Reports

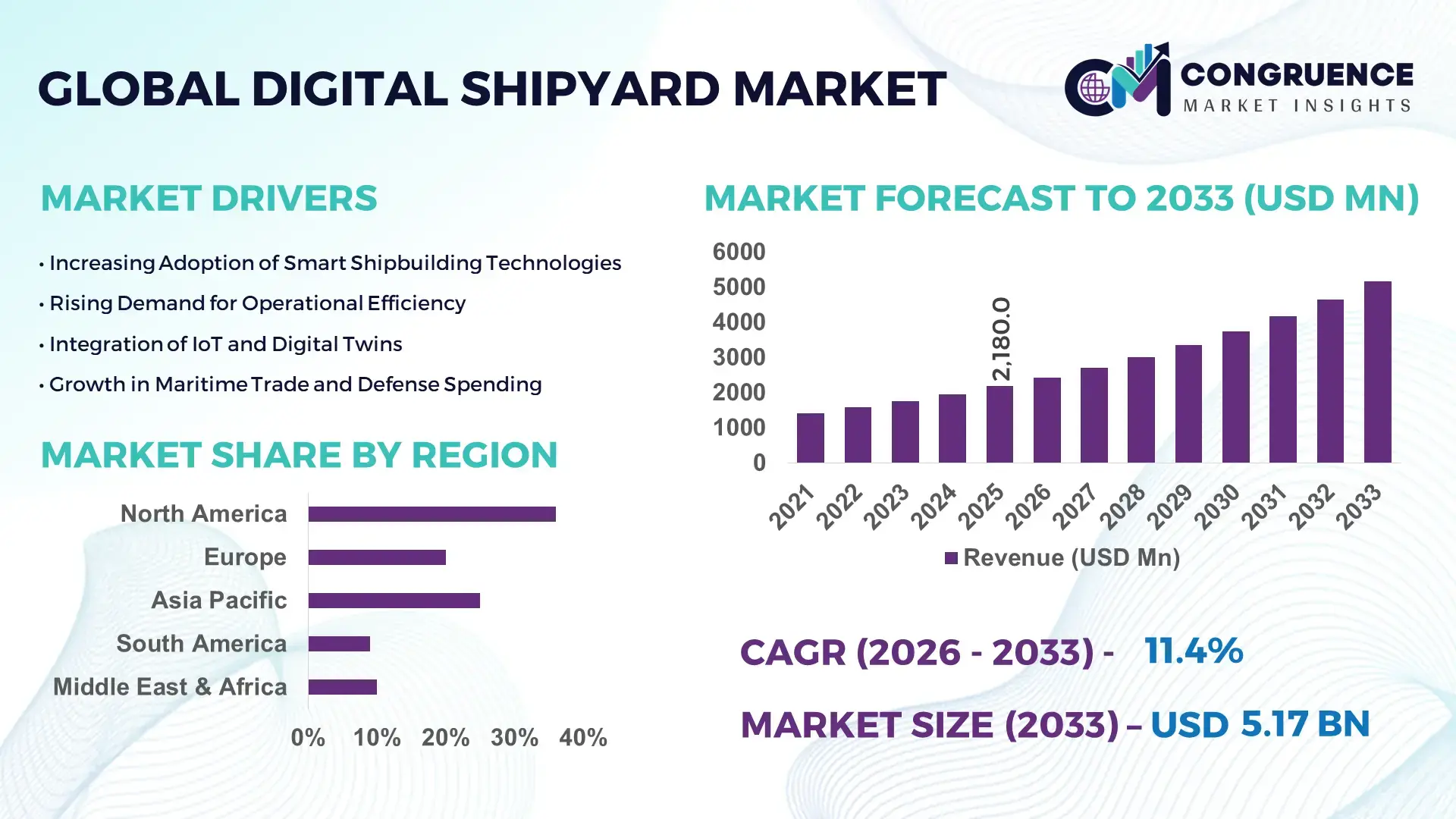

The Global Digital Shipyard Market was valued at USD 2180 Million in 2025 and is anticipated to reach a value of USD 5166.85 Million by 2033 expanding at a CAGR of 11.39% between 2026 and 2033. This growth is primarily driven by the rapid integration of advanced digital technologies to enhance shipbuilding efficiency, reduce lifecycle costs, and improve operational transparency.

The United States leads in the Digital Shipyard Market with substantial investments in naval modernization and commercial shipbuilding digitization programs. U.S. shipyards have integrated advanced digital twin technologies across more than 65% of large-scale naval projects, significantly improving production accuracy and reducing rework rates by nearly 30%. Annual investments in smart shipyard infrastructure exceed USD 1.5 billion, focusing on AI-driven design platforms, robotics, and IoT-enabled monitoring systems. The country’s defense sector accounts for over 55% of digital shipyard adoption, with commercial shipbuilders increasingly adopting cloud-based design and simulation tools. Additionally, workforce digitization initiatives have enhanced productivity by approximately 20%, reflecting a strong shift toward automated and data-driven shipbuilding ecosystems.

Market Size & Growth: USD 2180 Million in 2025, projected to reach USD 5166.85 Million by 2033, growing at 11.39% CAGR due to increased adoption of automation and digital twin technologies.

Top Growth Drivers: Automation adoption (45%), production efficiency improvement (30%), reduction in operational downtime (25%).

Short-Term Forecast: By 2028, predictive maintenance technologies are expected to reduce maintenance costs by 20% and improve asset utilization by 18%.

Emerging Technologies: Digital twins, AI-based ship design platforms, IoT-enabled smart shipyard systems.

Regional Leaders: North America projected at USD 1800 Million by 2033 with strong defense digitization; Europe at USD 1400 Million driven by green shipbuilding; Asia-Pacific at USD 1600 Million with rapid industrial expansion.

Consumer/End-User Trends: Naval defense and commercial shipbuilders account for over 70% of adoption, with increasing reliance on real-time analytics and automation tools.

Pilot or Case Example: In 2024, a European shipyard achieved 25% reduction in construction time through AI-enabled digital twin implementation.

Competitive Landscape: Market leader holds approximately 22% share, followed by key players including Siemens, Dassault Systèmes, Hexagon AB, AVEVA, and Kongsberg Gruppen.

Regulatory & ESG Impact: Regulations promoting carbon-neutral shipbuilding are driving adoption of energy-efficient digital systems reducing emissions by up to 15%.

Investment & Funding Patterns: Over USD 4 billion invested globally in digital shipyard transformation projects, with rising public-private partnerships.

Innovation & Future Outlook: Integration of AI, robotics, and cloud-based collaboration platforms is reshaping shipyard operations toward fully autonomous production environments.

The Digital Shipyard Market is witnessing strong contributions from defense, commercial shipping, and offshore energy sectors, collectively accounting for over 80% of industry demand. Recent innovations include AI-driven hull design optimization, automated welding robots improving precision by 35%, and digital twin simulations reducing design errors by nearly 40%. Regulatory frameworks focused on emissions reduction and sustainable shipbuilding are accelerating digital adoption, particularly in Europe and Asia-Pacific. Consumption patterns indicate that Asia-Pacific accounts for over 45% of new shipbuilding activity, while North America leads in technological deployment. Emerging trends such as cloud-based shipyard management and blockchain-enabled supply chain transparency are expected to define the future landscape, positioning the market for sustained digital transformation.

The Digital Shipyard Market holds strategic importance as global shipbuilding transitions toward data-driven, automated, and highly efficient production ecosystems. The integration of digital twin technology delivers up to 35% improvement in design accuracy compared to traditional CAD-based methods, enabling shipbuilders to reduce costly rework and accelerate delivery timelines. Artificial intelligence-powered analytics further enhances predictive maintenance capabilities, improving equipment uptime by nearly 25% compared to legacy maintenance practices.

Asia-Pacific dominates in production volume due to large-scale shipbuilding operations, while Europe leads in adoption with over 60% of shipyards implementing advanced digital solutions focused on sustainability and compliance. In the short term, by 2028, AI-enabled process optimization is expected to improve operational efficiency by 20% and reduce construction timelines by approximately 18%. From an ESG perspective, firms are committing to reducing carbon emissions by 30% by 2030 through the use of energy-efficient digital systems and optimized resource planning. Smart shipyards are also implementing waste reduction technologies, achieving up to 15% improvement in material utilization.

In 2024, a leading South Korean shipbuilder achieved a 28% increase in productivity by deploying a fully integrated digital twin platform combined with IoT-enabled monitoring systems. This micro-scenario demonstrates the measurable impact of digital transformation on operational performance. Looking ahead, the Digital Shipyard Market is set to become a cornerstone of resilient maritime infrastructure, enabling compliance with global environmental standards while driving sustainable growth through advanced automation and intelligent manufacturing systems.

The rising demand for automation in shipbuilding is significantly driving the Digital Shipyard Market. Automated systems such as robotic welding and AI-based design tools have improved production efficiency by up to 30%, reducing manual intervention and minimizing errors. Digital twins enable real-time simulation of shipbuilding processes, leading to a 25% reduction in rework and improved design accuracy. Additionally, IoT-enabled monitoring systems enhance equipment performance by providing predictive maintenance insights, reducing downtime by approximately 20%. The growing need to meet tight delivery schedules and manage complex ship designs is further encouraging shipbuilders to adopt digital solutions, resulting in streamlined operations and enhanced productivity across shipyard facilities.

High initial investment requirements remain a major restraint in the Digital Shipyard Market. The deployment of advanced technologies such as AI, IoT, and digital twin platforms involves substantial capital expenditure, often exceeding millions of dollars for large shipyards. Smaller and mid-sized shipbuilders face challenges in adopting these technologies due to limited financial resources. Additionally, integrating digital systems with legacy infrastructure can increase costs by up to 20%, requiring significant upgrades and workforce training. The lack of standardized digital frameworks also creates compatibility issues, further complicating implementation. These financial and technical barriers slow down adoption rates, particularly in developing regions where budget constraints and limited access to advanced technologies persist.

The expansion of smart shipbuilding presents significant growth opportunities for the Digital Shipyard Market. The increasing adoption of connected shipyard ecosystems, powered by IoT and cloud computing, enables real-time data exchange and improves operational efficiency by up to 25%. Emerging markets in Asia-Pacific are investing heavily in digital infrastructure, with shipbuilding output increasing by over 40% in recent years. The integration of augmented reality and virtual reality tools for design and training is also creating new avenues for innovation, enhancing workforce productivity by nearly 15%. Furthermore, the growing focus on sustainable shipbuilding practices is driving demand for digital solutions that optimize energy consumption and reduce emissions, opening new market segments and expanding the scope of digital shipyard technologies.

Cybersecurity risks and data integration complexities pose significant challenges to the Digital Shipyard Market. As shipyards increasingly rely on interconnected digital systems, the risk of cyberattacks has risen, with reported incidents increasing by over 20% in maritime industries. Protecting sensitive design data and operational systems requires advanced security measures, adding to overall costs. Additionally, integrating diverse data sources from multiple platforms can be complex, often leading to inefficiencies and data silos. Legacy systems may lack compatibility with modern digital tools, resulting in delays and increased implementation time. These challenges necessitate robust cybersecurity frameworks and standardized data integration protocols, which remain critical barriers to achieving seamless digital transformation in shipyard operations.

• Rapid Expansion of Digital Twin Adoption Across Shipyards: Digital twin technology is becoming a cornerstone of modern shipyard operations, with over 60% of large-scale shipbuilders integrating virtual simulation models into their workflows. These systems enable real-time monitoring and predictive analysis, reducing design errors by approximately 35% and improving production efficiency by nearly 28%. In advanced shipyards, digital twin implementation has shortened vessel development cycles by 20%, while improving asset lifecycle management by over 25%. The growing complexity of naval and commercial vessels is further accelerating adoption, particularly in technologically advanced regions.

• Accelerated Integration of AI and Automation in Shipbuilding Processes: Artificial intelligence and automation are transforming shipyard productivity, with more than 50% of shipyards deploying AI-driven planning and robotic systems. Automated welding and cutting technologies have improved precision rates by 30% while reducing material wastage by 18%. AI-powered scheduling tools have enhanced project timeline accuracy by nearly 22%, enabling better resource allocation. The shift toward autonomous operations is also reducing labor dependency by approximately 15%, addressing workforce shortages and improving overall operational resilience.

• Increasing Focus on Sustainable and Green Shipyard Operations: Sustainability is a major trend, with over 45% of shipyards adopting energy-efficient digital solutions to meet environmental regulations. Smart energy management systems have reduced power consumption by up to 20%, while digital optimization tools have lowered carbon emissions by nearly 15%. Shipbuilders are increasingly leveraging digital platforms to design eco-friendly vessels, resulting in improved fuel efficiency of up to 12%. Regulatory mandates and global sustainability targets are driving this transition toward greener digital shipyard practices.

• Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Digital Shipyard market. Research indicates that 55% of new shipbuilding projects achieve cost benefits through modular and prefabricated practices. Pre-fabricated ship components produced using automated machinery have reduced on-site labor requirements by 25% and shortened construction timelines by nearly 30%. Demand for high-precision fabrication technologies is particularly strong in Europe and North America, where efficiency and scalability are critical to meeting increasing shipbuilding demands.

The Digital Shipyard Market is segmented based on type, application, and end-user, each contributing significantly to the overall industry landscape. From a type perspective, solutions such as digital twin systems, robotics, and advanced analytics platforms are widely deployed to enhance shipyard operations. Applications range from ship design and engineering to production planning and maintenance optimization, reflecting the market’s broad functional scope. End-users primarily include naval defense organizations, commercial shipbuilders, and offshore energy companies, each adopting digital shipyard solutions to improve efficiency and reduce operational risks. The increasing integration of AI, IoT, and cloud-based systems across these segments is driving operational transformation, with adoption rates exceeding 50% in technologically advanced shipyards. Additionally, the segmentation highlights a clear shift toward automation and sustainability, as stakeholders prioritize cost optimization and compliance with environmental standards.

The Digital Shipyard Market by type is dominated by digital twin solutions, robotics and automation systems, IoT platforms, and advanced analytics software. Digital twin technology leads the segment, accounting for approximately 38% of adoption due to its ability to simulate shipbuilding processes and reduce design errors by up to 35%. Robotics and automation systems follow with around 27% share, driven by their role in improving production efficiency and reducing manual labor by nearly 20%. IoT-enabled monitoring platforms contribute close to 18%, enabling real-time data collection and predictive maintenance capabilities that enhance operational uptime by 25%.

Advanced analytics and cloud-based management systems represent the fastest-growing segment, expanding at an estimated CAGR of 14%, supported by increasing demand for data-driven decision-making and remote collaboration tools. These solutions are rapidly gaining traction as shipyards seek to optimize supply chain operations and improve project visibility. The remaining segments, including AR/VR-based design tools and cybersecurity solutions, collectively account for about 17% of the market, offering niche yet critical functionalities.

In terms of application, ship design and engineering holds the largest share of approximately 34%, driven by the increasing use of AI-powered design tools that improve accuracy and reduce design cycle times by up to 25%. Production planning and process optimization account for around 28% of the market, as shipyards adopt digital platforms to streamline workflows and enhance resource utilization. Maintenance and lifecycle management applications represent about 20%, supported by predictive maintenance technologies that reduce equipment downtime by nearly 22%.

Supply chain and logistics management is the fastest-growing application segment, with an estimated CAGR of 13%, fueled by the need for real-time tracking and efficient coordination across global supply networks. Digital platforms are enabling shipbuilders to reduce supply chain delays by up to 18% and improve inventory management efficiency by approximately 20%. The remaining applications, including training and simulation, contribute around 18%, supporting workforce development and operational readiness.

Naval defense organizations represent the leading end-user segment in the Digital Shipyard Market, accounting for approximately 42% of total adoption due to extensive investments in fleet modernization and advanced shipbuilding technologies. Commercial shipbuilders follow with around 33% share, driven by increasing global demand for cargo vessels and cruise ships, alongside the need for cost-efficient production processes. Offshore energy companies contribute nearly 15%, leveraging digital shipyard solutions to enhance the construction and maintenance of specialized vessels and platforms.

Commercial shipbuilders are emerging as the fastest-growing end-user segment, expanding at an estimated CAGR of 12%, supported by rising maritime trade and increasing adoption of automation technologies. These companies are achieving productivity gains of up to 20% through digital transformation initiatives. The remaining end-users, including ship repair and maintenance providers, account for approximately 10%, focusing on predictive maintenance and lifecycle optimization solutions.

Region North America accounted for the largest market share at 36% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 13.2% between 2026 and 2033.

North America’s dominance is supported by over 65% adoption of digital shipyard technologies across large naval facilities and more than 50% integration of AI-driven production systems. Europe holds approximately 28% share, driven by sustainability-focused shipbuilding programs, with over 40% of shipyards implementing energy-efficient digital tools. Asia-Pacific accounts for nearly 30% of global shipbuilding output, with China, South Korea, and Japan contributing over 70% of regional production capacity. Digital transformation investments in the region have increased by 35% in the last three years. Meanwhile, South America and the Middle East & Africa collectively account for around 6% share, with growing investments in offshore energy projects and port infrastructure modernization driving digital shipyard adoption.

How are advanced naval modernization programs shaping digital transformation in shipbuilding?

North America holds approximately 36% of the Digital Shipyard Market share, driven by strong demand from naval defense and commercial shipbuilding sectors. The region benefits from significant government investments, with over 55% of digital shipyard spending linked to defense modernization initiatives. Regulatory frameworks promoting cybersecurity and digital infrastructure resilience are accelerating adoption of advanced technologies such as AI, IoT, and digital twins. Over 60% of shipyards in the region have integrated automation systems, improving production efficiency by nearly 25%. A key example includes a leading U.S.-based shipbuilder deploying AI-enabled digital twin platforms to reduce construction errors by 30%. Consumer behavior in the region reflects high enterprise adoption, particularly in defense and large-scale commercial operations, where over 70% of companies prioritize digital integration to enhance operational efficiency and compliance.

Why is sustainability-driven innovation accelerating digital shipyard adoption?

Europe accounts for nearly 28% of the Digital Shipyard Market, with key markets including Germany, the United Kingdom, and France leading adoption. Over 45% of European shipyards have implemented environmentally sustainable digital solutions aligned with strict regulatory mandates. Policies focused on reducing maritime emissions by 30% by 2030 are driving demand for energy-efficient shipyard technologies. The region has witnessed over 40% adoption of digital twin systems and AI-based design platforms. A notable example is a European shipbuilder integrating automated production systems that improved manufacturing precision by 28%. Consumer behavior in Europe is heavily influenced by regulatory compliance, with over 65% of enterprises prioritizing sustainable and transparent digital shipyard solutions, reflecting a strong preference for environmentally responsible operations.

What factors are driving large-scale digital transformation in shipbuilding hubs?

Asia-Pacific represents the fastest-growing region and contributes nearly 30% of global Digital Shipyard Market activity, ranking first in shipbuilding volume. China, Japan, and South Korea collectively account for over 70% of regional ship production, supported by large-scale infrastructure and manufacturing capabilities. Digital adoption in the region has increased by more than 35% over the past three years, with significant investments in automation and AI technologies. A leading South Korean shipbuilder implemented smart shipyard systems that improved productivity by 27% and reduced construction timelines by 20%. Innovation hubs across the region are focusing on robotics and IoT integration, enhancing operational efficiency. Consumer behavior reflects rapid industrial adoption, with over 60% of shipbuilders investing in digital transformation to remain competitive in global markets.

How are offshore energy projects influencing digital shipyard demand?

South America holds approximately 4% of the Digital Shipyard Market, with Brazil and Argentina emerging as key contributors. The region’s growth is closely tied to offshore oil and gas exploration, which accounts for over 50% of demand for advanced shipbuilding technologies. Infrastructure investments have increased by 20% in recent years, focusing on modernizing shipyards and port facilities. Government incentives supporting industrial digitization are encouraging adoption of automation and digital design tools. A regional shipbuilder in Brazil has implemented IoT-based monitoring systems, improving equipment efficiency by 18%. Consumer behavior is influenced by sector-specific demand, with over 55% of adoption driven by energy and resource-based industries requiring specialized vessels and digital capabilities.

What role does infrastructure modernization play in advancing shipyard digitization?

The Middle East & Africa region accounts for approximately 2% of the Digital Shipyard Market, with the UAE and South Africa leading development. Demand is primarily driven by oil and gas, maritime logistics, and infrastructure expansion projects, contributing to over 60% of regional adoption. Governments are investing in smart port and shipyard initiatives, with digital transformation projects increasing by 25% in the past five years. Technological modernization includes the adoption of AI-driven maintenance systems and automated fabrication processes. A UAE-based shipyard has introduced digital workflow systems, improving operational efficiency by 22%. Consumer behavior reflects a growing focus on modernization, with over 50% of enterprises prioritizing digital tools to enhance productivity and align with international trade standards.

United States – 34% share in the Digital Shipyard Market, driven by extensive naval defense programs and high adoption of AI-driven shipbuilding technologies.

China – 28% share in the Digital Shipyard Market, supported by large-scale ship production capacity and rapid industrial digitalization initiatives.

The Digital Shipyard Market is moderately consolidated, with over 40 active global and regional players competing across technology platforms, software solutions, and integrated shipyard systems. The top five companies collectively account for approximately 55% of the market, reflecting a competitive yet concentrated landscape dominated by established technology providers and industrial automation firms. Leading players are focusing on strategic partnerships and collaborations, with more than 30% of companies engaging in joint ventures to expand their digital capabilities and geographic presence.

Innovation remains a key competitive factor, with over 50% of market participants investing heavily in research and development to enhance AI, digital twin, and IoT-based solutions. Product launches have increased by nearly 25% annually, particularly in areas such as predictive maintenance and real-time analytics platforms. Mergers and acquisitions are also shaping the market, with over 15 notable deals recorded in recent years aimed at strengthening digital portfolios and expanding service offerings.

Additionally, companies are prioritizing cloud-based platforms and cybersecurity solutions to address increasing data integration challenges. The competitive environment is further intensified by the entry of new technology startups, which account for approximately 20% of active players, bringing innovative solutions and increasing market dynamism.

Siemens

Dassault Systèmes

Hexagon AB

AVEVA

Kongsberg Gruppen

Accenture

IBM

BAE Systems

General Dynamics

Wärtsilä

ABB

SAP

Inmarsat

Rolls-Royce Holdings

HCLTech

The Digital Shipyard Market is being reshaped by a convergence of advanced technologies that enhance precision, efficiency, and lifecycle management across shipbuilding operations. Digital twin technology remains a foundational innovation, with over 60% of large shipyards deploying simulation-driven design environments that reduce engineering errors by up to 35% and accelerate development timelines by nearly 20%. These systems enable real-time synchronization between physical assets and virtual models, improving predictive decision-making and reducing rework costs significantly. Artificial intelligence and machine learning are increasingly embedded into shipyard workflows, with more than 50% of shipbuilders utilizing AI-powered scheduling and design optimization tools. These technologies improve production planning accuracy by approximately 25% and enhance predictive maintenance capabilities, reducing equipment downtime by nearly 22%. Robotics and automation systems, including automated welding and cutting solutions, have achieved precision improvements of up to 30% while lowering labor dependency by around 15%.

The integration of Internet of Things (IoT) platforms is further advancing operational visibility, with connected sensors enabling real-time monitoring of equipment performance and environmental conditions. IoT-driven systems have improved asset utilization rates by over 20% and reduced unexpected failures by approximately 18%. Cloud computing is also playing a critical role, with over 45% of shipyards adopting cloud-based collaboration platforms to streamline global supply chain coordination and enable remote project management. Emerging technologies such as augmented reality (AR) and virtual reality (VR) are transforming workforce training and design validation processes, improving training efficiency by nearly 25% and reducing onboarding time by 20%. Additionally, blockchain-based solutions are gaining traction for secure supply chain management, enhancing transparency and reducing data discrepancies by up to 15%. These combined technological advancements are positioning digital shipyards as highly efficient, data-driven ecosystems capable of meeting complex maritime demands.

• In March 2025, Siemens expanded its digital shipyard portfolio by enhancing its Xcelerator platform with advanced ship design and lifecycle management capabilities, enabling integrated digital twin environments that improve engineering efficiency by over 25%. Source: www.siemens.com

• In October 2024, Dassault Systèmes partnered with a leading global shipbuilder to deploy its 3DEXPERIENCE platform for end-to-end ship lifecycle management, improving design collaboration and reducing development cycle times by approximately 20%. Source: www.3ds.com

• In July 2024, Hexagon AB introduced upgraded digital reality solutions for shipyard operations, integrating laser scanning and AI analytics to improve dimensional accuracy by nearly 30% and enhance quality control processes across large-scale shipbuilding projects. Source: www.hexagon.com

• In January 2025, Kongsberg Gruppen implemented advanced digital shipyard solutions in collaboration with a naval program, incorporating IoT-enabled monitoring systems that increased operational efficiency by 22% and reduced maintenance downtime by approximately 18%. Source: www.kongsberg.com

The Digital Shipyard Market Report provides a comprehensive analysis of the global shipbuilding transformation driven by advanced digital technologies and automation systems. The scope covers a wide range of technology segments, including digital twin platforms, artificial intelligence-based design systems, IoT-enabled monitoring solutions, robotics and automation tools, and cloud-based collaboration platforms. These technologies collectively account for over 70% of modern shipyard digitalization initiatives, reflecting their critical role in enhancing operational efficiency and reducing production complexity.

The report evaluates key application areas such as ship design and engineering, production planning, maintenance and lifecycle management, and supply chain optimization. Among these, design and engineering processes represent over 30% of digital solution deployment, while production and maintenance applications together account for more than 45%, highlighting their importance in improving shipyard productivity and asset performance.

Geographically, the scope includes major regions such as North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with Asia-Pacific contributing nearly 30% of global shipbuilding activity and North America leading in technological adoption. The report also examines end-user segments including naval defense, commercial shipbuilding, and offshore energy industries, which together account for over 85% of total demand for digital shipyard solutions.

Additionally, the scope incorporates emerging trends such as smart shipyard ecosystems, blockchain-enabled supply chain management, and AR/VR-based workforce training, which are gaining traction across more than 40% of advanced shipyards. By focusing on these critical areas, the report delivers actionable insights for stakeholders seeking to navigate the evolving digital shipyard landscape and capitalize on technological advancements.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

11.39% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Siemens, Dassault Systèmes, Hexagon AB, AVEVA, Kongsberg Gruppen, Accenture, IBM, BAE Systems, General Dynamics, Wärtsilä, ABB, SAP, Inmarsat, Rolls-Royce Holdings, HCLTech |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |