Reports

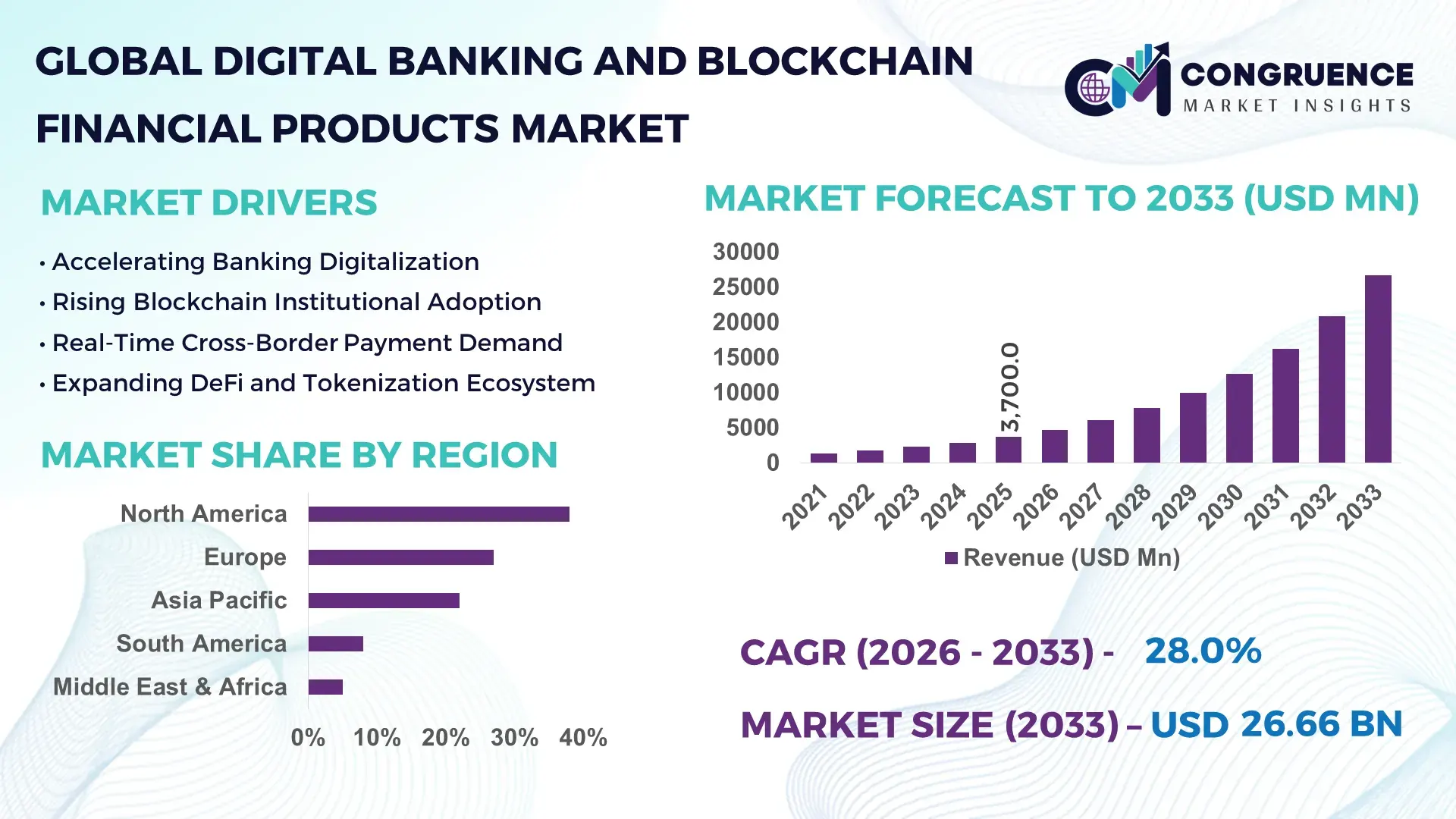

The Global Digital Banking and Blockchain Financial Products Market was valued at USD 3,700.0 Million in 2025 and is anticipated to reach USD 26,661.3 Million by 2033, expanding at a CAGR of 28% between 2026 and 2033, according to an analysis by Congruence Market Insights. The surge is underpinned by rapid digitization of financial services, wider acceptance of tokenized assets, and growing regulatory clarity around blockchain-based payments and digital assets.

The United States anchors global leadership through advanced cloud-based core banking capacity, high institutional investment in blockchain infrastructure, and large-scale deployment of real-time payment rails. In 2024–2025, U.S. banks and fintech firms collectively invested over USD 6–7 billion in distributed ledger pilots, custody platforms, and tokenization initiatives. More than 1,200 financial institutions tested or deployed blockchain-based settlement, while roughly 60% of major banks integrated APIs for open banking and embedded finance. Payment processing, trade finance, securities clearing, and asset tokenization are the most active applications, supported by robust data centers, high-performance nodes, and growing enterprise validator networks across New York, California, and Texas.

Market Size & Growth: USD 3.7 Bn in 2025 to USD 26.7 Bn by 2033, driven by accelerated tokenization of assets and real-time payments.

Top Growth Drivers: Digital wallet adoption 65%, settlement cost efficiency 40%, cross-border remittance speed 55%.

Short-Term Forecast: By 2028, average cross-border transaction time expected to fall by 35%.

Emerging Technologies: Layer-2 blockchains, privacy-preserving zero-knowledge proofs, and programmable smart contracts.

Regional Leaders (2033): North America USD 9.8 Bn (enterprise tokenization), Europe USD 7.1 Bn (regulatory-led adoption), Asia-Pacific USD 6.4 Bn (mobile-first banking).

Consumer/End-User Trends: Retail users favor wallets; enterprises prioritize tokenized treasury and settlement.

Pilot Example (2024): A global bank reduced reconciliation time by 45% using blockchain-based clearing.

Competitive Landscape: Leader ~22% share; key players include JPMorgan Onyx, Visa, Mastercard, Ripple, and Coinbase.

Regulatory & ESG Impact: MiCA-style frameworks and green-compute nodes gaining traction.

Investment & Funding: Over USD 18 Bn invested globally since 2022 across payments, custody, and DeFi rails.

Innovation & Outlook: Interoperable chains and programmable money to reshape wholesale finance.

Digital banking currently contributes the largest share through mobile platforms and API banking, while blockchain growth is fastest in payments, custody, and tokenized securities. Recent innovations include offline wallets, regulated stablecoins, and compliant DeFi liquidity pools. North America leads institutional consumption, Asia-Pacific leads retail usage, and Europe is shaping standards. Clearer regulations, lower energy consensus models, and deeper integration with cloud and AI are accelerating adoption toward a more interoperable, resilient financial ecosystem.

The Digital Banking and Blockchain Financial Products Market is becoming a core infrastructure layer for modern finance, blending programmable money, data transparency, and automated compliance. Strategically, it enables faster settlement, lower operational risk, and new revenue models around tokenized assets, embedded finance, and real-time treasury management. Large banks are migrating from legacy batch-processing systems toward API-first, cloud-native architectures integrated with distributed ledgers. For example, blockchain-based atomic settlement delivers ~40% faster clearing compared to traditional T+2 systems, while cutting manual reconciliation workloads by roughly 35–50%.

Regionally, Asia-Pacific dominates transaction volume, driven by super-app ecosystems and mobile wallets, while Europe leads in enterprise adoption with about 45% of major financial institutions piloting or using blockchain under regulated frameworks such as MiCA and DLT pilot regimes. North America remains the innovation hub for custody, tokenization, and institutional-grade stablecoins.

