Reports

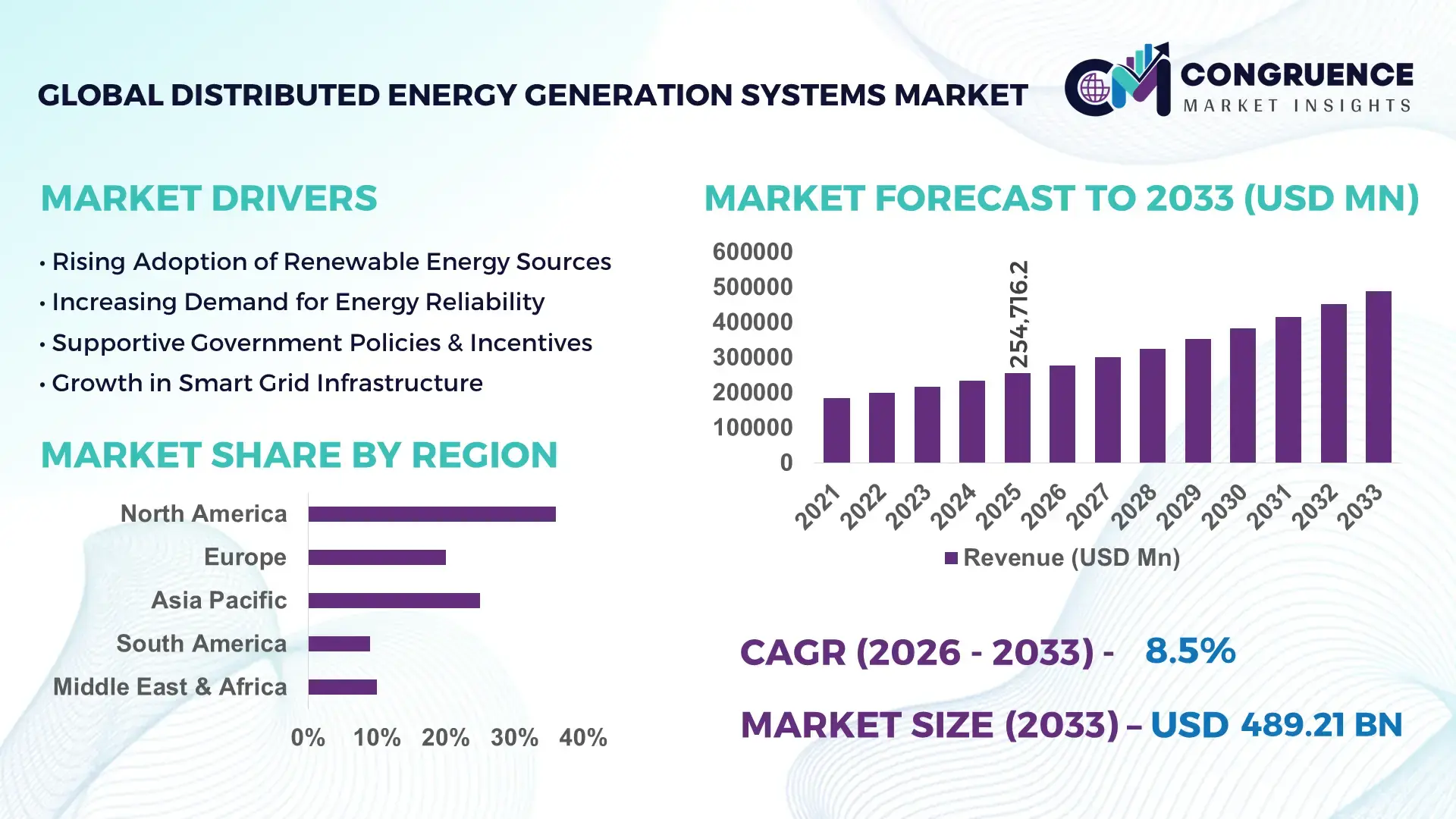

The Global Distributed Energy Generation Systems Market was valued at USD 254716.17 Million in 2025 and is anticipated to reach a value of USD 489208.98 Million by 2033 expanding at a CAGR of 8.5% between 2026 and 2033. This growth is primarily driven by increasing demand for decentralized energy solutions and grid resilience.

