Reports

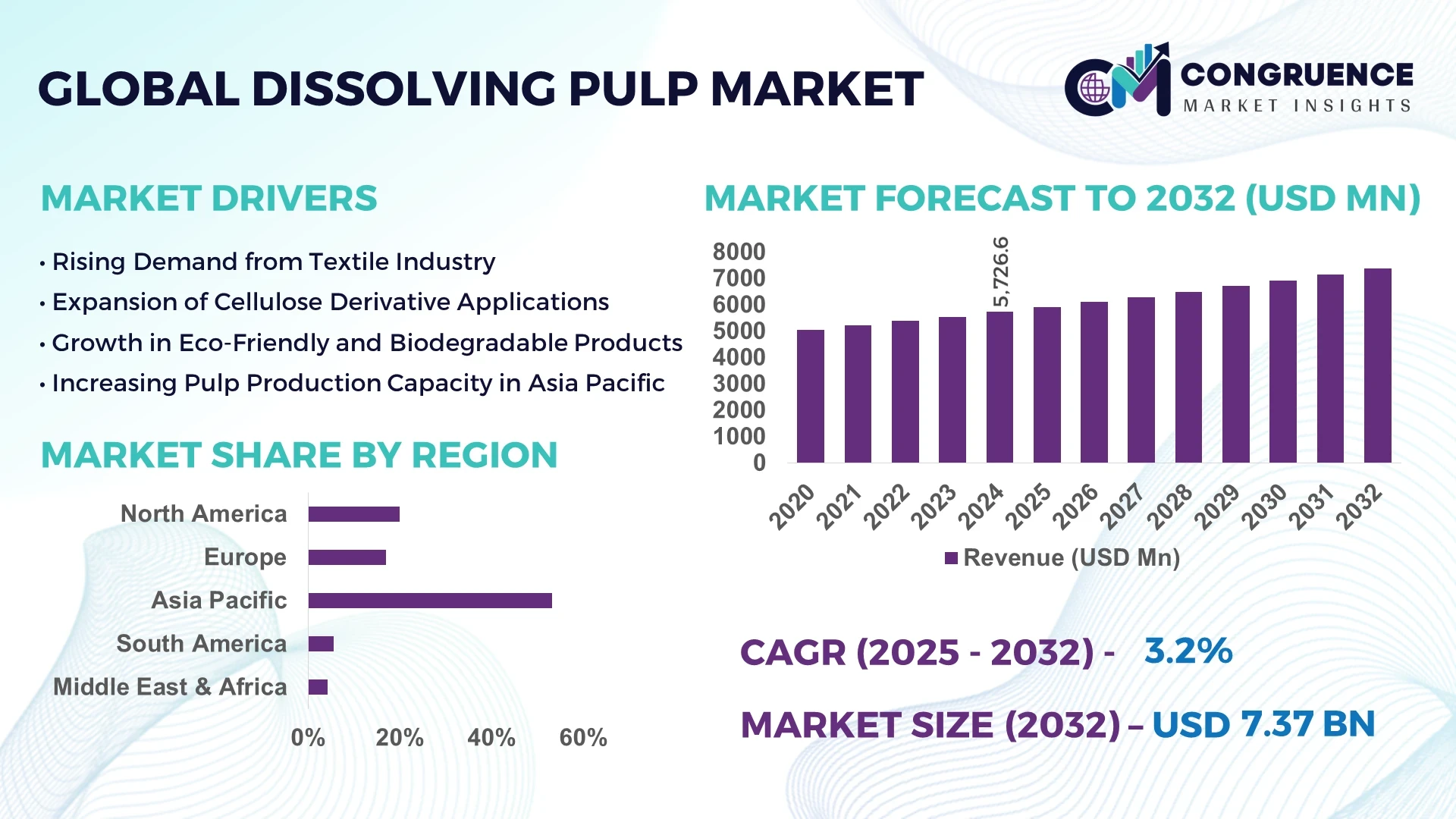

The Global Dissolving Pulp Market was valued at USD 5726.63 Million in 2024 and is anticipated to reach a value of USD 7367.78 Million by 2032, expanding at a CAGR of 3.2% between 2025 and 2032.

