Reports

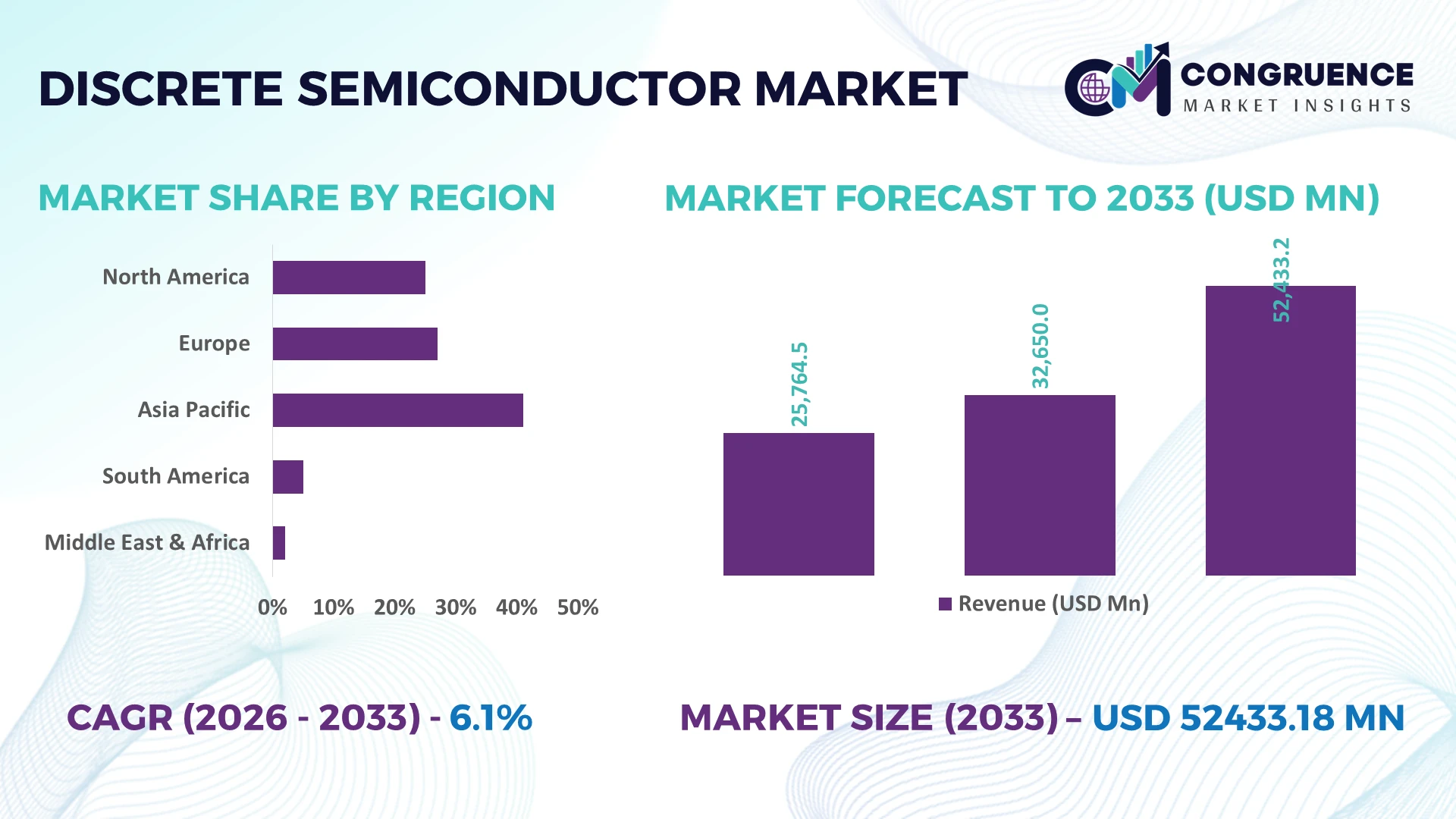

The Global Discrete Semiconductor Market was valued at USD 32650 Million in 2025 and is anticipated to reach a value of USD 52433.18 Million by 2033 expanding at a CAGR of 6.1% between 2026 and 2033. Rapid electrification across automotive platforms, high-voltage power conversion deployments, industrial automation upgrades, and AI-driven power infrastructure expansion are accelerating demand for advanced discrete semiconductor devices with higher efficiency and thermal performance.

China remains the dominant country, accounting for approximately 38% of global manufacturing capacity, supported by investments exceeding USD 45 billion in semiconductor expansion and strong demand from electric vehicles, consumer electronics, and industrial equipment. Compared with the United States, which leads in high-performance device innovation, China delivers larger production volumes, while export control measures continue reshaping regional supply chains. Wide-bandgap device adoption has exceeded 22% across new high-power applications, strengthening manufacturing resilience.

Strategic investment in diversified manufacturing, advanced power devices, and regional supply-chain resilience remains essential for sustaining competitive advantage.

Market Size & Growth: USD 32650 Million (2025) to USD 52433.18 Million (2033) at 6.1% CAGR, driven by EV power electronics and AI infrastructure expansion.

Top Growth Drivers: EV adoption (+24%), industrial automation (+18%), renewable power installations (+21%) strengthen global demand.

Short-Term Forecast: By 2027, power conversion efficiency improves by 15% through silicon carbide and gallium nitride integration.

Emerging Technologies: AI-enabled power management, SiC devices, and GaN components accelerate high-efficiency semiconductor deployment.

Regional Leaders: Asia-Pacific exceeds USD 24 billion, North America surpasses USD 11 billion, Europe approaches USD 9 billion, supported by regional manufacturing expansion.

Consumer/End-User Trends: More than 42% of new EV platforms integrate advanced discrete power devices for higher energy efficiency.

Pilot/Case Example: 2026 smart manufacturing deployment reduced semiconductor production defects by 19% using AI-based inspection.

Competitive Landscape: Top manufacturer holds approximately 14% share alongside Infineon, ON Semiconductor, STMicroelectronics, Vishay, and Rohm.

Regulatory & ESG Impact: Energy-efficiency standards reduce power losses by over 12%, supporting global industrial sustainability targets.

Investment & Funding: More than USD 20 billion supports fab expansion, strategic partnerships, and supply-chain diversification across major regions.

Innovation & Future Outlook: Advanced packaging, 200 mm SiC production, and intelligent power modules strengthen next-generation semiconductor competitiveness.

Discrete Semiconductor Market demand continues expanding across electric mobility, renewable energy systems, industrial drives, and AI data center power architectures. Manufacturers are accelerating silicon carbide and gallium nitride product innovation while increasing automation throughout fabrication facilities. Wide-bandgap devices now represent over 22% of new high-power designs, as regional supply-chain diversification and industrial policy initiatives reinforce production resilience, setting the stage for deeper strategic market analysis.

Discrete semiconductors have become a strategic foundation for power-efficient electronics as industries prioritize electrification, AI computing infrastructure, and resilient manufacturing ecosystems. Competition increasingly centers on securing advanced fabrication capacity, expanding silicon carbide (SiC) and gallium nitride (GaN) production, and reducing dependence on concentrated supply networks. Supply-chain restructuring following export restrictions and national semiconductor initiatives is accelerating localized manufacturing investments while strengthening long-term sourcing resilience for automotive, industrial, and energy applications.

Wide-bandgap devices provide up to 35% lower switching losses and nearly 20% higher power efficiency than conventional silicon components in high-voltage applications, reducing cooling requirements and improving system reliability. China leads large-scale manufacturing deployment, while the United States and Japan remain focused on advanced process innovation and premium power device development. Over the next two to three years, SiC integration is expected to exceed 30% across newly launched high-power electric mobility platforms, supported by automation upgrades and expanding industrial digitalization.

A practical example is the deployment of SiC-based traction inverters in electric vehicle manufacturing, where improved thermal performance enables smaller system footprints and higher operational efficiency. Companies are expanding wafer production, forming long-term supply partnerships, and investing in advanced packaging capabilities to strengthen competitive positioning. Organizations that integrate manufacturing resilience with next-generation power technologies will secure stronger operational flexibility and long-term strategic advantage.

Electrification across transportation, renewable energy, and industrial automation is driving sustained demand for advanced discrete semiconductor devices. More than 42% of newly introduced electric vehicle platforms now integrate high-performance power semiconductors, while industrial automation investments have increased by approximately 18% across major manufacturing economies. Silicon carbide deployment reduces energy losses by nearly 30% in demanding power applications, supporting efficiency targets and equipment reliability. China's expansion of domestic semiconductor manufacturing and industrial modernization policies continues to strengthen production capacity. In response, manufacturers are expanding SiC wafer facilities, accelerating product innovation, and establishing long-term partnerships with automotive and industrial equipment suppliers. The strategic advantage increasingly belongs to companies combining power efficiency, localized manufacturing, and diversified supply capabilities.