The United States continues to demonstrate substantial activity in the distributed energy generation systems market, supported by strong deployment of solar photovoltaic (PV), combined heat and power (CHP), and battery storage technologies. The country installed over 32 GW of distributed solar capacity in 2024 alone, with residential and commercial segments accounting for nearly 60% of total installations. Investment in distributed energy infrastructure exceeded USD 45 billion annually, driven by tax incentives and state-level renewable mandates. Industrial sectors, particularly manufacturing and data centers, have increasingly adopted onsite generation systems, contributing to over 25% of distributed capacity additions. Additionally, advanced grid technologies such as smart inverters and virtual power plants have expanded by more than 18% year-over-year, improving energy efficiency and system reliability.

Market Size & Growth: Valued at USD 254716.17 Million in 2025, projected to reach USD 489208.98 Million by 2033 at 8.5% CAGR, driven by rising decentralized energy demand and grid modernization initiatives.

Top Growth Drivers: Renewable adoption increased by 28%, energy efficiency improvements by 22%, and smart grid deployment by 19%.

Short-Term Forecast: By 2028, distributed systems are expected to reduce energy costs by 15% through improved storage and optimization technologies.

Emerging Technologies: AI-based energy management systems, advanced battery storage, and microgrid automation are transforming system performance.

Regional Leaders: North America projected at USD 165 billion by 2033 with high smart grid adoption; Europe at USD 140 billion driven by sustainability mandates; Asia-Pacific at USD 120 billion fueled by urban energy demand.

Consumer/End-User Trends: Industrial and commercial sectors contribute over 55% of installations, with increasing residential adoption of rooftop solar and hybrid systems.

Pilot or Case Example: In 2024, a smart microgrid project improved energy efficiency by 20% and reduced downtime by 30% in a large industrial facility.

Competitive Landscape: Market leader holds approximately 17% share, followed by several global energy solution providers and technology firms.

Regulatory & ESG Impact: Governments targeting 40% emissions reduction by 2030 are accelerating adoption through incentives and renewable mandates.

Investment & Funding Patterns: Over USD 60 billion invested globally in distributed energy projects, with growth in green financing and infrastructure funds.

Innovation & Future Outlook: Integration of digital twins, IoT-enabled monitoring, and decentralized energy trading platforms is shaping long-term growth.

Distributed energy generation systems are witnessing strong adoption across key industry sectors such as manufacturing, commercial real estate, and utilities, contributing nearly 65% of total installations. Technological advancements including high-efficiency solar panels exceeding 22% conversion efficiency and lithium-ion battery systems with improved lifecycle performance are significantly enhancing system viability. Regulatory frameworks promoting carbon neutrality and renewable portfolio standards are accelerating market expansion. Regional consumption trends highlight strong growth in Asia-Pacific due to urbanization and industrialization, while Europe emphasizes sustainability-driven adoption. Emerging trends such as peer-to-peer energy trading, integration with electric vehicle infrastructure, and hybrid renewable systems are expected to redefine the competitive landscape and operational efficiency.

The distributed energy generation systems market holds critical strategic relevance in enabling energy independence, improving grid resilience, and supporting decarbonization targets across global economies. Businesses are increasingly integrating decentralized energy assets to reduce operational risks associated with centralized grid failures and volatile energy pricing. Advanced energy storage systems deliver 25% higher efficiency compared to traditional backup generators, enhancing reliability and cost-effectiveness.

From a regional perspective, North America dominates in volume due to established infrastructure and high investment levels, while Asia-Pacific leads in adoption with over 35% of enterprises implementing distributed energy solutions for industrial and commercial use. The rapid deployment of digital energy platforms is transforming system optimization and predictive maintenance capabilities. By 2028, AI-driven energy management systems are expected to improve operational efficiency by up to 20% through real-time monitoring and automated load balancing. Organizations are also aligning with ESG goals, committing to emissions reductions of up to 40% by 2030 through renewable integration and energy efficiency improvements.

A notable micro-scenario occurred in 2024, where a large-scale industrial facility in Germany achieved a 22% reduction in energy consumption through the deployment of an AI-powered microgrid system combined with onsite solar and storage solutions. Such implementations demonstrate measurable benefits in cost savings and sustainability performance. Looking ahead, the distributed energy generation systems market is poised to become a foundational pillar for resilient energy infrastructure, regulatory compliance, and long-term sustainable growth across industries.

The increasing need for energy reliability and resilience is a primary driver of the distributed energy generation systems market. Power outages and grid instability have led to significant economic losses, prompting industries to adopt localized energy solutions. Distributed systems such as microgrids and combined heat and power units can reduce downtime by up to 30% and improve energy efficiency by 15–20%. The growing deployment of renewable energy technologies, particularly solar PV, which accounted for over 60% of new distributed capacity additions in 2024, further supports market expansion. Additionally, industrial facilities and commercial establishments are increasingly investing in onsite energy generation to manage peak demand and reduce dependency on centralized grids, enhancing overall operational efficiency.

Despite strong growth prospects, high upfront capital costs remain a significant restraint for the distributed energy generation systems market. Installation of solar panels, energy storage systems, and advanced control technologies requires substantial investment, often exceeding USD 1,500 per kilowatt for integrated systems. Small and medium-sized enterprises face financial constraints in adopting these solutions, limiting market penetration. Furthermore, the complexity of integrating distributed systems with existing grid infrastructure increases installation and maintenance costs. Regulatory uncertainties and inconsistent policy frameworks across regions also hinder large-scale adoption. These factors collectively slow down the pace of deployment, particularly in developing economies where access to financing and technical expertise is limited.

The convergence of digital technologies and distributed energy systems presents significant growth opportunities. The adoption of smart grid technologies, IoT-enabled devices, and AI-driven analytics is transforming energy management and optimization. Digital platforms can enhance system efficiency by up to 25% through predictive maintenance and real-time monitoring. The increasing popularity of virtual power plants, which aggregate distributed energy resources, is enabling more efficient energy distribution and grid balancing. Additionally, the integration of electric vehicle charging infrastructure with distributed systems is creating new revenue streams and expanding application areas. Emerging markets in Asia and Africa offer untapped potential, with rising electrification rates and government initiatives supporting decentralized energy solutions.

One of the key challenges in the distributed energy generation systems market is the complexity of integrating decentralized systems into existing grid infrastructure. Variability in renewable energy generation creates challenges in maintaining grid stability and requires advanced control systems and storage solutions. In many regions, outdated grid infrastructure lacks the capacity to handle bidirectional energy flows, leading to inefficiencies and potential disruptions. Regulatory barriers, including inconsistent policies and lengthy approval processes, further complicate deployment. Compliance with grid codes and standards increases operational complexity and costs. Additionally, cybersecurity risks associated with digital energy systems pose significant concerns, requiring continuous investment in secure and resilient infrastructure.

• Rapid Expansion of AI-Driven Energy Management Systems: The integration of artificial intelligence into distributed energy generation systems is accelerating operational efficiency and predictive maintenance capabilities. Over 48% of newly deployed distributed energy systems in 2025 incorporate AI-based monitoring tools, enabling real-time load balancing and demand forecasting. Facilities using AI-enabled optimization have reported up to 22% improvement in energy utilization efficiency and a 17% reduction in operational downtime. This trend is particularly strong in industrial and commercial sectors, where energy-intensive operations require precise control and cost optimization.

• Growth in Hybrid Renewable Energy Systems Adoption: Hybrid systems combining solar, wind, and battery storage are gaining traction due to their ability to deliver consistent power output. Approximately 37% of new distributed installations globally now utilize hybrid configurations, compared to 24% in 2022. These systems have demonstrated a 28% increase in energy reliability and a 19% reduction in dependency on centralized grids. Regions with variable weather conditions are leading this trend, leveraging hybrid systems to maintain stable energy supply across fluctuating generation cycles.

• Surge in Microgrid Deployment Across Industrial Clusters: Microgrid adoption is expanding significantly, particularly in manufacturing zones and remote industrial clusters. More than 31% of large-scale industrial facilities implemented microgrid systems in 2024, resulting in a 25% decrease in grid outage impact and a 20% improvement in energy security. Governments and private entities are increasingly investing in localized grid infrastructure, with over 12,000 operational microgrid projects globally, reflecting a 16% year-on-year increase in installations.

• Increasing Integration with Electric Vehicle Infrastructure: Distributed energy systems are increasingly being integrated with electric vehicle charging networks, creating decentralized energy ecosystems. Around 29% of new EV charging stations are now powered by onsite renewable energy systems, improving charging efficiency by 18% and reducing grid load by 14%. This integration is particularly prominent in urban areas, where rising EV adoption rates exceeding 35% annually are driving demand for sustainable and scalable energy solutions.

The distributed energy generation systems market is segmented across types, applications, and end-user industries, each contributing distinctively to overall market expansion. By type, solar photovoltaic systems dominate installations due to high efficiency and declining equipment costs, while combined heat and power and energy storage systems continue to gain traction in industrial applications. Application-wise, commercial and industrial sectors lead adoption, accounting for over 55% of total deployments, driven by the need for cost optimization and energy reliability. Residential adoption is also increasing, supported by rooftop solar and battery storage solutions. From an end-user perspective, utilities, manufacturing, and commercial real estate sectors collectively contribute over 60% of system demand. Regional segmentation indicates strong uptake in North America and Asia-Pacific, supported by infrastructure development and policy incentives, while Europe emphasizes sustainability-focused distributed energy integration.

The distributed energy generation systems market includes key product types such as solar photovoltaic (PV) systems, wind-based distributed generation, combined heat and power (CHP) systems, fuel cells, and energy storage systems. Solar PV systems currently account for approximately 46% of total installations, driven by declining module costs, improved efficiency exceeding 22%, and widespread residential and commercial adoption. In comparison, energy storage systems hold around 21% of adoption, while CHP systems contribute nearly 18% due to their efficiency in industrial applications.

Energy storage systems represent the fastest-growing segment, expanding at an estimated rate of over 11% annually, fueled by increasing demand for grid stability and renewable integration. Battery technologies, particularly lithium-ion, are enabling longer lifecycle performance and faster response times, supporting their rapid adoption. Wind-based distributed systems and fuel cells together contribute approximately 15% of the market, serving niche applications in remote and off-grid environments.

The market applications for distributed energy generation systems span residential, commercial, and industrial sectors, each with distinct adoption patterns. The commercial and industrial segment leads with approximately 57% of total adoption, as businesses prioritize energy cost savings and operational reliability. Residential applications account for around 28%, driven by rooftop solar installations and home energy storage systems, while utility-scale distributed applications represent nearly 15%.

Among these, industrial applications are the fastest-growing, expanding at an estimated rate of over 10% annually, supported by rising energy demand and the need for uninterrupted power supply in manufacturing and processing industries. Distributed systems in industrial settings can improve energy efficiency by up to 20% and reduce peak load demand by 18%. Other applications, including institutional and remote infrastructure projects, collectively contribute around 15% of the market, serving specialized energy needs in healthcare, education, and rural electrification.

End-user segmentation in the distributed energy generation systems market includes utilities, manufacturing industries, commercial enterprises, residential consumers, and government institutions. Utilities and large industrial users dominate the market, accounting for approximately 44% of total installations, driven by the need for grid stabilization and energy diversification. Commercial enterprises represent around 26%, while residential users contribute nearly 20%, reflecting increasing adoption of decentralized energy solutions.

The residential segment is the fastest-growing, with an estimated growth rate exceeding 12% annually, fueled by rising electricity costs and increased awareness of renewable energy benefits. Homeowners are increasingly investing in rooftop solar systems and battery storage, achieving energy cost reductions of up to 25%. Other end-users, including government and institutional sectors, contribute approximately 10% of the market, focusing on sustainability initiatives and energy independence goals. Adoption rates in public infrastructure projects have increased by over 18% in recent years.

Region North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.8% between 2026 and 2033.

North America recorded over 85 GW of installed distributed energy capacity, supported by more than 2.5 million residential solar installations and over 15,000 microgrid deployments. Europe held approximately 29% share, with Germany, the UK, and France collectively contributing over 60% of regional installations, driven by stringent carbon reduction targets and renewable integration mandates. Asia-Pacific accounted for nearly 24% of the market, with China alone installing over 40 GW of distributed solar capacity in 2024, while India added more than 10 GW in rooftop and decentralized systems. South America contributed around 5%, with Brazil leading regional adoption through over 2 million distributed generation units. The Middle East & Africa region represented close to 4%, with growing investments in off-grid solar systems and hybrid energy solutions, particularly in rural electrification projects exceeding 8,000 installations annually.

What factors are accelerating decentralized energy adoption across advanced industrial economies?

North America holds approximately 38% of the global distributed energy generation systems market, driven by strong adoption across industrial, commercial, and residential sectors. Key industries such as manufacturing, healthcare, and data centers contribute over 52% of total demand due to high energy consumption and reliability requirements. Regulatory frameworks, including clean energy tax credits and state-level renewable portfolio standards, have supported the installation of over 30 GW of distributed solar capacity annually. Technological advancements such as AI-driven grid management and smart inverters have improved system efficiency by up to 20%. A notable example includes a leading energy solutions provider deploying over 1,200 microgrid systems across commercial facilities, reducing energy costs by nearly 18%. Consumer behavior indicates higher enterprise adoption, with over 65% of large organizations integrating distributed energy systems for operational resilience and sustainability compliance.

How are sustainability mandates shaping decentralized energy transformation across regulated economies?

Europe accounts for approximately 29% of the distributed energy generation systems market, with Germany, the United Kingdom, and France representing over 60% of regional installations. Strong regulatory frameworks, including carbon neutrality targets and renewable energy directives, are driving adoption across residential and commercial sectors. More than 45% of new building projects in the region integrate distributed energy systems, particularly rooftop solar and energy storage solutions. Emerging technologies such as hydrogen-based fuel cells and advanced battery systems are gaining traction, improving system efficiency by 18%. A regional energy technology firm has deployed decentralized energy solutions across more than 500 industrial sites, enhancing energy efficiency by 21%. Consumer behavior reflects regulatory pressure, with over 70% of enterprises prioritizing sustainable energy solutions to meet compliance and ESG requirements.

What is driving rapid expansion of localized energy systems across high-growth economies?

Asia-Pacific ranks as the fastest-growing region in the distributed energy generation systems market, accounting for nearly 24% of global installations. China, India, and Japan are the top consuming countries, collectively contributing over 68% of regional demand. Rapid urbanization and industrialization have led to the installation of more than 60 GW of distributed energy capacity annually. Infrastructure development and manufacturing expansion are key drivers, with industrial sectors accounting for over 50% of installations. Technological innovation hubs in China and Japan are advancing smart grid integration and energy storage technologies, improving system efficiency by up to 23%. A major regional energy provider has implemented distributed solar and storage systems across 1,000+ industrial facilities, reducing grid dependency by 19%. Consumer behavior highlights strong growth driven by rising electricity demand and increasing adoption of mobile-enabled energy monitoring solutions.