To Learn More About This Report, Request A Free Sample Copy

Canada plays a significant role in the global dissolving pulp industry with its advanced processing facilities, sustainable forestry management systems, and continued capital investments in modern fiber conversion technologies, primarily focused on textile-grade viscose production and bioplastics.

The Dissolving Pulp Market serves a diverse range of sectors including textile, pharmaceutical, food additives, cosmetics, and personal care, with the textile industry being the largest end-user. Technological innovations such as enzyme-based pulp processing and energy-efficient pre-treatment techniques are improving yield and reducing environmental impact. Regulatory frameworks focusing on deforestation, carbon emissions, and green supply chain compliance are also influencing production strategies globally. Regions like Southeast Asia and Latin America are witnessing rising consumption due to growing demand for viscose staple fibers and cellulose-based derivatives. Moreover, increasing consumer preference for biodegradable and plant-based alternatives is boosting dissolving pulp adoption across packaging and hygiene applications. With demand for cleaner industrial practices and bio-based inputs, the future outlook of the dissolving pulp industry remains robust and transformation-ready.

Artificial Intelligence is significantly transforming the Dissolving Pulp Market by driving automation, enhancing quality control, and enabling predictive analytics across the value chain. Advanced AI-powered monitoring systems are being used to optimize chemical dosing, pulp consistency, and cooking conditions in real-time, thereby reducing energy consumption and minimizing waste. Machine learning algorithms are analyzing historical process data to predict equipment failures and improve asset uptime, which is particularly crucial in large-scale pulp mills where operational continuity directly impacts output volumes and cost efficiency.

In the supply chain, AI is streamlining raw material procurement and inventory forecasting, ensuring steady fiber availability while controlling input costs. Companies are also leveraging AI models for customer demand forecasting and production scheduling, leading to agile and responsive supply operations. AI-based vision systems are improving product grading and defect detection, delivering consistent quality in dissolving pulp used for viscose, cellulose ethers, and acetate production. Furthermore, AI integration with digital twin technologies is facilitating full-plant simulations to test and refine production adjustments without disrupting actual operations. As sustainability becomes critical, AI helps track environmental metrics such as carbon emissions, water use, and energy efficiency to support ESG compliance. Overall, AI is becoming a central force in shaping a more intelligent, efficient, and competitive Dissolving Pulp Market.

“In 2024, a leading Nordic pulp producer deployed an AI-powered fiber classification system that improved pulp yield accuracy by 8.6% and reduced chemical consumption by 12% during continuous batch processing, significantly enhancing operational efficiency and product consistency.”

The growing global emphasis on sustainable fashion has significantly boosted the demand for viscose and other regenerated cellulose fibers, directly impacting the Dissolving Pulp Market. Brands and consumers are increasingly opting for biodegradable, plant-based fibers over synthetic alternatives like polyester and nylon. As a result, textile-grade dissolving pulp—used in viscose, modal, and lyocell production—has seen a notable increase in consumption. According to recent production figures, over 7 million metric tons of regenerated cellulose fibers were manufactured in 2024, a significant portion of which relied on dissolving pulp. Manufacturers are investing in R&D to enhance pulp purity and fiber yield, improving their product’s appeal across the fashion and apparel supply chain. This eco-conscious shift is reinforcing the strategic importance of sustainable dissolving pulp sourcing and processing.

One of the primary restraints impacting the Dissolving Pulp Market is the increasingly stringent environmental regulations concerning emissions, effluents, and deforestation. Pulp mills are under pressure to reduce sulfur-based emissions and chemical discharges during the pulping and bleaching stages. Compliance with environmental norms like the EU Industrial Emissions Directive and various national forestry laws requires expensive retrofitting and process modifications. Moreover, restrictions on raw material sourcing from old-growth or uncertified forests are tightening global wood pulp supplies, driving up procurement costs. These challenges increase the operational burden on manufacturers, especially in regions with outdated infrastructure. As environmental standards continue to evolve, companies face the dual challenge of maintaining profitability while adhering to strict sustainability mandates.

An emerging opportunity in the Dissolving Pulp Market lies in its expanding use in bioplastics and cellulose-based food additives. As plastic bans tighten globally, manufacturers are developing bio-based films and containers derived from cellulose, a primary output of dissolving pulp. Additionally, food-grade cellulose is gaining traction as a stabilizer, emulsifier, and dietary fiber across bakery, dairy, and processed food industries. With the clean-label movement gaining strength, demand for natural, non-synthetic ingredients is expected to accelerate. Several pulp producers have announced expansions into food and packaging-grade cellulose derivatives, responding to this shift. This diversification into value-added sectors presents a long-term growth pathway for dissolving pulp manufacturers aiming to capitalize on circular economy trends and regulatory support for bio-based alternatives.

A critical challenge facing the Dissolving Pulp Market is the limited and often volatile supply of sustainably sourced wood raw materials. Certification bodies such as FSC and PEFC govern sustainable forest management, but only a fraction of global forests meet these certification standards. As demand increases, producers struggle to secure adequate, certified feedstock without compromising on sustainability benchmarks. Moreover, geopolitical factors, logging restrictions, and rising land-use competition for agriculture further strain raw material availability. In regions like Southeast Asia and South America, deforestation concerns add complexity to sourcing decisions. These supply chain disruptions not only escalate costs but also delay production schedules, threatening the reliability of pulp-based product manufacturing.

• Expansion of Textile-Grade Pulp Production in Asia-Pacific:

Asia-Pacific, particularly China and India, has experienced a significant rise in textile-grade dissolving pulp production to meet growing demand from the viscose fiber industry. In 2024, over 4.2 million metric tons of dissolving pulp were produced in China alone, driven by increasing exports of viscose rayon. Regional governments are supporting production expansion through investment incentives and sustainable forestry practices, while manufacturers are upgrading facilities to deliver higher alpha-cellulose content exceeding 92%, ideal for viscose processing.

• Integration of Closed-Loop Technologies in Pulp Mills:

Modern dissolving pulp facilities are adopting closed-loop water and chemical recovery systems to improve environmental performance. These systems reduce freshwater usage by up to 40% and lower sulfur compound emissions by more than 35%, aligning operations with global environmental mandates. Scandinavian and Canadian producers are leading this shift by incorporating membrane filtration and black liquor recovery technologies, improving both resource efficiency and cost competitiveness.

• Increased Demand from Pharmaceutical and Food Industries:

Pharmaceutical and food-grade dissolving pulp is gaining momentum due to stricter safety and purity requirements. In 2024, demand for microcrystalline cellulose (MCC), derived from high-purity pulp, grew by 14% globally, used extensively in drug formulations and food texturizers. Producers are diversifying their product lines to meet regulatory standards for food and pharma applications, including GMP-compliant manufacturing and ISO-certified quality control.

• Rising Investments in Sustainable Forestry and Certifications:

To secure long-term raw material supply, dissolving pulp manufacturers are significantly investing in certified plantations and sustainable forest management programs. By the end of 2024, over 62% of dissolving pulp used globally was sourced from FSC- or PEFC-certified forests. Companies are expanding afforestation projects and adopting satellite-based monitoring for real-time forest tracking, ensuring transparency and compliance with international deforestation-free sourcing standards.

The Dissolving Pulp Market is strategically segmented based on type, application, and end-user domains, each contributing uniquely to the industry's development. In terms of type, products vary by cellulose content, processing method, and intended use, with both hardwood and softwood pulp varieties seeing widespread deployment. Application-wise, dissolving pulp is extensively utilized in viscose production, followed by cellulose derivatives used in pharmaceuticals, food, and cosmetics. The market’s evolving end-user landscape includes the textile sector as the dominant consumer, while pharmaceuticals and personal care are gaining momentum due to the rising demand for sustainable, plant-based inputs. As regional dynamics shift, demand patterns also change, with Asian markets showing a preference for textile-grade pulp and Western regions focusing more on pharmaceutical and specialty applications. The segmentation reflects an industry balancing established applications with new innovations, highlighting the importance of tailored strategies for each vertical to remain competitive in a resource-sensitive market.

Textile-grade dissolving pulp remains the most widely consumed type in the market, primarily due to its high alpha-cellulose content and low hemicellulose levels, which make it ideal for producing viscose rayon and modal fibers. This type commands the majority share, especially in regions like Asia-Pacific, where the textile industry drives large-scale consumption. High-purity specialty-grade pulp is emerging as the fastest-growing segment, fueled by increasing demand from pharmaceutical, food, and electronics sectors that require consistent quality and stringent purity levels. These grades are essential for manufacturing microcrystalline cellulose, used in drug formulations and food processing. Other types, such as acetate-grade and ether-grade pulp, serve niche applications, including film coatings, cigarette filters, and performance-enhancing cellulose derivatives. Although smaller in volume, their specialized use cases contribute to steady demand across high-value verticals. The market’s segmentation by type reflects its diverse end-use alignment, allowing producers to innovate and meet specific industrial performance requirements.

Viscose fiber production continues to dominate the application segment of the Dissolving Pulp Market, supported by robust demand from the global fashion and apparel industry. In 2024 alone, over 70% of global dissolving pulp output was channeled into viscose and related regenerated fibers, due to their biodegradability and suitability for large-scale textile manufacturing. The fastest-growing application is in pharmaceutical and food processing, where dissolving pulp is used to derive additives such as microcrystalline cellulose and carboxymethyl cellulose. These substances serve as excipients in tablets, stabilizers in dairy, and thickeners in processed food, driven by the global clean-label movement and rising health awareness. Additional applications include cellophane film, cellulose acetate for photographic films and cigarette filters, and specialty polymers. Though smaller in scale, these segments offer consistent demand due to their technical performance and regulatory compliance benefits. The diversification of applications across both industrial and consumer-facing products underscores dissolving pulp’s strategic value in sustainable innovation.

The textile industry remains the leading end-user of dissolving pulp, driven by mass-scale adoption of viscose and modal fibers for clothing, home textiles, and industrial fabrics. The increasing global shift toward biodegradable and renewable materials has reinforced this sector’s dominance. In 2024, textile manufacturers accounted for the largest consumption share, particularly in fast-growing markets across China, India, and Bangladesh. The pharmaceutical industry is emerging as the fastest-growing end-user segment, supported by the expanding demand for high-purity cellulose in oral solid dosage forms, dietary supplements, and drug delivery systems. This surge is underpinned by advancements in tablet formulations and rising global medication consumption. Other important end-users include food and beverage companies, which utilize cellulose derivatives for texture, stability, and fiber enhancement, as well as the personal care industry for thickeners in cosmetics and hygiene products. This broad end-user base highlights the market’s cross-industry relevance and the expanding applications of dissolving pulp in sustainability-aligned product development.

Asia-Pacific accounted for the largest market share at 53.2% in 2024; however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 4.1% between 2025 and 2032.

To Learn More About This Report, Request A Free Sample Copy

Asia-Pacific’s dominance stems from extensive textile manufacturing, high consumer demand, and continuous investment in large-scale dissolving pulp production facilities. The region has also seen government backing for sustainable raw material sourcing. Meanwhile, Middle East & Africa are witnessing rising demand for biodegradable materials in industrial packaging, pharmaceuticals, and construction, supported by regulatory reforms, growing environmental awareness, and increasing industrial diversification. The global dissolving pulp market is shaped by regional priorities—from Asia’s large-scale output to Europe’s sustainability mandates and North America’s pharmaceutical advances. Regional consumption patterns, infrastructure developments, and regulatory frameworks collectively shape demand dynamics. As the industry matures, localized supply chain optimization, digital technologies, and sustainable forestry practices are expected to enhance competitiveness across various geographies.

Strong Demand in Cellulose-Based Pharmaceuticals and Bioplastics

North America held a market share of 18.7% in 2024, driven by increasing consumption of high-purity dissolving pulp in pharmaceutical formulations and the rise of cellulose-based bioplastics. The United States leads the region with growing investments in specialty-grade pulp mills catering to pharmaceutical-grade MCC and CMC applications. The U.S. FDA’s evolving regulatory framework on plant-based drug excipients has encouraged the domestic production of highly refined cellulose pulp. Canada, meanwhile, is prioritizing sustainability and closed-loop production models, backed by federal incentives for green manufacturing. Technological upgrades like AI-assisted quality control and chemical recovery systems are reshaping operational efficiency, reducing waste and enhancing purity standards in the dissolving pulp market.

Innovation Driven by Circular Economy and Green Policies

Europe captured a market share of 14.6% in 2024, with Germany, France, and Sweden emerging as key hubs for dissolving pulp demand. The region’s strong push toward circular economy practices has led to widespread adoption of certified sustainable pulp in textiles and personal care sectors. EU environmental policies—particularly the Green Deal and Forest Strategy—are reshaping sourcing norms and production techniques. Germany has seen growth in the textile-grade pulp sector, while Sweden is investing heavily in specialty pulp for hygiene and food-grade applications. Technological advancements such as enzymatic pre-treatment and low-emission bleaching have become standard in modern European pulp mills.

Rapid Industrialization and Fiber Manufacturing Expansion

Asia-Pacific dominated the market in 2024 with a commanding 53.2% share, supported by robust demand from textile and fashion industries. China is the top consumer and producer, with over 4.2 million metric tons of dissolving pulp output, followed by India and Indonesia, which are scaling up operations for both domestic use and export. The region benefits from integrated supply chains, skilled labor, and low-cost production facilities. Japan is advancing high-end cellulose applications in electronics and pharmaceuticals. Smart factories and automation, particularly in Chinese pulp plants, are optimizing yield and enhancing environmental compliance. Regional manufacturing hubs are further investing in biomass-based energy solutions to support sustainable growth.

Government-Led Forestry Incentives and Export-Driven Growth

South America held a 7.9% share in 2024, with Brazil and Argentina dominating production due to abundant eucalyptus plantations and favorable government policies. Brazil alone accounts for over 80% of the region’s dissolving pulp output, primarily for export to Asia and Europe. The Brazilian government has incentivized sustainable forestry through tax credits and investment grants. The region is also investing in energy-efficient pulp mills equipped with cogeneration facilities and chemical recovery systems. Argentina is seeing moderate growth in domestic consumption, with rising interest from pharmaceutical and food industries. Trade partnerships with Asia-Pacific countries are reinforcing South America's role as a global supplier.

Emerging Growth Through Industrial Diversification and Sustainability Goals

Middle East & Africa recorded the fastest regional growth trajectory in 2024, with expanding demand from countries like the UAE and South Africa. Industrial sectors in the region are shifting toward biodegradable materials in packaging, food, and construction. UAE’s Vision 2031 and South Africa’s green economy roadmap have accelerated interest in cellulose-based materials, including dissolving pulp. The region’s investment in agri-industrial infrastructure and sustainable raw material sourcing is laying the groundwork for domestic pulp production. Technological modernization, including digital monitoring of plantations and AI-driven process control, is gaining momentum. Regional collaborations for trade and regulatory alignment are also fostering market development.

China – 38.5% market share

High production capacity, integrated supply chains, and dominant textile-grade pulp manufacturing.

Brazil – 12.3% market share

Strong export capability backed by sustainable eucalyptus plantations and government incentives.

The competitive landscape of the Dissolving Pulp market is shaped by over 45 active global and regional players, each vying for strategic positioning through product innovation, capacity expansion, and sustainability-led initiatives. The market is moderately consolidated, with the top five manufacturers accounting for a significant portion of global production capacity. Companies are increasingly investing in advanced pulp processing technologies, including enzyme-based treatment, closed-loop chemical recovery systems, and AI-integrated monitoring platforms. Strategic collaborations between pulp producers and textile manufacturers are on the rise, aiming to secure long-term demand in the viscose and lyocell fiber markets. Several players have entered joint ventures to enhance their supply chains and raw material sourcing, especially in regions like Asia-Pacific and South America. Mergers and acquisitions have also played a key role in strengthening portfolios and expanding geographic reach. Competitive differentiation is now heavily influenced by ESG compliance, low-carbon operations, and vertical integration. Market leaders are prioritizing digital transformation and traceability to meet evolving regulatory and customer expectations across end-user sectors such as pharmaceuticals, textiles, and personal care.

Lenzing AG

Rayonier Advanced Materials Inc.

Sappi Limited

Bracell Limited

Domtar Corporation

Aoyang Technology Co., Ltd.

Grasim Industries Limited

Sun Paper Group

Sichuan Vanov New Material Co., Ltd.

Fortress Global Enterprises Inc.

Technological advancements in the Dissolving Pulp market are driving significant improvements in efficiency, sustainability, and product quality. One of the most notable shifts is the widespread adoption of pre-hydrolysis kraft (PHK) and acid sulfite processes to achieve high-purity cellulose with low hemicellulose content, which is crucial for downstream applications such as viscose rayon and lyocell production. Modern plants are integrating enzymatic pretreatment systems, which enhance fiber separation and reduce the need for aggressive chemical bleaching. This not only improves yield but also aligns with tightening environmental regulations in North America and Europe.

Automation and AI-powered control systems are now being deployed to monitor pulp consistency, optimize energy consumption, and predict maintenance needs. These digital tools help minimize downtime and reduce energy usage by up to 15%, especially in facilities operating at large scale. In parallel, chlorine-free bleaching technologies, such as oxygen and ozone-based systems, are replacing older elemental chlorine methods, resulting in safer effluent discharge and improved fiber quality.

In addition, bio-refinery integration is emerging as a key technological trend, allowing manufacturers to extract lignin, acetic acid, and other by-products from wood biomass. These value-added outputs support circular economy principles and diversify revenue streams for pulp manufacturers, particularly in regions like Scandinavia and Southeast Asia.

• In August 2024, Sappi Limited completed the upgrade of its Ngodwana Mill in South Africa, increasing dissolving pulp output by 75,000 tons annually. The modernization includes a new oxygen delignification system and enhanced fiberline controls to improve pulp purity and reduce chemical consumption.

• In March 2024, Bracell launched a new 100% traceable dissolving pulp product line at its São Paulo facility using blockchain-integrated logistics. This advancement allows real-time tracking from plantation to customer, enhancing transparency for textile manufacturers seeking sustainable sourcing verification.

• In November 2023, Grasim Industries began pilot testing of enzymatic pre-treatment at its Harihar unit in India, targeting enhanced reactivity in cellulose fibers. The test phase demonstrated a 12% improvement in pulp brightness and a 9% reduction in caustic soda consumption during processing.

• In July 2023, Rayonier Advanced Materials announced the implementation of AI-driven process optimization software at its Jesup, Georgia plant. Early results indicated a 10% gain in throughput and a 6% reduction in steam usage, contributing to lower operational costs and improved resource efficiency.

The Dissolving Pulp Market Report offers an in-depth analysis of the global landscape, encompassing key segments by type, application, and end-user. The report evaluates sulfite and kraft-based dissolving pulps, with specific attention to variants like pre-hydrolysis kraft and acid sulfite processes. These segments are assessed based on purity levels, fiber characteristics, and their suitability for end-use industries including textiles, pharmaceuticals, personal care, food additives, and industrial chemicals. The geographical coverage includes major regions such as North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. The report gives particular emphasis to high-consumption countries like China, India, Brazil, the United States, and Germany, where industrial applications and infrastructure development drive substantial demand. It also identifies regional manufacturing strengths, trade flow patterns, and import-export dynamics across these territories.

In terms of applications, the scope includes viscose rayon, lyocell, cellulose acetate, microcrystalline cellulose (MCC), and nitrocellulose. Market demand trends across these verticals are detailed with focus on fiber quality, processing compatibility, and environmental compliance. On the technology front, the report evaluates current advancements in bleaching techniques, AI-integrated automation systems, and closed-loop chemical recovery systems. It also touches on innovation in enzymatic treatments and blockchain-based traceability for sustainable sourcing. This comprehensive market report provides stakeholders with actionable insights for strategic planning, investment analysis, and opportunity identification across core and niche segments of the dissolving pulp value chain.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 5726.63 Million |

|

Market Revenue in 2032 |

USD 7367.78 Million |

|

CAGR (2025 - 2032) |

3.2% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

DJI Innovations, FLIR Systems Inc., Lockheed Martin Corporation, Teledyne Technologies Incorporated, Parrot Drones SAS, Northrop Grumman Corporation, PrecisionHawk Inc., AgEagle Aerial Systems Inc., AeroVironment Inc., Delair SAS |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |