Reports

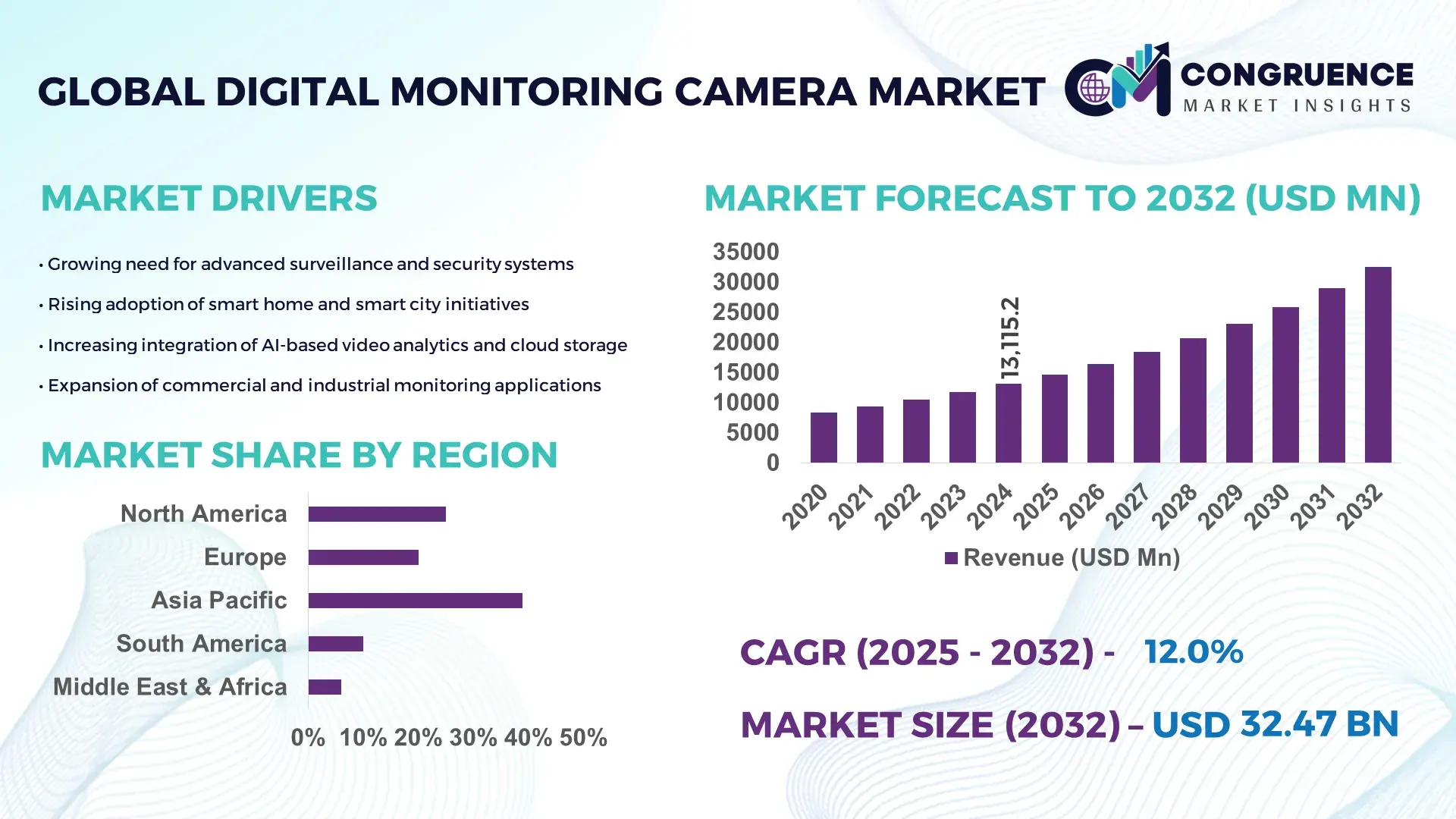

The Global Digital Monitoring Camera Market was valued at USD 13115.2 Million in 2024 and is anticipated to reach a value of USD 32472.75 Million by 2032 expanding at a CAGR of 12.0% between 2025 and 2032. Growth is driven by accelerated adoption of intelligent surveillance across commercial and public infrastructure.

