Reports

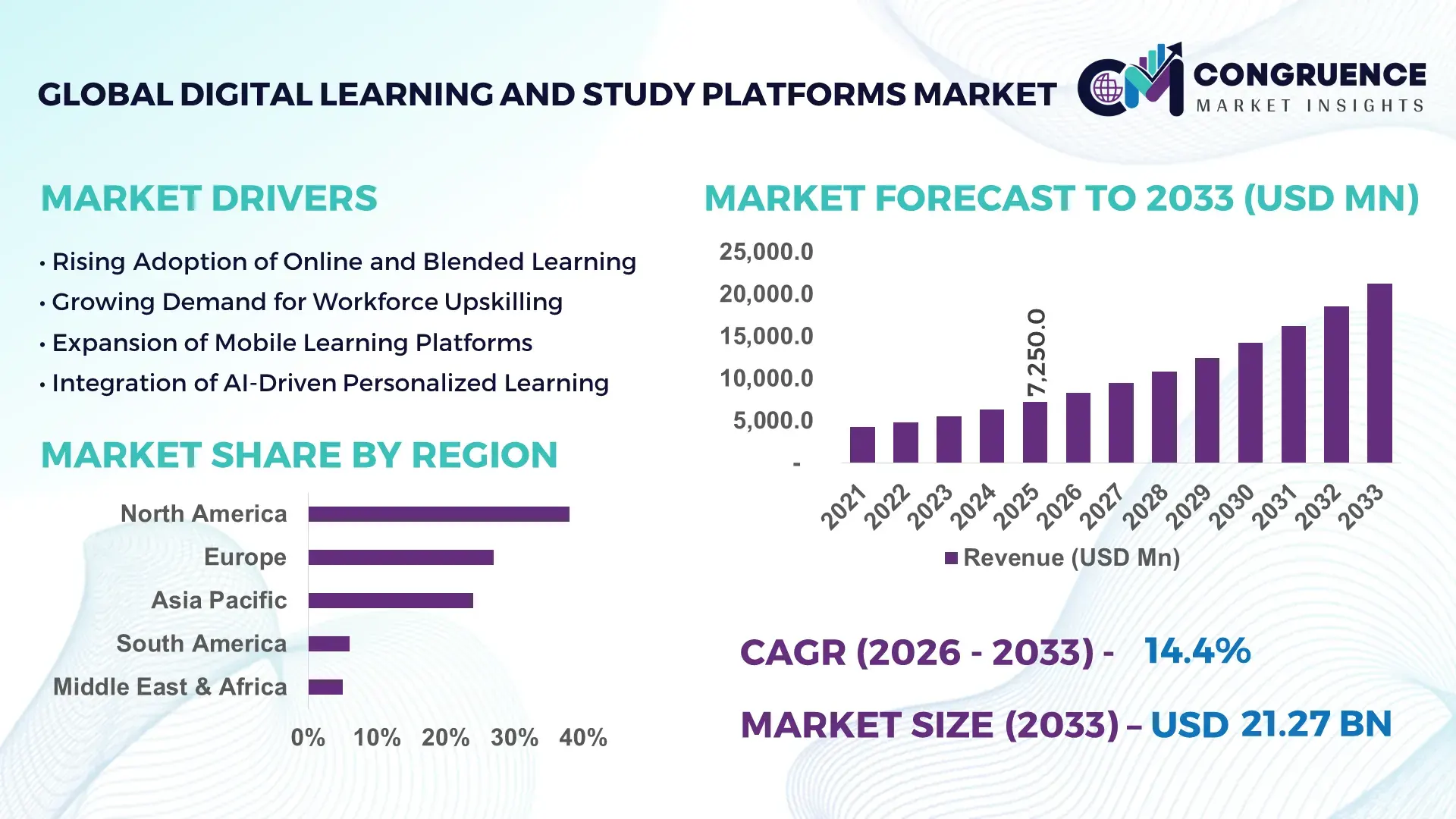

The Global Digital Learning and Study Platforms Market was valued at USD 7,250.0 Million in 2025 and is anticipated to reach a value of USD 21,269.0 Million by 2033 expanding at a CAGR of 14.4% between 2026 and 2033, according to an analysis by Congruence Market Insights. The market is primarily driven by accelerated digital transformation in education systems, rising remote learning adoption, and expanding enterprise-based online training initiatives.

The United States remains the dominant country in the Digital Learning and Study Platforms Market, supported by strong production capacity and technological infrastructure. Over 95% of U.S. K–12 schools have access to high-speed broadband, and more than 74% of public school districts deploy at least one dedicated digital learning platform. Annual EdTech investment in the U.S. exceeded USD 3.8 billion in recent funding cycles, supporting AI-driven tutoring systems, adaptive testing engines, and LMS cloud deployments. Corporate e-learning penetration among Fortune 500 firms surpasses 82%, with digital compliance and upskilling modules integrated into HR ecosystems. Higher education institutions increasingly adopt hybrid platforms, with over 60% offering fully online degree pathways supported by AI-based assessment and analytics systems.

Market Size & Growth: Valued at USD 7,250.0 Million in 2025 and projected to reach USD 21,269.0 Million by 2033, expanding at 14.4%, driven by enterprise digitization and hybrid education models.

Top Growth Drivers: 68% rise in mobile learning adoption; 55% improvement in learner engagement via AI tools; 47% enterprise shift toward cloud LMS deployment.

Short-Term Forecast: By 2028, AI-enabled personalization is expected to improve course completion rates by 32%.

Emerging Technologies: Generative AI tutoring engines, immersive AR/VR classrooms, blockchain-based credential verification.

Regional Leaders: North America projected at USD 8,900.0 Million by 2033 with strong enterprise LMS adoption; Europe at USD 5,400.0 Million driven by digital university reforms; Asia-Pacific at USD 4,800.0 Million with rapid mobile-first learning expansion.

Consumer/End-User Trends: Over 61% of learners prefer hybrid learning; 58% of enterprises integrate LMS with HR analytics systems.

Pilot or Case Example: In 2024, a U.S. university AI tutoring pilot improved student retention by 29% and reduced dropout rates by 18%.

Competitive Landscape: Market leader holds approximately 18% share, followed by major competitors including Coursera, Udemy, Blackboard, Byju’s, and Duolingo.

Regulatory & ESG Impact: Governments mandate digital accessibility compliance (WCAG 2.1), while institutions target 40% paper-use reduction via digital assessments.

Investment & Funding Patterns: Recent annual EdTech funding surpassed USD 6.0 Billion globally, with strong venture activity in AI-based microlearning platforms.

Innovation & Future Outlook: Integration of adaptive AI, analytics dashboards, and multilingual content engines is shaping scalable, global digital learning ecosystems.

Higher education contributes nearly 38% of platform usage, followed by K–12 at 34% and corporate training at 28%. AI-powered assessment tools reduce grading time by 45%, while gamified microlearning increases learner retention by 30%. Regulatory mandates on accessibility and digital credentialing accelerate adoption in North America and Europe. Asia-Pacific shows rapid mobile-driven expansion, with over 65% of users accessing platforms via smartphones, indicating strong future scalability.

The Digital Learning and Study Platforms Market has emerged as a strategic enabler of workforce transformation, academic continuity, and enterprise resilience. Organizations increasingly view digital platforms not only as instructional tools but as productivity infrastructure. AI-based adaptive learning delivers 35% faster skill acquisition compared to traditional classroom-based instruction, positioning it as a competitive differentiator for enterprises focused on rapid workforce upskilling. Learning analytics dashboards improve performance tracking accuracy by nearly 40% compared to legacy LMS reporting systems.

North America dominates in volume of institutional deployments, while Asia-Pacific leads in adoption growth with over 65% of learners accessing platforms via mobile-first ecosystems. Europe demonstrates strong enterprise integration, with approximately 58% of large firms embedding LMS into HR performance systems. By 2028, generative AI–driven tutoring systems are expected to reduce instructional design time by 30% while improving learner engagement metrics by 25%.

From a compliance perspective, firms are committing to digital sustainability goals, targeting 40% reduction in printed learning materials by 2030 through e-assessments and digital credentialing. In 2024, a U.S.-based university network achieved a 28% improvement in first-year student retention through AI-powered early intervention analytics.

Looking forward, the Digital Learning and Study Platforms Market will function as a pillar of resilience, regulatory compliance, and sustainable workforce development, supporting scalable education ecosystems aligned with digital economy demands.

The Digital Learning and Study Platforms Market is shaped by rapid digitization of educational infrastructure, enterprise reskilling initiatives, and the mainstreaming of AI-enabled content delivery systems. Increasing broadband penetration, cloud computing scalability, and mobile device proliferation continue to expand accessibility. Over 70% of global internet users now access educational content online, reflecting widespread behavioral shifts toward flexible learning formats. Hybrid academic models are standardizing digital platform usage across universities, while corporate compliance training increasingly transitions to automated LMS ecosystems. Additionally, cross-border certification, multilingual AI translation engines, and blockchain-based credential authentication are influencing institutional procurement strategies. The market’s trajectory is influenced by regulatory digital accessibility standards, cybersecurity frameworks, and performance-based analytics adoption, positioning Digital Learning and Study Platforms as core infrastructure within modern knowledge economies.

Enterprise digital transformation initiatives significantly contribute to market expansion. Approximately 72% of large enterprises have implemented structured digital upskilling programs, with 58% integrating LMS directly into HR analytics systems. AI-enabled microlearning modules improve employee productivity by 24% and reduce onboarding time by nearly 30%. Remote and hybrid work models, adopted by over 60% of global enterprises, further intensify reliance on scalable digital learning systems. Additionally, compliance-driven industries such as healthcare and finance require periodic certification, pushing automated course deployment and real-time tracking adoption rates above 65% among regulated organizations.

Despite growth, uneven broadband access limits platform penetration in developing regions. Nearly 37% of rural populations globally lack stable high-speed internet, restricting synchronous e-learning participation. Device affordability also remains a concern, with over 30% of students in low-income regions relying on shared mobile devices. Cybersecurity concerns further restrict adoption; 43% of educational institutions report at least one data breach attempt annually. Integration complexities between legacy IT systems and modern cloud-based LMS platforms create additional operational constraints for institutions with outdated digital infrastructure.

AI-driven personalization offers significant growth potential. Adaptive learning engines improve knowledge retention by 35% and increase course completion rates by 28%. Multilingual AI translation tools enable cross-border enrollment growth exceeding 40% in international online programs. Gamification modules enhance engagement metrics by nearly 30%, while predictive analytics can identify at-risk learners with 85% accuracy. Emerging markets in Southeast Asia and Africa, where mobile internet penetration exceeds 60%, provide substantial untapped demand for mobile-first digital learning ecosystems.

Data privacy regulations such as GDPR and student data protection laws impose strict compliance requirements. Approximately 48% of educational IT budgets are allocated toward cybersecurity upgrades and compliance audits. Cloud migration exposes institutions to phishing and ransomware risks, with reported education-sector cyber incidents increasing by 44% year-over-year. Additionally, ensuring accessibility compliance (WCAG 2.1) requires content redesign and platform restructuring, increasing implementation timelines and operational costs. These challenges necessitate sustained investment in secure, interoperable infrastructure.

AI-Powered Adaptive Learning Achieving 35% Higher Retention Rates: AI-based adaptive engines are transforming instructional delivery. Institutions deploying AI tutors report 35% higher knowledge retention and 32% faster module completion. Over 62% of universities now pilot predictive analytics to identify at-risk students, improving intervention success rates by 27%. Automated grading systems reduce faculty workload by nearly 45%, enhancing institutional efficiency.

Mobile-First Learning Ecosystems Expanding Beyond 65% User Penetration: More than 65% of global users access digital learning platforms via smartphones. In Asia-Pacific, mobile-only learners account for nearly 48% of total enrollments. Push-notification learning reminders improve daily active usage by 22%, while bite-sized microlearning increases completion rates by 30%. 5G rollout is projected to improve streaming-based virtual classroom quality by 40% in urban centers.

Immersive AR/VR Classrooms Delivering 50% Engagement Boost: AR/VR-based simulation modules improve practical skill acquisition by 38% and raise engagement metrics by 50% in technical education segments. Over 41% of STEM-focused institutions now experiment with immersive labs. VR safety training programs reduce real-world incident rates by 23%, demonstrating measurable ROI in industrial applications.

Blockchain Credentialing Reducing Verification Time by 60%: Digital credentialing platforms using blockchain reduce verification processing time by 60% and cut administrative costs by 25%. Approximately 36% of higher education institutions have adopted digital badges or verifiable certificates. Cross-border digital degree authentication improves international student mobility by 18%, strengthening global academic integration.

The Digital Learning and Study Platforms Market is segmented by type, application, and end-user, reflecting diverse deployment models and consumption patterns across education and enterprise ecosystems. From a type perspective, cloud-based platforms dominate institutional adoption due to scalability, integration flexibility, and centralized analytics capabilities. On-premise and hybrid systems continue to serve regulated industries requiring strict data governance. Application-wise, academic learning remains the largest segment, supported by widespread LMS integration across K–12 and higher education institutions, while corporate training demonstrates accelerated adoption driven by workforce reskilling mandates. End-user segmentation highlights higher education institutions as primary adopters, followed by K–12 schools and enterprise organizations. Increasing mobile penetration, AI-powered personalization, and digital credentialing solutions further refine segmentation patterns, with measurable gains in learner engagement, certification turnaround time, and compliance tracking efficiency across each segment.

The Digital Learning and Study Platforms Market by type includes Cloud-Based Platforms, On-Premise Platforms, and Hybrid Deployment Models. Cloud-based platforms currently account for approximately 64% of total adoption, primarily due to their scalability, subscription flexibility, and seamless integration with analytics and AI-driven personalization tools. Over 70% of new institutional LMS deployments are cloud-native, reflecting accelerated migration away from legacy infrastructure.

On-premise systems hold nearly 21% of adoption, mainly within government institutions and regulated sectors requiring strict data sovereignty controls. However, hybrid models represent the fastest-growing segment, expanding at an estimated CAGR of 16.8%, as enterprises seek balanced control and scalability. Hybrid deployments are projected to exceed 25% penetration by 2033 due to cybersecurity prioritization and compliance requirements.

Other niche types, including mobile-only learning platforms and open-source LMS frameworks, collectively contribute around 15%, serving cost-sensitive and regional education markets.

In 2024, the U.S. Department of Education reported that over 80% of federally funded higher education institutions transitioned to cloud-based LMS infrastructures to enhance cybersecurity and remote accessibility capabilities.

Application segments include Academic Learning, Corporate Training & Workforce Development, Competitive Exam Preparation, and Skill-Based Certification Programs. Academic learning leads with approximately 46% share, supported by widespread LMS integration across public and private institutions. Over 74% of universities globally use centralized digital learning systems for content distribution and assessment management.

Corporate training accounts for about 32% of usage, driven by compliance mandates and digital upskilling initiatives. While academic platforms dominate current adoption, corporate learning is the fastest-growing application, expanding at an estimated CAGR of 17.5%, fueled by remote workforce models and AI-based performance tracking. Competitive exam preparation and certification programs collectively contribute around 22%, benefiting from mobile-first delivery and gamification strategies.

In 2025, more than 41% of global enterprises reported piloting AI-driven digital learning systems for workforce skill mapping. Additionally, 63% of Gen Z learners prefer digital-first certification pathways over traditional classroom instruction.

In 2024, UNESCO documented digital learning system deployments across more than 150 national education initiatives, improving access to structured online education for over 2 million learners in developing regions.

End-user segmentation includes Higher Education Institutions, K–12 Schools, Corporate Enterprises, Government & Public Sector Organizations, and Individual Learners. Higher education institutions lead with approximately 38% share, as over 60% of universities offer hybrid or fully online degree programs supported by centralized digital platforms. Learning analytics integration enables performance tracking improvements of nearly 30% in tertiary institutions.

Corporate enterprises represent the fastest-growing end-user segment, expanding at an estimated CAGR of 18.2%, driven by compliance training automation and digital skill certification programs. Around 58% of multinational enterprises have embedded LMS solutions into HR and performance management systems. K–12 schools contribute roughly 27%, with national digital curriculum mandates increasing platform standardization. Government agencies and individual learners collectively account for approximately 17%, particularly in civil service training and language learning applications.

In 2025, nearly 44% of enterprises globally increased digital learning budgets to support AI-based workforce reskilling. Additionally, 66% of university students report weekly engagement with adaptive learning dashboards.

In 2024, the European Commission’s Digital Education Action Plan review indicated that over 70% of public universities in EU member states integrated centralized digital learning platforms for standardized academic delivery and credentialing.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 16.9% between 2026 and 2033.

North America’s leadership is supported by over 82% enterprise LMS penetration among large corporations and more than 74% digital platform integration across higher education institutions. Europe follows with approximately 27% share, driven by cross-border digital credential frameworks and standardized e-learning compliance regulations adopted in over 65% of EU universities. Asia-Pacific holds nearly 24% of global demand, with mobile-based learning accounting for over 65% of total usage in emerging economies. South America contributes around 6%, supported by national digital education reforms covering 58% of public schools in major economies. The Middle East & Africa represent close to 5%, with government-backed digital transformation programs increasing e-learning adoption across public sector training institutions by 40% in recent years.

North America accounts for approximately 38% of the global Digital Learning and Study Platforms Market, reflecting strong enterprise and academic integration. Over 80% of Fortune 1000 companies deploy structured LMS frameworks, particularly in healthcare, finance, and IT sectors. Regulatory initiatives promoting digital accessibility standards have driven platform modernization across 72% of public universities. Cloud-native LMS deployment exceeds 70% among new institutional contracts, while AI-based adaptive modules improve student performance tracking accuracy by nearly 35%. A key regional player, Coursera, continues expanding partnerships with over 300 universities and industry leaders to deliver accredited online degree programs and workforce certifications. Consumer behavior indicates higher enterprise-led adoption, with 61% of professionals engaging in employer-sponsored online upskilling programs annually. Hybrid learning formats are preferred by nearly 68% of university students, reinforcing sustained demand.

Europe holds approximately 27% share of the Digital Learning and Study Platforms Market, with Germany, the United Kingdom, and France representing the largest national contributors. Over 70% of universities across EU member states have integrated centralized LMS platforms aligned with digital accessibility frameworks. Regulatory emphasis on GDPR compliance has increased secure cloud deployments by 45% across institutions. Emerging technologies such as AI-powered grading systems and blockchain credentialing are adopted by nearly 36% of higher education institutions. A prominent regional provider, Blackboard (with extensive European operations), supports multilingual LMS environments serving over 1,000 institutions. Consumer behavior trends show that 59% of learners prefer structured, accredited digital certification programs. Regulatory pressure also drives demand for explainable AI in assessment algorithms, influencing procurement decisions in public education systems.

Asia-Pacific accounts for nearly 24% of the global Digital Learning and Study Platforms Market and ranks as the fastest-growing region. China, India, and Japan represent the top consuming countries, collectively contributing over 70% of regional demand. Mobile learning accounts for more than 65% of total platform access, reflecting smartphone penetration exceeding 75% in urban populations. Government-led digital literacy programs support infrastructure expansion, with over 60% of public institutions implementing centralized digital content repositories. Regional innovation hubs in India and Singapore actively develop AI tutoring engines and multilingual learning apps. Byju’s, a major regional player, has scaled digital course distribution to millions of learners through app-based subscription models. Consumer behavior indicates strong preference for mobile AI-driven microlearning modules, particularly among Gen Z users, with engagement rates surpassing 40% weekly active usage.

South America represents approximately 6% of the global Digital Learning and Study Platforms Market, led by Brazil and Argentina. Brazil alone accounts for over 45% of regional platform deployments. National digital inclusion policies have extended broadband access to nearly 70% of urban public schools. Government incentives encourage LMS adoption in vocational and public sector training institutions, covering approximately 52% of state-run educational facilities. Local EdTech providers increasingly focus on Portuguese and Spanish language localization to address regional demand. Consumer behavior patterns show rising mobile usage, with 58% of learners accessing digital courses via smartphones. Corporate training adoption is growing steadily, particularly in finance and telecommunications sectors, where compliance-based digital certification programs are integrated into HR systems.

The Middle East & Africa account for roughly 5% of the global Digital Learning and Study Platforms Market, with the UAE and South Africa emerging as key growth countries. Public sector digital transformation programs have expanded e-learning integration across 48% of government training institutions. Oil & gas and construction sectors increasingly deploy compliance-based LMS systems to train over 60% of technical staff through digital modules. Technological modernization efforts include AI-based language translation for multilingual workforce training. Regional partnerships with global cloud providers have increased secure LMS hosting capacity by nearly 35%. Consumer behavior reflects growing preference for mobile and blended learning formats, particularly among young professionals, with online certification enrollments increasing by 28% year-over-year in major metropolitan areas.

United States – 34% Market Share: It is driven by strong enterprise LMS penetration, widespread higher education digitization, and sustained EdTech investment exceeding 80% institutional cloud adoption.

China – 19% market share: It benefits from large-scale mobile learning adoption, government-backed digital literacy initiatives, and AI-powered tutoring platforms serving millions of active users annually.

The Digital Learning and Study Platforms Market exhibits a moderately fragmented structure, characterized by the presence of more than 250 active global and regional competitors offering LMS, MOOC platforms, AI-based tutoring systems, and enterprise training solutions. The top five companies collectively account for approximately 42% of total market share, indicating a competitive but innovation-driven landscape. Market leaders maintain strong positioning through diversified portfolios spanning academic degrees, professional certifications, enterprise compliance training, and AI-enabled learning analytics.

Strategic initiatives increasingly define competitive differentiation. Over 60% of leading vendors have launched generative AI-powered features since 2024, including automated assessment grading, personalized content sequencing, and AI-driven tutoring assistants. Partnerships between platform providers and over 500 universities globally have expanded accredited online degree offerings, while corporate alliances with Fortune 1000 enterprises strengthen recurring B2B contracts.

Mergers and acquisitions remain active, particularly in mobile learning apps and skill certification startups, with at least 18 notable transactions recorded across 2024–2025. Competitive intensity is further amplified by regional players focusing on vernacular content, mobile-first access models, and gamification features. Innovation trends such as blockchain-based credential verification, immersive VR classrooms, and predictive learner analytics are reshaping market positioning, compelling vendors to allocate nearly 25% of operational budgets toward R&D and AI integration initiatives.

Blackboard

Byju’s

edX

Pluralsight

LinkedIn Learning

Moodle

Instructure (Canvas LMS)

Skillsoft

2U Inc.

Kahoot!

Chegg

FutureLearn

Technological evolution remains central to the Digital Learning and Study Platforms Market, with artificial intelligence, cloud computing, immersive technologies, and blockchain forming the core innovation pillars. AI-powered adaptive learning engines currently influence more than 62% of newly deployed platforms, enabling personalized content sequencing based on learner behavior analytics. Predictive analytics systems improve student retention tracking accuracy by approximately 35%, while automated grading algorithms reduce instructor workload by nearly 45%.

Generative AI integration is accelerating, with over 58% of enterprise learning systems embedding AI tutors capable of real-time question resolution and dynamic content summarization. Cloud-native infrastructure dominates new deployments, accounting for more than 70% of institutional LMS implementations, ensuring scalability, uptime above 99.5%, and enhanced cybersecurity compliance frameworks.

Immersive technologies such as AR and VR are gaining traction in technical and healthcare education, where simulation-based learning improves practical skill acquisition by 38% compared to traditional modules. Blockchain-enabled credentialing systems reduce verification time by 60% and enhance cross-border academic mobility.

Mobile-first architecture is equally transformative, with 65% of users globally accessing platforms through smartphones. API-driven interoperability enables integration with HR systems, CRM tools, and digital assessment engines, supporting unified performance dashboards. Advanced cybersecurity tools, including multi-factor authentication and AI-driven anomaly detection, are implemented in over 55% of enterprise-grade systems, reflecting heightened data protection priorities.

• In September 2024, Coursera expanded its AI-powered Coursera Coach to support interactive personalized instruction, learning assistance, and career guidance. Coach improvements have supported over 1 million learners, with measurable increases in quiz pass rates and lessons completed. Source: www.blog.coursera.org

• In October 2025, Coursera reported that 97% of courses now include its GenAI tutor, available in 26 languages, with expanded AI capabilities like role-play immersive simulations and machine-translated content across 7,500+ courses, improving learner engagement and retention. Source: www.in.investing.com

• In June 2025, Duolingo introduced a new Chess learning course within its app, combining step-by-step lessons with interactive puzzles and mini matches guided by its virtual coach “Oscar,” broadening learning beyond languages and math. Sources: www.blog.duolingo.com

• In December 2025, Duolingo revealed major platform expansions, including 172 new language courses, the launch of Duolingo Score to showcase learner progress professionally, and enhancements to its chess offering with player-vs-player modes and advanced content segments. Sources: www.blog.duolingo.com

The Digital Learning and Study Platforms Market Report provides a comprehensive analysis of platform types, deployment models, applications, end-user segments, and geographic coverage across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. The scope encompasses cloud-based, on-premise, and hybrid deployment frameworks, evaluating their adoption across academic institutions, corporate enterprises, government agencies, and individual learners.

Application coverage includes academic learning systems, corporate workforce development platforms, certification and exam preparation modules, language learning ecosystems, and AI-powered microlearning environments. The report assesses adoption metrics such as mobile usage exceeding 65% globally, AI-based personalization deployment in over 60% of new systems, and blockchain credentialing adoption across more than one-third of higher education institutions.

Technological analysis within the report highlights artificial intelligence, predictive analytics, immersive AR/VR simulations, cybersecurity frameworks, and API-driven interoperability trends. Regional evaluation covers over 30 key countries, analyzing broadband penetration levels above 70% in advanced economies and mobile-first expansion across emerging markets.

The scope further examines competitive benchmarking among more than 250 active vendors, innovation intensity levels, partnership ecosystems exceeding 500 university collaborations, and enterprise LMS integration across 80% of large multinational organizations. Emerging segments such as AI-driven tutoring assistants, digital credential marketplaces, and multilingual adaptive platforms are included to provide forward-looking strategic insights for investors, policymakers, and corporate decision-makers.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 7,250.0 Million |

| Market Revenue (2033) | USD 21,269.0 Million |

| CAGR (2026–2033) | 14.4% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Coursera; Udemy; Duolingo; Blackboard; Byju’s; edX; Pluralsight; LinkedIn Learning; Moodle; Instructure (Canvas LMS); Skillsoft; 2U Inc.; Kahoot!; Chegg; FutureLearn |

| Customization & Pricing | Available on Request (10% Customization Free) |