In the short term (by 2028), AI-driven risk monitoring combined with on-chain analytics is expected to reduce fraud-related payment losses by 20–25%, while smart contract automation could lower back-office costs by 30% for trade finance and securities processing.

From an ESG perspective, firms are committing to 30–50% reductions in blockchain energy intensity by 2030 through proof-of-stake networks, renewable-powered data centers, and carbon-tracked validators.

A practical micro-scenario occurred in 2024, when a multinational bank consortium used a shared blockchain rail for cross-border settlements and achieved a 48% reduction in settlement failures plus a 60% cut in processing time.

Looking ahead, the market is positioning itself as a pillar of financial resilience, compliance, and sustainable growth, where programmable finance, interoperable ledgers, and AI-driven governance create a faster, safer, and more transparent global financial system.

The Digital Banking and Blockchain Financial Products Market is shaped by converging forces of digital transformation, regulatory evolution, and technological interoperability. Banks are shifting from centralized legacy cores to modular cloud architectures that integrate real-time payments, open banking APIs, and distributed ledgers. Rising cross-border commerce and volatile currency environments are pushing institutions toward faster settlement rails and programmable liquidity. Meanwhile, regulators are moving from experimental sandboxes to formal frameworks, reducing uncertainty and encouraging institutional participation. Enterprise demand for data transparency, auditability, and automated compliance is accelerating adoption of smart contracts and on-chain analytics. At the same time, scalability constraints, cybersecurity risks, and fragmented standards create friction across jurisdictions. Competition between centralized fintech platforms and decentralized finance protocols is intensifying, forcing incumbents to modernize. Overall, the market is characterized by rapid innovation cycles, strategic partnerships between banks and blockchain providers, and a gradual shift from pilots to production-grade deployments across payments, custody, and securities markets.

Global commerce increasingly requires instant, always-on financial infrastructure. Traditional correspondent banking can take 2–5 days for cross-border transfers, involving multiple intermediaries and high fees. Digital banking platforms integrated with blockchain rails enable near-real-time settlement in minutes or seconds, reducing operational friction and liquidity lock-ups. Large corporations are adopting programmable treasury systems that automatically route payments across stablecoins, central bank digital currencies (CBDCs), and instant payment networks. Major banks report 30–50% reductions in reconciliation workloads when using shared ledger systems. Small and medium enterprises benefit from lower remittance costs—often falling from 6–8% to below 2%. Mobile wallet penetration exceeding 65% in many emerging markets further amplifies demand for interoperable digital rails. Governments are also expanding instant payment schemes, which increasingly interconnect with blockchain-based settlement layers, reinforcing a virtuous cycle of speed, transparency, and cost efficiency that accelerates market expansion.

Despite progress, inconsistent regulations across jurisdictions create compliance complexity for global banks and fintech firms. Licensing requirements, data residency rules, and varying treatment of stablecoins and digital assets force companies to maintain multiple regional architectures, raising costs and slowing scale. Cybersecurity remains a critical concern: high-profile smart contract exploits and wallet breaches have resulted in multi-billion-dollar losses in recent years, making risk-averse institutions cautious. Many banks still rely on legacy core systems that are difficult to integrate with blockchain networks, leading to lengthy modernization cycles. Interoperability gaps between chains also limit seamless liquidity movement. Additionally, concerns around illicit finance and sanctions compliance require heavy monitoring infrastructure, increasing operational overhead. The shortage of specialized blockchain talent further constrains deployment speed. Together, these factors delay full-scale adoption, pushing many institutions to remain in pilot mode rather than committing to large production rollouts.

Tokenization of real-world assets—such as bonds, real estate, and private equity—opens a multi-trillion-dollar opportunity for digital finance. Fractional ownership can broaden investor access while improving liquidity and transparency. Several governments are advancing CBDC pilots that can interoperate with commercial bank wallets and private blockchains, creating new settlement pathways for wholesale and retail transactions. Financial institutions can build programmable cash products that automate tax, compliance checks, and conditional payments. Trade finance stands to benefit significantly: blockchain-based document workflows can cut processing times from weeks to days, reducing fraud and paperwork costs. Interoperable bridges between payment networks and digital asset rails will enable seamless value transfer across borders. As regulatory clarity improves, institutional-grade custody and compliance tools are likely to unlock large-scale participation from asset managers, insurers, and pension funds, expanding the ecosystem far beyond payments into capital markets and treasury operations.

Many blockchain networks still face throughput and latency limitations during peak demand, leading to congestion and higher transaction fees. This unpredictability discourages mission-critical financial use cases that require guaranteed performance. Interoperability between different ledgers remains fragmented, forcing firms to build costly custom integrations or rely on bridges that can introduce security vulnerabilities. Enterprise-grade infrastructure—such as regulated custody, node hosting, and compliance analytics—requires substantial upfront investment. Banks must modernize legacy systems while maintaining uptime and regulatory compliance, a complex and capital-intensive undertaking. Energy consumption, although improving, continues to raise reputational concerns for some networks. Additionally, the absence of universally accepted standards for token formats, identity, and data sharing complicates cross-border collaboration. These technical and operational barriers slow scaling and increase the total cost of ownership for institutions pursuing digital banking and blockchain strategies.

Modular digital finance infrastructure gaining traction: Banks are adopting modular, prefabricated digital stacks where payment, identity, and settlement components are pre-built and assembled like “plug-and-play” systems. Around 55% of new digital transformation projects report faster deployment and lower integration costs using modular architectures. Automated API orchestration reduces manual coding hours by roughly 30–40%, while standardized smart contract libraries shorten product launch cycles across Europe and North America.

Real-time analytics embedded into ledgers: Institutions are embedding AI-driven monitoring directly into blockchain nodes, enabling continuous risk scoring and anomaly detection. Early adopters report 20–25% reductions in fraud alerts and 35% faster compliance reviews. On-chain dashboards are becoming standard for treasury teams managing multi-currency liquidity in real time.

Growth of regulated stablecoins and tokenized deposits: More than 40 banks globally are piloting tokenized deposits, allowing instant interbank transfers on private ledgers. Stablecoin transaction volumes grew by over 25% in 2024, driven by corporate treasury use and cross-border trade settlements that avoid traditional correspondent delays.

Interoperability and multi-chain banking: Financial institutions are increasingly using interoperability protocols that connect at least 3–5 different blockchains in a single workflow. Cross-chain routing has cut average settlement failures by 30%, while enabling banks to choose the most cost-efficient network for each transaction type.

The Digital Banking and Blockchain Financial Products Market is segmented by type, application, and end-user, reflecting the diverse ways financial institutions and consumers engage with next-generation digital finance solutions. By type, the market spans digital banking platforms, blockchain-based payment instruments, tokenized assets, digital wallets, and decentralized finance products, each addressing distinct operational and transactional needs. Application-wise, adoption is concentrated in payments and settlements, followed by lending, asset management, identity verification, and trade finance, where automation and transparency deliver measurable efficiency gains. From an end-user perspective, large financial institutions remain the primary adopters due to scale and regulatory readiness, while fintech firms, enterprises, and retail consumers are accelerating uptake through mobile-first and embedded finance models. This segmentation highlights a transition from pilot-led experimentation toward enterprise-wide deployment, with usage patterns increasingly shaped by real-time processing demands, regulatory compliance requirements, and consumer preference for seamless, always-on financial services.

The market by type includes Digital Banking Platforms, Blockchain-Based Payment and Settlement Products, Tokenized Assets & Securities, Digital Wallets & Stablecoins, and Decentralized Finance (DeFi) Products. Digital banking platforms currently represent the leading type, accounting for approximately 38% of total adoption, supported by widespread deployment of mobile banking apps, cloud-native core systems, and API-based open banking frameworks across retail and corporate banking. These platforms are foundational for customer onboarding, account management, and omnichannel service delivery.

Blockchain-based payment and settlement products follow closely, holding around 27% adoption, driven by demand for faster cross-border transfers and reduced reconciliation complexity. Tokenized assets and securities represent the fastest-growing type, expanding at an estimated 32% CAGR, as financial institutions pilot on-chain bonds, funds, and real-world asset tokenization to improve liquidity and settlement efficiency. Growth is fueled by institutional-grade custody solutions and regulatory sandboxes.

Digital wallets and stablecoins, along with DeFi products, collectively account for the remaining 35%, serving niche but expanding use cases such as peer-to-peer payments, programmable treasury, and decentralized liquidity access.

In 2025, a central bank–regulated pilot enabled tokenized government bonds to be settled on a blockchain network, reducing settlement cycles from two days to same-day processing for institutional participants.

By application, the payments and settlements segment dominates, representing nearly 41% of total usage, as institutions prioritize speed, cost efficiency, and transparency in domestic and cross-border transactions. Digital banking interfaces combined with blockchain rails enable near-real-time settlement and automated reconciliation, making this the most mature and widely deployed application.

Lending and credit management applications account for about 19%, leveraging digital onboarding, automated credit scoring, and smart contracts for disbursement and repayment tracking. Asset and wealth management, including custody and tokenized investment products, is the fastest-growing application area, expanding at approximately 29% CAGR, supported by rising institutional interest in fractional ownership and on-chain fund administration.

Other applications—such as identity verification, compliance automation, and trade finance—together contribute roughly 21%, addressing documentation-heavy workflows and fraud reduction. In 2025, over 40% of global enterprises reported piloting blockchain-enabled payment solutions for cross-border supplier settlements. More than 58% of digitally active consumers indicated higher usage of mobile wallets integrated with banking apps for everyday transactions.

In 2025, a multinational trade corridor implemented blockchain-based trade finance documentation, cutting average processing times by over 50% and significantly reducing manual paperwork.

End-user adoption is led by large banks and financial institutions, which account for approximately 46% of market usage, reflecting their scale, regulatory readiness, and need for high-throughput transaction infrastructure. These institutions deploy digital banking cores and private or permissioned blockchains for payments, custody, and interbank settlement.

Fintech companies are the fastest-growing end-user group, expanding at an estimated 34% CAGR, driven by their agility, API-first models, and focus on user-centric digital experiences such as embedded finance, neobanking, and cross-border remittances. Enterprises and corporates represent about 18%, adopting blockchain-enabled treasury, payroll, and supplier payment solutions to improve cash-flow visibility.

Retail consumers and SMEs, together contributing the remaining 36%, are accelerating adoption through mobile wallets, instant payments, and digital lending platforms: In 2025, more than 62% of Gen Z users preferred app-based digital banks over traditional branches. Approximately 44% of SMEs in emerging markets reported using blockchain-enabled payment tools to manage international transactions.

In 2025, a consortium of SMEs adopted a blockchain-based invoicing and payment platform, achieving a 30% reduction in payment delays and improved working-capital cycles.

North America accounted for the largest market share at 38% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 28% between 2026 and 2033.

The regional landscape reflects divergent adoption patterns shaped by regulatory maturity, digital infrastructure, and financial innovation ecosystems. North America leads in enterprise-grade blockchain deployment, with over 1,200 financial institutions piloting distributed ledger solutions and nearly 60% of Tier-1 banks integrating tokenized settlement tools. Europe follows with approximately 27% share, driven by regulatory frameworks such as MiCA, digital euro pilots, and strong sustainability mandates across Germany, France, and the UK. Asia-Pacific holds around 22% share but dominates in transaction volume, supported by 65% mobile wallet penetration, rapid fintech scaling in India, and China’s extensive digital yuan ecosystem. South America contributes roughly 8%, with Brazil emerging as a hub for instant payments and crypto-enabled remittances. The Middle East & Africa (5%) is advancing through sovereign blockchain initiatives, digital identity programs, and financial inclusion strategies across the UAE, Saudi Arabia, and South Africa.

North America represents roughly 38% of the global market, anchored by high institutional spending, advanced cloud infrastructure, and deep capital markets integration. Demand is primarily driven by banking, capital markets, healthcare finance, and insurance, where secure data sharing and real-time settlements are critical. Over 70% of large U.S. banks now use API-driven digital cores, while more than 45% are running blockchain pilots for custody, collateral management, or securities settlement. Regulatory clarity from the SEC and OCC, along with state-level crypto-friendly policies in Wyoming and New York’s BitLicense framework, have accelerated compliant adoption. Technologically, banks are shifting toward hybrid models combining permissioned ledgers with public blockchains, supported by AI-driven compliance monitoring and zero-knowledge privacy tools. JPMorgan’s Onyx platform exemplifies regional leadership, processing billions of dollars in intraday settlements via blockchain rails. Consumer behavior skews toward high enterprise adoption, particularly in healthcare and finance, where secure interoperability and auditability are prioritized over retail experimentation.

Europe commands approximately 27% of the market, with Germany, the UK, France, the Netherlands, and Switzerland as key innovation centers. Regulatory bodies such as the European Central Bank (ECB) and European Securities and Markets Authority (ESMA) are driving structured experimentation through DLT pilot regimes and digital euro initiatives. Sustainability rules and taxonomy-aligned finance have pushed banks to adopt energy-efficient blockchain networks, with over 40% of new deployments favoring proof-of-stake systems. Adoption of tokenized bonds, carbon credits, and on-chain funds is rising, particularly in Germany and France, where major banks are issuing digitally native securities. The UK is advancing stablecoin regulation and sandbox programs for payments innovation. Local players like Societe Generale–Forge are building institutional custody and tokenization platforms. Consumer behavior reflects strong regulatory influence—European enterprises demand explainable, auditable, and compliant digital banking systems before scaling production deployments.

Asia-Pacific is the fastest-expanding region by volume, with adoption concentrated in China, India, Japan, South Korea, and Singapore. The region accounts for nearly 22% of global share but leads in daily transaction throughput due to widespread mobile payments and super-app ecosystems. China’s digital yuan trials now cover over 260 million users, integrating e-commerce, transit, and government disbursements. India is scaling UPI-linked digital banking while fintech firms experiment with blockchain-based remittances. Japan and Singapore are hubs for institutional tokenization and regulated stablecoins. Infrastructure investment in data centers, 5G, and cloud banking platforms is accelerating enterprise integration. Local leaders such as Ant Group and GMO Internet are building permissioned blockchain rails for supply-chain finance and digital identity. Consumer behavior is mobile-first—growth is fueled by e-commerce, gig economy payments, and AI-powered financial apps that blend wallets, lending, and investment services.

South America holds roughly 8% of the market, led by Brazil and Argentina, with emerging activity in Colombia, Chile, and Mexico. Brazil’s Pix instant payment system has exceeded 150 million users, acting as a gateway for blockchain-linked remittances and digital wallets. Argentina’s inflationary environment has driven high adoption of stablecoins and cross-border digital transfers. Governments are exploring blockchain for public procurement, land registries, and tax transparency. Energy-rich nations are also leveraging low-cost renewable power for blockchain infrastructure hosting. Local fintechs such as Mercado Pago are integrating crypto wallets with traditional banking services, enabling millions of users to hold, transfer, and spend digital assets seamlessly. Consumer behavior is closely tied to media, language localization, and mobile accessibility, with strong demand for Spanish- and Portuguese-native financial interfaces.

The Middle East & Africa region represents about 5% of the market but is rapidly modernizing through smart-city programs, digital identity, and blockchain-enabled government services. The UAE and Saudi Arabia lead adoption, focusing on trade finance, logistics payments, and cross-border settlements aligned with Vision 2030 and digital economy strategies. South Africa is emerging as a fintech hub, with growing blockchain use in remittances and mobile banking. Energy and construction sectors are integrating digital payments for large infrastructure projects, while free-trade zones in Dubai and Abu Dhabi are fostering crypto and tokenization ecosystems. Regulators are introducing clear frameworks for virtual assets, custodianship, and stablecoins. Local players like Emirates NBD and Hub71 fintech startups are piloting blockchain-based treasury and supply-chain finance solutions. Consumer behavior favors secure, mobile-first digital wallets, especially among young, tech-savvy urban populations.

United States – 30% Market Share: Strong institutional investment, deep capital markets, and large-scale blockchain infrastructure deployment.

China – 18% Market Share: Massive digital payment ecosystem and nationwide digital currency pilots driving adoption of programmable finance.

The Digital Banking and Blockchain Financial Products Market features a dynamic and competitive environment with over 120 active competitors globally, ranging from traditional financial institutions to specialized fintech and blockchain technology firms. The market structure is moderately fragmented, with the top 5 companies holding an estimated combined share of 42–45% through offerings such as blockchain-enabled payment systems, tokenized financial products, and digital asset custody services. Strategic initiatives are reshaping the competitive landscape: leading banks and technology firms are forming partnerships, launching tokenized products, and acquiring niche players to expand infrastructure capabilities.

In 2025, major incumbents accelerated product innovations: Mastercard and MoonPay partnered to enable stablecoin payments across more than 150 million Mastercard acceptance points worldwide, bridging traditional card networks with blockchain payments. J.P. Morgan Asset Management launched the My OnChain Net Yield Fund (MONY) on a public blockchain, seeding it with USD 100 million to offer institutional investors tokenized money-market exposure. Meanwhile, UniCredit issued its first tokenized structured note on a public blockchain, digitizing securities issuance workflows and lowering operational overhead. These developments illustrate how competitive positioning increasingly depends on cross-industry collaboration, blockchain integrations, and expansion into tokenization services that appeal to institutional and retail segments alike. Innovation trends such as real-time settlement rails, interoperability protocols, and programmable smart contracts are essential differentiators that influence competitive advantage and market share distribution. The overall competitive climate emphasizes agility, integrated digital platforms, and ecosystem partnerships that span traditional banking and decentralized finance technologies.

Circle Internet Group

Coinbase Global

Ripple Labs

SoFi

MoonPay

Fiserv

Revolut

BNP Paribas Digital Finance Division

HSBC Digital Asset Services

UniCredit Blockchain Securities Unit

Chainlink (Blockchain Oracle Infrastructure)

Block.one (EOS ecosystem)

Aave (DeFi Lending Protocol)

Paxos Trust Company

Franklin Templeton Digital Markets

Franklin Digital Finance

The Digital Banking and Blockchain Financial Products Market is increasingly shaped by technologies that enhance scalability, security, interoperability, and automation across financial services. Distributed Ledger Technology (DLT) remains central, enabling tamper-evident transaction records and automated settlement through smart contracts that eliminate manual reconciliation, reduce errors, and compress settlement cycles. Interoperability protocols and blockchain oracles facilitate real-world data integration, bridging traditional finance systems with on-chain ecosystems to support programmable finance, real-time pricing, and cross-chain asset transfers.

Stablecoins and programmable digital cash are core infrastructure elements; by late 2025, stablecoin supply exceeded $230 billion in market value, serving as an “always-on” settlement layer for cross-border payments and corporate treasury operations. Native blockchain oracles such as Chainlink enable trusted price feeds, compliance data distribution, and proof-of-reserve checks for tokenized instruments across more than 2,000 applications and financial systems.

Tokenization platforms supported by enterprise wallets and custodial services enable the issuance and transfer of real-world assets—including bonds, money-market funds, and structured notes—directly on public and permissioned blockchains. Hybrid infrastructure models combine centralized cores with blockchain rails, offering API-driven access to digital products while satisfying regulatory and audit requirements. Secure hardware modules and privacy protocols enhance data protection and consumer confidence in digital finance systems.

Artificial Intelligence (AI) and Machine Learning (ML) bolster fraud detection, credit scoring, and compliance automation, reducing manual risk management cycles by significant margins. Identity and access management systems leverage decentralized identifiers (DIDs) to strengthen KYC/AML processes and support portable, user-controlled digital identity credentials. Modular APIs and cloud-native architectures further accelerate developer innovation, enabling financial institutions and fintechs to compose tailored digital banking experiences that integrate seamlessly with blockchain-based services, fostering rapid product iteration and ecosystem growth.

• In May 2025, Mastercard and MoonPay partnered to enable stablecoin payments globally, allowing enterprises and consumers to pay and be paid using stablecoin balances via Mastercard-branded cards accepted at over 150 million locations worldwide. Source: www.mastercard.com

• In December 2025, J.P. Morgan Asset Management launched the My OnChain Net Yield Fund (MONY), a tokenized money-market fund on the Ethereum blockchain seeded with USD 100 million, providing qualified investors access to tokenized short-term debt instruments and stablecoin settlement. Source: www.theblock.co

• In 2025, UniCredit issued its first fully tokenized structured note on a public blockchain, streamlining issuance and custody processes for professional wealth management clients and marking a key advancement in European blockchain securities issuance. Source: www.reuters.com

• In September 2025, BNP Paribas and HSBC joined the privacy-focused Canton Network blockchain, expanding institutional access to multi-asset tokenized transactions and enhancing liquidity for digital asset markets with over USD 3.6 trillion in tokenized assets on the network. Source: www.hoganlovells.com

The Digital Banking and Blockchain Financial Products Market Report provides a comprehensive analysis of the intersection between digital banking platforms and blockchain-enabled financial products, covering the full spectrum of technologies, applications, and end-user segments shaping modern finance. The scope includes detailed segment breakdowns by type (digital banking platforms, blockchain payments and settlements, digital wallets and stablecoins, tokenized assets, and decentralized finance products), along with application areas such as cross-border payments, treasury and liquidity management, lending, identity and compliance solutions, and trade finance automation. Geographic coverage spans key regions including North America, Europe, Asia-Pacific, South America, and Middle East & Africa, assessing adoption patterns, infrastructure trends, regulatory environments, and consumer behavior variations in each market.

The report also explores the role of emerging technologies—such as distributed ledger protocols, smart contracts, blockchain oracles, digital identity frameworks, and AI-powered compliance engines—in enabling secure, scalable, and interoperable financial ecosystems. Industry focus areas include institutional investor adoption of tokenized funds, retail consumer uptake of digital banking and wallet services, neobanking innovation, and enterprise blockchain integration for real-time settlement. Competitive analysis includes profiles of major players driving innovation, strategic partnerships, product launches, and cross-industry collaborations impacting market positioning. Niche segments such as CBDC integration, cross-chain liquidity protocols, and embedded finance models are also examined, providing decision-makers with insights into market breadth, operational challenges, and future growth opportunities across the digital banking and blockchain finance landscape.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 3,700.0 Million |

| Market Revenue (2033) | USD 26,661.3 Million |

| CAGR (2026–2033) | 28% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Visa, Mastercard, J.P. Morgan, Circle Internet Group, Coinbase Global, Ripple Labs, SoFi, MoonPay, Fiserv, Revolut, BNP Paribas Digital Finance Division, HSBC Digital Asset Services, UniCredit, Chainlink, Block.one ,Aave, Paxos Trust Company, Franklin Templeton Digital Markets, Franklin Digital Finance |

| Customization & Pricing | Available on Request (10% Customization Free) |