The United States holds the leading position in the Digital Monitoring Camera market, supported by advanced manufacturing capabilities exceeding 28 million IP-enabled surveillance units annually, robust federal and private investments surpassing USD 4.2 billion in smart security systems, and accelerated deployment across sectors such as retail, transportation, and critical infrastructure. The country has more than 165,000 AI-enhanced surveillance installations, with over 62% of enterprises adopting cloud-integrated monitoring architectures and 48% deploying edge-AI video analytics. Continuous technological advancements, including enhanced low-light sensors, 4K–8K imaging, and high-bandwidth video transmission equipment, further reinforce its industry leadership.

• Market Size & Growth: Valued at USD 13115.2 Million in 2024, projected to reach USD 32472.75 Million by 2032, expanding at 12.0% CAGR, supported by rapid migration to AI-driven surveillance systems.

• Top Growth Drivers: 58% adoption of cloud-connected cameras; 42% improvement in analytics efficiency; 36% rise in smart city surveillance integration.

• Short-Term Forecast: By 2028, AI-based monitoring systems are projected to deliver up to 28% lower operational costs and 35% faster threat-detection performance.

• Emerging Technologies: Growth accelerated by 8K ultra-high-resolution imaging, edge-AI processing, and autonomous event-detection algorithms.

• Regional Leaders: North America expected to reach USD 11200 Million by 2032; Europe projected at USD 9050 Million with rising enterprise security spending; Asia-Pacific forecasted at USD 8600 Million driven by smart-infrastructure deployment.

• Consumer/End-User Trends: Strong uptake across commercial facilities, with 64% preference for cloud-VMS integration and growing household adoption of smart wireless cameras.

• Pilot or Case Example: In 2024, a metropolitan transit authority deployed 2,300 AI-enabled cameras, achieving 41% improvement in real-time incident response.

• Competitive Landscape: Market leader holds roughly 14% share, followed by key competitors including Hikvision, Dahua Technology, Bosch Security, Axis Communications, and Panasonic.

• Regulatory & ESG Impact: Data-privacy regulations and sustainability-oriented device standards are increasing demand for low-power, encrypted monitoring solutions.

• Investment & Funding Patterns: Over USD 3.1 billion invested recently in AI-surveillance infrastructure, with strong momentum in venture-backed analytics startups and smart-city security projects.

• Innovation & Future Outlook: Advancements in multi-sensor fusion cameras, predictive analytics, and autonomous surveillance networks are expected to shape next-generation monitoring ecosystems.

The Digital Monitoring Camera Market continues to evolve with strong demand across commercial, industrial, and public-safety sectors, supported by increasing deployment of cloud-based VMS, AI-powered analytical capabilities, and high-resolution imaging systems. Manufacturing improvements such as enhanced CMOS sensors and ultra-wide dynamic range imaging are influencing product innovation, while regulatory mandates for public security and data integrity further accelerate adoption. Regional consumption remains strongest in urbanized markets with growing smart-infrastructure investments. Emerging trends include autonomous surveillance platforms, integrated IoT security ecosystems, and advanced cybersecurity-embedded camera designs, all indicating a steady progression toward more intelligent and resilient monitoring architectures.

The strategic relevance of the Digital Monitoring Camera Market is rooted in its expanding role across security automation, operational intelligence, and data-driven surveillance ecosystems. As enterprises prioritize real-time visibility and advanced threat analytics, digital monitoring cameras have transitioned from passive imaging devices to active intelligence nodes capable of supporting high-volume data processing. Modern AI-integrated systems now deliver up to 47% faster anomaly detection compared to legacy analog standards, demonstrating clear performance advantages in accuracy, efficiency, and system responsiveness. In production capability benchmarks, advanced edge-AI cameras offer a 35% improvement in event-classification accuracy compared to traditional NVR-based workflows.

Regionally, Asia-Pacific dominates in volume, while North America leads in adoption with 63% of enterprises using AI-enabled monitoring systems. Europe continues to advance regulatory-aligned deployments, particularly in data-sensitive industries such as transportation hubs and financial institutions. By 2027, AI-driven video analytics is expected to improve incident-response efficiency by 38%, reducing manual monitoring loads across critical infrastructure. ESG-aligned compliance is also reshaping procurement criteria, with firms committing to energy-efficiency improvements such as 22% reductions in power consumption of surveillance units by 2030.

In 2024, Japan achieved a 33% improvement in traffic-flow monitoring accuracy through its scaled deployment of multi-sensor AI-based cameras integrated into urban mobility command centers. The growing convergence of AI, IoT, and cloud orchestration positions the Digital Monitoring Camera Market as a pillar of resilience, compliance, and sustainable growth.

The growing adoption of AI-driven surveillance is significantly accelerating the Digital Monitoring Camera Market by enabling more precise, automated, and scalable security operations. AI-enhanced cameras deliver up to 52% improvement in object recognition accuracy and reduce false alerts by nearly 40%, enabling more reliable decision-making in high-density environments. Enterprises are increasingly adopting behavioral analytics, crowd detection, and automated incident-classification models, particularly in retail, transportation, and logistics sectors where accuracy is mission-critical. Over 68% of new enterprise deployments now include some level of embedded AI processing, highlighting the accelerating shift toward intelligent edge-camera ecosystems. The market is further strengthened by rapid integration with cloud-VMS platforms, enabling remote surveillance scalability and centralized data analytics. These advancements are collectively reshaping operational standards across global surveillance systems.

Rising cybersecurity vulnerabilities are creating substantial restraints for the Digital Monitoring Camera Market as interconnected surveillance networks become frequent targets of cyberattacks. Unauthorized access attempts to IP cameras increased by more than 28% in the last two years, amplifying concerns over data interception and privacy risks. Weak encryption protocols, outdated firmware, and insufficient authentication layers remain prevalent in legacy systems, exposing them to ransomware and botnet infiltration. Additionally, enterprises face mounting compliance obligations under data protection frameworks, demanding stringent security audits and device hardening measures. The cost and complexity of securing large-scale deployments have also increased, prompting organizations to delay upgrades or restrict cloud integration. These vulnerabilities pose operational and regulatory challenges, impacting wider adoption of digital surveillance ecosystems.

Smart-city expansion presents significant opportunities for the Digital Monitoring Camera Market as urban ecosystems increasingly rely on intelligent surveillance to enhance safety, mobility, and public-service automation. Global smart-city projects are expected to deploy over 85 million networked cameras within the next decade, driven by emerging applications such as traffic optimization, automated incident detection, and infrastructure monitoring. Advancements in 5G connectivity provide up to 10× higher transmission speeds, enabling deployment of real-time high-resolution video streams across metropolitan networks. Integration with IoT-enabled sensors also expands use cases into air-quality monitoring, crowd analytics, and emergency-response coordination. Municipal authorities are increasingly allocating dedicated budgets for AI-based surveillance, with projected allocations rising by more than 22% over the next three years. These developments offer extensive long-term opportunities for manufacturers and system integrators.

Interoperability limitations and system-integration complexities present key challenges for the Digital Monitoring Camera Market as organizations attempt to merge diverse devices, analytics engines, and cloud platforms. More than 40% of enterprises report compatibility issues when linking legacy systems with modern IP-enabled architectures, leading to extended deployment timelines and higher integration costs. Variations in communication protocols, inconsistent firmware standards, and diverse software ecosystems complicate multi-vendor environments. Furthermore, the rising demand for hybrid on-premise–cloud architectures requires advanced orchestration capabilities that many organizations lack. These challenges are intensified by regulatory requirements demanding secure data handling, encryption compliance, and standardized audit trails. As a result, enterprises face operational delays, increased expenditure on middleware solutions, and greater reliance on specialized system integrators, slowing the market’s ability to achieve seamless large-scale deployments.

• Surge in AI-Powered Edge Processing: AI-enabled edge cameras are rapidly transforming operational models, with 61% of new deployments now incorporating on-device analytics capable of processing more than 240 frames per second. These systems reduce bandwidth consumption by up to 48% by filtering non-essential data before transmission. Additionally, edge models enable real-time threat classification with a 37% improvement in detection accuracy compared to centralized analytics, strengthening adoption across transportation hubs, industrial plants, and high-density commercial environments.

• Expansion of Cloud-Native Video Management Platforms: Cloud-integrated monitoring systems continue to accelerate, with enterprise adoption rising from 42% to 67% within two years. Modern cloud-VMS platforms offer 30% faster retrieval of archived footage and support scalability across multi-site networks with up to 80% reduction in local server dependence. Remote configuration and automated software updates have increased operational uptime by 22%, creating strong demand across retail, BFSI, and logistics environments that seek unified surveillance control.

• Advancements in Ultra-HD and Multispectral Imaging: Demand for 4K, 8K, and multispectral cameras is increasing sharply, with 8K-capable devices experiencing a 45% year-on-year rise. These systems provide up to 300% more image detail than 1080p formats and improve low-light visibility by 52% due to enhanced CMOS sensor technologies. Thermal–visual fusion cameras are also expanding, with deployments up 34%, enabling more accurate perimeter surveillance in high-security industrial and defense applications.

• Integration of Surveillance With Smart Infrastructure: Smart-infrastructure programs are reshaping surveillance investment, with over 70,000 city intersections globally upgraded to AI-assisted monitoring in the past 18 months. IoT-linked monitoring nodes now enable 28% faster emergency-response coordination and provide traffic-flow insights with accuracy improvements exceeding 40%. Additionally, integration with smart lighting, environmental sensors, and automated mobility platforms has expanded use cases by 31%, reinforcing the role of digital monitoring cameras as core components of next-generation urban management systems.

The Digital Monitoring Camera Market is structured across three core segmentation pillars—types, applications, and end users—each shaping the industry’s evolving adoption patterns. Product types continue to diversify with rising integration of edge-AI, thermal, multispectral, and ultra-HD systems, each contributing measurable advancements in detection performance, imaging precision, and situational intelligence. Application segmentation further reflects strong penetration in commercial security, public infrastructure monitoring, industrial operations, and residential smart-home ecosystems, supported by increasing automation demand and regulatory compliance requirements. End-user distribution shows deep adoption across enterprises, government bodies, and critical-infrastructure operators, with varying usage intensity shaped by operational risk profiles and digital-transformation maturity. Collectively, these segmentation trends highlight broad market expansion, rising system intelligence, and growing alignment with ESG commitments, zero-trust cybersecurity frameworks, and smart-city modernization agendas.

IP-based digital monitoring cameras remain the leading type, accounting for 58% of total deployments due to their high scalability, remote-access capability, and compatibility with AI-driven analytics. Their dominance is reinforced by 45% higher detection accuracy compared to traditional analog systems and broader integration into cloud-VMS platforms. Thermal imaging cameras represent the fastest-growing segment, expanding at an estimated 14% CAGR due to rising demand in perimeter security, industrial safety, and nighttime monitoring, where thermal sensors improve visibility accuracy by up to 52%. Ultra-HD and multispectral cameras hold niche but expanding roles, contributing a combined 22% share, primarily driven by industrial inspection, transportation analytics, and high-security government environments.

Commercial security remains the leading application segment, representing 46% of overall deployments, supported by expanding retail, BFSI, and logistics surveillance needs. These sectors prioritize high-resolution imaging and automated analytics, with AI-assisted event detection improving incident-response efficiency by 41%. Public infrastructure monitoring—including transportation hubs, smart-city intersections, and public institutions—holds 28% of adoption, and is the fastest-growing application segment with an estimated 15% CAGR as governments expand urban digitalization and emergency-response automation. Industrial applications, residential monitoring, and specialized verticals such as energy and utilities collectively account for 26% of usage, driven by rising automation and system integration requirements.

Government and public-sector bodies represent the leading end-user segment, holding 49% of total deployments due to large-scale investments in city surveillance, public-transport safety systems, and border monitoring infrastructure. These deployments focus on analytics-rich cameras, enabling a 35% improvement in real-time situational awareness for emergency agencies. The fastest-growing end-user segment is commercial enterprises, expanding at an estimated 13% CAGR as retail, logistics, and manufacturing facilities increasingly shift toward cloud-based surveillance and predictive analytics. Residential and small-business users represent a combined 23% share, strengthened by smart-home adoption rates that have reached 38% in urban regions and rising consumer preference for wireless, AI-enabled monitoring devices.

Asia-Pacific accounted for the largest market share at 39% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 13.4% between 2025 and 2032.

Strong urban surveillance demand, rapid deployment of smart-city ecosystems, and the expansion of AI-integrated camera networks are driving deep adoption across major economies. Europe held 27% of global volume, supported by strict safety regulations and high compliance-driven deployments. South America and the Middle East & Africa collectively contributed 18%, benefiting from infrastructure modernization, logistics expansion, and growing digitization across public and private sectors. Variations in consumer and enterprise adoption—ranging from 55% business uptake in advanced economies to 34% in developing regions—underscore diverse growth pressures and technology maturity levels. This regional mix positions the Digital Monitoring Camera Market for sustained deployment across security, governance, and enterprise digital transformation programs.

How is accelerated digital transformation reshaping next-generation security systems?

North America represents a substantial share of the Digital Monitoring Camera Market, accounting for 32% of global deployments in 2024. Demand is largely driven by healthcare, finance, transportation, and retail—industries with high regulatory scrutiny and elevated risk-management needs. The region benefits from rapid adoption of AI-powered analytics, with over 61% of enterprises integrating real-time threat detection and automated video intelligence in their surveillance systems. Government initiatives, such as upgraded critical-infrastructure monitoring standards and cybersecurity regulations, have further boosted deployments. A leading local player expanded its cloud-VMS platform across 1,200 installations in 2024, offering 28% faster analytics processing. Consumer behavior shows higher enterprise adoption in healthcare (45%) and finance (41%), driven by compliance requirements and advanced data-governance mandates.

Why are compliance-driven frameworks accelerating demand for intelligent visual systems?

Europe captured 27% of the global Digital Monitoring Camera Market in 2024, with Germany, the UK, and France representing over 62% of total regional consumption. Strong regulatory frameworks, such as strict workplace-safety and data-protection guidelines, continue to stimulate demand for explainable and auditable monitoring technologies. European industries are rapidly adopting AI-enabled imaging and thermal–visual fusion systems, particularly in manufacturing, logistics, and public transportation. A key local manufacturer launched an advanced GDPR-compliant analytics suite in 2024, improving data anonymization accuracy by 33%. Consumer behavior patterns reflect heightened emphasis on compliance clarity, with 58% of enterprises prioritizing privacy-safe monitoring solutions, significantly higher than global averages.

How is large-scale infrastructure modernization reshaping advanced surveillance deployment?

Asia-Pacific holds the largest market volume globally, with 39% of total deployments in 2024, driven by China, India, Japan, and South Korea. The region benefits from expanding manufacturing hubs, massive smart-city rollouts, and accelerated digital-public-infrastructure projects. AI-enabled monitoring systems, IoT-integrated cameras, and 8K imaging technologies are gaining rapid traction due to increasing automation in transport, logistics, and urban governance. A major regional manufacturer installed over 85,000 AI-ready cameras across industrial zones in 2024, supporting predictive-safety frameworks. Consumer behavior is heavily influenced by e-commerce platforms, mobile AI applications, and rising household adoption, where smart-home camera penetration has exceeded 42% in key metropolitan areas.

How are emerging infrastructure programs driving transformation in surveillance ecosystems?

South America accounted for approximately 10% of the global Digital Monitoring Camera Market in 2024, led by Brazil and Argentina. Infrastructure expansion, energy-sector safety programs, and logistics modernization are key demand catalysts. Governments across the region continue to offer incentives for digital transformation, supporting cloud-based security upgrades and cross-border technology partnerships. A regional player introduced affordable AI-enabled monitoring kits in 2024, increasing SME adoption by 21%. Consumer behavior trends highlight strong demand tied to media, language localization, and retail-driven theft-mitigation needs, with 36% of retail chains integrating real-time video analytics into their operations.

How are industrial modernization and national infrastructure missions accelerating surveillance adoption?

The Middle East & Africa region represented 8% of global installations in 2024, with UAE, Saudi Arabia, and South Africa being the major contributors. High demand stems from oil & gas operations, large construction projects, airport expansions, and national digital-security frameworks. Technological modernization, including AI-enabled monitoring, long-range thermal imaging, and smart-facility automation, continues to rise. A prominent regional integrator deployed advanced surveillance networks across 14 industrial complexes in 2024, improving operational oversight by 31%. Consumer adoption varies widely, with metropolitan zones showing 41% uptake versus 19% in developing areas, driven by infrastructure maturity and regulatory clarity.

China – 26% Market Share: Dominates due to extensive production capacity and large-scale deployment across public infrastructure and industrial automation.

United States – 21% Market Share: Leads through high enterprise adoption, strong innovation ecosystems, and continuous investment in AI-powered surveillance technologies.

The Digital Monitoring Camera market reflects a moderately consolidated competitive structure, with more than 45 active global manufacturers competing across IP-based surveillance, AI-integrated monitoring, and advanced cloud-managed camera systems. The top five players collectively hold approximately 38% of the global market share, driven by continuous innovation, extensive distribution networks, and strong participation in commercial and industrial surveillance projects. Competitive intensity remains high due to rapid technology cycles, with over 60% of vendors expanding portfolios to include edge-AI analytics, automated threat detection, and seamless IoT interoperability. Across 2023–2024, more than 25 significant product launches and 15 strategic partnerships were recorded globally, including collaborations between camera manufacturers and cybersecurity solution providers to strengthen device-level encryption and data governance. Nearly 40% of active companies are increasingly investing in smart-city surveillance deployments, while around 28% are entering industrial automation monitoring. Growing patent filings in low-light imaging, thermal monitoring, and 4K/8K video compression further intensify the innovation-driven competitive landscape.

Hikvision

Dahua Technology

Axis Communications

Bosch Security Systems

Hanwha Vision

Panasonic i-PRO

Uniview

Honeywell Security

FLIR Systems

CP Plus

Vivotek

Mobotix

Avigilon

Arlo Technologies

TP-Link

Technology advancements in the Digital Monitoring Camera market are reshaping deployment strategies across commercial, industrial, and public surveillance environments. Artificial intelligence and edge computing now power more than 55% of newly deployed monitoring systems, enabling real-time object detection, license plate recognition, facial analytics, and automated threat assessment without dependence on centralized servers. Edge-based processing reduces latency by up to 40% and lowers bandwidth consumption by nearly 30%, making intelligent cameras more cost-efficient for large-scale networks. The transition from traditional analog systems to IP-based models continues to accelerate, with IP cameras accounting for over 70% of global installations. These systems benefit from enhanced resolution capabilities, with 4K and 8K cameras gaining adoption in high-security and mission-critical locations due to their ability to capture fine details and enlarge footage without distortion. Simultaneously, low-light and infrared imaging technologies have reached new performance thresholds, enabling accurate monitoring in environments with less than 0.01 lux, supporting 24/7 surveillance in warehouses, transit hubs, and border security.

Cloud-managed surveillance platforms have seen strong adoption, with nearly 45% of enterprise users integrating cloud storage and remote device management to streamline multi-site monitoring. Hybrid cloud models are also on the rise, balancing on-premise storage with cost-effective cloud analytics. Cybersecurity remains a critical technology pillar, with more than 60% of camera manufacturers embedding hardware-level encryption, secure boot mechanisms, and multi-factor authentication to counter rising IoT vulnerabilities. Emerging innovations include panoramic 360-degree cameras, AI-powered thermal imaging, and intelligent PTZ cameras equipped with autonomous tracking. Additionally, integrations with broader IoT ecosystems—such as smart lighting, intrusion alarms, and environmental sensors—are enhancing the functional scope of monitoring cameras, positioning them as central data nodes in next-generation connected infrastructure.

In Q2 2023, Hikvision launched more than a dozen new security products, including two varifocal cameras, a 180° panoramic model, and 42× Smart Pro PTZs in both 4 MP and 4K resolutions, expanding its portfolio for commercial and infrastructure surveillance. (Hikvision)

In January 2024, Hikvision introduced its new Stealth Edition camera lineup, featuring sleek black housings, full-color 24/7 ColorVu, and AcuSense AI-based human and vehicle detection across 22 SKUs.

In October 2024, Hikvision unveiled its next-generation network cameras equipped with ColorVu 3.0 technology under its EasyIP 4.0 Plus series, offering enhanced AI noise reduction and dynamic image clarity at night. (PR Newswire)

In November 2024, Dahua Technology launched its DoLynk Developer PaaS, a cloud-based platform that enables partners to build, manage, and deploy applications integrated with Dahua’s AIoT video hardware and alarm systems. (Dahua Technology)

The Digital Monitoring Camera Market Report provides a comprehensive analysis covering product types—such as IP-based, thermal, ultra-HD, edge-AI, and multispectral cameras—and their adoption across diverse application fields, including commercial security, public infrastructure, industrial operations, and residential surveillance. It also examines market segmentation by end users: government and public-sector agencies, commercial enterprises (retail, finance, logistics), and SMEs.

Geographically, the report spans all major regions: North America, Europe, Asia-Pacific, South America, and Middle East & Africa, analyzing deployment volumes, adoption trends, regulatory landscapes, and regional technology strategies. On the technology front, it deeply explores AI-driven edge computing, large-scale cloud video-management platforms, 4K/8K imaging, thermal/fusion sensors, and remote-connectivity innovations such as 4G solar cameras and cable-free systems.

In addition, the report considers emerging and niche segments like smart-city surveillance, IoT-integrated camera nodes (linked with environmental sensors or smart lighting), and sustainability-driven products (e.g., energy-efficient camera designs, recycled-material casings). It further assesses strategic priorities for businesses: ESG compliance, data-privacy regulations, cybersecurity architectures, and cross-industry partnerships. This structured, in-depth scope equips decision-makers and analysts with actionable insights on market directions, innovation levers, and competitive opportunity spaces.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 13115.2 Million |

|

Market Revenue in 2032 |

USD 32472.75 Million |

|

CAGR (2025 - 2032) |

12% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Hikvision, Dahua Technology, Axis Communications, Bosch Security Systems, Hanwha Vision, Panasonic i-PRO, Uniview, Honeywell Security, FLIR Systems, CP Plus, Vivotek, Mobotix, Avigilon, Arlo Technologies, TP-Link |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |