Reports

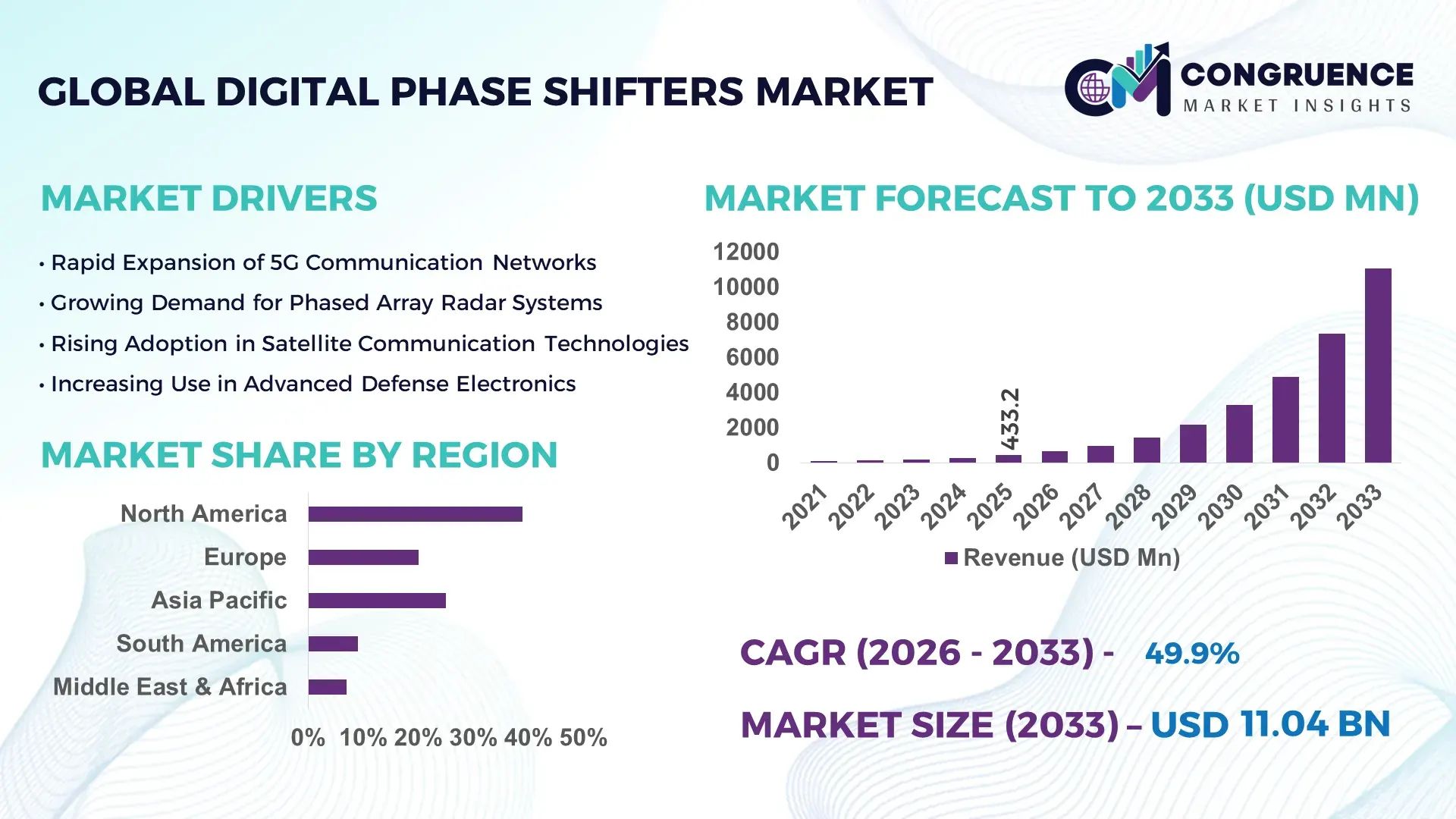

The Global Digital Phase Shifters Market was valued at USD 433.22 Million in 2025 and is anticipated to reach a value of USD 11043.92 Million by 2033 expanding at a CAGR of 49.9% between 2026 and 2033. This rapid expansion is primarily driven by rising deployment of advanced radar, satellite communication systems, and 5G infrastructure requiring precise phase control and signal integrity.

The United States represents the most dominant national ecosystem in the Digital Phase Shifters market due to its large-scale semiconductor fabrication capabilities and strong defense electronics investments. The country hosts more than 35 major RF semiconductor manufacturing facilities supporting phased-array radar, satellite payloads, and 5G base station development. Over 60% of advanced AESA radar systems deployed globally incorporate digital phase shifter architectures designed or manufactured by U.S.-based technology firms. Defense modernization programs allocate billions annually toward next-generation radar and electronic warfare platforms, accelerating adoption of GaN-based RF components. Additionally, approximately 48% of domestic telecom infrastructure upgrades integrating millimeter-wave technologies rely on digitally controlled phase shifting modules for beamforming applications in 5G and emerging 6G trials.

Market Size & Growth: The Digital Phase Shifters Market was valued at USD 433.22 Million in 2025 and is projected to reach USD 11043.92 Million by 2033, expanding at a CAGR of 49.9%, primarily driven by large-scale adoption of phased-array radar and high-frequency communication systems.

Top Growth Drivers: 5G infrastructure expansion (62% adoption growth), defense radar modernization programs (55% increase in advanced radar deployment), and satellite communication bandwidth optimization (47% efficiency improvement).

Short-Term Forecast: By 2028, digital beamforming technologies are expected to improve signal steering precision by 38% while reducing RF system calibration costs by nearly 25%.

Emerging Technologies: Gallium Nitride (GaN) RF semiconductors, integrated RFIC digital phase control chips, and AI-assisted beamforming algorithms.

Regional Leaders: North America projected to reach USD 4.8 Billion by 2033 driven by defense programs; Asia-Pacific estimated at USD 3.7 Billion due to telecom infrastructure expansion; Europe forecast to reach USD 1.9 Billion supported by aerospace radar upgrades.

Consumer/End-User Trends: Aerospace and defense sectors account for nearly 45% of high-frequency phase control deployments, while telecom infrastructure contributes approximately 35% through 5G beamforming equipment integration.

Pilot or Case Example: In 2024, a phased-array radar modernization program implemented digital beam steering modules achieving 32% improved target detection accuracy and 21% reduction in signal interference.

Competitive Landscape: Market leader holds approximately 28% share, followed by Analog Devices, Qorvo, MACOM Technology Solutions, and Mini-Circuits.

Regulatory & ESG Impact: Governments are promoting energy-efficient RF semiconductor manufacturing processes targeting 20–25% reduction in power consumption for telecom infrastructure components.

Investment & Funding Patterns: Over USD 2.6 Billion has been invested globally in RF semiconductor fabrication expansion and next-generation radar electronics development between 2023 and 2025.

Innovation & Future Outlook: Integration of AI-driven beamforming, high-frequency mmWave architectures, and compact RFIC digital phase control modules is reshaping signal processing efficiency and system miniaturization.

Digital Phase Shifters technology plays a critical role across aerospace, defense, telecommunications, and satellite communication industries. Aerospace and defense applications contribute nearly 45% of component demand, primarily for active electronically scanned array (AESA) radar systems and electronic warfare platforms. Telecommunications accounts for roughly 35% of usage through beamforming technologies deployed in 5G millimeter-wave base stations. Rapid innovation in GaN semiconductor materials, RFIC integration, and digitally programmable phase control circuits is enabling compact, high-frequency modules supporting frequencies above 30 GHz. Additionally, increasing satellite constellations and next-generation communication networks are accelerating global consumption of advanced phase control components, positioning the Digital Phase Shifters market for strong technological evolution and infrastructure-driven demand.

The Digital Phase Shifters Market has become strategically essential for high-frequency communication, radar modernization, and advanced electronic warfare systems. The technology enables precise signal beam steering in phased-array antennas, improving detection accuracy and communication reliability. Integrated GaN-based digital phase shifting modules deliver nearly 40% higher power efficiency compared to traditional analog phase shifters, making them increasingly preferred in aerospace radar and 5G base station architectures. Asia-Pacific dominates in production volume due to strong semiconductor fabrication ecosystems, while North America leads in adoption with nearly 58% of defense and aerospace enterprises integrating digitally controlled RF phase technologies into advanced radar platforms. Telecom operators deploying millimeter-wave networks are increasingly integrating digital beamforming chips capable of supporting frequencies above 28 GHz.

By 2028, AI-assisted beamforming optimization algorithms are expected to improve signal direction accuracy by 35% while reducing interference by nearly 30% in dense urban communication networks. At the same time, RF semiconductor manufacturers are committing to ESG targets such as 20% energy reduction in fabrication facilities by 2030 through improved wafer processing efficiency. In 2024, a U.S.-based defense electronics initiative achieved 31% improvement in radar target resolution through AI-assisted digital phase control technology integrated into phased-array antenna systems. As global communication and defense systems grow increasingly complex, the Digital Phase Shifters Market is emerging as a critical pillar supporting resilient, energy-efficient, and scalable RF signal processing infrastructure.

The Digital Phase Shifters Market is influenced by rapid expansion in phased-array radar systems, high-frequency communication networks, and satellite-based connectivity infrastructure. Growing demand for millimeter-wave communication technologies and electronically steered antennas is driving adoption across aerospace, defense, and telecommunications sectors. Advances in RF semiconductor materials such as gallium nitride and silicon germanium are enabling compact phase control modules capable of operating above 30 GHz. Defense modernization initiatives across multiple countries are accelerating procurement of advanced radar platforms incorporating digital beamforming technologies. At the same time, large-scale rollout of 5G and future 6G infrastructure is increasing the need for digitally programmable RF components that support high-speed data transmission, low signal distortion, and efficient directional signal control in dense network environments.

Phased-array radar technology relies heavily on digitally controlled phase shifters to steer antenna beams electronically without mechanical movement. Global defense modernization programs have accelerated deployment of active electronically scanned array (AESA) radar platforms, with more than 70% of newly developed military radar systems integrating digital beamforming architectures. These systems improve detection precision by nearly 30% while enabling faster target tracking capabilities. Aerospace and naval defense platforms increasingly deploy multi-element antenna arrays requiring hundreds of phase control modules per radar system. Additionally, satellite communication payloads and high-frequency telecom networks require accurate signal phase alignment for stable transmission, significantly increasing demand for programmable RF phase shifting devices across multiple high-technology sectors.

Digital phase shifters rely on advanced RF semiconductor fabrication processes that require high-precision lithography and specialized materials such as gallium nitride and silicon germanium. Manufacturing these components involves complex wafer processing and high testing costs due to the need for precise phase accuracy at frequencies exceeding 20–30 GHz. Semiconductor fabrication facilities capable of producing such high-frequency RFIC components represent less than 15% of global chip manufacturing capacity. Additionally, stringent performance validation and reliability testing required for aerospace and defense applications extend product development cycles. These technical barriers increase production costs and limit rapid scalability, particularly for smaller manufacturers attempting to enter the high-frequency RF semiconductor market.

The global rollout of 5G millimeter-wave communication networks and early development of 6G technologies are creating significant opportunities for digital phase shifter manufacturers. Beamforming antennas used in 5G base stations rely on digitally programmable phase shifting modules to direct high-frequency signals toward users, improving network efficiency. Telecommunications infrastructure deployments supporting frequencies above 28 GHz require precise signal phase control to maintain low latency and high data throughput. Industry projections indicate that future 6G communication architectures could incorporate antenna arrays containing hundreds of digitally controlled RF elements per base station. This growing infrastructure requirement is expanding the potential market for high-frequency RFIC phase shifting devices across telecom, satellite broadband, and next-generation wireless connectivity applications.

As communication systems move toward higher frequencies and larger phased-array antenna architectures, integrating hundreds of digital phase shifter modules into compact RF systems presents significant engineering challenges. High-density RF circuits generate substantial heat, particularly in applications operating above 30 GHz. Thermal management limitations can reduce component lifespan and affect signal stability. Additionally, maintaining accurate phase alignment across large antenna arrays requires extremely precise calibration and synchronization algorithms. Complex system integration and heat dissipation requirements increase engineering costs and extend design timelines for aerospace radar platforms and high-performance telecom equipment, creating technical barriers for large-scale deployment of advanced digital phase shifting technologies.

• Accelerated Integration of Digital Beamforming in 5G and Millimeter-Wave Networks: Telecommunications operators are rapidly deploying digital beamforming technologies to support high-frequency wireless communication. Nearly 62% of new 5G base stations operating in millimeter-wave bands incorporate digital phase shifters to enable precise beam steering and improved signal coverage. Networks operating above 28 GHz require phase control accuracy within ±5 degrees to maintain stable connections. Telecom equipment manufacturers have increased phased-array antenna integration by more than 45% since 2022, enabling higher data transmission speeds and reducing signal interference in dense urban environments where device connectivity density exceeds 1 million devices per square kilometer.

• Rising Adoption of Gallium Nitride (GaN) RF Semiconductor Technology: GaN-based digital phase shifters are gaining rapid traction due to their superior thermal performance and high-frequency capabilities. Approximately 48% of newly developed RF integrated circuits used in radar and communication systems now utilize GaN technology, compared with less than 30% five years ago. GaN components can operate at power densities exceeding 5 W/mm, enabling radar systems to extend detection ranges by nearly 35%. Aerospace and defense manufacturers are increasingly transitioning from silicon-based RF components to GaN architectures to support next-generation radar platforms operating above 30 GHz.

• Expansion of Satellite Communication Constellations Driving Phase Control Demand: The growth of low Earth orbit satellite constellations is significantly increasing demand for digitally controlled RF phase shifting modules. Modern satellite payloads integrate phased-array antennas containing more than 200 phase control elements to ensure precise signal alignment with ground stations. Over 8,500 satellites are currently operational worldwide, with nearly 65% utilizing advanced beam-steering technologies. Digital phase shifters allow satellites to dynamically adjust communication beams, improving bandwidth efficiency by up to 40% and enabling multi-user connectivity across large geographic regions.

• Increased Deployment in Advanced Radar and Electronic Warfare Systems: Defense modernization programs worldwide are accelerating adoption of digitally controlled phase shifters in active electronically scanned array radar platforms. Modern fighter aircraft radar systems incorporate up to 1,500 antenna elements, each requiring individual phase control for accurate beam steering. Radar detection precision has improved by nearly 30% through digital phase control architectures compared to legacy mechanical scanning systems. Electronic warfare platforms also rely on programmable phase shifting modules to manipulate RF signals and counter hostile radar systems, with more than 70% of newly developed military radar platforms integrating digital beamforming technology.

The Digital Phase Shifters market segmentation highlights significant variation across product types, application areas, and end-user industries. Type-based segmentation includes 4-bit, 5-bit, 6-bit, and higher-bit digital phase shifters used in RF signal control and beamforming systems. Higher-bit phase shifters offer improved resolution and precision, supporting high-frequency radar and communication technologies. Application segmentation is primarily driven by radar systems, satellite communication, and telecom infrastructure, where beam steering and signal alignment are critical for performance. From an end-user perspective, aerospace and defense industries dominate demand due to extensive deployment of phased-array radar platforms. Telecommunications providers represent another major consumer group as global 5G infrastructure expansion requires digitally controlled RF components for efficient signal direction and network capacity optimization.

Digital phase shifters are categorized by bit resolution, including 4-bit, 5-bit, 6-bit, 7-bit, and higher-bit configurations used in RF beamforming systems. Among these, 6-bit digital phase shifters currently represent the leading segment with approximately 38% adoption across radar and advanced communication platforms. These devices provide phase resolution close to 5.6 degrees per step, enabling accurate beam steering in phased-array antennas used in radar and satellite communication systems. In comparison, 4-bit phase shifters account for roughly 24% of installations due to their lower complexity and cost advantages in commercial communication equipment. Meanwhile, 5-bit variants contribute nearly 21% of deployments, particularly in mid-frequency radar and telecom infrastructure applications where moderate phase precision is sufficient.

The fastest-growing category is higher-bit digital phase shifters, particularly 7-bit and 8-bit architectures, which are expanding at an estimated growth rate of nearly 12% annually due to rising demand for ultra-precise beamforming in next-generation radar and satellite payloads. These devices offer phase accuracy below 3 degrees, improving signal steering performance and reducing beam distortion. The remaining segments collectively represent about 17% of the market and typically serve specialized electronic warfare and experimental communication systems requiring custom RF configurations.

Digital phase shifters are widely used across several high-frequency communication and sensing applications including radar systems, satellite communication, telecommunications infrastructure, and electronic warfare technologies. Radar applications currently dominate the market with nearly 44% adoption due to widespread deployment of active electronically scanned array radar platforms in military aircraft, naval systems, and ground-based surveillance networks. Satellite communication systems represent around 28% of total usage, where digital phase shifters enable phased-array antennas to dynamically direct signals toward ground stations and optimize bandwidth allocation. Telecommunications infrastructure represents another rapidly expanding application segment, accounting for approximately 20% of current installations. Digital beamforming technology enables telecom operators to direct millimeter-wave signals toward individual users, improving network capacity and reducing interference in dense urban areas. This segment is also the fastest-growing application area with an estimated growth rate of nearly 14% annually as telecom providers accelerate deployment of advanced 5G base stations and begin research on 6G wireless communication architectures.

Other specialized applications, including electronic warfare platforms and research-based communication systems, collectively account for nearly 8% of demand. These systems require highly programmable RF phase control modules capable of rapidly adjusting signal direction during defense or scientific operations.

The Digital Phase Shifters market serves several major end-user industries including aerospace and defense, telecommunications providers, satellite operators, and research institutions. Aerospace and defense organizations represent the largest end-user segment with approximately 46% adoption due to extensive use of phased-array radar, missile guidance systems, and electronic warfare platforms. These applications require precise phase control across hundreds or thousands of antenna elements, making digital phase shifters essential for accurate signal steering and threat detection capabilities. Telecommunications companies account for nearly 30% of end-user demand as global 5G network expansion accelerates the deployment of digitally controlled beamforming antennas in base stations. Satellite communication providers represent around 15% of market demand, particularly in low Earth orbit satellite constellations where phased-array antennas require advanced phase control technologies to maintain dynamic signal alignment with ground terminals.

The fastest-growing end-user segment is telecommunications infrastructure, expanding at an estimated annual rate of approximately 15% due to increasing mobile data traffic and demand for high-frequency millimeter-wave connectivity. Research institutions, government laboratories, and semiconductor testing organizations collectively represent the remaining 9% of market participation, primarily supporting innovation in RF semiconductor and radar technologies.

Region North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 12.8% between 2026 and 2033.

North America maintains strong adoption due to large-scale aerospace and defense procurement programs integrating phased-array radar systems containing more than 1,000 antenna elements per platform. Europe accounts for approximately 26% of global demand supported by defense modernization initiatives and satellite communication expansion. Asia-Pacific contributes nearly 29% of market activity, driven by semiconductor manufacturing hubs and telecom infrastructure deployment exceeding 1.5 million 5G base stations across key economies. South America represents about 4% of installations, while Middle East & Africa holds close to 3%, primarily supported by radar modernization and satellite communication infrastructure expansion.

What factors are accelerating adoption of advanced RF beamforming technologies across defense and telecom systems?

North America represents approximately 38% of global Digital Phase Shifters installations, driven primarily by aerospace, defense electronics, and advanced telecommunications infrastructure. The United States leads regional demand with over 70% of radar modernization projects incorporating phased-array antenna architectures. Government initiatives supporting defense electronics manufacturing and semiconductor innovation have increased funding allocations exceeding 15% annually for next-generation radar technologies. Rapid deployment of millimeter-wave telecom infrastructure has resulted in more than 180,000 high-frequency base stations integrating digital beamforming components. A regional semiconductor manufacturer recently introduced a digitally programmable RF phase control chip capable of supporting frequencies above 40 GHz. Enterprise adoption trends also reflect higher investment in aerospace and telecommunications technology modernization compared with other global regions.

How are advanced radar programs and telecom upgrades transforming RF signal control technologies?

Europe accounts for approximately 26% of global Digital Phase Shifters demand, with Germany, the United Kingdom, and France representing the largest technology adoption centers. Defense modernization programs across these countries are accelerating phased-array radar deployments, particularly in naval and air defense systems containing more than 800 antenna elements per platform. Regulatory agencies across the region are promoting energy-efficient semiconductor manufacturing and high-performance communication infrastructure to support advanced satellite networks. Telecom operators are integrating digital beamforming solutions in more than 120,000 upgraded 5G base stations across major European markets. A regional RF semiconductor manufacturer recently launched a high-frequency phase control module designed for radar systems operating above 32 GHz. Consumer adoption patterns also reflect strong regulatory-driven demand for high-performance, energy-efficient communication infrastructure technologies.

What technological shifts are driving high-volume production of RF beam steering components?

Asia-Pacific represents approximately 29% of the Digital Phase Shifters market and ranks among the fastest expanding technology ecosystems due to strong semiconductor manufacturing and telecom infrastructure expansion. China, Japan, and India collectively account for more than 65% of regional demand, supported by large-scale 5G deployments exceeding 1.5 million base stations. Semiconductor fabrication facilities across the region produce nearly 45% of global RF integrated circuits used in radar and communication systems. Innovation hubs in Japan and South Korea are accelerating development of high-frequency beamforming technologies operating above 28 GHz. A leading regional semiconductor manufacturer recently introduced a compact digital phase control chipset supporting phased-array antennas with more than 256 elements. Technology adoption trends show strong demand from telecom operators and satellite communication providers deploying advanced wireless infrastructure.

How are telecom upgrades and satellite connectivity programs shaping advanced RF component demand?

South America accounts for nearly 4% of global Digital Phase Shifters installations, with Brazil and Argentina representing the largest regional technology markets. Telecommunications infrastructure modernization programs have expanded high-frequency network deployment across more than 30 metropolitan areas, increasing demand for digitally controlled beamforming systems. Satellite communication systems supporting remote connectivity across rural regions require phased-array antennas capable of dynamic signal steering. Regional trade policies promoting electronics manufacturing are encouraging semiconductor assembly facilities to expand RF component production. A regional telecommunications equipment provider recently deployed beamforming antennas incorporating over 120 digital phase control elements across urban network towers. Consumer adoption patterns highlight increasing reliance on mobile connectivity and satellite-based communication services for remote and underserved locations.

How are defense modernization and communication infrastructure upgrades increasing demand for RF beamforming systems?

Middle East & Africa collectively account for approximately 3% of the Digital Phase Shifters market, driven by defense modernization initiatives and satellite communication infrastructure expansion. Countries such as the United Arab Emirates and South Africa are investing heavily in radar surveillance systems integrating phased-array antennas containing more than 600 digitally controlled elements. Telecommunications operators across the Gulf region are expanding 5G coverage with more than 45,000 upgraded network towers requiring beamforming technologies. Government policies encouraging high-technology infrastructure investment have accelerated demand for advanced RF electronics. A regional technology provider recently collaborated with satellite communication operators to deploy phased-array ground stations incorporating programmable digital phase shifting modules to support high-capacity broadband connectivity across remote regions.

United States – 34% Digital Phase Shifters market share, supported by strong aerospace and defense electronics manufacturing capacity and large-scale radar modernization programs.

China – 21% Digital Phase Shifters market share, driven by rapid telecom infrastructure expansion and extensive semiconductor fabrication capabilities supporting RF communication technologies.

The Digital Phase Shifters market is moderately consolidated with approximately 45 active technology providers competing across RF semiconductor manufacturing, defense electronics integration, and telecommunications equipment production. The top five companies collectively account for nearly 52% of global market participation due to their advanced semiconductor fabrication capabilities and extensive defense industry partnerships. These firms focus heavily on developing high-frequency phase control modules capable of operating above 30 GHz to support next-generation radar and millimeter-wave communication systems.

Strategic initiatives in this market include aggressive investment in RF integrated circuit innovation, partnerships with aerospace defense contractors, and expansion of semiconductor fabrication capacity. Over the past three years, more than 30 new product launches have been introduced focusing on compact digital phase shifter architectures designed for phased-array antennas containing over 256 signal channels. Several companies have also formed joint development agreements with telecom infrastructure providers to support advanced beamforming technologies used in high-density 5G networks.

Innovation competition is also intensifying in the development of GaN-based RF semiconductors capable of improving thermal performance and signal efficiency by nearly 40% compared to legacy silicon technologies. Companies are increasingly integrating programmable digital phase control features directly into RFIC designs to reduce system complexity and improve beam steering accuracy. These technological advancements, combined with rising defense and telecommunications demand, continue to reshape competitive positioning across the global Digital Phase Shifters market.

Analog Devices

Qorvo

MACOM Technology Solutions

Mini-Circuits

Renesas Electronics

Skyworks Solutions

Infineon Technologies

NXP Semiconductors

Texas Instruments

Broadcom

Murata Manufacturing

Teledyne Technologies

Technological advancement in the Digital Phase Shifters market is closely linked to rapid progress in RF semiconductor materials, integrated circuit design, and phased-array antenna architectures. Gallium Nitride (GaN) and Silicon Germanium (SiGe) technologies are increasingly replacing traditional silicon-based RF components due to their higher power density and frequency capability. GaN-based phase shifter modules can operate above 40 GHz while maintaining power densities exceeding 5 W/mm, enabling longer radar detection ranges and higher signal integrity in high-frequency communication systems.

Another major innovation involves highly integrated RFIC-based digital phase shifters capable of controlling up to 256 antenna elements within a single phased-array module. These compact architectures significantly reduce system size and energy consumption in advanced radar and 5G infrastructure equipment. Modern beamforming antenna systems deployed in telecommunications infrastructure can contain between 64 and 512 antenna elements, each requiring digitally programmable phase control to optimize signal direction and network capacity.

Advancements in millimeter-wave technologies operating between 24 GHz and 100 GHz are further expanding the adoption of digital phase shifting modules in next-generation wireless communication platforms. AI-assisted beamforming algorithms are also emerging, enabling real-time signal optimization and interference mitigation. These intelligent RF control technologies can improve signal alignment accuracy by nearly 30%, supporting higher data throughput and enhanced network reliability across aerospace, defense, satellite communication, and telecom infrastructure systems.

• In February 2025, Analog Devices introduced a new wideband digital phase shifter integrated into its RF front-end solutions for phased-array radar and electronic warfare applications. The device supports operation up to 40 GHz and enables precise beam steering in advanced radar systems with improved phase resolution and reduced insertion loss. Source: www.analog.com

• In September 2024, Qorvo expanded its RF semiconductor portfolio with a new high-frequency digital phase shifter designed for 5G millimeter-wave base stations. The component supports multi-channel beamforming architectures used in advanced telecom infrastructure, enabling improved signal direction control and enhanced network capacity in dense urban deployments. Source: www.qorvo.com

• In April 2025, MACOM Technology Solutions launched a new GaN-based digital phase shifter module optimized for phased-array radar platforms used in aerospace and defense applications. The device operates across frequencies up to 30 GHz and supports compact beamforming systems containing hundreds of antenna elements. Source: www.macom.com

• In October 2024, Mini-Circuits released a digitally controlled RF phase shifter designed for laboratory testing, satellite communication equipment, and radar signal calibration applications. The product enables phase adjustment across a wide frequency range and provides precise signal alignment for high-frequency RF system testing environments. Source: www.minicircuits.com

The Digital Phase Shifters Market Report provides a comprehensive analysis of industry dynamics, technology evolution, and global deployment patterns across key sectors including aerospace and defense, telecommunications infrastructure, satellite communication, and electronic warfare systems. The report evaluates multiple product configurations such as 4-bit, 5-bit, 6-bit, and higher-resolution digital phase shifters used in RF beamforming and phased-array antenna architectures.

It covers a broad range of applications including radar systems, satellite communication payloads, high-frequency wireless infrastructure, and signal calibration equipment used in research laboratories and semiconductor testing facilities. Advanced RF technologies such as GaN-based semiconductors, millimeter-wave communication systems operating above 28 GHz, and integrated RFIC phase control modules are also examined as part of the technology landscape.

Geographically, the report analyzes market developments across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting regional production capacity, infrastructure deployment, and technological innovation hubs. The study further explores industry investment trends, strategic collaborations among semiconductor manufacturers and defense contractors, and the growing role of digitally programmable beamforming technologies in modern communication and surveillance systems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

49.9% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Analog Devices, Qorvo, MACOM Technology Solutions, Mini-Circuits, Renesas Electronics, Skyworks Solutions, Infineon Technologies, NXP Semiconductors, Texas Instruments, Broadcom, Murata Manufacturing, Teledyne Technologies |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |