Reports

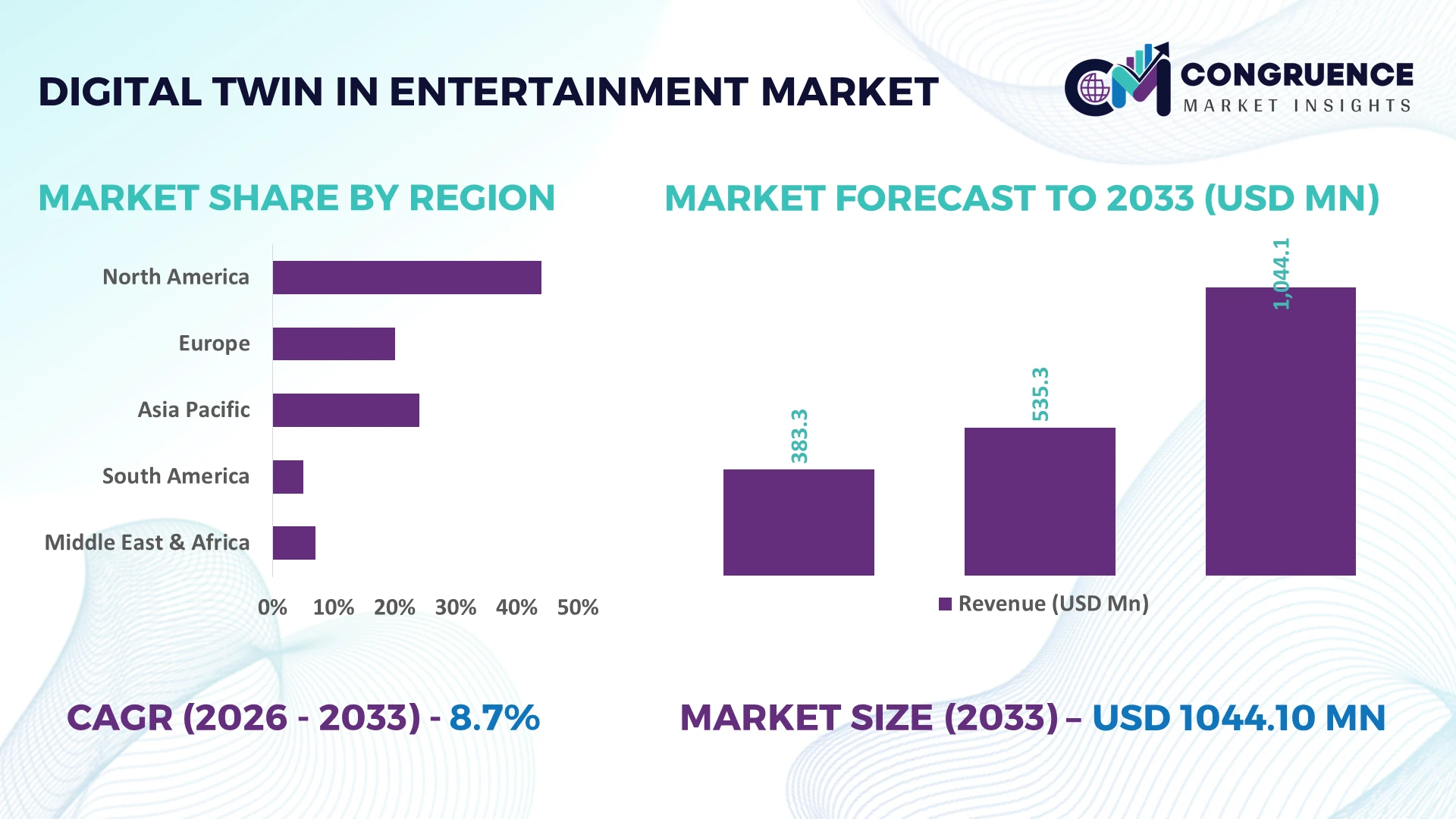

The Global Digital Twin in Entertainment Market was valued at USD 535.28 Million in 2025 and is anticipated to reach a value of USD 1044.1 Million by 2033 expanding at a CAGR of 8.71% between 2026 and 2033. Growth is driven by the rapid integration of AI-powered digital twins for virtual production, immersive live events, gaming environments, and real-time asset optimization across global entertainment ecosystems.

The United States leads the market with approximately 37% of global deployment activity, supported by extensive investment in virtual production studios, cloud rendering infrastructure, and media technology platforms, while South Korea has accelerated adoption across gaming and immersive entertainment with deployment growth exceeding 22%. Continued investment following AI governance initiatives introduced in 2026 has strengthened enterprise implementation, while advanced production workflows reduce digital asset creation time by nearly 30% compared with conventional pipelines.

Organizations prioritizing scalable digital twin platforms and AI-enabled production ecosystems are positioned to secure stronger operational efficiency, faster content delivery, and sustainable competitive differentiation.

Market Size & Growth: USD 535.28 Million (2025) to USD 1044.1 Million (2033) at 8.71% CAGR, driven by AI-enabled virtual production and real-time content optimization.

Top Growth Drivers: AI-assisted production (+31%), immersive gaming adoption (+27%), cloud rendering expansion (+24%) accelerate market momentum.

Short-Term Forecast: By 2028, production costs decline 18% while digital asset creation efficiency improves 26% through automated workflows.

Emerging Technologies: AI, spatial computing, and real-time rendering improve production accuracy by over 30% across advanced entertainment ecosystems.

Regional Leaders: North America approaches USD 390 Million, Asia-Pacific exceeds USD 290 Million, Europe reaches USD 230 Million, supported by regional studio expansion and localization.

Consumer & End-User Trends: More than 48% of entertainment companies prioritize digital twin deployment for immersive experiences and operational optimization.

Pilot Case Example: In 2026, a virtual production deployment reduced rendering time by 35% while improving collaborative content development efficiency.

Competitive Landscape: Leading vendors collectively control nearly 42% of market activity alongside major cloud, gaming, visualization, and media technology providers.

Regulatory & ESG Impact: AI governance frameworks and energy-efficient computing reduce infrastructure power consumption by approximately 16% across digital production environments.

Investment & Funding: Global investment exceeds USD 2.1 Billion, fueled by strategic partnerships, regional expansion, and enterprise technology modernization.

Innovation & Future Outlook: AI-generated environments, autonomous content simulation, and interoperable digital ecosystems strengthen next-generation entertainment production strategies.

Demand continues to strengthen across virtual production, esports, live event management, digital broadcasting, and interactive gaming as entertainment companies prioritize intelligent simulation and operational visibility. AI-enhanced content pipelines and real-time physics modeling improve production efficiency by nearly 25%, while broader cloud infrastructure localization and evolving digital governance frameworks support secure deployment, setting the foundation for the strategic market analysis that follows.

Digital twin technology has become a strategic differentiator for entertainment companies seeking faster content production, lower operational costs, and immersive audience experiences. Film studios, gaming developers, broadcasters, and live event operators increasingly rely on synchronized virtual environments to optimize creative workflows and asset management. Infrastructure modernization through cloud-native production platforms and AI-enabled simulation is replacing fragmented production pipelines, while stricter digital governance and content security requirements are accelerating enterprise-grade deployment across global entertainment ecosystems.

Compared with conventional production planning, digital twin platforms reduce digital asset rework by approximately 28% and shorten production cycle times by nearly 32% through real-time collaboration and predictive simulation. The United States continues to lead large-scale studio implementation, whereas Japan emphasizes precision digital content engineering and virtual character ecosystems with higher deployment density across animation and gaming. During the next two to three years, enterprise adoption across large entertainment organizations is expected to exceed 50%, supported by wider GPU infrastructure availability and integrated AI production tools.

A practical example is the deployment of digital twins for live concert planning, where organizers simulate crowd movement, stage configurations, and lighting before physical installation, reducing setup revisions by nearly 25%. Entertainment technology providers are expanding strategic alliances with cloud, AI, and visualization specialists while increasing investment in interoperable production platforms. Companies capable of integrating digital twins into end-to-end content ecosystems will strengthen operational resilience, accelerate innovation cycles, and establish durable competitive positioning.

The strongest market driver is the rapid enterprise adoption of AI-powered virtual production and real-time simulation across film, gaming, broadcasting, and live entertainment. More than 45% of large studios have expanded investment in digital production infrastructure, while automated asset generation improves workflow efficiency by approximately 30% and reduces production revisions by nearly 22%. The United States continues upgrading virtual production facilities as AI computing capacity expands, encouraging ecosystem-wide modernization. Entertainment technology companies are responding through cloud partnerships, visualization software innovation, and digital content platform expansion. The strategic advantage extends beyond production speed, enabling standardized asset reuse across multiple projects while improving operational consistency and creative scalability.

Limited interoperability between production software, rendering engines, and legacy media infrastructure remains a significant structural barrier. Around 34% of entertainment organizations continue operating hybrid production environments, while integration expenses can account for nearly 20% of digital transformation budgets. Japan and several European production houses also face compatibility challenges when combining older animation workflows with modern simulation platforms. These constraints delay enterprise deployment, increase implementation complexity, and reduce operational efficiency. Companies are mitigating risks through standardized data architectures, localized cloud infrastructure, long-term technology partnerships, and modular deployment strategies that simplify system integration without disrupting ongoing production operations.

A major opportunity lies in combining digital twins with generative AI, spatial computing, and immersive audience analytics to create intelligent entertainment ecosystems. AI-assisted production environments can improve creative productivity by approximately 35%, while predictive audience engagement models increase campaign precision by nearly 18%. South Korea continues investing in metaverse-compatible entertainment infrastructure, creating favorable conditions for integrated digital experiences. Companies are strengthening competitive positions through joint R&D initiatives, cloud-based collaboration platforms, and ecosystem partnerships connecting studios, game developers, and technology providers. A notable strategic opportunity is the commercialization of reusable digital assets across multiple entertainment formats, significantly improving long-term production efficiency.

The primary long-term challenge is scaling digital twin deployments while maintaining cybersecurity, performance consistency, and skilled workforce availability. Nearly 41% of enterprises identify integration of AI, simulation, and real-time rendering as a complex operational priority, while cybersecurity incidents targeting media infrastructure have increased digital risk awareness across the industry. The United Kingdom and the United States are strengthening digital resilience expectations for enterprise technology environments, requiring more secure production ecosystems. Companies must expand workforce capabilities, strengthen cyber protection, invest in high-performance computing infrastructure, and establish standardized deployment frameworks to maintain operational continuity and competitive differentiation as digital production environments become increasingly interconnected.

AI-Driven Virtual Production Scaling Entertainment studios are embedding digital twins into production planning, with AI-assisted scene simulation increasing by nearly 38% and digital asset reuse improving approximately 30%. Cloud-native workflows shorten rendering queues by 24%, reducing production bottlenecks. Technology transitions toward GPU-intensive infrastructure are encouraging vendors to expand platform partnerships and integrated visualization capabilities across the United States and Japan.

Real-Time Venue Intelligence Expansion Live entertainment operators are deploying venue twins for crowd analytics, emergency planning, and energy optimization. Simulation-driven operational decisions improve visitor flow efficiency by around 27% while reducing event setup adjustments by 22%. Increased public safety requirements and large-scale event modernization are driving operators to automate facility monitoring and strengthen collaboration with infrastructure technology providers.

Cross-Platform Content Synchronization Gaming and broadcasting companies are adopting interoperable digital twin environments that synchronize production assets across multiple platforms. Shared content libraries reduce duplicate asset creation by approximately 29%, while collaborative production cycles accelerate by 25%. Companies are restructuring digital workflows, standardizing data architectures, and investing in unified production ecosystems to improve scalability and content consistency.

Predictive Operations and Automation Entertainment enterprises are integrating predictive analytics into digital twin platforms, enabling equipment utilization improvements exceeding 20% and maintenance planning accuracy approaching 35%. Labor shortages affecting advanced production environments have accelerated automation investment. A notable shift is the growing use of operational twins for back-end infrastructure rather than only creative production, prompting vendors to expand lifecycle management capabilities through enterprise software integration.

Virtual Production Twins represent the leading segment because they deliver integrated visualization, real-time collaboration, and production simulation within a single environment. Approximately 41% of enterprise deployments prioritize this category due to faster content creation, lower revision rates, and improved cross-team coordination. Asset Twins remain widely adopted for digital asset lifecycle management, while Process Twins optimize production workflows by reducing operational delays by nearly 22%. System Twins continue supporting interconnected media infrastructure where synchronization across rendering, storage, and cloud computing environments is operationally critical.

Venue Twins are emerging as the fastest-growing segment, supported by increasing deployment across stadiums, entertainment arenas, and large public events. Adoption has expanded by approximately 28% as operators prioritize crowd simulation, safety planning, and facility optimization. Companies are strengthening portfolios through AI integration, cloud interoperability, and enterprise partnerships that enable scalable deployment across multiple entertainment environments. Investment priorities are gradually shifting toward integrated twin ecosystems capable of supporting production, operations, and audience management within a unified platform.

Film Production remains the dominant application because digital twins improve production planning, virtual set design, and real-time collaboration throughout complex filming environments. Around 44% of enterprise deployments are concentrated within film production, while AI-enabled simulation reduces production revisions by nearly 26%. Broadcasting continues expanding digital twin implementation for studio operations and workflow orchestration, whereas Theme Parks increasingly utilize simulation platforms for visitor management and infrastructure optimization.

Gaming represents the fastest-growing application as developers integrate persistent digital environments, physics simulation, and live service optimization into production pipelines. Deployment activity has increased by approximately 31%, supported by cloud gaming infrastructure and advanced rendering technologies. Live Events also continue expanding through digital venue management and operational simulation that improves planning efficiency and resource allocation. Companies are scaling platform interoperability, strengthening technology alliances, and investing in unified production ecosystems that support multiple entertainment applications from a single operational framework.

Media Companies account for the largest share of digital twin adoption because they operate extensive production, broadcasting, streaming, and digital asset management infrastructure. Nearly 39% of enterprise implementations originate from media organizations seeking unified production environments and automated operational oversight. Film Studios remain significant adopters through virtual production expansion, while Broadcasters increasingly deploy digital twins to optimize newsroom coordination, transmission infrastructure, and studio automation for continuous content delivery.

Gaming Companies represent the fastest-growing end-user group as live-service gaming and immersive digital environments require continuous simulation, monitoring, and optimization. Adoption has increased by approximately 33%, supported by investments in AI-driven development platforms and cloud-native production pipelines. Event Organizers are expanding deployment for venue simulation, crowd management, and operational planning before large-scale entertainment events. Technology vendors are responding through customized enterprise platforms, subscription-based deployment models, ecosystem partnerships, and industry-specific software capabilities that improve scalability while strengthening long-term customer retention.

North America accounted for the largest market share at 39.4% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a 10.3% CAGR between 2026 and 2033.

AI-Powered Production Infrastructure Leads Regional Transformation

North America remains the leading regional market due to its concentration of major film studios, gaming companies, hyperscale cloud providers, and advanced virtual production infrastructure. More than 46% of enterprise-grade entertainment deployments are concentrated across the United States and Canada, supported by widespread adoption of AI-assisted production environments and real-time rendering platforms. Studio modernization programs continue replacing conventional production workflows with integrated digital ecosystems, reducing production delays by approximately 24%. Strategic partnerships between entertainment companies, cloud infrastructure providers, and visualization technology firms are accelerating deployment across film, broadcasting, and immersive entertainment. Continued investment in GPU infrastructure, digital content pipelines, and collaborative production platforms strengthens operational efficiency while supporting faster commercialization of high-value digital content.

United States Market Outlook: The United States remains the regional technology leader through its extensive concentration of virtual production studios, digital media enterprises, and cloud computing infrastructure. Nearly 60% of large entertainment organizations have incorporated advanced simulation technologies into production planning, supported by enterprise AI integration and expanding high-performance computing capacity. Continuous investment in digital content ecosystems, studio automation, and collaborative production environments enables companies to accelerate content delivery while improving production consistency across multiple entertainment formats.

Digital Modernization Strengthens Creative Ecosystems

Europe continues expanding digital twin deployment through media modernization, creative technology investment, and standardized digital production practices. The region contributes approximately 27% of global implementation activity, supported by advanced broadcasting infrastructure, animation production, and immersive media development. Enterprise deployment has increased by nearly 21% as production companies prioritize integrated digital workflows and secure content management. Sustainability objectives also encourage efficient virtual production methods that reduce unnecessary physical resource consumption during large-scale productions. Companies are strengthening collaboration between software developers, content creators, and technology providers while expanding interoperable production platforms that improve operational visibility and digital asset management.

Germany Market Outlook: Germany serves as Europe's primary enterprise hub through its strong industrial software ecosystem, advanced visualization expertise, and growing digital media infrastructure. Entertainment technology firms continue integrating simulation platforms with cloud-based production environments, while enterprise adoption of intelligent production workflows has exceeded 35% among large media organizations. Continued investment in AI development, digital engineering capabilities, and collaborative innovation strengthens Germany's competitive position within the regional entertainment technology landscape.

Rapid Digital Ecosystem Expansion Accelerates Adoption

Asia-Pacific is emerging as the fastest-expanding regional market because of accelerating digital entertainment investment, expanding gaming ecosystems, and advanced production infrastructure. Approximately 34% of new enterprise deployments originate from the region, supported by rapid cloud infrastructure development and AI-enabled content creation. Entertainment companies are integrating digital twins into animation, esports, film production, and immersive entertainment environments to improve production speed and operational scalability. Strategic investment in next-generation digital infrastructure and localized cloud computing continues reducing deployment complexity while strengthening regional technology ecosystems. Companies increasingly prioritize platform interoperability and scalable production architectures to support expanding entertainment demand.

China Market Outlook: China leads regional deployment through its large digital entertainment industry, extensive cloud infrastructure, and strong investment in AI-enabled production technologies. More than 40% of large-scale entertainment technology projects integrate intelligent simulation or virtual production capabilities across gaming, film, and interactive media. Domestic technology providers continue expanding cloud collaboration platforms and enterprise visualization capabilities, strengthening digital production capacity while supporting large-scale content creation and operational efficiency.

Entertainment Digitalization Creates New Demand

South America is experiencing steady digital twin adoption as entertainment organizations modernize production workflows and expand cloud-based operations. Brazil and neighboring markets are increasing investment in virtual production capabilities, digital broadcasting, and live event management. Enterprise implementation has improved by approximately 18% as organizations seek greater production efficiency and lower operational disruption. Infrastructure availability and skilled workforce capacity remain uneven across several markets, encouraging phased deployment strategies rather than enterprise-wide implementation. Technology providers are responding through localized partnerships, managed cloud services, and modular deployment models that reduce implementation complexity while supporting long-term digital transformation.

Brazil Market Outlook: Brazil represents the region's largest opportunity because of its extensive broadcasting industry, expanding streaming ecosystem, and active live entertainment sector. Around one-third of major media organizations are investing in AI-supported production modernization and cloud-based content management platforms. Local technology partnerships and improved digital infrastructure continue strengthening enterprise readiness, enabling broader adoption of simulation-driven production workflows and collaborative digital content operations.

Infrastructure Investment Supports Digital Entertainment

The Middle East & Africa market is advancing through government-backed digital transformation programs, smart venue development, and investment in world-class entertainment infrastructure. Large-scale entertainment projects increasingly integrate digital twins for operational planning, visitor management, and immersive experiences. Enterprise deployment has expanded by approximately 20%, supported by intelligent infrastructure modernization and next-generation event facilities. Organizations are emphasizing cloud-enabled operational visibility and AI-supported simulation to improve planning accuracy while reducing project execution risks. Strategic collaboration between technology providers and entertainment developers continues strengthening regional deployment capabilities across emerging digital entertainment ecosystems.

Saudi Arabia Market Outlook: Saudi Arabia has established itself as the regional leader through significant investment in entertainment infrastructure, digital innovation initiatives, and smart venue development. More than 30% of newly developed large entertainment facilities incorporate advanced digital planning technologies during project execution. Government-backed digital transformation initiatives, combined with expanding partnerships between international technology providers and domestic entertainment organizations, continue accelerating enterprise deployment and strengthening the country's long-term competitive position in immersive entertainment technologies.

The Digital Twin in Entertainment Market is shaped by competition between global platform providers such as NVIDIA, Unity Technologies, Epic Games, Autodesk, and Siemens, and specialized visualization, simulation, and virtual production technology firms targeting niche entertainment workflows. The top five participants collectively account for approximately 49% of market activity, while regional developers compete through localized deployment and industry-specific customization. Competition centers on AI-enabled rendering, real-time simulation, cloud interoperability, and production workflow optimization, with advanced platforms improving production efficiency by nearly 30% and reducing digital asset development time by approximately 25%. Companies are expanding through cloud partnerships, virtual production alliances, enterprise software integration, and selective acquisitions to strengthen end-to-end digital ecosystems. The competitive shift favors interoperable platforms combining AI, simulation, and collaborative production rather than standalone visualization tools. High-performance computing requirements, proprietary software ecosystems, and enterprise integration complexity create significant entry barriers. Winning requires scalable AI-driven platforms, seamless interoperability, strong enterprise partnerships, rapid deployment capabilities, and continuous innovation.

NVIDIA Corporation

Siemens AG

Unity Technologies

Epic Games

Autodesk Inc.

Dassault Systèmes

Hexagon AB

Bentley Systems

PTC Inc.

Microsoft Corporation

Amazon Web Services

IBM Corporation

Digital twin platforms are rapidly evolving through AI-assisted simulation, real-time rendering, cloud-native production, and high-performance GPU computing. More than 52% of large entertainment enterprises are deploying AI-enabled production workflows to improve content creation speed and operational visibility. Compared with conventional production planning, intelligent digital twin platforms reduce production revisions by approximately 28% while improving collaborative workflow efficiency by nearly 32%. Cloud-connected digital assets also enable synchronized production across geographically distributed teams, strengthening enterprise scalability and reducing project delays.

Emerging technologies including generative AI, spatial computing, volumetric capture, and edge-enabled rendering are transforming entertainment production ecosystems. Real-time simulation improves resource utilization by approximately 24%, while predictive infrastructure monitoring lowers unexpected operational interruptions by nearly 20%. Global cloud providers, leading visualization vendors, and advanced media studios gain the strongest competitive advantage because integrated technology stacks support faster deployment, higher asset interoperability, and continuous production optimization across film, gaming, broadcasting, and live entertainment environments.

Between 2026 and 2028, autonomous production orchestration, interoperable digital ecosystems, and AI-driven content optimization will become strategic technology priorities. Enterprise adoption of unified digital production platforms is expected to exceed 60%, replacing fragmented legacy systems with intelligent environments capable of managing creative, operational, and infrastructure workflows simultaneously. Companies investing early in scalable simulation platforms, secure cloud integration, and automated production intelligence will achieve stronger operational resilience, shorter development cycles, and greater competitive differentiation as digital entertainment production becomes increasingly data-driven.

February 2024 – Epic Games and Disney announced a long-term partnership to build an open entertainment universe connected to Fortnite using Unreal Engine. Disney also committed a USD 1.5 billion equity investment, strengthening large-scale digital content and immersive experience development.

October 2024 – Epic Games introduced Unreal Engine 5.5 Preview at Unreal Fest Seattle, expanding real-time rendering and creator workflows. The company also launched improved royalty terms offering eligible developers a 3.5% royalty rate, accelerating enterprise adoption across interactive entertainment production. Source: (Unreal Engine)

January 2025 – NVIDIA expanded Omniverse with generative physical AI models and new digital twin blueprints, while Microsoft, Siemens, Accenture, and other technology leaders adopted the platform. The initiative supports AI-enabled digital twins through an ecosystem spanning more than seven major enterprise partners.

March 2025 – Siemens announced the general availability of Teamcenter Digital Reality Viewer powered by NVIDIA Omniverse, enabling photorealistic digital twins with standards-based interoperability. The solution reduces workflow waste and improves engineering collaboration through integrated enterprise-scale visualization capabilities.

This report provides comprehensive analysis of the Digital Twin in Entertainment Market across five major types, five key applications, and five principal end-user categories, supported by detailed assessment of North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. The study evaluates enterprise deployment patterns, technology integration, competitive positioning, digital production workflows, and AI-enabled simulation trends. More than 40% of enterprise implementations are concentrated in virtual production and media operations, highlighting evolving investment priorities across entertainment ecosystems.

The report further examines competitive strategies, digital infrastructure modernization, cloud-native production platforms, real-time rendering technologies, and emerging AI-driven content ecosystems between 2026 and 2033. It delivers actionable insights for investment planning, partnership evaluation, product development, expansion strategy, and technology adoption while identifying high-potential growth segments, deployment opportunities, enterprise transformation priorities, and shifting competitive dynamics influencing long-term business decision-making across the global entertainment industry.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 535.28 Million |

Market Revenue in 2033 | USD 1044.1 Million |

CAGR (2026 - 2033) | 8.71% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | NVIDIA Corporation, Siemens AG, Unity Technologies, Epic Games, Autodesk Inc., Dassault Systèmes, Hexagon AB, Bentley Systems, PTC Inc., Microsoft Corporation, Amazon Web Services, IBM Corporation |

Customization & Pricing | Available on Request (10% Customization is Free) |