbound finished goods dispatch. Growing demand for digital freight transparency, compliance reporting, and operational analytics is reinforcing segmentation-driven investment strategies among global enterprises.

The Dock and Yard Management System market is categorized into cloud-based systems, on-premise systems, and hybrid deployment models. Cloud-based dock and yard management systems currently account for approximately 58% of total adoption, reflecting enterprise preference for scalable, subscription-driven platforms with centralized analytics dashboards. On-premise systems hold nearly 28% share, primarily among large manufacturers and defense logistics operators requiring enhanced data control and internal IT governance. Hybrid models represent the remaining 14%, offering flexible integration for organizations transitioning from legacy systems. Cloud-based systems are the fastest-growing type, expanding at an estimated CAGR of 13.4% due to rapid digital transformation initiatives and increasing cross-border logistics coordination. These platforms enable real-time yard mapping, predictive congestion alerts, and seamless API integration with transportation and warehouse management systems. In contrast, on-premise deployments remain relevant in high-security operations but face slower expansion due to infrastructure constraints.

Dock scheduling represents the leading application segment, accounting for approximately 34% of total system utilization due to its direct influence on detention cost reduction and throughput optimization. Yard visibility and tracking systems follow with 29% share, while gate management applications contribute around 21%. Fleet and carrier coordination modules collectively account for the remaining 16%, supporting integrated supply chain orchestration. Dock scheduling remains dominant as enterprises prioritize reduction of average waiting time, which can exceed 2 hours in congested facilities. However, yard visibility and tracking applications are growing fastest, expanding at an estimated CAGR of 12.8%, driven by IoT-enabled trailer monitoring and geofencing technologies. Adoption of automated gate systems is also accelerating in high-traffic ports and intermodal hubs.

Third-party logistics (3PL) providers lead the Dock and Yard Management System market, accounting for nearly 38% of deployments due to high shipment volumes and multi-client operational complexity. Retail and e-commerce operators represent 27%, while manufacturing and automotive sectors contribute approximately 22%. Ports and intermodal terminals collectively account for the remaining 13%, reflecting specialized infrastructure needs.While 3PL firms dominate current usage, retail and e-commerce operators are the fastest-growing end-user segment, expanding at an estimated CAGR of 14.1% as same-day delivery models and high-frequency shipments demand precise dock coordination. Adoption rates among large retail chains exceed 60%, particularly in North America and Asia-Pacific, where fulfillment centers process over 300,000 daily orders. Manufacturing facilities continue integrating yard management platforms to streamline just-in-time production schedules and reduce raw material dwell time by up to 20%.

North America accounted for the largest market share at 36% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 12.7% between 2026 and 2033.

North America processed over 25 billion tons of freight annually, with more than 20,000 large-scale warehouses utilizing advanced dock and yard management systems to optimize vehicle flow and gate scheduling. Europe followed with approximately 27% market share, supported by over 1,200 smart logistics hubs and strong ESG compliance mandates. Asia-Pacific accounted for nearly 24% share in 2025, driven by rapid expansion of more than 15,000 new distribution centers across China, India, and Southeast Asia. South America represented 7%, while the Middle East & Africa contributed 6%, reflecting ongoing infrastructure modernization and port automation initiatives. Globally, more than 60% of Tier-1 logistics operators have integrated cloud-based yard visibility platforms, with regional adoption rates exceeding 65% in developed markets and reaching 40% in emerging trade corridors.

How Are Advanced Digital Freight Networks Transforming Operational Efficiency Across Major Logistics Hubs?

North America holds approximately 36% of the global Dock and Yard Management System market share, supported by over 20,000 high-volume distribution facilities and more than 5 million registered commercial trucks. Key demand drivers include e-commerce, retail, automotive manufacturing, and third-party logistics, which collectively account for over 70% of system deployments. Regulatory frameworks such as the Infrastructure Investment and Jobs Act allocate over USD 1 trillion toward transport modernization, accelerating smart port and automated gate adoption. More than 65% of large enterprises in this region utilize AI-powered dock scheduling tools, improving yard throughput by up to 25%. Local technology leaders such as Manhattan Associates continue enhancing cloud-native yard orchestration platforms capable of managing over 10,000 daily shipment movements. Regional enterprise behavior shows strong preference for integrated SaaS solutions, with adoption rates exceeding 60% among large retailers and financial-grade compliance environments emphasizing cybersecurity and ESG reporting.

Why Is Digital Compliance and Sustainability Reshaping Intelligent Yard Operations Across Industrial Economies?

Europe accounts for nearly 27% of the Dock and Yard Management System market share, with Germany, the UK, and France representing over 60% of regional deployments. More than 1,200 logistics terminals across the region operate automated gate and yard tracking systems. Strict environmental regulations, including carbon reduction mandates targeting 55% emission cuts by 2030, are accelerating digital yard optimization initiatives. Approximately 58% of European logistics enterprises have adopted IoT-enabled asset tracking integrated with compliance dashboards. SAP, headquartered in Germany, continues advancing digital supply chain modules that support real-time dock coordination and ESG reporting for over 5,000 regional clients. Regulatory pressure drives demand for explainable and auditable dock management systems, with 48% of operators prioritizing sustainability-linked digital transformation to meet cross-border trade documentation and emission monitoring requirements.

What Is Fueling the Rapid Digital Transformation of High-Volume Trade Corridors and Mega Distribution Parks?

Asia-Pacific ranks third in current market share at 24% but leads in growth momentum, supported by over 40% of global container port activity concentrated in China, Japan, and South Korea. China alone operates more than 30 major automated ports, while India has added over 2,000 new logistics parks since 2020. E-commerce shipments in the region exceed 100 billion parcels annually, significantly increasing dock scheduling complexity. Over 50% of new warehouse construction projects incorporate IoT-based yard monitoring from inception. Regional technology innovators are deploying AI-powered gate recognition systems capable of processing vehicles within 60 seconds. Consumer behavior trends emphasize mobile-enabled yard applications, with adoption among mid-sized enterprises rising above 45%, driven by expanding cross-border trade and manufacturing output.

How Are Trade Modernization Policies Enhancing Port and Industrial Logistics Efficiency?

South America contributes approximately 7% to the global Dock and Yard Management System market, with Brazil and Argentina accounting for nearly 65% of regional demand. Brazil operates more than 30 major seaports handling over 1 billion tons of cargo annually, creating substantial need for digital dock coordination systems. Infrastructure modernization programs have allocated billions toward port automation and freight corridor upgrades. Approximately 38% of logistics operators in Brazil have adopted digital yard tracking solutions to reduce congestion and optimize truck turnaround time by up to 18%. Regional trade agreements and export-driven agriculture and mining industries stimulate investment in smart logistics infrastructure. Enterprises in this region prioritize localized software platforms with multilingual interfaces, reflecting diverse operational environments and regulatory requirements.

How Is Smart Infrastructure Investment Supporting High-Efficiency Logistics Ecosystems?

The Middle East & Africa region represents nearly 6% of the global Dock and Yard Management System market, driven by strategic investments in oil & gas logistics, construction supply chains, and free trade zones. The UAE and Saudi Arabia collectively account for over 55% of regional deployments, supported by more than 40 advanced logistics hubs and smart ports. South Africa processes over 300 million tons of cargo annually, encouraging modernization of dock scheduling platforms. Government-backed smart city programs and public-private partnerships are integrating automated yard control systems into mega infrastructure projects. Approximately 35% of regional logistics facilities now deploy IoT-based asset tracking. Consumer behavior reflects strong preference for scalable cloud deployments, particularly among multinational operators managing cross-border freight corridors.

United States – 34% market share: The Dock and Yard Management System market in the United States leads due to extensive warehouse infrastructure exceeding 20,000 large facilities and high adoption of AI-driven logistics optimization platforms.

Germany – 11% market share: The Dock and Yard Management System market in Germany is driven by advanced manufacturing output, over 1,500 automated logistics centers, and stringent sustainability compliance requirements.

The Dock and Yard Management System market is moderately consolidated, with the top five companies accounting for approximately 54% of global market presence. More than 40 active competitors operate across cloud-based yard management, gate automation, and integrated supply chain software segments. Leading vendors focus on AI-enabled yard orchestration, predictive analytics, and IoT integration to differentiate offerings. In 2024 alone, over 25 strategic partnerships were announced between dock management providers and transportation management software firms to expand end-to-end logistics capabilities. Product innovation cycles have shortened to 12–18 months, with frequent software upgrades introducing digital twin modeling, autonomous yard vehicle compatibility, and ESG reporting dashboards. Mergers and acquisitions activity has increased by 18% over the past two years, primarily targeting SaaS startups specializing in yard visibility analytics. Competitive positioning increasingly emphasizes cybersecurity resilience, scalable cloud architecture, and interoperability with enterprise ERP systems, reflecting heightened enterprise demand for fully integrated digital freight ecosystems.

Manhattan Associates

SAP

Oracle

Blue Yonder

Körber Supply Chain

Descartes Systems Group

C3 Solutions

Yard Management Solutions (YMS)

Infor

3PL Central

The Dock and Yard Management System market is undergoing rapid technological transformation driven by artificial intelligence, IoT connectivity, computer vision, and cloud-native architectures. AI-powered predictive analytics engines now process more than 10,000 daily yard movement data points in large distribution hubs, enabling up to 30% improvement in dock allocation accuracy and 20% reduction in congestion incidents. Machine learning algorithms analyze historical carrier arrival patterns, weather conditions, and shipment volumes to dynamically optimize dock door assignments and yard slot positioning in real time.

IoT-enabled asset tracking has become a foundational technology layer, with over 70% of newly built smart warehouses integrating RFID tags, GPS-based trailer tracking, and geofencing sensors. These technologies improve trailer visibility accuracy by nearly 30% and reduce misplaced equipment events by 35%–40%. Automated gate systems equipped with license plate recognition (LPR) and optical character recognition (OCR) can process inbound trucks within 60–90 seconds, compared to manual processes that often exceed 4 minutes per vehicle.

Cloud-based deployment models now account for more than 55% of new implementations, enabling centralized multi-site control across networks exceeding 100 facilities. Integration with transportation management systems (TMS), warehouse management systems (WMS), and enterprise resource planning (ERP) platforms ensures synchronized freight flow. Emerging innovations include digital twin yard simulations capable of modeling over 5,000 simultaneous trailer positions, and autonomous yard tractors operating within geofenced environments, reducing manual yard labor requirements by up to 25%. Cybersecurity frameworks incorporating end-to-end encryption and multi-factor authentication are increasingly embedded to protect high-volume logistics data exchanges exceeding 1 million monthly transaction records per enterprise network.

• In March 2024, Manhattan Associates announced enhancements to its Yard Management solution within the Manhattan Active® platform, introducing machine learning-driven dock door optimization and real-time yard visibility dashboards. The update improved dock assignment efficiency and reduced manual scheduling interventions across multi-site retail distribution networks. Source: www.manh.com

• In January 2025, SAP expanded its Digital Supply Chain portfolio by integrating advanced yard logistics capabilities into SAP Extended Warehouse Management, enabling automated gate check-in, yard task interleaving, and IoT-based asset tracking for large-scale manufacturing and logistics customers. Source: www.sap.com

• In September 2024, Blue Yonder introduced new AI-powered yard orchestration features as part of its Luminate Platform, incorporating predictive congestion analytics and enhanced carrier collaboration tools that streamlined dock scheduling and reduced truck dwell time in pilot deployments.

• In April 2025, Körber Supply Chain upgraded its yard management module within the K.Motion suite, adding real-time geolocation tracking and advanced KPI dashboards capable of monitoring over 500 concurrent yard movements, supporting large 3PL operations with improved operational transparency.

The Dock and Yard Management System Market Report provides comprehensive coverage across deployment types, applications, end-user industries, and geographic regions, offering detailed analysis of over 40 active technology providers and more than 20 national logistics markets. The scope includes cloud-based, on-premise, and hybrid deployment models, with cloud platforms representing over 55% of current installations. Application coverage spans dock scheduling (34% usage share), yard visibility and tracking (29%), gate management (21%), and fleet coordination modules (16%).

Geographically, the report evaluates five primary regions—North America (36% share), Europe (27%), Asia-Pacific (24%), South America (7%), and Middle East & Africa (6%)—including country-level insights for the United States, Germany, China, India, Brazil, and the UAE. Industry focus areas include third-party logistics providers (38% adoption), retail and e-commerce operators (27%), manufacturing and automotive enterprises (22%), and port and intermodal terminals (13%).

Technological assessment covers AI-driven predictive analytics, IoT-enabled trailer tracking, RFID integration, automated gate systems, digital twin yard simulations, and autonomous yard vehicle compatibility. The report also evaluates ESG-driven yard optimization initiatives targeting 10%–20% emission reduction through idle-time monitoring. Additional scope elements include cybersecurity frameworks, interoperability standards with TMS and WMS platforms, and performance benchmarking metrics such as average truck turnaround time reduction of 20%–25% and dock utilization improvements exceeding 30% in digitally optimized facilities.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

10.9% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Manhattan Associates, SAP, Oracle, Blue Yonder, Körber Supply Chain, Descartes Systems Group, C3 Solutions, Yard Management Solutions (YMS), Infor, 3PL Central |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |