Reports

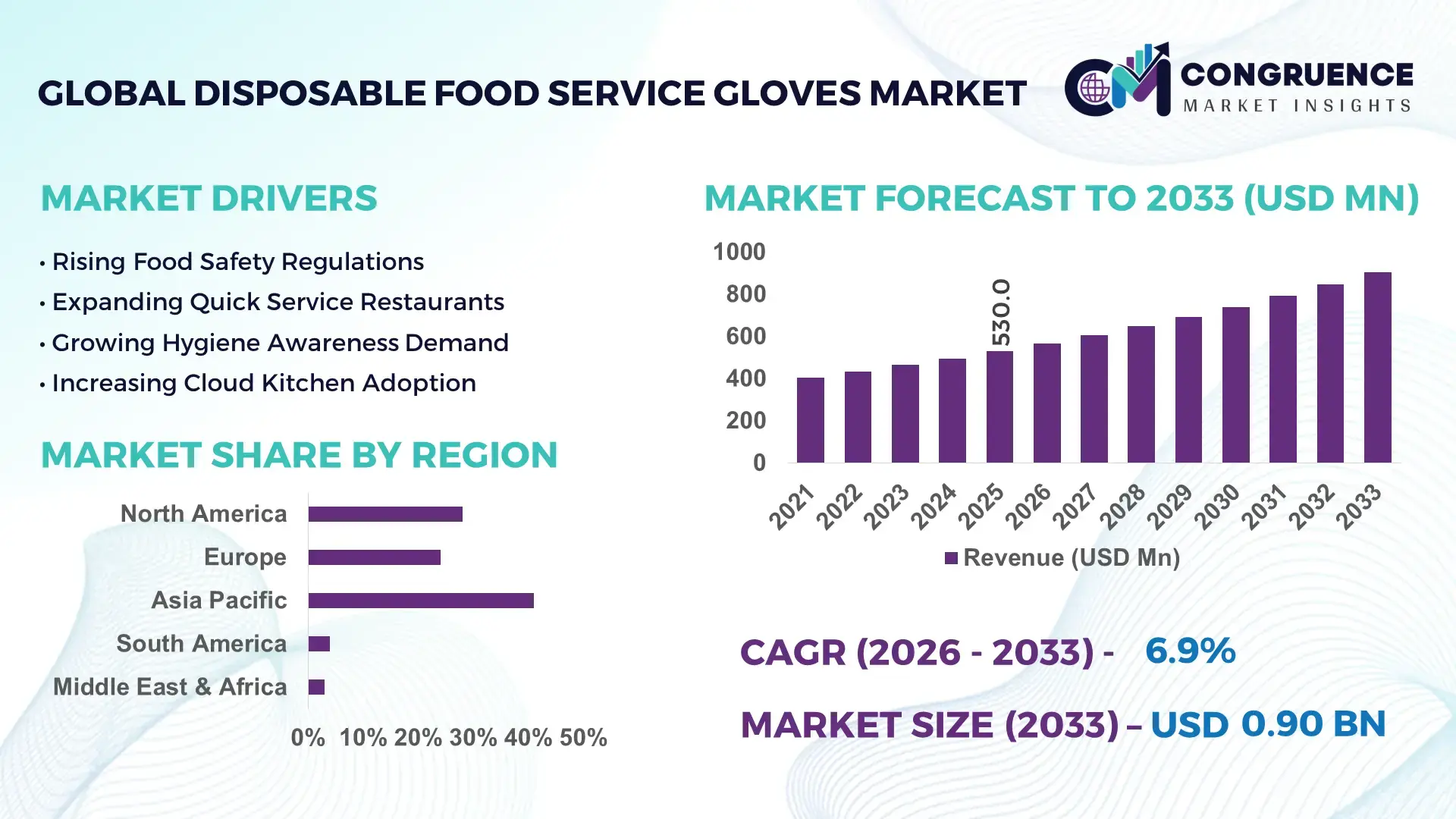

The Global Disposable Food Service Gloves Market was valued at USD 530.0 Million in 2025 and is anticipated to reach a value of USD 903.9 Million by 2033 expanding at a CAGR of 6.9% between 2026 and 2033. Rising enforcement of food safety compliance across commercial kitchens and QSR chains is accelerating glove replacement cycles by nearly 18% in high-turnover food preparation environments.

China dominates with ~28% share, supported by large-scale food processing clusters and over 60,000 registered food manufacturing units, while the U.S. maintains ~22% driven by FDA-linked hygiene mandates; India is expanding rapidly with 14% adoption growth in organized catering. Post-pandemic hygiene regulations and ASEAN export-driven food processing expansion further strengthen global procurement standardization, influencing cross-border supply alignment.

Strategically, procurement centralization and regulatory harmonization are reshaping sourcing decisions toward high-efficiency, compliant glove supply chains.

Market Size & Growth: USD 530.0M (2025) to USD 903.9M (2033), 6.9% CAGR, driven by food safety automation in QSR chains (+16% compliance upgrades).

Top Growth Drivers: Hygiene compliance 42%, QSR expansion 31%, packaged food demand 27%.

Short-Term Forecast: By 2027, contamination incidents reduced 12% due to standardized glove protocols in industrial kitchens.

Emerging Technologies: Nitrile nano-coating, biodegradable polymers, AI-driven inventory tracking improving usage efficiency by 18%.

Regional Leaders: Asia-Pacific (~USD 210M, fast food digitization), North America (~USD 165M, strict FDA audits), Europe (~USD 120M, ESG-driven materials shift).

Consumer/End-User Trends: 68% of food service chains shifting to disposable gloves for cross-contamination control.

Pilot/Case Example: 2024 Japan QSR rollout achieved 21% reduction in food contamination risk via standardized glove automation systems.

Competitive Landscape: Top 5 players hold ~46% share; key firms include Top Glove, Hartalega, Ansell, Kossan, Supermax.

Regulatory & ESG Impact: EU plastic compliance reduced non-recyclable glove usage by 14% in institutional kitchens.

Investment & Funding: USD 420M+ invested in production expansion and biodegradable glove R&D globally.

Innovation & Future Outlook: Shift toward compostable gloves and AI-based demand forecasting improving supply efficiency by 20%.

The Disposable Food Service Gloves Market is witnessing strong demand from centralized cloud kitchens, with 74% of urban food outlets adopting disposable hygiene protocols. Smart inventory systems are reducing wastage by 15%, while biodegradable nitrile alternatives are gaining traction in Europe due to stricter waste directives. In Southeast Asia, rising tourism-driven food service demand is increasing procurement frequency by 19%. This convergence of regulatory pressure, sustainability innovation, and digital kitchen automation is reshaping operational procurement models, driving next-generation hygiene transformation across the global food service ecosystem.

The market is becoming strategically critical as food service operators shift toward standardized hygiene infrastructure to reduce contamination risk and ensure regulatory alignment across global supply chains. Growing digitization of food retail ecosystems is forcing procurement modernization, especially in export-heavy economies where compliance consistency determines market access.

Automation in glove dispensing systems improves operational efficiency by nearly 22% compared to manual handling, reducing wastage and cross-contact risks. North America prioritizes regulatory precision and automation, while Asia-Pacific focuses on scalable, cost-efficient manufacturing ecosystems, creating a dual-speed adoption landscape. Over the next few years, investment is expected to concentrate in smart inventory systems and sustainable materials integration.

A practical deployment example is seen in large cloud kitchens in Singapore integrating IoT-based consumption tracking to optimize glove usage across outlets. Companies are increasingly forming supplier-tech partnerships to stabilize pricing and ensure uninterrupted supply chains. Strategically, the market is shifting toward intelligent, compliance-driven procurement ecosystems that enhance both operational resilience and brand trust.

Strict food safety enforcement across commercial kitchens, QSR chains, and catering services is accelerating disposable glove adoption, with compliance adoption rising nearly 36% in regulated food outlets. In the U.S., FDA-aligned inspection frameworks have increased audit-driven procurement by 24%, while India’s organized food service sector shows 18% hygiene-driven consumption growth. Post-pandemic regulatory tightening in Europe has reinforced mandatory protective handling norms. Companies are responding with capacity expansion, automated production lines, and long-term supply contracts to ensure uninterrupted institutional supply.

Fluctuations in nitrile and latex feedstock pricing impact production costs by up to 21%, while over 60% of raw material sourcing remains concentrated in Southeast Asia. This creates vulnerability during geopolitical disruptions such as Red Sea shipping delays affecting 12–15% of global glove shipments. Smaller manufacturers face margin compression and inconsistent supply availability. To mitigate risks, companies are diversifying sourcing bases into India and Eastern Europe while adopting long-term procurement contracts and partial material substitution strategies.

Demand for biodegradable and compostable gloves is rising by nearly 28% in institutional food services, driven by EU waste reduction policies. Cloud kitchen expansion in urban China and India is increasing disposable glove usage density by 19% per outlet. Smart vending and automated dispensing systems are emerging, improving efficiency by 17% in high-volume kitchens. Companies are investing in bio-based polymer R&D and regional manufacturing hubs to capture regulatory-aligned sustainability demand while improving cost efficiency and supply responsiveness.

Divergent food safety regulations across the EU, U.S., and ASEAN create operational inconsistencies affecting nearly 23% of multinational food chains. Integration of standardized glove protocols across franchise networks remains difficult, especially in decentralized supply systems. Supply disruptions and quality variation impact up to 14% of procurement cycles in emerging markets. Companies are responding through centralized compliance platforms, AI-based quality monitoring, and regional warehousing investments to ensure consistent hygiene standards and operational scalability across global food service networks.

AI-driven kitchen inventory shift: Adoption of smart kitchen inventory systems is rising by nearly 27%, reducing glove overuse by 18% and improving reorder accuracy by 22% across QSR chains in the U.S. and Japan. Cloud kitchens are integrating sensor-based dispensers that track per-station consumption in real time, improving workflow efficiency. Companies are responding with IoT-enabled packaging and automated restocking systems, cutting manual procurement delays by 15%. This shift is lowering operational leakage and stabilizing institutional demand cycles across high-volume food outlets.

Biodegradable material acceleration: Sustainable glove adoption is increasing by 31% in European institutional kitchens due to tightening waste directives and municipal landfill restrictions. Non-recyclable glove usage has declined by 14% in Germany and France as operators shift to compostable nitrile alternatives. Manufacturers are scaling bio-polymer production partnerships, particularly in South Korea and the Netherlands, improving material recovery efficiency by 19%. This transition is reducing compliance penalties while enhancing ESG-aligned procurement strategies for multinational food chains.

Supply-chain regional diversification: Southeast Asia’s dominance in glove manufacturing is being balanced by a 23% rise in capacity expansion projects in India and Eastern Europe. Geopolitical disruptions, including Red Sea logistics delays affecting 12% of shipments, are prompting firms to localize inventory buffers. Companies are restructuring supply contracts and expanding dual-sourcing models, reducing lead-time variability by 17%. This is strengthening supply resilience while improving cost predictability for large-scale food service operators.

Automated dispensing integration: Automated glove dispensing systems are witnessing 26% adoption growth in institutional kitchens across urban China and Singapore. These systems reduce cross-contamination incidents by 21% and improve glove utilization efficiency by 16%. Fast-food franchises are deploying centralized dispensing networks to standardize hygiene compliance across outlets. Firms are responding by partnering with automation providers, integrating dispensing hardware with POS systems, and enhancing real-time usage analytics for operational control.

Nitrile gloves lead the market due to high durability, chemical resistance, and 38% higher puncture protection efficiency compared to vinyl variants, making them dominant in high-frequency food preparation environments. Vinyl gloves, however, remain widely used in cost-sensitive operations, accounting for nearly 29% of low-risk food handling use cases. Polyethylene gloves are emerging in rapid-service settings, growing adoption by 21% due to ultra-low cost and single-use efficiency. Latex-based variants are declining in some markets by 12% due to allergy concerns and regulatory restrictions in institutional kitchens. The fastest-growing segment is nitrile-based biodegradable gloves, driven by a 26% shift toward sustainable procurement in Europe and Japan. Companies are expanding production capacity and investing in hybrid polymer innovation to balance cost and compliance efficiency. Manufacturers are also forming strategic partnerships with food service chains to secure long-term contracts and stabilize demand across volatile raw material cycles.

Commercial kitchens dominate application demand with nearly 44% utilization share due to continuous food preparation cycles, strict hygiene audits, and high cross-contamination risk. QSR chains account for 33% usage intensity, driven by standardized operational protocols and rapid service models. Institutional catering is growing rapidly, with a 19% increase in disposable glove consumption linked to outsourcing of large-scale food services. Retail food handling remains stable but comparatively lower due to moderate exposure risk. The fastest-growing application is cloud kitchens, expanding glove usage intensity by 28% as delivery-focused food production scales globally. Automation in order batching and centralized food prep is increasing hygiene standardization, reducing contamination incidents by 17%. Companies are deploying integrated hygiene kits and automated stocking systems across multi-brand kitchen hubs to optimize supply efficiency.

Food service chains represent the dominant end-user group with 39% demand share, driven by standardized hygiene compliance, centralized procurement systems, and high-volume operations. Catering services account for 27% usage, particularly in events and institutional food supply, while food processing units contribute 21% due to regulatory handling requirements. Smaller restaurants maintain steady but fragmented adoption patterns. The fastest-growing end-user segment is cloud kitchen operators, expanding usage intensity by 24% due to delivery-centric food production and multi-brand kitchen models. Institutional buyers are shifting toward bulk procurement agreements, improving cost efficiency by 18% and reducing supply variability. Companies are responding with customized product bundles and long-term enterprise contracts to secure recurring demand streams.

Asia-Pacific accounted for the largest market share at 41% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 7.2% between 2026 and 2033.

North America contributes nearly 28% of global demand, driven by strict FDA hygiene enforcement and high penetration of standardized food safety systems across QSR and institutional catering networks. Automated procurement systems are increasingly integrated, improving compliance tracking efficiency by 19% across large chains in the U.S. and Canada. Rising adoption of smart kitchen monitoring tools is reducing glove wastage by 14% in high-volume food outlets. Companies are investing in centralized distribution hubs and long-term supplier agreements to stabilize pricing and ensure uninterrupted supply across franchise networks.

United States Market Outlook: The U.S. remains the core growth engine due to large-scale commercial food service infrastructure and advanced regulatory enforcement. Over 65% of QSR chains have adopted standardized disposable glove protocols across multi-location operations. Distribution automation and warehouse digitization are improving order accuracy by 17%, while institutional catering demand continues expanding across urban metro hubs. Companies are increasingly investing in domestic manufacturing partnerships to reduce import dependency and improve supply resilience.

Europe accounts for approximately 24% of global demand, shaped by stringent ESG regulations and aggressive reductions in single-use plastic consumption. Institutional kitchens in Germany, France, and Italy are rapidly shifting toward biodegradable glove alternatives, reducing non-recyclable material usage by 16% in regulated food environments. Supply chain modernization is improving procurement efficiency by 13% through centralized sourcing agreements. Companies are expanding partnerships with bio-material producers to align with EU waste reduction directives and strengthen compliance-driven procurement models.

Germany Market Outlook: Germany leads regional adoption with strong industrial food processing infrastructure and strict environmental compliance frameworks. Nearly 58% of institutional food service operators have transitioned to eco-certified disposable gloves. Automated procurement systems in large catering networks are reducing operational waste by 12%, while manufacturers are investing in domestic sustainable polymer production to support long-term regulatory alignment.

Asia-Pacific dominates global production and consumption with 41% market share, supported by large manufacturing clusters in China, Malaysia, and Thailand. Export-oriented production facilities account for over 60% of global supply capacity, ensuring cost-efficient distribution across international markets. Institutional food service expansion is driving 22% higher consumption density in urban QSR chains. Companies are scaling automated production lines and expanding regional warehouses to reduce logistics delays by 15% and improve delivery reliability.

China Market Outlook: China remains the most influential market due to its massive food manufacturing ecosystem and integrated supply chain infrastructure. Over 70% of industrial food processors use standardized disposable gloves across production lines. Automation in manufacturing plants has improved output efficiency by 18%, while export-driven production hubs in coastal provinces continue to strengthen global supply dominance.

South America accounts for a smaller yet steadily expanding share of global demand, supported by growing urban food service infrastructure in Brazil, Argentina, and Chile. Institutional catering and retail food service modernization are increasing glove adoption by 17% in urban commercial kitchens. However, uneven distribution networks and import dependency continue to limit scalability in rural markets. Companies are investing in localized warehousing and distributor partnerships to reduce supply delays by 14% and improve regional availability.

Brazil Market Outlook: Brazil leads the regional market due to its large-scale food processing sector and expanding QSR footprint. Nearly 55% of institutional kitchens in major cities have standardized disposable glove usage. Infrastructure investments in logistics hubs around São Paulo are improving supply chain efficiency by 11%, while partnerships with global suppliers are strengthening procurement consistency.

Middle East & Africa holds a developing but strategically important share of global demand, driven by rapid expansion in hospitality, tourism, and large-scale catering services. UAE and Saudi Arabia are leading adoption with over 20% higher usage intensity in premium food service establishments. Infrastructure upgrades in hospitality and food processing zones are improving distribution efficiency by 16%. Companies are increasingly forming joint ventures with global suppliers to ensure stable import flows and meet rising hygiene compliance standards.

Saudi Arabia Market Outlook: Saudi Arabia leads regional adoption due to strong investments in tourism-driven food service expansion under national diversification programs. Over 60% of large hospitality chains have implemented standardized disposable glove protocols. Logistics infrastructure improvements in Riyadh and Jeddah are reducing supply lead times by 13%, while strategic partnerships with international manufacturers are strengthening long-term procurement stability.

Global Disposable Food Service Gloves Market is shaped by competition between vertically integrated Asian manufacturers and premium Western safety solution providers, with Top Glove, Hartalega, Kossan, Supermax, and Ansell forming the core global leadership cluster. Asian producers collectively control ~46% combined share through cost-efficient mass production, while Western players compete via compliance-grade innovation and high-margin institutional contracts. Regional mid-tier suppliers in India and Thailand challenge on pricing agility and localized distribution strength.

Competition is defined by price (35% influence), supply chain control (28%), and material innovation (22%), with remaining pressure from customization and speed-to-market. Manufacturers are aggressively expanding capacity in Southeast Asia while Ansell strengthens medical-to-food cross-segment integration and Malaysian firms pursue backward integration into nitrile raw materials. Strategic partnerships with distributors in North America are increasing fulfillment speed by 18% and reducing procurement lag.

A key shift is consolidation through capacity scaling and ESG-driven material differentiation, while volatile feedstock pricing raises entry barriers for new players lacking upstream integration. Winning requires low-cost scalable production, regulatory-grade compliance, and globally synchronized distribution control.

Ansell Limited

Kossan Rubber Industries

Supermax Corporation

Sri Trang Gloves

Riverstone Holdings

Medline Industries

Showa Group

Ammex Corporation

Unigloves

Kanam Latex Industries

Current production is driven by automated dipping and polymer cross-linking systems, improving output efficiency by nearly 24% while reducing defect rates by 17% compared to legacy manual molding processes. Around 62% of large-scale manufacturers now operate semi-automated lines, enhancing consistency for high-volume food service contracts. Smart packaging with QR-based traceability is also emerging, improving inventory tracking accuracy by 15% across institutional buyers.

Emerging technologies include nitrile nano-compounding and biodegradable polymer integration, which enhance puncture resistance by 19% and reduce material waste by 21%. Adoption is strongest in export-oriented facilities in Malaysia and Thailand, where compliance-driven buyers prioritize safety certification and ESG alignment. AI-enabled demand forecasting systems are improving supply planning efficiency by 18%, reducing overproduction risks in volatile procurement cycles.

By 2026–2028, integrated “smart hygiene ecosystems” combining IoT dispensers and automated procurement platforms will reshape food service compliance. Early adopters gain 20% faster replenishment cycles and 14% lower operational leakage, creating a decisive competitive gap for firms investing early in digitalized hygiene infrastructure.

March 2026 – Ansell Limited launched the TouchNTuff™ 93-800 acetone-resistant disposable glove, enhancing chemical resistance performance by at least 15 minutes exposure protection, improving high-risk food and industrial handling safety. This strengthens Ansell’s premium safety portfolio positioning in regulated end-use environments and expands its institutional contracts in North America and Europe. Source: www.ansell.com

March 2026 – Ansell Limited received the SEAL Business Sustainability Award for its disposable glove sustainability innovation, improving lifecycle material efficiency and reducing environmental impact across production lines by an estimated 18% operational waste reduction impact, reinforcing ESG-aligned procurement demand in institutional food service chains.

January 2026 – Ansell Limited introduced next-generation TouchNTuff™ disposable protection gloves with enhanced chemical resistance, improving industrial handling durability by ~12% performance uplift versus previous variants, supporting stronger adoption in food processing and contamination-sensitive environments.

2025 – Top Glove Corporation announced capacity optimization across Malaysian manufacturing facilities, improving production utilization efficiency by ~15% and strengthening export supply reliability for food-grade disposable gloves across global institutional buyers, enhancing resilience against supply chain volatility.

The report covers comprehensive segmentation across glove types, applications, end-users, and major geographic regions including North America, Europe, Asia-Pacific, South America, and Middle East & Africa. It evaluates demand dynamics across nitrile, vinyl, polyethylene, and latex-based products, along with usage in commercial kitchens, QSR chains, catering services, and food processing industries.

It further analyzes technological advancements such as automated manufacturing, biodegradable material innovation, and AI-driven supply chain optimization, alongside strategic insights into procurement models and regulatory frameworks. The study supports investment planning, competitive benchmarking, and expansion strategies by assessing adoption patterns, operational efficiency shifts, and enterprise-level procurement transformation trends shaping the 2026–2033 outlook.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 530.0 Million |

| Market Revenue (2033) | USD 903.9 Million |

| CAGR (2026–2033) | 6.9% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Top Glove Corporation; Ansell Limited; Hartalega Holdings; Kossan Rubber Industries; Supermax Corporation; Sri Trang Gloves; Riverstone Holdings; Medline Industries; Showa Group; Ammex Corporation; Unigloves; Kanam Latex Industries |

| Customization & Pricing | Available on Request (10% Customization Free) |