Reports

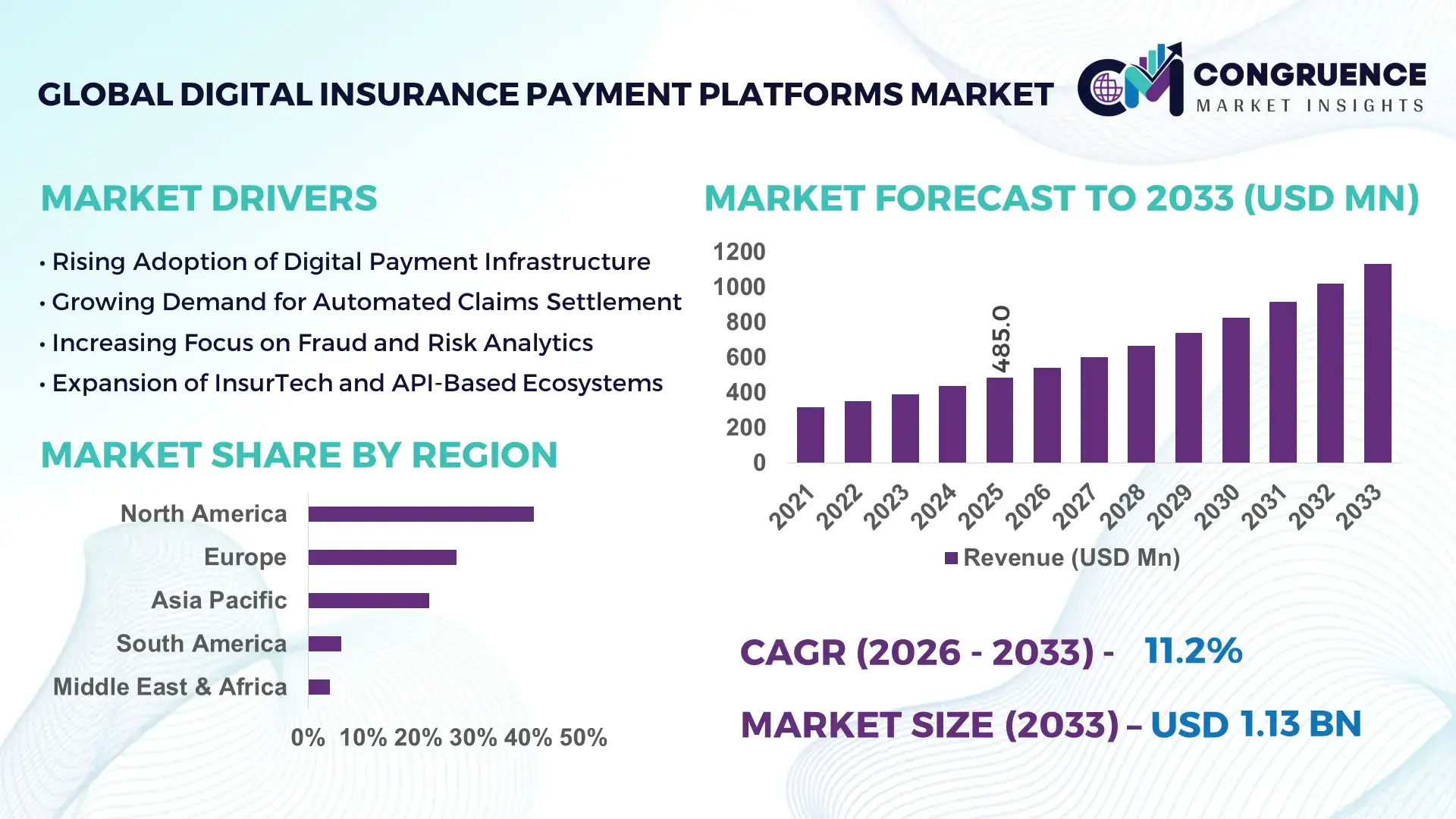

The Global Digital Insurance Payment Platforms Market was valued at USD 485.0 Million in 2025 and is anticipated to reach a value of USD 1,133.9 Million by 2033 expanding at a CAGR of 11.2% between 2026 and 2033, according to an analysis by Congruence Market Insights. Growth is primarily driven by rising digital premium collections, increasing claims automation, and strong demand for embedded fintech payment integrations across life and non-life insurance ecosystems.