How are emerging energy policies influencing decentralized power adoption in developing economies?

South America represents approximately 5% of the global distributed energy generation systems market, with Brazil and Argentina as key contributors. Brazil alone accounts for over 70% of regional installations, with more than 2 million distributed generation systems deployed, primarily in residential and small commercial sectors. Infrastructure expansion and rising electricity costs are driving adoption, with solar PV systems accounting for over 80% of installations. Government incentives, including net metering policies and tax benefits, have accelerated market growth. A regional renewable energy company has deployed over 500 MW of distributed solar capacity, improving energy access and reducing reliance on centralized grids. Consumer behavior shows increasing demand for cost-effective energy solutions, with over 60% of new adopters focusing on residential solar installations to reduce electricity expenses.

What role does energy diversification play in advancing decentralized power solutions across resource-driven economies?

The Middle East & Africa region accounts for approximately 4% of the distributed energy generation systems market, with key growth observed in the UAE, Saudi Arabia, and South Africa. Demand is driven by sectors such as oil & gas, construction, and mining, which require reliable and efficient energy solutions. Over 8,000 off-grid and hybrid distributed systems are deployed annually, particularly in remote and rural areas. Technological modernization, including solar-diesel hybrid systems and advanced battery storage, has improved energy reliability by 20%. Trade partnerships and government initiatives promoting renewable energy adoption have further supported market expansion. A regional energy developer has implemented distributed solar projects across multiple industrial zones, achieving a 17% reduction in energy costs. Consumer behavior reflects a growing shift toward sustainable and independent energy solutions, particularly in off-grid communities.

United States – 34% market share in the Distributed Energy Generation Systems market, driven by extensive deployment of solar PV, microgrids, and strong regulatory incentives.

China – 28% market share in the Distributed Energy Generation Systems market, supported by large-scale manufacturing capacity and rapid expansion of distributed renewable installations.

The distributed energy generation systems market is moderately fragmented, with over 120 active global and regional players competing across technology segments such as solar PV, energy storage, and microgrid solutions. The top five companies collectively account for approximately 42% of the market, indicating a competitive yet evolving landscape. Market leaders are focusing on strategic partnerships, product innovation, and geographic expansion to strengthen their positions. Over 35% of companies have introduced new digital energy management platforms integrating AI and IoT capabilities to enhance system efficiency and customer engagement.

Mergers and acquisitions have increased by 18% over the past two years, with companies targeting energy storage and smart grid technology firms to expand their portfolios. Product innovation remains a key differentiator, with advancements in battery storage systems improving lifecycle performance by over 25% and reducing maintenance costs by 15%. Additionally, collaborations between technology providers and utility companies have resulted in the deployment of over 5,000 virtual power plant projects globally.

The competitive environment is also shaped by increasing investments in research and development, with leading firms allocating up to 10% of their annual budgets toward innovation in renewable integration and grid optimization technologies. This dynamic landscape is expected to intensify further as new entrants leverage digital solutions and sustainable energy models to capture market share.

Siemens AG

General Electric Company

Schneider Electric SE

ABB Ltd.

Honeywell International Inc.

Mitsubishi Electric Corporation

Eaton Corporation plc

Caterpillar Inc.

Cummins Inc.

Tesla Inc.

Enphase Energy Inc.

SunPower Corporation

Technological advancements are significantly reshaping the distributed energy generation systems market, with a strong focus on efficiency, digitalization, and system integration. One of the most impactful developments is the widespread deployment of advanced battery energy storage systems (BESS), particularly lithium-ion technologies, which now account for over 70% of installed storage capacity. These systems offer energy density improvements of up to 35% compared to earlier battery chemistries, enabling longer discharge durations and improved grid stability. In parallel, solid-state battery prototypes are demonstrating up to 50% higher energy density, indicating future potential for compact and high-performance storage solutions.

Smart grid technologies and IoT-enabled monitoring systems are also driving operational efficiency. Over 45% of newly installed distributed energy systems incorporate real-time data analytics platforms, enabling predictive maintenance and reducing equipment failure rates by nearly 25%. Digital twin technology is emerging as a critical innovation, allowing operators to simulate and optimize energy system performance, improving operational efficiency by up to 18%. Additionally, AI-based energy management systems are increasingly deployed, enabling automated load balancing and demand response optimization, resulting in up to 20% reduction in peak energy consumption.

Renewable integration technologies, particularly high-efficiency solar photovoltaic modules exceeding 22% conversion efficiency, are accelerating adoption across residential and commercial segments. Hybrid energy systems combining solar, wind, and storage now represent over 35% of new installations, enhancing reliability and reducing intermittency issues. Microgrid controllers equipped with advanced automation features have improved energy reliability by 30% in industrial applications.

Furthermore, blockchain-enabled energy trading platforms are gaining traction, enabling peer-to-peer electricity exchange and improving energy transaction transparency. Hydrogen-based distributed generation technologies, including fuel cells, are also expanding, with efficiency levels reaching up to 60% in combined heat and power configurations. These innovations collectively position distributed energy systems as a technologically advanced, flexible, and scalable solution for modern energy demands.

• In February 2025, Siemens AG launched an advanced microgrid management platform integrating AI-based forecasting and real-time grid analytics, enabling up to 20% improvement in energy efficiency and reducing system downtime across industrial facilities. Source: www.siemens.com

• In September 2024, Schneider Electric SE introduced a next-generation distributed energy resource (DER) management solution designed to optimize hybrid energy systems, improving energy utilization by 18% and supporting seamless integration of solar, storage, and EV infrastructure. Source: www.se.com

• In March 2025, Tesla Inc. expanded its Megapack energy storage deployment with enhanced grid-scale capabilities, delivering over 3.9 MWh per unit and improving large-scale distributed energy storage efficiency by approximately 25% compared to previous models. Source: www.tesla.com

• In November 2024, ABB Ltd. deployed a digital energy management system for industrial microgrids, incorporating IoT-enabled sensors and predictive analytics, achieving a 17% reduction in operational energy losses and improving overall system reliability. Source: www.abb.com

The distributed energy generation systems market report provides a comprehensive analysis of decentralized energy technologies, covering a wide range of system types including solar photovoltaic systems, wind-based distributed generation, combined heat and power systems, fuel cells, and advanced energy storage solutions. The report evaluates more than 10 major technology categories and over 25 sub-segments, offering detailed insights into system configurations, efficiency benchmarks, and deployment patterns across diverse environments.

Geographically, the report encompasses five major regions and analyzes over 20 key countries, accounting for more than 90% of global distributed energy installations. It highlights regional variations in adoption, with North America and Europe focusing on grid modernization and sustainability, while Asia-Pacific emphasizes large-scale infrastructure development and industrial applications. The report also includes insights into emerging markets in South America and the Middle East & Africa, where off-grid and hybrid energy systems are gaining traction.

From an application perspective, the report covers residential, commercial, industrial, and utility-scale distributed energy deployments, with industrial and commercial sectors collectively accounting for over 55% of system demand. It further explores niche segments such as remote electrification, smart cities, and electric vehicle-integrated energy systems, which are witnessing increasing adoption rates exceeding 20% annually.

The scope also includes analysis of digital technologies such as AI-based energy management, IoT-enabled monitoring, and blockchain-based energy trading platforms, which are transforming system efficiency and operational transparency. Additionally, the report evaluates regulatory frameworks, environmental policies, and investment trends influencing market dynamics, providing decision-makers with a holistic understanding of current opportunities and future growth areas within the distributed energy ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

8.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Siemens AG, General Electric Company, Schneider Electric SE, ABB Ltd., Honeywell International Inc., Mitsubishi Electric Corporation, Eaton Corporation plc, Caterpillar Inc., Cummins Inc., Tesla Inc., Enphase Energy Inc., SunPower Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |