Reports

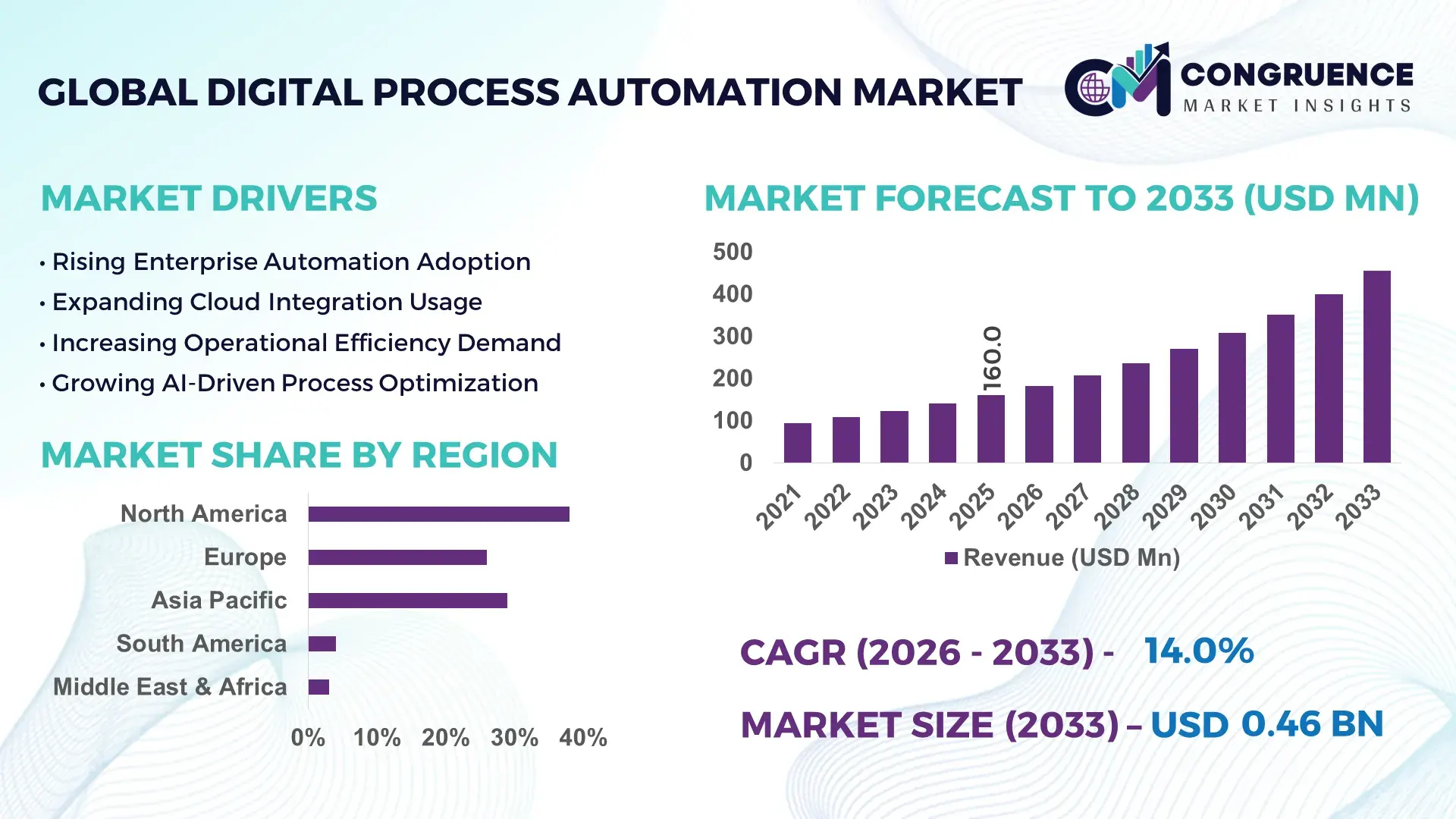

The Global Digital Process Automation Market was valued at USD 160.0 Million in 2025 and is anticipated to reach a value of USD 456.4 Million by 2033 expanding at a CAGR of 14% between 2026 and 2033. AI-driven workflow orchestration across enterprise ERP and cloud-native stacks is accelerating process digitization, with manufacturing and BFSI reducing manual cycle times by nearly 35% through integrated automation platforms.

The United States holds ~34% share driven by over USD 52 billion enterprise digitalization investments, while China accounts for ~21% supported by large-scale industrial AI deployment; India’s adoption is rising at ~18% in IT services and shared business operations, creating a widening execution gap between mature and emerging digital economies. The U.S.–China technology race in enterprise AI integration continues to reshape vendor ecosystems and platform standardization.

Strategic implication is that enterprises are increasingly prioritizing scalable automation ecosystems over isolated tools to secure cross-border operational efficiency and compliance readiness.

Market Size & Growth: USD 160.0M (2025) to USD 456.4M (2033), 14% CAGR, with AI workflow integration boosting enterprise efficiency by 28%

Top Growth Drivers: 42% cloud migration, 37% AI adoption, 31% process cost reduction pressure accelerating automation demand

Short-Term Forecast: By 2027, operational costs in automated enterprises decline by 22% while process turnaround improves by 30%

Emerging Technologies: AI orchestration, low-code platforms, hyperautomation ecosystems improving workflow speed by 40%

Regional Leaders: North America (~38%, cloud-first enterprise adoption), Asia-Pacific (~29%, industrial scaling), Europe (~24%, regulatory-driven automation)

Consumer/End-User Trends: 61% of large enterprises adopt hybrid automation models integrating legacy + cloud workflows

Pilot/Case Example: 2024 BFSI deployment reduced claim processing time by 48% using AI-based document automation

Competitive Landscape: Top vendor holds ~18% share, with UiPath, IBM, Microsoft, Appian, and Automation Anywhere leading ecosystem expansion

Regulatory & ESG Impact: Compliance automation reduces audit cycle time by 33% under evolving digital governance frameworks

Investment & Funding: Over USD 6.8B invested in automation startups and platform scaling through VC and enterprise partnerships

Innovation & Future Outlook: Shift toward autonomous enterprise systems with 50% higher workflow self-healing capability by 2030

The Digital Process Automation Market is witnessing rising demand across BFSI, healthcare, telecom, and manufacturing, where AI-enabled workflow automation reduces operational bottlenecks by nearly 32%. Low-code platforms and intelligent process mining are accelerating deployment speed by 45%, while regulatory digitization in Europe and supply-chain digitization in Asia are reshaping enterprise automation priorities. A growing trend shows 58% of enterprises integrating automation with cloud ERP systems, signaling a shift toward fully connected digital operations.

Digital Process Automation is becoming central to enterprise competitiveness as organizations shift toward data-driven, compliance-heavy, and cost-optimized operations. Rising regulatory scrutiny in financial services and healthcare is pushing firms to adopt standardized automation frameworks, while global supply-chain fragmentation is increasing reliance on real-time process visibility. This positions automation as a core infrastructure layer rather than a supporting IT function.

Compared to traditional manual workflows, AI-enabled process automation delivers up to 40% faster execution cycles and nearly 30% lower operational overhead through predictive task routing and exception handling. North America leads large-scale enterprise deployment, while Asia-Pacific shows faster scaling through cloud-native adoption, especially in manufacturing hubs where deployment velocity is 25% higher than in legacy-heavy European environments.

Over the next 2–3 years, enterprises are expected to prioritize platform consolidation and cross-system interoperability. A practical example includes multinational banks integrating end-to-end automation in compliance reporting, reducing audit preparation effort by nearly 45%. Companies are increasing partnerships with hyperscalers and automation vendors to strengthen resilience and achieve scalable, regulation-ready digital operations.

AI-driven workflow automation adoption across enterprises is increasing rapidly, with 46% of large organizations integrating process automation into core ERP and CRM systems. In the United States, enterprise digital transformation spending has risen by 29%, while Germany’s manufacturing automation penetration has crossed 38%, driven by Industry 4.0 initiatives. This shift is causing a structural move from siloed automation tools to end-to-end orchestration platforms. Financial services firms in Japan are reducing manual reconciliation workloads by nearly 33% through intelligent automation layers. In response, companies such as IBM and Microsoft are expanding cloud-native automation ecosystems and forming enterprise partnerships, while Indian IT service providers are scaling delivery centers to support global low-code deployments and managed automation services.

Nearly 52% of enterprises in Europe still operate hybrid legacy systems, creating interoperability gaps that delay full-scale digital process automation deployment. Integration costs have increased by around 27% in multi-platform environments, while cybersecurity compliance requirements in banking and healthcare add an additional 19% operational overhead. In the UK financial sector, fragmented data architectures have slowed automation rollouts in mid-sized institutions by 31%. This constraint directly impacts scalability and ROI timelines, especially for SMEs in Southeast Asia lacking standardized digital infrastructure. To mitigate risks, companies are investing in modular automation architectures, adopting API-first integration models, and entering long-term vendor contracts to stabilize implementation costs while reducing dependency on outdated legacy systems.

Emerging markets such as India and Vietnam are witnessing over 41% growth in enterprise automation adoption, driven by rapid cloud migration and government-backed digital infrastructure programs. Low-code and no-code platforms are reducing deployment time by nearly 44%, enabling mid-sized enterprises to participate in automation ecosystems previously dominated by large corporations. China’s smart manufacturing initiatives are integrating AI-based process orchestration across 36% of industrial clusters, creating scalable efficiency gains. This shift is opening new opportunities in compliance automation, digital procurement, and predictive operations management. Companies are actively investing in R&D partnerships and ecosystem alliances with hyperscalers to build localized automation stacks, particularly in regulated industries such as telecom and BFSI, where efficiency and compliance alignment are becoming critical competitive levers.

Approximately 49% of global enterprises report difficulty scaling automation beyond pilot phases due to inconsistent data structures and system fragmentation. Cybersecurity risks in automated workflows have increased by 22%, particularly in cloud-connected enterprise environments across the United States and South Korea. In industrial sectors, latency issues in real-time process orchestration reduce efficiency gains by nearly 18% when legacy systems remain partially integrated. This directly affects operational consistency and long-term deployment reliability. Companies are responding by investing in zero-trust architectures, advanced encryption protocols, and cross-platform orchestration frameworks, while also forming cybersecurity-focused partnerships to strengthen resilience. However, workforce skill gaps in automation engineering remain a structural barrier, limiting sustained scalability across complex enterprise ecosystems.

AI-driven orchestration scaling rapidly Enterprise adoption of AI-based workflow orchestration has increased by 44%, with 39% of U.S. Fortune 500 firms embedding automation directly into ERP systems. Japan’s manufacturing sector reports a 31% reduction in production downtime through predictive process automation, driven by labor shortages and supply-chain volatility. This shift is improving operational continuity by 28% and reducing manual intervention costs significantly. Companies such as SAP and IBM are expanding AI-integrated automation suites while enterprises are restructuring legacy workflows into unified digital process layers for faster execution.

Low-code democratization accelerating deployment speed Low-code platform usage has expanded by 52%, enabling 46% faster deployment cycles for enterprise automation initiatives. In India and Southeast Asia, SMEs account for nearly 37% of new adoption due to reduced technical dependency. This is shortening development timelines by 33% and lowering implementation overheads across service industries. Vendors are responding by enhancing drag-and-drop automation tools and forming ecosystem partnerships with cloud providers to scale adoption in mid-market segments.

Regulatory automation pressure intensifying globally Compliance-driven automation adoption has risen by 41% in banking and healthcare sectors, particularly across the EU where digital audit mandates have increased reporting efficiency by 36%. Cross-border data governance rules are pushing enterprises to restructure workflows, reducing compliance processing delays by 29%. Organizations are investing in automated audit trails and regulatory workflow engines to ensure real-time compliance monitoring, especially in multinational financial operations.

Hyperintegration across enterprise systems expanding System integration demands have increased by 47%, with 42% of enterprises shifting toward API-first automation architectures. In South Korea and Germany, smart factory ecosystems report a 34% improvement in cross-platform process synchronization. This is reducing operational fragmentation and improving real-time decision-making speed by 26%. Companies are responding by adopting unified orchestration platforms and expanding strategic partnerships with cloud hyperscalers to ensure scalable integration across distributed systems.

Workflow automation dominates the market due to its ability to streamline end-to-end enterprise operations, with adoption levels reaching nearly 48% across large organizations. Its scalability and integration strength enable 42% faster process execution compared to task-level automation tools. Integration automation follows closely, especially in hybrid IT environments, growing rapidly as 36% of enterprises modernize legacy systems. Robotic process automation remains widely used in repetitive workflows, contributing to nearly 31% efficiency gains in administrative functions, while decision automation is emerging in analytics-heavy industries such as BFSI and telecom. The fastest-growing segment is integration automation, driven by API-first architectures and cloud migration, expanding adoption by nearly 39% in enterprises modernizing fragmented systems. Companies are prioritizing workflow and integration convergence to reduce operational silos and improve real-time visibility. Vendors are responding with unified automation platforms combining RPA, AI, and orchestration layers, with enterprise deployments increasingly shifting toward scalable multi-process automation ecosystems.

IT operations remain the leading application segment, accounting for nearly 46% of automation deployments due to high infrastructure dependency and demand for real-time system monitoring. Business process optimization follows closely, delivering up to 38% improvement in operational efficiency across BFSI and manufacturing workflows. Customer service automation is expanding rapidly as enterprises reduce service resolution time by 33% through AI-enabled workflows, while HR and finance automation are gaining traction in mid-sized enterprises. The fastest-growing application is customer experience automation, driven by increasing demand for personalized digital interactions and reducing response time by nearly 41% across service industries. Companies are scaling chatbot-driven workflows and omnichannel automation systems to improve engagement efficiency. Enterprises in the U.S. and India are leading deployment expansion, particularly in telecom and e-commerce ecosystems where automation is becoming central to operational competitiveness.

Large enterprises remain the dominant end-user group, accounting for nearly 53% of total deployments due to complex operational structures and multi-system integration requirements. BFSI and manufacturing firms lead adoption intensity, achieving up to 35% improvement in process efficiency through large-scale automation ecosystems. SMEs represent a rapidly growing segment, expanding adoption by nearly 42% as low-code platforms reduce technical barriers and deployment costs. Government and public sector organizations are increasingly digitizing workflows, improving administrative processing speed by 28%. The fastest-growing end-user segment is SMEs, driven by cloud-based subscription models and modular automation platforms that reduce upfront investment constraints. Companies are targeting this segment with flexible pricing, managed services, and plug-and-play automation solutions. Large vendors are forming partnerships with regional IT service providers to expand SME penetration, particularly in India and Southeast Asia where digital infrastructure expansion is accelerating enterprise modernization.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 16% between 2026 and 2033.

North America remains the dominant hub for Digital Process Automation, driven by advanced cloud infrastructure, early AI adoption, and strong enterprise digitization across BFSI, healthcare, and IT services. The region contributes 38% share, supported by high-density deployment of workflow orchestration platforms and rapid integration of AI copilots into enterprise systems. Nearly 41% of Fortune 500 firms in the U.S. have embedded end-to-end automation layers across core operations, improving process efficiency by 33%. Strategic partnerships between hyperscalers and automation vendors are accelerating platform consolidation and reducing deployment fragmentation.

United States Market Outlook: The U.S. leads regional automation maturity with extensive enterprise-scale deployments across banking, insurance, and technology sectors. Over 45% of large enterprises have adopted AI-driven process orchestration tools, while federal digital modernization programs have accelerated cloud migration across public systems. Industrial automation investments in 2025 exceeded USD 60 billion, with measurable productivity improvements of 28% in automated workflows across Fortune 100 firms.

Europe holds a strong position in Digital Process Automation, supported by stringent regulatory frameworks, industrial modernization, and rising demand for compliance-driven digital workflows. The region accounts for 26% share, with strong adoption in Germany, France, and the UK. Nearly 44% of enterprises in the EU have implemented structured automation frameworks to comply with digital audit and data governance requirements. Manufacturing digitization under Industry 4.0 has improved production efficiency by 29%, while cross-border digital compliance systems are reshaping enterprise operations. Vendors are focusing on localized compliance-ready automation platforms to support fragmented regulatory landscapes.

Germany Market Outlook: Germany remains the industrial backbone of Europe’s automation ecosystem, with over 48% of manufacturing enterprises deploying process automation in production and supply chain operations. Smart factory initiatives have improved operational efficiency by 31%, particularly in automotive and engineering clusters. Germany’s strong engineering ecosystem and regulatory alignment with EU digital standards continue to attract major automation investments from global technology providers.

Asia-Pacific is emerging as the fastest-growing region, driven by rapid industrial digitization, expanding cloud infrastructure, and strong government-backed digital transformation programs. The region holds 29% share, led by China, India, and Japan. Nearly 52% of enterprises in Asia-Pacific are adopting low-code and AI-based automation tools to streamline operations. Manufacturing hubs in China report 36% improvement in process efficiency through intelligent automation, while India’s IT services sector is scaling global automation delivery capabilities. Vendors are investing heavily in regional data centers and localized automation ecosystems.

China Market Outlook: China dominates regional automation scale with strong adoption across manufacturing and smart industrial clusters. Over 54% of large industrial enterprises have integrated AI-powered process automation into production systems. Industrial IoT integration across major provinces has improved operational efficiency by 32%, supported by state-driven smart manufacturing initiatives and heavy investment in digital infrastructure.

South America is witnessing steady adoption of Digital Process Automation, driven by banking modernization, telecom expansion, and gradual enterprise cloud migration. The region accounts for 4% share, with Brazil and Chile leading deployment activity. Nearly 39% of large financial institutions have adopted workflow automation to improve transaction processing efficiency by 27%. Infrastructure limitations still constrain large-scale deployment, but increasing cloud penetration is accelerating mid-market adoption. Vendors are focusing on SaaS-based automation models to overcome legacy system constraints and reduce implementation complexity.

Brazil Market Outlook: Brazil leads regional adoption with strong penetration in banking, retail, and telecom sectors. Over 42% of large enterprises have implemented process automation tools to streamline compliance and customer operations. Digital banking expansion has improved transaction efficiency by 25%, supported by rising fintech investments and cloud infrastructure growth across major urban hubs.

Middle East & Africa is experiencing accelerating adoption of Digital Process Automation, driven by government-led digital transformation programs and rising enterprise modernization initiatives. The region holds 3% share, with strong momentum in the UAE, Saudi Arabia, and South Africa. Nearly 46% of public sector organizations are deploying automation tools to enhance administrative efficiency by 30%. Smart city initiatives and national digital strategies are driving cloud adoption and workflow digitization across key industries such as oil & gas, banking, and logistics.

United Arab Emirates Market Outlook: The UAE leads regional automation maturity with strong investments in AI-driven governance and smart infrastructure. Over 55% of government services are now digitally automated, improving service delivery efficiency by 34%. National AI strategies and large-scale cloud partnerships are positioning the UAE as a regional hub for enterprise automation innovation and digital infrastructure development.

Global Digital Process Automation is dominated by platform-led competition where UiPath, Microsoft, IBM, Automation Anywhere, Appian, and ServiceNow compete for enterprise orchestration leadership, while niche workflow vendors target cost-sensitive and vertical-specific deployments. The top 5 players collectively hold ~40% share, with Microsoft alone accounting for over 52% share influence in broader workflow ecosystems due to bundling within enterprise software stacks. Competition is primarily platform vs ecosystem vs enterprise suite integration, where UiPath and Automation Anywhere lead pure-play automation, Microsoft dominates ecosystem-driven adoption, and IBM and Appian focus on regulated enterprise workflows. Key competitive levers include technology depth (35%), integration capability (28%), and deployment speed (22%), with pricing pressure concentrated in mid-market solutions. Companies are expanding through AI agent integration, acquisitions, and hyperscaler partnerships, while vertical integration across ERP, CRM, and cloud stacks is intensifying. The market is shifting toward consolidated automation ecosystems rather than standalone tools, increasing competitive pressure on smaller vendors. Entry barriers remain high due to enterprise switching costs, compliance requirements, and deep integration dependency. Winning requires scalable AI-native platforms with strong ecosystem lock-in and rapid enterprise deployment capability.

Microsoft

IBM

Automation Anywhere

Appian

ServiceNow

SAP

Oracle

Pegasystems

Nintex

Workato

Blue Prism

OpenText

Digital Process Automation is increasingly built on AI-native orchestration layers where agentic AI, process mining, and low-code automation platforms are converging into unified enterprise systems. AI-driven workflow engines improve decision accuracy by nearly 38%, while process mining tools reduce workflow inefficiencies by around 29%, enabling enterprises to redesign operations rather than simply automate them. Around 55% of large enterprises are now integrating automation directly into ERP and CRM ecosystems, replacing traditional rule-based systems.

Emerging technologies such as agentic automation, generative AI workflow builders, and event-driven architecture are reshaping enterprise execution models. Compared to legacy RPA systems, AI-integrated platforms deliver up to 42% higher process adaptability and reduce manual intervention by nearly 35%, shifting competition toward intelligence-led automation rather than task replication. This particularly benefits cloud-first enterprises in the U.S. and India, where scalability and API-based integration are critical.

By 2026–2028, digital process automation will transition toward fully autonomous enterprise systems where workflows self-adjust based on predictive analytics. Over 60% of deployments are expected to adopt hybrid AI-human orchestration models, enabling continuous optimization. Companies investing early in AI-native platforms gain stronger operational resilience, faster deployment cycles, and long-term ecosystem lock-in advantages.

June 2026 – UiPath: Introduced Maestro Case for dynamic enterprise process orchestration, enhancing exception-heavy workflow handling and improving end-to-end process visibility by ~40% across enterprise deployments; strengthens shift toward agentic automation in regulated industries such as BFSI and telecom, enabling faster case resolution and reduced manual intervention; Source: www.uipath.com

June 2026 – UiPath: One NZ deployed UiPath automation to accelerate telco provisioning workflows, reducing mobile service activation time from days to minutes with ~85% cycle-time reduction, improving customer onboarding efficiency and supporting large-scale telecom digital transformation.

May 2026 – UiPath: Launched Automation Suite on-premises agentic AI capabilities for public sector organizations, enabling secure deployment across hybrid cloud environments and improving process automation efficiency by ~30% while ensuring data sovereignty compliance for government workloads.

March 2026 – UiPath: Expanded collaboration with Microsoft to enhance secure automated workflows across Microsoft Defender and Sentinel ecosystems, improving incident response and operational efficiency by ~35%, strengthening cybersecurity-driven automation adoption in enterprise SOC environments.

The Digital Process Automation Market Report covers a comprehensive evaluation of automation technologies, including workflow automation, integration automation, robotic process automation, and decision automation across enterprise ecosystems. It analyzes deployment trends across BFSI, healthcare, manufacturing, telecom, and government sectors, highlighting adoption patterns and operational transformation across digital enterprises. The report also evaluates technology shifts such as AI orchestration, low-code platforms, and process mining solutions influencing automation efficiency and scalability.

The study spans major global regions, including North America, Europe, Asia-Pacific, South America, and Middle East & Africa, assessing enterprise penetration levels, infrastructure readiness, and digital transformation maturity. It provides insights into competitive positioning, ecosystem strategies, and investment flows shaping the 2026–2033 outlook. With detailed segmentation and enterprise adoption patterns, the report supports strategic planning, market entry decisions, and long-term technology investment prioritization for stakeholders across the digital automation value chain.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 160.0 Million |

| Market Revenue (2033) | USD 456.4 Million |

| CAGR (2026–2033) | 14% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | UiPath; Microsoft; IBM; Automation Anywhere; Appian; ServiceNow; SAP; Oracle; Pegasystems; Nintex; Workato; Blue Prism; OpenText |

| Customization & Pricing | Available on Request (10% Customization Free) |