The United States represents the dominant country in the Digital Insurance Payment Platforms Market, supported by over 5,000 active insurance carriers and more than 300 million digitally connected policyholders. In 2025, over 78% of U.S. insurance premium payments are processed digitally, while nearly 65% of claims disbursements utilize automated electronic payment rails such as ACH and RTP networks. Investment in InsurTech exceeded USD 8 billion in recent funding cycles, with a significant portion directed toward payment orchestration, fraud analytics, and API-driven billing systems. More than 60% of Tier-1 insurers in the country have integrated real-time payment capabilities, and digital wallet-based premium collection has surpassed 35% adoption among younger policyholders.

Market Size & Growth: Valued at USD 485.0 Million in 2025 and projected to reach USD 1,133.9 Million by 2033, expanding at 11.2% CAGR due to accelerated digital premium processing and automated claims settlement adoption.

Top Growth Drivers: 78% digital premium adoption rate; 45% reduction in payment reconciliation time; 52% operational efficiency gain through automated billing systems.

Short-Term Forecast: By 2028, automated claims payout systems are expected to reduce processing turnaround time by 40% and cut administrative costs by 28%.

Emerging Technologies: AI-driven fraud detection, blockchain-enabled smart claims contracts, and real-time payment (RTP) integration APIs.

Regional Leaders: North America projected at USD 420 Million by 2033 with high real-time payment penetration; Europe at USD 310 Million driven by PSD2-enabled open banking; Asia-Pacific at USD 270 Million fueled by mobile-first premium payments.

Consumer/End-User Trends: Over 70% of policyholders prefer digital billing portals; subscription-style micro-insurance payments are growing by 30% annually among millennials.

Pilot or Case Example: In 2024, a U.S. insurer implemented AI-based claims disbursement automation achieving 38% faster payouts and 22% fraud reduction.

Competitive Landscape: Fiserv (~18% share), Guidewire, Stripe, DXC Technology, and Duck Creek Technologies dominate competitive positioning.

Regulatory & ESG Impact: Open banking mandates and digital payment security frameworks improved transaction transparency by 35% while reducing paper-based processing by 50%.

Investment & Funding Patterns: Over USD 2.5 Billion invested in InsurTech payment solutions since 2023, with venture-backed API platforms gaining traction.

Innovation & Future Outlook: Embedded insurance payments, AI-powered billing orchestration, and cross-border digital settlement solutions are shaping long-term platform scalability.

Life and health insurance collectively contribute over 55% of platform usage, while property & casualty accounts for nearly 35% of transaction volumes. Recent innovations include tokenized premium payments and biometric-based claim authentication. Regulatory mandates such as open banking frameworks have accelerated API integrations by 40%. North America leads in transaction density, while Asia-Pacific records over 60% mobile-based premium payments, signaling strong future digital convergence.

The Digital Insurance Payment Platforms Market holds strategic relevance as insurers transition from legacy batch-processing systems to real-time, API-driven payment infrastructures. Modern AI-powered payment orchestration platforms deliver 45% faster reconciliation compared to traditional manual clearing systems, while blockchain-based smart contracts reduce claims validation cycles by nearly 35% compared to conventional documentation-heavy standards. This operational modernization directly enhances liquidity management, fraud mitigation, and regulatory reporting accuracy.

North America dominates in transaction volume due to high digital banking penetration, while Asia-Pacific leads in adoption intensity with over 60% of policyholders preferring mobile-first premium payments. Europe demonstrates strong compliance-led modernization, with more than 70% of insurers integrating open banking APIs into billing systems. By 2028, AI-driven fraud analytics embedded within payment platforms are expected to reduce false claims processing losses by 30% while improving settlement speed by 25%.

From an ESG perspective, insurers are committing to 50% reductions in paper-based billing processes by 2030, leveraging fully digital premium invoicing and electronic claims documentation. In 2024, a leading U.S. insurer achieved a 32% reduction in operational overhead through real-time payment integration and automated reconciliation engines.

Looking forward, the Digital Insurance Payment Platforms Market is positioned as a core pillar of operational resilience, regulatory compliance, and sustainable digital transformation across global insurance ecosystems.

The Digital Insurance Payment Platforms Market is shaped by accelerating digital transformation across the insurance value chain. Insurers are prioritizing automation in premium collection, installment billing, cross-border claims payouts, and multi-channel customer payment interfaces. Increasing adoption of real-time payment rails and open banking APIs has transformed settlement cycles from multi-day clearing windows to near-instant execution.

Embedded finance models are integrating payment functionality directly into insurance distribution channels, enabling seamless checkout experiences within broker portals and aggregator apps. Fraud detection technologies using AI and behavioral analytics have reduced suspicious transaction rates by over 20% in digitally advanced markets. Additionally, regulatory mandates around data protection and transaction traceability are pushing insurers toward encrypted, tokenized payment ecosystems. The competitive environment is increasingly technology-centric, with insurers investing heavily in cloud-native billing platforms and API-driven payment gateways to ensure scalability and operational transparency.

Digital premium adoption has surpassed 70% in advanced insurance markets, significantly transforming billing infrastructures. Consumers increasingly demand auto-debit subscriptions, mobile wallet payments, and real-time claim reimbursements. Automated payment systems reduce reconciliation errors by nearly 35% and cut manual administrative workload by approximately 40%. Additionally, subscription-based micro-insurance products—growing at over 30% annually in urban regions—require flexible recurring billing systems. Insurers deploying integrated payment orchestration platforms report up to 25% improvement in customer retention due to seamless digital experiences. The growing preference for contactless and remote financial transactions continues to accelerate platform modernization across life, health, and property insurance segments.

Over 45% of mid-sized insurers still operate on legacy core systems built more than 15 years ago, limiting integration with real-time payment APIs. Migration costs for full-scale billing modernization can increase IT budgets by 20–30% during transition phases. Interoperability challenges between legacy policy administration systems and modern payment gateways often lead to delayed reconciliation cycles. Furthermore, cybersecurity risks remain significant, as financial service platforms experience over 1,000 attempted cyber incidents per week globally. Compliance complexity across jurisdictions—especially concerning cross-border transactions and data residency—adds operational burden and slows implementation timelines for digital payment infrastructures.

Embedded finance integration within e-commerce and digital banking ecosystems offers significant expansion potential. More than 65% of online insurance purchases now occur via aggregator or partner platforms, creating demand for API-based embedded payment capabilities. Cross-border digital insurance products are increasing by nearly 25% annually, necessitating multi-currency and real-time FX settlement features. Mobile micro-insurance adoption in emerging markets has exceeded 50% among first-time policy buyers. Insurers leveraging AI-based payment analytics can improve fraud detection accuracy by 30% and enhance underwriting precision through transaction data insights. These innovations open scalable revenue streams and expand access to underinsured populations.

Digital insurance payment ecosystems handle high-value financial and personal data, making them prime targets for cyber threats. Financial institutions globally report that phishing and payment fraud attempts have increased by over 25% annually. Compliance with PSD2, PCI-DSS, and evolving data privacy laws requires continuous investment in encryption, tokenization, and identity authentication mechanisms. Implementation of advanced fraud detection systems can raise operational expenditure by up to 15% in the short term. Additionally, maintaining 99.9% system uptime while integrating multi-channel payment options demands resilient cloud infrastructure and constant monitoring, increasing technical complexity for insurers.

Real-Time Claims Settlement Expansion (40% Faster Processing): Insurers adopting real-time payment rails have reduced average claims payout cycles from 5 days to under 3 days, representing nearly 40% faster settlement performance. Over 62% of Tier-1 insurers have integrated RTP or instant ACH systems, significantly improving customer satisfaction scores by 18%.

AI-Driven Fraud Detection Reducing False Claims by 30%: Advanced machine learning algorithms now analyze transaction patterns across more than 200 behavioral variables. Insurers deploying AI-based fraud analytics report up to 30% reduction in false claim payouts and 22% improvement in anomaly detection accuracy.

API-Based Open Banking Integration (70% Adoption in Europe): With open banking frameworks expanding, over 70% of insurers in regulated European markets have integrated secure payment APIs, enabling direct bank-to-insurer transfers and reducing transaction fees by 15%.

Growth in Mobile-First Premium Payments (60% Usage in Asia-Pacific): Mobile wallet and QR-based premium payments account for more than 60% of digital insurance transactions in Asia-Pacific. Instant notification systems have improved premium renewal compliance rates by 25%, strengthening recurring revenue predictability.

The Digital Insurance Payment Platforms Market is segmented by type, application, and end-user, reflecting the evolving structure of insurance payment ecosystems. By type, the market includes premium collection platforms, claims disbursement systems, billing & invoicing automation platforms, fraud & risk analytics modules, and payment orchestration APIs. Premium collection and billing automation platforms dominate due to high recurring transaction volumes and subscription-based insurance models. By application, premium processing remains the largest use case, followed by claims settlement and policy renewal management, as insurers prioritize operational efficiency and digital customer engagement. End-user segmentation highlights large insurance carriers as primary adopters, followed by mid-sized insurers, brokers, and digital-first InsurTech firms. Notably, over 70% of Tier-1 insurers have integrated multi-channel payment capabilities, while mobile-first premium transactions exceed 60% in emerging Asia-Pacific markets. The segmentation landscape indicates strong momentum toward API-based modular systems capable of integrating with legacy and cloud-native core insurance infrastructures.

The Digital Insurance Payment Platforms Market by type comprises premium collection platforms, claims disbursement platforms, billing & invoicing automation systems, fraud detection & payment risk analytics modules, and payment orchestration/API integration platforms. Premium collection platforms currently account for approximately 38% of overall platform adoption, as recurring premium transactions represent the highest transaction frequency across life, health, and property insurance lines. Claims disbursement systems hold nearly 24%, driven by insurer focus on improving settlement speed and customer satisfaction. Billing & invoicing automation solutions represent about 18%, enabling automated installment management and reducing reconciliation errors by up to 35%. Fraud detection and analytics modules contribute around 12%, increasingly integrated with AI engines for anomaly detection. The remaining 8% is attributed to payment orchestration APIs and cross-border settlement tools, which serve niche but rapidly expanding use cases. Payment orchestration/API platforms are the fastest-growing segment, expanding at an estimated CAGR of 14.6%, fueled by open banking regulations and embedded insurance models. These solutions enable seamless integration with digital wallets, banking rails, and third-party distribution platforms.

By application, the Digital Insurance Payment Platforms Market is categorized into premium processing, claims management & settlement, policy renewals, cross-border insurance payments, and fraud monitoring. Premium processing remains the leading application, accounting for approximately 44% of total usage due to recurring billing models and subscription-based micro-insurance products. Claims management & settlement holds around 28%, reflecting insurer efforts to shorten payout cycles and improve digital customer journeys. Policy renewal automation contributes 14%, enhancing retention through automated reminders and digital billing links. Cross-border payments represent 8%, driven by global travel, expatriate insurance, and multinational corporate policies. Fraud monitoring applications account for the remaining 6%, though their integration across other modules increases their functional importance. Claims management & settlement is the fastest-growing application segment, expanding at nearly 15.2% CAGR, supported by AI-driven claims validation and real-time payout systems that reduce processing times by up to 40%. In 2025, more than 42% of global insurers reported piloting AI-enabled claims disbursement systems to enhance operational transparency. Additionally, over 65% of digital-first policyholders prefer instant digital payouts over traditional bank transfer cycles.

End-user segmentation includes large insurance carriers, mid-sized insurers, insurance brokers & agencies, InsurTech companies, and reinsurance providers. Large insurance carriers dominate the market with approximately 52% adoption share, driven by high transaction volumes and complex multi-channel billing requirements. Mid-sized insurers hold around 23%, increasingly investing in cloud-native payment infrastructure to remain competitive. InsurTech firms account for 12%, leveraging API-first architectures and embedded finance capabilities. Brokers and agencies contribute 9%, primarily using integrated billing portals for policyholder transactions. Reinsurance providers represent the remaining 4%, focused on high-value cross-border settlement platforms. InsurTech companies represent the fastest-growing end-user segment, expanding at nearly 16.1% CAGR due to rapid digital product launches and mobile-first distribution models. Over 48% of new insurance startups launched in 2025 incorporated integrated digital payment gateways at inception. Furthermore, 58% of policyholders aged under 35 report preferring insurers offering app-based premium and claims payment functionality.

North America accounted for the largest market share at 41% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of14.8% between 2026 and 2033.

North America’s dominance is supported by over 78% digital premium penetration and more than 65% real-time claims settlement adoption across Tier-1 insurers. Europe holds approximately 27% share, driven by PSD2-enabled open banking frameworks and strong compliance mandates. Asia-Pacific accounts for nearly 22% of global adoption, with mobile-based insurance payments exceeding 60% in key markets. South America contributes about 6%, while the Middle East & Africa collectively represent around 4%, reflecting gradual modernization of insurance billing ecosystems. Cross-border insurance payments have grown by 25% globally, with Asia-Pacific and Europe showing the highest transaction density growth. Real-time payment infrastructure integration exceeds 70% among insurers in developed economies, significantly improving payout turnaround by up to 40% compared to traditional clearing systems.

North America represents approximately 41% of the global Digital Insurance Payment Platforms Market, driven by high digital banking penetration and advanced real-time payment infrastructure. The United States and Canada collectively process more than 75% of insurance premiums through digital channels. Key industries fueling demand include life & health insurance, property & casualty, and commercial insurance lines. Regulatory frameworks such as enhanced PCI-DSS compliance standards and real-time payment network expansions support secure transaction ecosystems. Technological transformation is evident, with over 70% of Tier-1 insurers deploying AI-driven fraud analytics and API-based payment orchestration layers. Fiserv, a major regional player, has expanded real-time claims disbursement integrations, enabling insurers to cut settlement time by nearly 35%. Consumer behavior indicates that over 68% of policyholders prefer automated recurring premium deductions, while mobile claim reimbursement adoption has exceeded 50% among policyholders under 40 years of age.

Europe accounts for nearly 27% of the global Digital Insurance Payment Platforms Market, led by Germany, the United Kingdom, and France. Regulatory oversight by the European Central Bank and open banking directives under PSD2 have accelerated API-driven direct bank transfers, reducing transaction processing costs by up to 15%. Over 70% of European insurers have integrated secure open banking APIs for premium collection and settlement. Emerging technologies such as blockchain-based payment authentication and AI fraud scoring systems are increasingly deployed to ensure compliance with strict data protection regulations. Guidewire and other regional technology providers are expanding digital billing modules across major European insurers. Consumer behavior varies across the region, with Northern European markets showing over 80% digital premium adoption, while Southern Europe demonstrates growing demand for mobile wallet-linked insurance payments due to rising fintech penetration.

What Is Fueling the Surge in Mobile-First Insurance Payment Adoption?

Asia-Pacific holds approximately 22% of the Digital Insurance Payment Platforms Market and ranks as the fastest-growing regional ecosystem. China, India, and Japan are the top consuming countries, collectively accounting for over 65% of regional digital insurance transactions. Mobile wallet and QR-code premium payments exceed 60% usage in urban markets. Infrastructure expansion, including real-time payment rails and national digital identity frameworks, has accelerated payment authentication and onboarding. Regional innovation hubs in Singapore and India are fostering InsurTech startups integrating embedded finance models into e-commerce and super-app ecosystems. A leading regional fintech player has enabled instant claim settlements under 24 hours for over 10 million micro-insurance users. Consumer behavior shows that more than 72% of first-time policy buyers prefer mobile-based premium payments, reflecting strong alignment with digital commerce and smartphone penetration trends.

South America represents around 6% of the global Digital Insurance Payment Platforms Market, with Brazil and Argentina as key contributors. Brazil accounts for nearly 55% of the regional transaction volume, supported by instant payment systems such as PIX. Insurance payment modernization is closely linked to financial inclusion initiatives and digital banking adoption exceeding 70% in urban populations. Government-backed fintech policies and digital identity programs are enhancing online premium collection infrastructure. Local insurance providers are integrating installment-based billing and mobile claim payments to address underinsured populations. Consumer trends reveal that over 48% of policyholders prefer installment-based digital premium options, particularly in micro and SME insurance segments. Regional growth is further supported by rising smartphone usage, now exceeding 75% penetration across major economies.

The Middle East & Africa account for approximately 4% of the Digital Insurance Payment Platforms Market, with the UAE and South Africa leading adoption. Digital transformation initiatives aligned with national economic diversification strategies are modernizing insurance billing and claims systems. Over 60% of insurers in the UAE have adopted cloud-based billing platforms integrated with secure payment gateways. Oil & gas, construction, and health insurance sectors drive demand for automated premium and claims processing. Regulatory enhancements promoting fintech sandboxes and digital payment licensing have accelerated secure transaction frameworks. A major regional insurer recently implemented real-time claims reimbursement, reducing payout processing time by 30%. Consumer behavior indicates that more than 55% of urban policyholders prefer mobile or online premium payment channels, reflecting rapid fintech ecosystem expansion.

United States – 36% Market Share: Strong real-time payment infrastructure, over 78% digital premium adoption, and high enterprise-level integration of AI-driven payment systems drive Digital Insurance Payment Platforms Market leadership.

Germany – 11% Market Share: Advanced open banking compliance, strong regulatory enforcement, and high enterprise adoption of API-based billing systems position Germany as a key contributor to the Digital Insurance Payment Platforms Market.

The Digital Insurance Payment Platforms Market exhibits a moderately fragmented structure, with more than 80 active global and regional competitors offering billing automation, claims disbursement, payment orchestration, and fraud analytics solutions. The top five companies collectively account for approximately 52% of the total market share, indicating a competitive yet innovation-driven environment. Leading players differentiate through API-first architectures, embedded finance integrations, and AI-powered fraud detection engines capable of reducing false claims by up to 30%.

Strategic initiatives are heavily focused on partnerships between insurers and fintech providers. Over 60% of Tier-1 insurers have entered at least one strategic technology partnership since 2023 to accelerate real-time payment integration. Mergers and acquisitions activity has increased by nearly 18% year-over-year, targeting niche providers specializing in tokenization, cross-border settlement, and open banking compliance modules. Product launches increasingly emphasize cloud-native platforms, with over 70% of new deployments occurring in SaaS environments.

Competition is also shaped by cybersecurity capabilities, as insurers demand platforms capable of supporting 99.9% system uptime and advanced encryption standards. Vendors investing in blockchain-based smart contracts and AI-driven reconciliation systems are gaining competitive traction, particularly in North America and Europe. The market is progressively consolidating around technology depth, regulatory alignment, and multi-rail payment orchestration capabilities.

DXC Technology

Duck Creek Technologies

Majesco

Cognizant

Accenture

SAP SE

Oracle Financial Services

ACI Worldwide

FIS (Fidelity National Information Services)

Adyen

Mastercard

Visa

TCS (Tata Consultancy Services)

Technology innovation is central to the Digital Insurance Payment Platforms Market, with real-time payment (RTP) infrastructure integration emerging as a defining capability. More than 65% of Tier-1 insurers now support instant payment rails, reducing claims settlement cycles from 5–7 days to under 48 hours. API-driven payment orchestration layers enable insurers to integrate multiple banking rails, digital wallets, and card networks within a single dashboard, improving reconciliation efficiency by nearly 40%.

Artificial intelligence plays a pivotal role in fraud detection and predictive analytics. AI-based behavioral scoring systems analyze over 200 transaction variables, improving anomaly detection accuracy by up to 30%. Machine learning models are increasingly used for payment failure prediction, lowering transaction rejection rates by 15–20%. Blockchain-enabled smart contracts are being piloted for automated claims validation, potentially cutting documentation processing time by 35%.

Cloud-native SaaS deployments account for more than 70% of new platform implementations, enabling scalability and 99.9% uptime service levels. Tokenization and end-to-end encryption standards aligned with PCI-DSS compliance reduce exposure to data breaches. Biometric authentication and digital identity verification systems are gaining traction, particularly in Asia-Pacific, where mobile-based premium payments exceed 60% of total transactions. The integration of embedded finance capabilities within broker portals and super-app ecosystems is further transforming payment experiences, positioning technology as the primary competitive differentiator in the market.

• In October 2025, Guidewire Software announced an expanded strategic partnership with One Inc, bringing One Inc’s embedded claims payment solution ClaimsPay® into the Canadian property & casualty insurance market via the Guidewire Marketplace, enabling insurers to deliver fully digital, localized claims disbursements supporting Interac, virtual cards, PayPal, EFT and direct deposit options. This pre-built integration aims to accelerate cloud-first payment modernization. Source: www.businesswire.com

• In October 2025, Guidewire Software was named among the top 25 global fintech providers in the 2025 IDC FinTech Rankings, reinforcing its scale and innovation in cloud-based insurance platform transformation across underwriting, billing and claims management ecosystems. Source: www.ir.guidewire.com

• In April 2025, Guidewire Software announced a planned investment of USD 60 million to accelerate Platform enhancements and cloud transformation specifically for Japanese insurers, including enriched BillingCenter and PolicyCenter capabilities with localized features and integrations tailored to the Japanese market. Source: www.ir.guidewire.com

• In 2025, Stripe rolled out major product updates globally—including enhanced payment orchestration, expanded support for 125+ payment methods, AI-powered authorization optimization, and increased extensibility for enterprises—through its Sessions 2025 announcements, strengthening real-time payment handling, multi-rail integration, and fraud analytics across its platform. Source: www.stripe.com

The Digital Insurance Payment Platforms Market Report provides a comprehensive assessment of payment infrastructure solutions across premium collection, claims disbursement, billing automation, fraud detection, and API-based payment orchestration segments. The report evaluates over 5 primary product categories and analyzes their adoption across life, health, property & casualty, and commercial insurance lines. It examines integration models including cloud-native SaaS, hybrid deployments, and on-premise legacy modernization frameworks.

Geographic analysis covers North America, Europe, Asia-Pacific, South America, and Middle East & Africa, incorporating regional adoption rates, digital payment penetration levels, and regulatory compliance environments. The report includes evaluation of real-time payment integration, open banking APIs, blockchain smart contracts, AI-driven fraud detection engines, and biometric authentication technologies. Over 70% of global insurers transitioning toward automated billing ecosystems are assessed within enterprise adoption frameworks.

The scope further encompasses end-user insights across large carriers, mid-sized insurers, brokers, InsurTech startups, and reinsurance providers. It evaluates transaction density trends, cross-border payment growth exceeding 25% annually in selected corridors, and the increasing prevalence of mobile-first premium payments surpassing 60% in emerging markets. Additionally, the report explores ESG alignment through paperless billing initiatives and digital compliance mandates, offering decision-makers a structured view of competitive positioning, technology roadmaps, regulatory alignment, and long-term digital transformation pathways within the Digital Insurance Payment Platforms Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 485.0 Million |

| Market Revenue (2033) | USD 1,133.9 Million |

| CAGR (2026–2033) | 11.2% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Fiserv; Guidewire Software; Stripe; DXC Technology; Duck Creek Technologies; Majesco; Cognizant; Accenture; SAP SE; Oracle Financial Services; ACI Worldwide; FIS; Adyen; Mastercard; Visa; TCS |

| Customization & Pricing | Available on Request (10% Customization Free) |