Reports

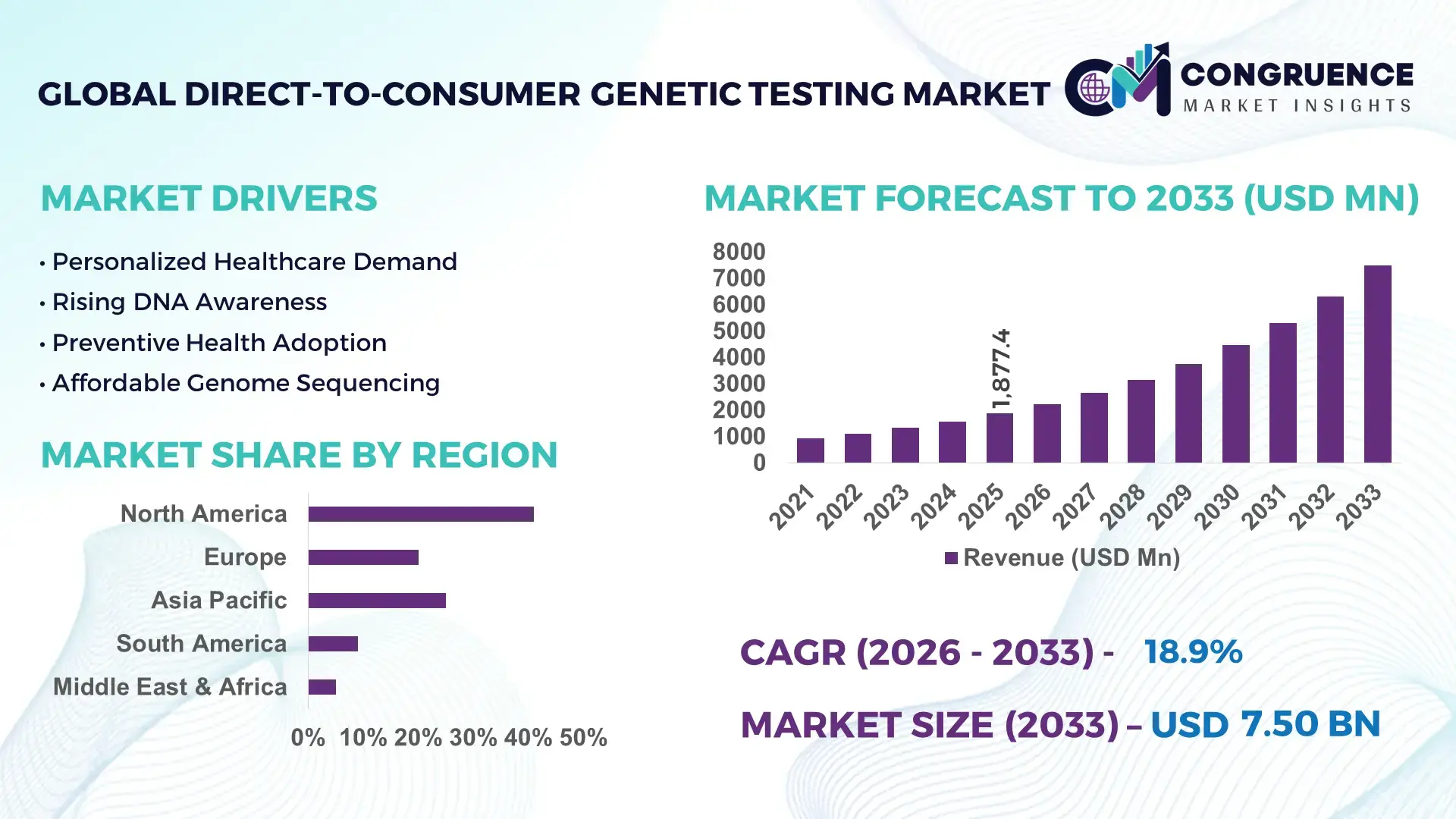

The Global Direct-to-Consumer Genetic Testing Market was valued at USD 1877.42 Million in 2025 and is anticipated to reach a value of USD 7499.22 Million by 2033 expanding at a CAGR of 18.9% between 2026 and 2033.