Production economics remain constrained by high fabrication costs, substrate availability, and dependence on specialized manufacturing ecosystems. Silicon carbide wafer production costs remain approximately 25% higher than conventional silicon processing, while lead times for selected high-performance devices have improved but still exceed pre-2020 levels by nearly 15% in several supply categories. Concentrated material sourcing and advanced packaging dependencies continue to affect procurement flexibility, particularly for manufacturers outside established semiconductor hubs. Companies are responding through supplier diversification, localized assembly operations, and multi-year procurement agreements that improve operational continuity. Organizations achieving balanced sourcing strategies are better positioned to stabilize production schedules, protect margins, and maintain customer commitments during periods of component market volatility.

Next-generation power electronics create significant opportunities across electric mobility, smart grids, industrial robotics, and AI infrastructure. Wide-bandgap semiconductor adoption is expected to surpass 35% in newly commissioned high-power industrial systems, while intelligent energy management platforms improve power conversion efficiency by approximately 18%. India's semiconductor manufacturing initiatives and Japan's advanced materials ecosystem are expanding opportunities for technology partnerships and localized production. Companies are increasing investment in advanced packaging, automated testing, and collaborative research programs to accelerate commercialization of high-performance devices. An emerging opportunity lies in integrating intelligent power management with edge computing, enabling lower operating costs while supporting increasingly complex electrified industrial environments.

Expanding production of advanced discrete semiconductors requires highly specialized fabrication technologies, skilled engineering talent, and consistent manufacturing quality across multiple facilities. Advanced packaging processes can increase production complexity by nearly 28%, while qualification cycles for automotive-grade components frequently extend beyond 12 months. The rapid evolution of AI servers, electric vehicles, and industrial control systems places additional pressure on manufacturing precision and workforce development, particularly in the United States and Europe. Companies must invest in factory automation, workforce training, digital process control, and collaborative technology ecosystems to sustain product quality and deployment consistency. Long-term competitiveness depends on scaling manufacturing excellence alongside continuous innovation rather than capacity expansion alone.

Advanced Packaging Accelerates Adoption: Automotive and industrial manufacturers are rapidly shifting toward advanced packaging to improve thermal performance and power density. More than 28% of new high-power device programs now use enhanced packaging architectures, while assembly cycle efficiency has improved by nearly 16%. Export-control adjustments and reliability requirements are encouraging manufacturers in Japan and the United States to localize packaging capabilities through automation, strategic outsourcing, and equipment modernization, reducing production bottlenecks and improving qualification speed.

AI Infrastructure Reshapes Device Mix: AI servers and hyperscale computing facilities are increasing demand for high-efficiency power semiconductors capable of handling higher switching frequencies. Nearly 32% of newly deployed AI power systems now integrate wide-bandgap devices, reducing conversion losses by approximately 20%. Enterprise operators are redesigning power distribution architectures, while semiconductor manufacturers expand partnerships with data center equipment suppliers to optimize performance, thermal management, and long-term operational reliability.

Localized Manufacturing Expands Capacity: Semiconductor companies are restructuring manufacturing footprints as supply-chain resilience becomes a procurement priority. More than 27% of announced production investments now support domestic fabrication or assembly, while inventory planning accuracy has improved by around 14% through digital supply-chain platforms. India and the United States are attracting new production initiatives, with companies balancing regional sourcing strategies instead of relying on single-country manufacturing concentration, strengthening operational continuity.

Digital Production Improves Yield: Smart manufacturing technologies are transforming semiconductor fabrication through AI-driven inspection, predictive maintenance, and digital process control. Automated defect detection improves manufacturing yield by nearly 18%, while equipment downtime declines by approximately 15%. Rising labor costs and increasingly complex device architectures are accelerating factory digitization, prompting manufacturers to expand automation investments and collaborative engineering programs that improve consistency without significantly increasing production footprints.

MOSFETs remain the leading segment due to their high switching efficiency, broad application range, and cost-effective integration across automotive, industrial, and consumer electronics systems. They account for approximately 36% of total discrete semiconductor demand because of mature manufacturing ecosystems and compatibility with modern power management architectures. Diodes continue serving essential rectification and protection functions, while transistors maintain strong relevance in amplification and switching applications. Thyristors remain preferred for heavy industrial power control where durability and high-current handling outweigh switching speed.

IGBTs represent the fastest-growing type as electric mobility and renewable energy installations increase demand for high-voltage power conversion. Adoption in traction inverters and industrial drives has expanded by nearly 24%, supported by improved thermal performance and system efficiency. Manufacturers are increasing investment in advanced IGBT modules, silicon carbide integration, and collaborative product development while optimizing production capacity to address growing electrification requirements. Investment priorities increasingly favor higher-value power semiconductor portfolios over conventional commodity components.

Power Management remains the leading application because virtually every electronic system requires efficient voltage regulation, energy conversion, and power protection. This segment represents approximately 39% of deployment volume as electric vehicles, industrial equipment, and AI computing platforms demand increasingly efficient power architectures. Consumer Electronics continues providing stable shipment volumes through smartphones, appliances, and computing devices, while Signal Processing supports communication equipment requiring reliable high-speed switching and protection capabilities.

Automotive Electronics is the fastest-growing application, supported by rapid electrification and advanced driver assistance technologies. Deployment of discrete power devices within new electric vehicle platforms has increased by nearly 26%, while Motor Control applications continue expanding across robotics and automated manufacturing. Companies are scaling dedicated automotive product lines, strengthening system-level integration, and collaborating with vehicle manufacturers to improve efficiency, reliability, and thermal performance. Demand is shifting toward application-specific semiconductor solutions that deliver higher operational efficiency under demanding electrical conditions.

Automotive remains the dominant end-user as vehicle electrification, intelligent power distribution, and advanced electronic control systems require large volumes of discrete semiconductors. Approximately 34% of total industry demand originates from automotive manufacturing, supported by expanding electric vehicle production and higher semiconductor content per vehicle. Consumer Electronics continues generating consistent purchasing activity through mobile devices and computing products, while Industrial customers maintain stable demand for automation equipment, motor drives, and energy management systems requiring long operational life.

Healthcare represents the fastest-growing end-user segment as diagnostic equipment, portable medical devices, and precision monitoring systems require highly reliable power components. Semiconductor deployment in medical electronics has expanded by approximately 19%, while Telecommunications continues upgrading network infrastructure with higher-efficiency power devices for next-generation connectivity. Companies are responding through application-specific product customization, strategic partnerships with equipment manufacturers, and differentiated pricing models that strengthen long-term customer relationships across specialized industry ecosystems.

Asia-Pacific accounted for the largest market share at 48.6% in 2025 however, North America is expected to register the fastest growth, expanding at a 6.8% CAGR between 2026 and 2033.

Advanced Power Device Manufacturing and AI Infrastructure Expansion

North America continues strengthening its position through advanced semiconductor manufacturing, AI data center deployment, and electric vehicle production. The region contributes approximately 23% of global market demand, supported by domestic fabrication expansion and increasing adoption of silicon carbide and gallium nitride technologies. Strategic investments in semiconductor manufacturing, reinforced by industrial policy initiatives, are improving supply-chain resilience and reducing dependence on overseas production. More than 30% of recently announced high-power semiconductor manufacturing projects emphasize advanced packaging and power device production. Companies continue expanding long-term partnerships with automotive manufacturers, cloud infrastructure providers, and industrial automation firms to strengthen technology commercialization and manufacturing efficiency.

United States Market Outlook: The United States leads regional innovation through advanced semiconductor design, fabrication, and packaging capabilities supported by strong investment in AI infrastructure and electric mobility. More than 35% of domestic semiconductor capital expenditure is directed toward advanced manufacturing modernization and power semiconductor capacity. Close collaboration among technology companies, automotive manufacturers, and defense suppliers strengthens commercialization of next-generation discrete semiconductors while improving long-term production resilience and operational competitiveness.

Electrification and Sustainable Industrial Modernization

Europe maintains a strong position through automotive electrification, industrial automation, and energy-efficiency regulations supporting advanced power semiconductor deployment. The region represents approximately 21% of global demand, with manufacturing concentrated around automotive and industrial equipment supply chains. More than 20% of recent industrial modernization investments include power electronics upgrades that improve operational efficiency and energy management. Companies continue integrating high-performance discrete semiconductors into renewable energy systems, factory automation platforms, and electric mobility solutions while expanding regional research partnerships that accelerate advanced device development.

Germany Market Outlook: Germany remains Europe's leading market because of its strong automotive manufacturing base, industrial automation leadership, and advanced engineering ecosystem. More than 40% of regional automotive semiconductor integration projects involve German manufacturers and suppliers developing high-efficiency power electronics. Close cooperation between semiconductor companies, industrial equipment producers, and automotive OEMs continues accelerating deployment of advanced discrete semiconductor technologies across manufacturing and mobility applications.

Manufacturing Scale and Export Leadership

Asia-Pacific dominates the global market through extensive semiconductor manufacturing capacity, vertically integrated supply chains, and large-scale electronics production. The region accounts for approximately 48.6% of global market activity, supported by strong demand from electric vehicles, consumer electronics, telecommunications, and industrial equipment. Manufacturing utilization across leading fabrication hubs consistently exceeds 80%, enabling efficient production scaling. Continuous investment in advanced wafer fabrication, packaging facilities, and automation technologies strengthens export competitiveness while supporting growing domestic semiconductor consumption across multiple industries.

China Market Outlook: China remains the region's largest market due to its extensive semiconductor manufacturing ecosystem, expanding electric vehicle industry, and strong government-backed industrial development. Approximately 38% of global discrete semiconductor manufacturing capacity is concentrated within the country. Domestic manufacturers continue investing in localized production, advanced packaging, and power semiconductor innovation while strengthening partnerships across automotive, renewable energy, and industrial automation sectors to improve supply security and technology competitiveness.

Industrial Automation Supports Market Expansion

South America is steadily increasing discrete semiconductor deployment through industrial modernization, renewable energy projects, and expanding automotive manufacturing. The region contributes approximately 4% of global demand, with growth supported by factory automation and power infrastructure upgrades. More than 18% of recent industrial equipment modernization projects incorporate higher-efficiency power semiconductor solutions to improve productivity and energy utilization. Although local fabrication remains limited, manufacturers increasingly establish regional distribution partnerships and technical support operations to improve product availability and customer responsiveness.

Brazil Market Outlook: Brazil leads the regional market through its automotive production, industrial manufacturing, and expanding renewable energy sector. Semiconductor deployment continues increasing across motor control systems, industrial automation, and power conversion equipment. More than one-quarter of regional industrial modernization initiatives are concentrated within Brazil, encouraging global semiconductor suppliers to strengthen distribution networks, engineering support, and localized customer engagement strategies.

Infrastructure Digitalization and Industrial Investment

The Middle East & Africa market is advancing through smart infrastructure programs, energy diversification, and industrial digitalization initiatives requiring efficient power semiconductor technologies. The region accounts for approximately 3.4% of global market demand, with increasing deployment across utilities, transportation, telecommunications, and industrial facilities. More than 16% of newly commissioned smart infrastructure projects integrate advanced power electronics for improved energy management. Companies are expanding regional partnerships, technical service capabilities, and localized engineering support to strengthen market access while addressing growing infrastructure modernization requirements.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as the region's leading market through industrial diversification, smart city development, and significant investment in digital infrastructure. Large-scale energy transition projects continue increasing demand for high-efficiency discrete semiconductor devices across power conversion and automation systems. Government-supported industrial development programs and expanding technology partnerships are strengthening long-term deployment opportunities while encouraging international semiconductor companies to establish stronger regional operational footprints.

The competitive landscape is led by Infineon Technologies, STMicroelectronics, ON Semiconductor, Vishay Intertechnology, and Rohm Semiconductor, competing directly with regional manufacturers in China and Taiwan focused on cost-efficient production and faster delivery. Global technology leaders emphasize silicon carbide, gallium nitride, and advanced packaging, while regional suppliers compete through manufacturing scale and localized customer support. The top five companies collectively control approximately 46% of the market, creating intense rivalry around technology leadership and supply reliability. Power device efficiency improvements exceeding 20% and manufacturing automation gains of nearly 18% increasingly outweigh pure pricing strategies. Companies are expanding wafer capacity, securing long-term automotive supply agreements, integrating packaging operations, and forming strategic partnerships with electric vehicle and industrial equipment manufacturers. Competition is shifting toward control of advanced materials, packaging capability, and resilient supply chains rather than volume alone. High qualification requirements, capital-intensive fabrication, and specialized engineering expertise remain major entry barriers. Winning requires differentiated power technologies, manufacturing resilience, rapid product qualification, and deep customer integration.

Infineon Technologies AG

STMicroelectronics N.V.

ON Semiconductor Corporation

Vishay Intertechnology, Inc.

Rohm Co., Ltd.

Nexperia B.V.

Toshiba Electronic Devices & Storage Corporation

Renesas Electronics Corporation

Diodes Incorporated

Littelfuse, Inc.

Fuji Electric Co., Ltd.

Mitsubishi Electric Corporation

Wide-bandgap semiconductor technologies are redefining discrete semiconductor performance across electric mobility, industrial automation, and AI power infrastructure. Silicon carbide (SiC) and gallium nitride (GaN) devices reduce switching losses by up to 35% while improving power conversion efficiency by nearly 20% compared with conventional silicon devices. Around 30% of newly designed high-power electronic platforms now integrate wide-bandgap components, enabling smaller cooling systems, higher operating frequencies, and improved equipment reliability. Automotive manufacturers and industrial equipment suppliers gain the strongest competitive advantage through lower energy consumption and higher system durability.

Manufacturing technologies are advancing through AI-assisted inspection, digital twins, and advanced packaging integration. Automated optical inspection improves production yield by approximately 18%, while predictive process control reduces manufacturing downtime by nearly 15%. Compared with legacy inspection workflows, AI-enabled quality systems accelerate defect detection and shorten qualification cycles, allowing manufacturers to introduce new power devices more efficiently. Companies investing in intelligent fabrication achieve stronger operational consistency and improved customer responsiveness.

Between 2026 and 2028, heterogeneous integration, advanced wafer bonding, and intelligent power modules will become strategic differentiators. Adoption of advanced packaging is expected to exceed 40% across premium power semiconductor platforms as manufacturers pursue higher power density and improved thermal performance. Early adopters strengthening material innovation, automated production, and ecosystem partnerships will secure faster commercialization, stronger supply resilience, and sustainable competitive positioning in high-value semiconductor applications.

December 2024: onsemi announced the acquisition of Qorvo's Silicon Carbide JFET technology business, including United Silicon Carbide, for USD 115 million, expanding its EliteSiC portfolio and targeting AI data center power applications. The deal expands its addressable opportunity by approximately USD 1.3 billion within five years, strengthening high-efficiency power semiconductor leadership. Source: investor.onsemi.com

February 2025: Infineon Technologies released its first customer products manufactured on 200 mm silicon carbide wafers while preparing high-volume production in Malaysia. The transition from 150 mm to 200 mm wafers significantly improves manufacturing efficiency and strengthens supply capacity for electric vehicles, renewable energy, and industrial applications. Source: infineon.com

November 2025: Infineon Technologies partnered with SolarEdge to jointly develop modular solid-state transformer technology for AI data centers. The solution delivers more than 99% efficiency while supporting 2–5 MW building blocks, enabling higher power density and lower operating costs for next-generation digital infrastructure. Source: infineon.com

June 2026: onsemi signed a definitive agreement to acquire Synaptics in an all-stock transaction valued at approximately USD 7 billion, combining power, sensing, connectivity, and AI computing technologies. The acquisition strengthens its position in Physical AI and broadens intelligent semiconductor solutions across automotive and industrial markets. Source: reuters.com

This report provides comprehensive analysis of the global discrete semiconductor market across the complete value chain, covering technology evolution, competitive positioning, manufacturing trends, and strategic demand drivers between 2026 and 2033. The assessment evaluates five major product types, five application segments, and five end-user industries across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. More than 45% of the analysis emphasizes power semiconductor deployment, manufacturing localization, and next-generation wide-bandgap technologies reflecting current industry priorities.

The report further examines enterprise investment strategies, supply-chain restructuring, technology adoption patterns, and competitive benchmarking across leading manufacturers. It evaluates production capacity expansion, advanced packaging, silicon carbide and gallium nitride innovation, and regional manufacturing shifts while identifying operational opportunities in electric mobility, AI infrastructure, industrial automation, renewable energy, and smart electronics. The insights support market entry planning, portfolio optimization, expansion strategy, partnership evaluation, risk assessment, and long-term competitive positioning for technology developers, manufacturers, investors, and industrial stakeholders.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 32650 Million |

Market Revenue in 2033 | USD 52433.18 Million |

CAGR (2026 - 2033) | 6.1% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Infineon Technologies AG, STMicroelectronics N.V., ON Semiconductor Corporation, Vishay Intertechnology, Inc., Rohm Co., Ltd., Nexperia B.V., Toshiba Electronic Devices & Storage Corporation, Renesas Electronics Corporation, Diodes Incorporated, Littelfuse, Inc., Fuji Electric Co., Ltd., Mitsubishi Electric Corporation |

Customization & Pricing | Available on Request (10% Customization is Free) |