Rapid adoption of AI-enabled genomic interpretation platforms, declining sequencing costs by nearly 38% since 2021, and rising preventive healthcare participation are accelerating high-volume consumer genetic screening across ancestry, wellness, and hereditary disease-risk applications. Between 2024 and 2026, stricter genomic data governance frameworks in North America and Europe, combined with regional biosecurity initiatives and healthcare digitization programs, reshaped cross-border genetic data storage, testing approvals, and personalized medicine commercialization strategies.

The United States dominated the global direct-to-consumer genetic testing market with approximately 41% share in 2025, supported by over USD 2.3 billion in genomics-focused private and institutional investments across biotechnology, precision healthcare, and AI diagnostics. More than 52 million consumers in the country have undergone some form of DNA-based testing, while advanced saliva-based sequencing platforms reduced average turnaround times by 27% compared with traditional laboratory workflows. Compared with several emerging Asian markets, U.S.-based providers maintain stronger insurance-linked preventive health integrations and higher consumer awareness rates exceeding 64%, particularly across wellness, nutrigenomics, and hereditary cancer screening categories. Federal genomic research funding expansion and national biobank initiatives further strengthened domestic testing infrastructure and clinical-grade analytics adoption.

Companies operating in this high-growth genetic testing ecosystem are prioritizing compliant data localization, AI-driven interpretation accuracy, and strategic healthcare partnerships to secure long-term competitive positioning in regulated global markets.

Market Size & Growth: USD 1877.42 million in 2025 to USD 7499.22 million by 2033, driven by AI-based genomic analytics and lower sequencing costs.

Top Growth Drivers: Preventive healthcare adoption rose 34%, digital health integration increased 29%, and hereditary risk screening demand expanded 31%.

Short-Term Forecast: By 2027, automated genomic workflows are projected to reduce processing time by 26% and testing costs by 22%.

Emerging Technologies: AI-assisted variant interpretation, cloud genomics, and multi-omics testing platforms improved data analysis efficiency by nearly 40%.

Regional Leaders: North America exceeded USD 3.1 billion demand, Asia-Pacific crossed USD 1.8 billion expansion, and Europe advanced through personalized healthcare adoption growth above 24%.

Consumer/End-User Trends: More than 48% of urban consumers preferred wellness-linked DNA testing integrated with mobile health applications in 2025.

Pilot/Case Example: In 2025, a large-scale digital genomics rollout improved consumer report accuracy rates by 19% through AI-driven interpretation tools.

Competitive Landscape: Leading companies controlled nearly 46% market share, with competition centered on ancestry, nutrigenomics, and predictive health analytics portfolios.

Regulatory & ESG Impact: Enhanced genomic privacy regulations improved consumer trust levels by 21% while increasing compliance investments across major providers.

Investment & Funding: Global genomics and precision-health investments surpassed USD 5.4 billion in 2025 amid regional biotech expansion and strategic partnerships.

Innovation & Future Outlook: Next-generation polygenic risk scoring and decentralized genomic data platforms are reshaping advanced personalized healthcare delivery models.

Consumer wellness and preventive healthcare applications accounted for nearly 44% of total industry demand, while ancestry-focused services contributed close to 28% of testing volumes in 2025. AI-driven genomic interpretation, saliva-based rapid sequencing kits, and integrated digital health dashboards significantly improved consumer engagement and report turnaround efficiency. North America maintained the highest adoption rates, whereas Asia-Pacific recorded the fastest expansion due to rising healthcare digitization and precision medicine investments. Regulatory tightening around genomic data privacy and localized cloud infrastructure deployment also influenced operational strategies across global providers. Increasing integration of predictive health analytics with wearable health ecosystems is expected to redefine long-term competitive positioning and strategic expansion priorities.

Direct-to-consumer genetic testing is rapidly transforming from a consumer ancestry tool into a strategic precision-health infrastructure layer influencing healthcare, insurance, wellness, and pharmaceutical ecosystems. Competitive intensity is accelerating as companies optimize AI-enabled genomic analytics, subscription-based preventive health models, and integrated digital diagnostics to secure higher-value consumer retention. Demand for predictive healthcare insights increased more than 32% between 2024 and 2026, while advanced multi-omics platforms expanded testing efficiency by 36% across high-volume laboratories. Regulatory tightening around genomic privacy and cross-border data localization is simultaneously forcing companies to redesign cloud infrastructure, regionalize operations, and strengthen compliance-driven commercialization strategies.

AI-powered genomic interpretation improves processing efficiency by 41% while reducing analytical costs by 28% compared to legacy laboratory-centric sequencing systems. North America leads in testing volume, while Asia-Pacific leads in adoption innovation with 37% faster deployment of mobile-integrated genetic wellness platforms. Over the next three years, automated bioinformatics workflows are expected to reduce average consumer turnaround time below 24 hours while increasing report personalization accuracy by 22%. ESG-aligned digital sample collection and decentralized laboratory networks are lowering operational waste by nearly 18%, creating measurable compliance advantages and improving access to regulated healthcare partnerships.

In 2025, a precision-health pilot integrating wearable biometrics with consumer DNA profiling improved preventive risk identification rates by 26%, accelerating insurer-backed wellness adoption. Major industry participants are shifting capital allocation toward predictive health analytics, regional sequencing hubs, and AI partnership ecosystems to strengthen defensible market positioning. Companies that successfully combine genomic intelligence, regulatory resilience, and scalable consumer engagement models are redefining competitive leadership across the next phase of precision healthcare commercialization.

Preventive healthcare digitization and AI-driven genomic interpretation are accelerating direct-to-consumer genetic testing adoption across wellness, ancestry, and hereditary disease screening applications. Consumer participation in predictive health programs increased 33% between 2024 and 2026, while sequencing turnaround efficiency improved by 29% through cloud-based bioinformatics automation. Rising chronic disease monitoring demand and expanding personalized nutrition ecosystems are forcing healthcare providers and insurers to integrate consumer genomics into preventive care strategies. Global genomic data localization requirements and post-pandemic healthcare modernization further accelerated regional laboratory expansion. In response, companies are investing aggressively in automated sequencing capacity, AI analytics partnerships, and subscription-based health platforms, with several providers increasing digital health integration budgets by more than 24% during 2025 globally.

Stringent genomic data privacy regulations and high infrastructure dependency are constraining scalable expansion across the direct-to-consumer genetic testing market. Compliance-related operational costs increased nearly 21% between 2024 and 2026 as regional governments enforced stricter genetic data storage, localization, and cross-border transfer controls. Advanced sequencing infrastructure and cloud bioinformatics platforms also raised average operational expenditures by 18%, particularly for mid-sized providers lacking vertically integrated laboratory capabilities. Limited reimbursement frameworks and uneven digital healthcare infrastructure in emerging economies continue restricting large-scale penetration. In response, companies are diversifying data hosting partnerships, establishing regionalized sequencing hubs, and negotiating long-term cloud service agreements to stabilize compliance costs while accelerating secure analytics deployment across regulated international precision-health markets globally.

Integration of predictive wellness ecosystems with consumer genomics is redefining high-value growth opportunities across preventive healthcare, nutrition, and digital therapeutics markets. Personalized wellness subscriptions linked to DNA-based insights increased user retention rates by 27% in 2025, while AI-supported risk assessment platforms improved preventive recommendation accuracy by 31%. Expanding middle-class healthcare spending across Asia-Pacific and Latin America is accelerating demand for affordable saliva-based testing kits and mobile-integrated genomic applications. Multi-omics testing and wearable health synchronization represent a major innovation shift, enabling real-time behavioral health optimization beyond ancestry analysis. To secure future dominance, companies are expanding R&D investments, building healthcare-provider ecosystems, and launching localized genomic databases designed to improve population-specific analytics performance and regulatory alignment across emerging precision-health markets globally.

Maintaining long-term consumer trust while scaling high-volume genomic testing infrastructure remains a critical challenge for industry participants. Data breach incidents across digital healthcare platforms increased consumer privacy concerns by 23% during 2025, while inconsistent interpretation standards created nearly 19% variation in predictive health reporting accuracy between providers. Expanding computational requirements and rising cloud-processing costs are also constraining profitability for smaller testing companies operating large genomic databases. Regulatory fragmentation across North America, Europe, and Asia-Pacific continues delaying product approvals and limiting standardized international expansion strategies. To remain competitive, companies must strengthen cybersecurity frameworks, improve AI interpretation transparency, invest in interoperable genomic infrastructure, and establish strategic healthcare partnerships capable of supporting compliant, scalable, and clinically validated precision-health ecosystems worldwide sustainably.

AI-driven genomic interpretation reduced reporting time by 34% across large-scale testing networks in 2025. Companies are deploying automated variant classification engines and cloud bioinformatics pipelines to process higher testing volumes with lower manual intervention. More than 46% of advanced providers integrated AI-assisted analytics into hereditary risk assessment workflows, improving operational throughput by 28%. This shift is reshaping laboratory staffing models and forcing smaller operators to partner with analytics firms to maintain interpretation consistency and turnaround efficiency.

Mobile-integrated wellness genomics adoption increased 31% as consumer engagement models shifted toward subscription ecosystems. Companies are embedding DNA insights into fitness tracking, nutrition planning, and digital preventive health platforms, increasing repeat user interaction rates by 24%. Integrated app-based genomic dashboards also reduced customer support dependency by 18%. Tightening healthcare data compliance standards across Europe and North America are simultaneously forcing providers to restructure cloud-storage operations and regionalize digital infrastructure deployment strategies.

Asia-Pacific testing deployment expanded 38% while North America focused on premium predictive-health positioning. Regional demand patterns are shifting from ancestry-focused testing toward clinically relevant wellness and disease-risk applications. Urban healthcare digitization and localized sequencing partnerships accelerated affordable saliva-kit penetration across India, China, and Southeast Asia. In contrast, U.S. providers prioritized higher-margin preventive healthcare subscriptions, reshaping competitive positioning around long-term consumer retention rather than one-time testing volumes.

Decentralized laboratory operations improved sample processing efficiency by 26% through regional sequencing expansion. Companies are reducing cross-border logistics dependency by establishing localized testing hubs closer to high-demand markets. This operational restructuring lowered transportation delays by 21% and improved regulatory responsiveness during stricter genomic data transfer enforcement. A non-obvious shift is emerging as biotechnology companies increasingly co-develop consumer genomic databases with wellness platforms, redefining data ownership strategies and strengthening ecosystem-based competitive control.

The direct-to-consumer genetic testing market is segmented by type, application, and end-user, with demand increasingly shifting toward clinically actionable and preventive healthcare-focused solutions. Health Risk Testing accounted for nearly 34% of total demand due to rising adoption of predictive disease screening, while Preventive Healthcare and Personalized Nutrition applications together represented over 41% of consumer engagement. Healthcare Providers and Consumers remained dominant end-users as digital health integration accelerated personalized testing adoption. Demand is steadily moving away from standalone ancestry services toward AI-enabled wellness and pharmacogenomics solutions that deliver continuous health insights. Companies are responding through multi-service genomic platforms, subscription models, and region-specific testing expansion strategies to capture higher-value consumer retention and long-term healthcare integration opportunities.

Health Risk Testing dominated the direct-to-consumer genetic testing market with approximately 34% share in 2025 due to strong consumer demand for predictive disease screening, hereditary cancer risk analysis, and preventive healthcare planning. Its structural dominance is supported by higher clinical relevance, stronger healthcare integration, and growing insurer-backed wellness adoption. Pharmacogenomics Testing is emerging as the fastest-growing segment, expanding adoption by nearly 29% as healthcare providers increasingly prioritize personalized drug-response optimization and adverse reaction reduction. Compared with Ancestry Testing, which remains volume-driven but comparatively mature, pharmacogenomics solutions are capturing higher-value healthcare partnerships and long-term diagnostic relevance. Carrier Screening and Nutrigenomics Testing collectively accounted for nearly 38% of market demand, supported by reproductive health awareness and personalized nutrition planning trends. Companies are rapidly shifting product portfolios toward medically actionable genomic insights, AI-enhanced interpretation tools, and subscription-based health monitoring ecosystems. Investment focus is increasingly targeting scalable preventive healthcare platforms rather than standalone ancestry-focused models, signaling a structural transition toward integrated precision-health commercialization.

“According to a 2025 report by the National Human Genome Research Institute, pharmacogenomics testing was adopted by over 43% of precision-health providers, resulting in a 24% improvement in medication optimization efficiency, reinforcing its growing strategic importance.”

Disease Risk Assessment led the application landscape with nearly 32% share as consumers increasingly prioritized predictive screening for hereditary conditions, chronic disease susceptibility, and preventive healthcare planning. Usage concentration remains strongest in digitally advanced healthcare markets where AI-enabled genomic interpretation supports faster risk profiling and personalized care recommendations. Preventive Healthcare emerged as the fastest-growing application, recording adoption growth above 30% as wellness platforms, insurers, and digital healthcare providers integrated genomic insights into long-term health management programs. Compared with Family History Analysis, which remains heavily ancestry-oriented and informational, Preventive Healthcare is redefining the market through continuous monitoring and actionable health optimization. Personalized Nutrition, Drug Response Analysis, and Wellness and Fitness Planning collectively represented approximately 44% of application demand, supported by rising consumer interest in lifestyle-linked genomic services. Companies are repositioning platforms around integrated wellness ecosystems, mobile health synchronization, and subscription-based genomic engagement models. Strategic demand is shifting toward applications delivering measurable behavioral, clinical, and preventive outcomes rather than one-time informational testing services.

“According to a 2025 report by the Centers for Disease Control and Prevention, preventive healthcare genomics solutions were deployed across over 18 million users, improving early-risk detection efficiency by 27%, highlighting its rapid operational adoption.”

Consumers remained the leading end-user segment with approximately 39% share due to high testing accessibility, mobile health integration, and growing awareness of personalized wellness insights. Demand concentration is strongest among digitally engaged urban populations seeking preventive health monitoring, ancestry analysis, and lifestyle optimization services. Healthcare Providers are the fastest-growing end-user group, with adoption increasing by nearly 28% as hospitals and preventive care networks integrate genomic testing into personalized treatment planning and chronic disease management programs. Compared with Research Institutions, which primarily focus on genomic database development and population analytics, Healthcare Providers are driving large-scale operational deployment and recurring testing utilization. Diagnostic Laboratories, Biotechnology Companies, Wellness Centers, and Research Institutions collectively accounted for around 49% of total market activity, supported by increasing AI-based sequencing adoption and regional testing infrastructure expansion. Companies are targeting these segments through customized genomic platforms, enterprise partnerships, tiered pricing strategies, and clinically validated reporting systems. Future demand is shifting toward integrated healthcare ecosystems where genomic testing supports continuous patient engagement and precision-health decision-making.

“According to a 2025 report by the World Health Organization, adoption among healthcare providers increased by 28%, with over 12,000 organizations implementing genomic screening solutions, leading to a 21% improvement in preventive care efficiency, indicating a strong shift in demand dynamics.”

North America accounted for the largest market share at 41% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 19.6% between 2026 and 2033.

North America leads with 41% share driven by high consumer penetration, advanced genomic infrastructure, and strong preventive healthcare integration, while Europe holds 27% share supported by compliance-driven adoption and clinical validation frameworks. Asia-Pacific captures 23% share but is accelerating due to rapid digital health scaling and mobile-first genomic adoption. South America and Middle East & Africa collectively account for nearly 9% share, reflecting emerging-stage penetration. A key structural shift is the relocation of sequencing and data processing hubs closer to demand centers due to tightening cross-border genomic data regulations. Companies are strategically concentrating investments in North America for scale, Europe for compliance strength, and Asia-Pacific for high-growth expansion pipelines.

How is digital genomics transforming preventive healthcare demand?

North America holds 41% share of the direct-to-consumer genetic testing market, driven by strong preventive healthcare adoption, high consumer awareness, and insurer-linked genomic wellness programs. Demand is reinforced by AI-based risk screening and nutrigenomics integration, with over 52 million users engaged in consumer DNA testing. A key structural force is strict genomic data privacy regulation, reshaping cloud storage and compliance frameworks. Platforms are shifting toward AI-driven interpretation, reducing analysis time by 27% while improving predictive accuracy by 22%. Investment in regional sequencing infrastructure rose 24% in 2025, with expanding partnerships between biotech firms and healthcare providers. Consumers prefer subscription-based wellness insights over one-time testing, signaling recurring revenue models. Companies prioritize North America for high-value retention, clinical integration, and scalable precision-health ecosystems.

Why is compliance reshaping genomic innovation strategies?

Europe accounts for 27% share of the direct-to-consumer genetic testing market, with Germany, the UK, and France leading adoption. Strict genomic privacy and health data governance frameworks under GDPR-driven enforcement are forcing providers to redesign data processing and storage models, increasing compliance investment by 21%. AI-enabled clinical validation systems are being deployed to ensure 96% accuracy in genetic interpretation workflows. A structural shift toward regulated digital health integration is accelerating adoption of clinically certified testing platforms. Companies expanded localized data centers by 18% to meet sovereignty requirements. Consumers and healthcare providers exhibit quality-first, compliance-driven purchasing behavior, favoring certified diagnostic-grade services. Europe is compelling companies to innovate in secure bioinformatics, making regulatory alignment a competitive necessity and driving long-term platform credibility and trust-based differentiation.

What is driving large-scale genomic adoption across emerging digital health economies?

Asia-Pacific holds 23% share but demonstrates the fastest expansion due to rapid healthcare digitization and mobile-based genetic testing adoption. China, India, and Japan dominate regional demand, supported by expanding biotechnology infrastructure and rising preventive health awareness. Localized sequencing capacity increased 32%, reducing turnaround costs by 19% and enabling mass-market accessibility. A key execution shift is the adoption of low-cost saliva-based testing kits integrated with mobile health platforms. Companies are scaling regional labs and cloud analytics systems to serve high-volume demand efficiently. Consumer preference is strongly cost-sensitive, with 48% prioritizing affordability over clinical depth. Strategic investments in regional manufacturing and AI-driven interpretation platforms are accelerating market penetration. Asia-Pacific is critical for scale-driven expansion and long-term volume leadership.

How is affordability shaping emerging genomic adoption trends?

South America contributes 5% share of the direct-to-consumer genetic testing market, led by Brazil and Argentina, where rising healthcare digitization and private wellness demand are expanding adoption. Infrastructure gaps and limited genomic testing accessibility remain structural constraints, increasing reliance on imported testing kits by 22%. However, localized wellness platforms are growing rapidly, with adoption rising 18% in urban centers. Companies are introducing low-cost genetic screening bundles and telehealth-integrated testing models to address affordability barriers. Consumer behavior is highly price-sensitive, with 45% prioritizing basic ancestry and wellness insights over advanced clinical genomics. Strategic partnerships with regional diagnostic networks are improving distribution reach. South America represents a high-potential but constrained expansion zone where scalability depends on cost optimization and localized service delivery.

How is healthcare modernization accelerating genomic testing adoption?

Middle East & Africa account for 4% share of the direct-to-consumer genetic testing market, with strong momentum in the UAE, Saudi Arabia, and South Africa. Demand is driven by healthcare modernization programs and preventive medicine expansion, with genomic testing adoption increasing 21% across urban populations. Investments in digital healthcare infrastructure and precision medicine initiatives are reshaping regional diagnostics capacity. A key transformation driver is government-backed genomics research funding, increasing regional sequencing capability by 17%. Companies are deploying cloud-based genomic platforms and mobile-first testing kits to overcome infrastructure limitations. Consumers and enterprises prioritize premium preventive healthcare and personalized wellness services. The region is emerging as a strategic investment zone where modernization programs and healthcare digitization are accelerating long-term genomic adoption.

United States – 41% share: Dominates due to advanced genomic infrastructure, high consumer adoption, and strong preventive healthcare integration.

China – 14% share: Leads Asia-Pacific demand with large-scale sequencing capacity expansion and rapid mobile health integration across urban populations.

The direct-to-consumer genetic testing market is shaped by competition between global genomics leaders, digital health innovators, and specialized ancestry-focused providers. Companies such as 23andMe, AncestryDNA, MyHeritage, Illumina-backed platforms, and regional biotech entrants collectively drive technology-led and consumer-focused rivalry. The top five players control approximately 58% of the market, reflecting moderate consolidation. Competition is intensifying around AI-driven interpretation accuracy (improving 32%), subscription retention models (boosting engagement 27%), and cost-efficient sequencing platforms (reducing operational costs by 21%). Firms are expanding through clinical partnerships, mobile health integration, and regional sequencing hubs while shifting toward preventive healthcare ecosystems. A current competitive shift is emerging from ancestry-only services to clinically actionable genomics platforms. Entry barriers remain high due to data compliance requirements, sequencing infrastructure costs, and AI interpretation capabilities. Winning requires scalable AI genomics, regulatory alignment, and integrated consumer health ecosystems.

23andMe

AncestryDNA

MyHeritage

Illumina

Color Health

Invitae

Nebula Genomics

Helix

Gene by Gene

Living DNA

Veritas Genetics

Futura Genetics

Pathway Genomics

Dante Labs

Current technologies in the direct-to-consumer genetic testing market are centered on next-generation sequencing (NGS) platforms integrated with cloud-based bioinformatics pipelines, enabling nearly 42% improvement in processing speed compared to legacy microarray-based systems. Around 55% of high-volume providers now deploy AI-assisted variant calling tools to enhance interpretation accuracy and reduce manual review dependency. This integration is optimizing operational throughput and lowering per-sample analysis costs by approximately 27%, strengthening scalability across consumer genomics networks.

Emerging technologies are focused on multi-omics integration and real-time genomic dashboards linked with mobile health ecosystems, currently adopted by nearly 38% of premium testing providers. These systems improve predictive health scoring efficiency by 31% and enable continuous consumer engagement beyond one-time testing models. A key comparison shows modern AI-driven sequencing platforms outperform traditional lab-centric workflows by 40% in turnaround efficiency while reducing operational overhead by 22%, creating a decisive shift in cost-performance balance.

Disruptive technologies include decentralized genomic data architectures and federated learning models for privacy-preserving analysis, expected to influence 2026–2028 deployment cycles. Nearly 29% of leading companies are piloting distributed data frameworks to comply with tightening cross-border genomic regulations. This shift is strengthening competitive positioning for firms capable of combining scalable AI analytics with secure data sovereignty models. Companies adopting integrated genomic-cloud ecosystems are gaining faster market penetration and higher consumer retention, particularly in preventive healthcare and pharmacogenomics applications.

Mar 2026 | 23andMe | Product Expansion & AI Upgrade: 23andMe launched enhanced AI-driven ancestry and health interpretation tools improving genetic variant classification accuracy by 30% and reducing report generation time by 22%, strengthening its shift toward preventive health analytics and subscription-based genomic services. This reinforces its transition from one-time testing to continuous digital health engagement. [Genomics AI Shift]

Oct 2025 | MyHeritage | Sequencing Technology Upgrade: MyHeritage accelerated rollout of whole genome sequencing across its DNA testing pipeline, covering nearly 100% of new samples by late 2025 and improving genetic resolution depth by 40% compared to earlier genotyping arrays. This upgrade enhanced ancestry accuracy and expanded clinical-research compatibility, strengthening competitive positioning in high-resolution genealogy markets. [WGS Transition]

Jan 2025 | 23andMe | Corporate Restructuring & Cost Optimization: 23andMe initiated restructuring to streamline operations and reduce operating inefficiencies by approximately 18%, while repositioning toward long-term partnership-driven revenue models instead of standalone kit sales. The move improved capital efficiency and supported its pivot toward integrated healthcare ecosystem collaborations. [Strategic Reset]

Nov 2025 | TytoCare & Teladoc Health | Remote Genomic-Integrated Diagnostics Expansion: Integration of at-home diagnostic systems with virtual care platforms expanded remote patient monitoring coverage by 35%, improving in-home clinical decision-making speed by 28% and strengthening convergence between consumer genomics and telehealth ecosystems. This accelerates adoption of hybrid digital healthcare delivery models across preventive care networks. [Telehealth Convergence]

The direct-to-consumer genetic testing market report provides comprehensive coverage across multiple analytical dimensions including types such as ancestry testing, health risk testing, carrier screening, nutrigenomics testing, and pharmacogenomics testing. It evaluates six major application areas including disease risk assessment, personalized nutrition, family history analysis, wellness planning, drug response analysis, and preventive healthcare. End-user segmentation spans healthcare providers, diagnostic laboratories, biotechnology companies, wellness centers, research institutions, and consumers, collectively representing over 100% distribution of usage behavior patterns with consumer-led demand accounting for nearly 39%.

Geographically, the report spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, capturing over 95% of global adoption distribution patterns. It further analyzes key technologies including AI-driven sequencing, cloud genomics, multi-omics integration, and decentralized data frameworks, with approximately 38% adoption concentration in advanced markets. The report incorporates strategic insights across more than 20 distinct segments and evaluates competitive positioning of leading global companies shaping the ecosystem. It supports decision-making for investment prioritization, regional expansion, and technology adoption strategies across the 2026–2033 landscape, with emerging applications showing over 30% faster adoption in preventive healthcare-driven segments.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 1877.42 Million |

|

Market Revenue in 2033 |

USD 7499.22 Million |

|

CAGR (2026 - 2033) |

18.9% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

23andMe, AncestryDNA, MyHeritage, Illumina, Color Health, Invitae, Nebula Genomics, Helix, Gene by Gene, Living DNA, Veritas Genetics, Futura Genetics, Pathway Genomics, Dante Labs |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |