Reports

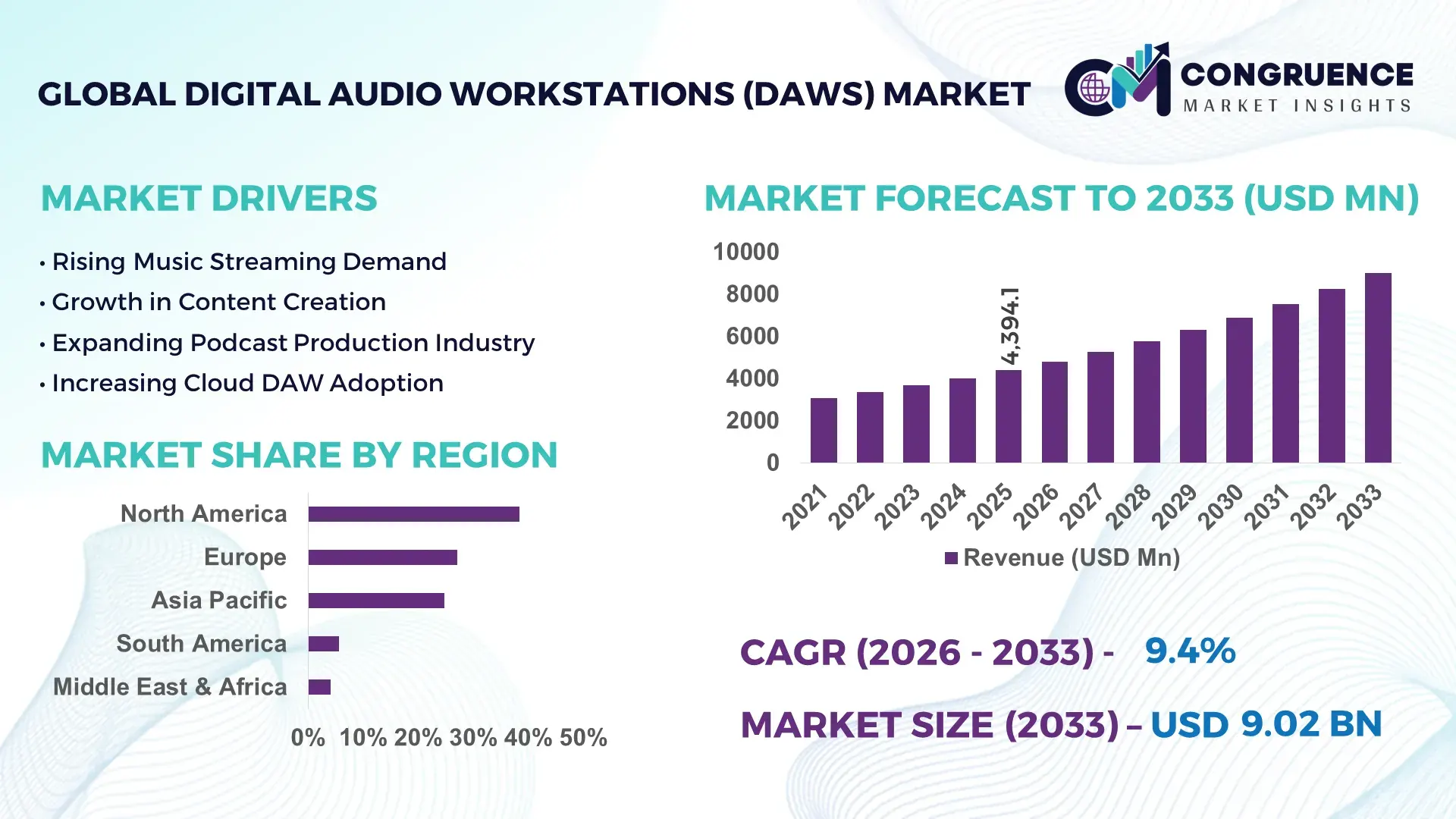

The Global Digital Audio Workstations (DAWs) Market was valued at USD 4,394.1 Million in 2025 and is anticipated to reach a value of USD 9,015.9 Million by 2033 expanding at a CAGR of 9.4% between 2026 and 2033. Growth is being driven by the rapid integration of AI-assisted audio editing, cloud-based collaboration workflows, and expanding creator-economy production ecosystems across music, gaming, and streaming industries.

The United States remains the dominant country in the market, accounting for approximately 34% of global software audio production activity, supported by over 120,000 professional recording facilities, strong adoption across music, gaming, and film industries, and continued investment in AI-powered content creation platforms. Compared with Germany, which represents nearly 8% of professional audio software usage, the U.S. benefits from a creator economy exceeding 50 million active participants and higher cloud-audio workflow penetration exceeding 45%. The country also benefits from ongoing digital media expansion linked to post-pandemic remote production models.

Vendors prioritizing AI-enhanced workflows, subscription ecosystems, and creator-focused cloud infrastructure are securing stronger competitive positioning in high-value professional and prosumer segments.

Market Size & Growth: USD 4,394.1 million in 2025 reaching USD 9,015.9 million by 2033, supported by a 9.4% CAGR and accelerating adoption of AI-assisted audio production tools.

Top Growth Drivers: AI-enabled editing adoption (+38%), cloud collaboration usage (+31%), and independent creator expansion (+27%) are reshaping production workflows.

Short-Term Forecast: By 2028, audio editing cycle times are projected to decline by 25% through automation and intelligent workflow optimization.

Emerging Technologies: AI mastering, generative audio creation, and real-time cloud production platforms are improving production efficiency by over 30%.

Regional Leaders: North America exceeds USD 3.0 billion, Europe approaches USD 2.2 billion, and Asia-Pacific surpasses USD 2.5 billion, driven by streaming and gaming content expansion.

Consumer/End-User Trends: More than 60% of independent creators now utilize subscription-based audio production platforms and collaborative cloud environments.

Pilot/Case Example: In 2024, AI-powered mastering deployments reduced post-production workloads by nearly 35% across selected commercial studios.

Competitive Landscape: Leading vendors collectively control approximately 55% of the market, with Avid, Steinberg, Apple, Ableton, and PreSonus maintaining strong product ecosystems.

Regulatory & ESG Impact: Cloud-first production environments lowered on-site infrastructure requirements by nearly 20%, supporting digital efficiency objectives.

Investment & Funding: Over USD 1.2 billion has been directed toward creator-tech, audio software, and digital content infrastructure partnerships since 2023.

Innovation & Future Outlook: Voice-driven editing, AI co-production tools, and integrated immersive-audio workflows are defining next-generation competitive differentiation.

The Digital Audio Workstations (DAWs) Market is increasingly shaped by demand from music streaming, podcast production, gaming audio, virtual events, and creator-led content ecosystems. Recent innovations include AI-powered mastering, automated mixing engines, and browser-based collaborative production environments. Nearly 40% of new professional audio workflows now incorporate cloud-enabled features, while expanding digital content exports and distributed production teams continue to reinforce demand, creating a strong foundation for strategic market evolution.

Digital Audio Workstations are becoming strategically important as audio content shifts from traditional studio environments toward creator-centric, cloud-connected, and AI-assisted production ecosystems. Competition increasingly revolves around workflow efficiency, ecosystem integration, and subscription-based user retention. The market is also benefiting from broader digital infrastructure modernization, with remote production environments becoming standard across music, broadcasting, gaming, and digital media industries.

Modern AI-enabled DAWs can reduce editing and mastering workloads by approximately 30–40% compared with conventional manual workflows, allowing producers to accelerate content delivery while lowering operational costs. The United States leads in professional deployment scale and software innovation, while countries such as South Korea and Germany are advancing adoption through gaming, broadcasting, and digital media production investments. Over 60% of independent creators now rely on digital-first production workflows, highlighting the shift away from traditional studio dependency.

A practical example is the integration of cloud collaboration platforms that enable geographically distributed teams to edit, mix, and finalize projects in real time. Vendors are expanding strategic partnerships with streaming platforms, plugin developers, and AI technology providers to strengthen ecosystem value. Over the next two to three years, adoption of AI-assisted production, immersive audio formats, and browser-based workflows is expected to intensify, positioning advanced DAW platforms as critical competitive assets for content creation and digital media enterprises.

The strongest growth catalyst is the structural transformation of digital content production workflows through AI-enhanced audio creation and editing technologies. More than 60% of professional creators now utilize automated editing features, while AI-assisted mastering can reduce production time by nearly 35%. The global creator economy has expanded by over 25% during the past three years, increasing demand for scalable production platforms. The rapid growth of podcasting, gaming audio, and streaming content has further intensified software adoption. As distributed production becomes standard across the United States and the United Kingdom, vendors are expanding cloud-based collaboration capabilities. This shift improves productivity, shortens content release cycles, and encourages companies to invest in advanced audio intelligence, subscription ecosystems, and integrated production environments.

Market expansion continues to face structural limitations from interoperability challenges, plugin compatibility issues, and premium software pricing. Professional-grade DAW deployments often require additional plugin investments representing 20–40% of total workflow expenditure. Approximately 35% of independent creators report compatibility constraints when collaborating across multiple software environments. In Japan and Germany, enterprise audio teams frequently manage diverse software stacks that increase integration complexity and support costs. The shift toward subscription licensing has also generated resistance among some professional users, with nearly 30% preferring perpetual ownership models. To reduce risk, vendors are expanding cross-platform support, enhancing open-standard integrations, and developing bundled software ecosystems that improve workflow continuity while lowering operational friction.

Significant opportunity exists in immersive audio production, cloud-native workflows, and AI-generated content ecosystems. Adoption of spatial and immersive audio formats has increased by more than 28% among premium media producers, while cloud-based collaboration usage has expanded by nearly 40% since 2022. South Korea and India are emerging as attractive markets due to strong growth in gaming, digital entertainment, and creator-driven media production. The evolution of browser-based DAWs enables deployment without high-performance local hardware, reducing infrastructure costs by approximately 25%. Companies are increasing R&D investments in generative audio technologies, real-time collaboration engines, and creator monetization ecosystems. A non-obvious opportunity lies in enterprise podcasting and corporate media production, where workflow automation delivers measurable productivity advantages.

The primary long-term challenge involves scaling sophisticated production capabilities while maintaining usability, security, and platform consistency. More than 45% of professional audio teams now operate across distributed environments, increasing synchronization and asset-management complexity. Cybersecurity risks affecting cloud-based creative platforms have risen by approximately 20% as remote collaboration expands. Additionally, advanced AI features require specialized training, and nearly one-third of users report skill gaps when adopting automated production tools. In countries such as the United States and Canada, organizations face growing pressure to manage large audio asset libraries across multiple cloud environments. Vendors must address these issues through stronger infrastructure investments, workforce enablement programs, and secure collaboration architectures to ensure long-term competitiveness and sustainable deployment performance.

AI-Powered Production Automation AI-assisted editing, mastering, and audio restoration tools have moved into mainstream production workflows, with adoption among professional creators exceeding 45% and automated mastering usage increasing by nearly 35% over the past two years. Labor shortages in audio engineering and rising content volumes are accelerating deployment. Companies are integrating machine learning engines directly into DAW environments, reducing editing cycles by approximately 30% while improving workflow consistency and lowering production bottlenecks across music, podcasting, and digital media operations.

Cloud-Native Collaboration Expansion Cloud-based project collaboration has grown by more than 40% since 2023 as distributed production teams become standard across the United States and Europe. Nearly 50% of independent creators now exchange project files through cloud-connected workflows rather than local infrastructure. This transition shortens project turnaround times by approximately 25% and improves resource utilization. Vendors are expanding cloud partnerships, enhancing real-time synchronization capabilities, and restructuring software architectures to support scalable multi-user production environments.

Spatial Audio Workflow Integration Demand for immersive content has increased significantly, with spatial audio deployment among premium streaming and gaming producers rising by over 30%. More than 20% of newly released digital entertainment projects now incorporate immersive audio formats. The transition is reshaping plugin ecosystems, production pipelines, and monitoring requirements. Software developers are responding through dedicated spatial mixing tools, expanded hardware compatibility, and strategic partnerships with content distribution platforms seeking differentiated user experiences.

Creator Economy Platform Consolidation Subscription-based audio production ecosystems now account for nearly 60% of new software onboarding activity, reflecting a shift away from perpetual-license models. Creator-focused content production volumes have expanded by more than 25%, while integrated marketplace adoption for plugins and audio assets has increased by approximately 28%. A non-obvious trend is the consolidation of educational resources, monetization tools, and production software into unified platforms. Companies are strengthening ecosystem retention through bundled services, community partnerships, and integrated content distribution capabilities.

Software-based DAWs remain the leading segment, accounting for approximately 68% of total deployments due to superior scalability, lower infrastructure requirements, and seamless integration with third-party plugins, cloud workflows, and AI-powered production tools. Their flexibility enables adoption across professional studios, independent creators, broadcasters, and educational institutions. Continued migration toward subscription-based licensing and cloud-enabled environments has reinforced software-centric deployment models. Vendors are expanding plugin ecosystems, automation capabilities, and collaborative features to strengthen customer retention and workflow efficiency. Cloud-Based DAWs represent the fastest-growing segment as distributed production environments become increasingly common. Adoption has increased by nearly 40% since 2023, supported by remote collaboration requirements and browser-accessible production capabilities. Traditional On-Premise DAWs continue to maintain relevance among high-end commercial studios requiring low-latency processing and advanced hardware integration, while Hybrid DAWs are gaining traction among enterprise media teams seeking workflow flexibility. Companies are directing investments toward cloud synchronization, AI integration, and cross-device interoperability, reflecting changing customer priorities. This shift is reshaping product development roadmaps and increasing competitive focus on ecosystem connectivity rather than standalone software functionality.

Music Production continues to be the leading application segment, representing approximately 52% of professional DAW utilization. Demand remains concentrated among recording artists, commercial studios, independent creators, and music publishers seeking efficient content creation workflows. Increased adoption of AI-assisted mixing and mastering has reduced production timelines by nearly 30%, encouraging wider deployment among both professional and prosumer users. Companies are expanding software capabilities through advanced audio processing, virtual instruments, and integrated content management tools to support growing production volumes. Podcasting and Digital Content Creation is emerging as the fastest-growing application area, supported by expanding creator economies and digital media consumption trends. Usage within this segment has increased by over 35% in recent years as businesses, educators, and content creators invest in audio-first engagement strategies. Broadcasting and Film Post-Production remain established segments requiring sophisticated editing environments, while Gaming Audio Production is strengthening through demand for immersive sound design and interactive audio experiences. Vendors are scaling cloud collaboration, automation tools, and workflow integration features to address evolving operational requirements across these diverse applications.

Professional Studios and Content Creators represent the dominant end-user group, accounting for approximately 48% of overall platform utilization. Demand concentration is driven by intensive production requirements, large project volumes, advanced plugin ecosystems, and continuous workflow optimization needs. More than 55% of commercial audio projects are produced within professional creator environments, reinforcing their importance as the industry's primary purchasing segment. Vendors continue developing premium production suites, enterprise-grade collaboration tools, and advanced audio processing capabilities to address professional workflow demands. Independent Creators and Prosumers constitute the fastest-growing end-user segment, with adoption expanding by nearly 38% over the past three years. Lower entry barriers, subscription-based pricing models, and access to AI-assisted production tools are accelerating participation. Media & Broadcasting Organizations remain significant users due to content volume requirements, while Educational Institutions increasingly deploy DAWs to support digital media curricula and workforce development programs. Companies are responding through flexible pricing structures, creator-focused ecosystems, educational partnerships, and cloud-enabled production environments. Future demand is increasingly shifting toward scalable platforms that balance professional-grade functionality with accessibility and affordability.

North America accounted for the largest market share at 38.4% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11.2% between 2026 and 2033.

North America maintains the largest share of the Digital Audio Workstations (DAWs) Market, supported by its concentration of professional recording studios, streaming-content producers, gaming companies, and media enterprises. The region accounts for approximately 38.4% of global adoption, with the United States representing the majority of enterprise deployments. Strong integration of AI-powered editing, automated mastering, and cloud collaboration platforms continues to reshape production workflows. More than 60% of professional content creators in the region utilize advanced automation tools within audio production environments. Strategic partnerships between software developers, cloud providers, and content distribution platforms are accelerating workflow modernization while improving production scalability and operational efficiency across commercial audio sectors.

United States Market Outlook: The United States serves as the innovation center for advanced audio production technologies, supported by a creator economy exceeding 50 million participants and a highly developed digital entertainment ecosystem. The country hosts a significant concentration of professional recording facilities, gaming studios, and streaming-content producers. More than 45% of professional audio workflows now incorporate cloud-based collaboration capabilities, enabling distributed production teams to operate efficiently. Continued investment in AI-enabled content tools, digital media infrastructure, and creator-focused software ecosystems reinforces the country's leadership in next-generation audio production technologies.

Europe remains a strategically important market, accounting for approximately 27.1% of global demand. The region benefits from a strong concentration of music production companies, broadcast networks, audio engineering firms, and content creation enterprises. Studio modernization initiatives and increasing deployment of cloud-connected production environments are driving operational upgrades. Adoption of immersive audio production workflows has increased by nearly 30% among premium media producers. Regulatory emphasis on digital innovation and creative-sector competitiveness is encouraging investments in advanced software platforms. Companies are expanding collaborative production capabilities and integrating AI-assisted editing tools to enhance productivity while addressing evolving content-production requirements.

Germany Market Outlook: Germany represents the region's most influential market due to its established audio engineering expertise, advanced media infrastructure, and strong software development ecosystem. The country accounts for roughly 20% of Europe's professional audio software utilization and maintains a robust presence in broadcasting, music production, and digital entertainment. German enterprises are actively deploying AI-assisted editing platforms and spatial audio technologies to improve production efficiency. Ongoing investment in digital media infrastructure and professional training programs continues to strengthen the country's position as a leading hub for audio production innovation.

Asia-Pacific is emerging as the fastest-growing regional market, supported by rapid digital content creation, gaming industry expansion, and increasing cloud infrastructure deployment. The region accounts for approximately 24.8% of global market activity and continues to strengthen its competitive position through rising adoption among independent creators and digital media enterprises. More than 40% growth in creator-focused platform usage has been observed across key markets over the past several years. Expanding broadband infrastructure, smartphone penetration, and streaming-content consumption are accelerating software deployment. Vendors are increasing localization efforts, strategic partnerships, and cloud-based service offerings to capture rising demand from emerging creator communities and professional production teams.

China Market Outlook: China remains the largest market within Asia-Pacific due to its vast digital entertainment sector, large creator base, and extensive technology infrastructure. The country hosts one of the world's most active livestreaming, gaming, and short-form content ecosystems. More than 70% of digital content creators rely on software-based production tools for audio processing and content enhancement. Domestic technology providers and international vendors are investing heavily in AI-powered audio applications, cloud collaboration environments, and creator-focused platforms to support expanding production requirements and platform monetization opportunities.

South America is experiencing steady market expansion as digital media production becomes increasingly professionalized across entertainment, broadcasting, and creator-economy sectors. The region contributes approximately 5.6% of global market demand and benefits from rising investment in digital content infrastructure. Podcast production and independent music creation have expanded significantly, with creator-platform participation increasing by nearly 25% in recent years. Infrastructure disparities and software affordability remain execution constraints, yet growing subscription-based software adoption is improving accessibility. Vendors are expanding regional partnerships and localized pricing models to support broader market penetration while strengthening engagement with independent creators and small production businesses.

Brazil Market Outlook: Brazil represents the region's largest and most strategically important market due to its scale, digital content production activity, and rapidly expanding creator ecosystem. The country leads South America in music streaming consumption and podcast production volume. More than 40% of professional audio creators have adopted cloud-enabled production workflows, improving collaboration and content turnaround times. Strong engagement across music, gaming, and influencer-driven media sectors continues to drive demand for advanced audio editing, mastering, and content-production platforms tailored to local market requirements.

The Middle East & Africa market is gradually strengthening through investments in digital infrastructure, creative industries, and media-sector modernization initiatives. The region accounts for approximately 4.1% of global market participation and is benefiting from increased deployment of cloud-based production technologies. Government-backed digital transformation programs and media diversification strategies are supporting growth in content creation capabilities. Adoption of collaborative production platforms has increased by nearly 20% among commercial media organizations. Companies are responding by expanding regional partnerships, improving cloud accessibility, and introducing localized solutions designed to address evolving enterprise and creator requirements.

United Arab Emirates Market Outlook: The United Arab Emirates serves as the region's primary innovation hub for digital media and content production. Strong government support for creative industries, advanced telecommunications infrastructure, and growing investment in media technology have strengthened market competitiveness. More than 30% of newly established digital media businesses utilize cloud-based production ecosystems for audio and content creation workflows. The country's expanding entertainment, broadcasting, and digital marketing sectors continue to attract technology providers seeking strategic access to high-value media and content-production opportunities across the broader Middle East.

The Digital Audio Workstations (DAWs) Market is characterized by competition between established platform leaders such as Avid, Steinberg, Apple, Ableton, and PreSonus/Fender, and emerging challengers including Cockos (REAPER), Bitwig, and cloud-native audio production providers. The top five players collectively control approximately 55–60% of market activity, creating a moderately concentrated competitive structure. Competition is centered on AI-powered workflow automation, ecosystem integration, cloud collaboration, and subscription-based service models rather than price alone. AI-assisted production features can reduce editing workloads by 30–40%, while cloud-enabled collaboration improves project turnaround times by nearly 25%. Leading vendors are expanding through technology partnerships, immersive audio capabilities, creator-focused ecosystems, and integrated plugin marketplaces. The competitive shift is increasingly driven by AI-enabled production, browser-based workflows, and platform consolidation that combines software, content assets, and creator services. Entry barriers remain significant due to entrenched user ecosystems, plugin compatibility requirements, and high switching costs affecting more than 50% of professional users. Winning requires superior workflow efficiency, ecosystem depth, AI innovation, and seamless cross-platform collaboration capabilities.

Steinberg Media Technologies GmbH

Ableton AG

Apple Inc.

Cockos Incorporated

Bitwig GmbH

Image-Line Software

MAGIX Software GmbH

Harrison Audio LLC

MOTU Inc.

Tracktion Corporation

Acoustica Inc.

Adobe Inc.

Soundtrap AB

Artificial intelligence is becoming the most influential technology layer within Digital Audio Workstations. AI-powered mastering, stem separation, dialogue cleanup, and automated mixing tools are reducing production workloads by approximately 30–40% while improving editing consistency. More than 45% of professional creators now utilize at least one AI-assisted workflow component. Vendors including Avid, Steinberg, and Ableton are embedding machine-learning engines directly into production environments, transforming DAWs from recording platforms into intelligent content-production ecosystems. This shift delivers measurable operational advantages through faster project completion and reduced manual intervention.

Cloud-native production environments represent the next major technology transition. Compared with traditional local-file workflows, cloud-enabled collaboration can improve project turnaround times by nearly 25% while reducing infrastructure dependency. Adoption has surpassed 40% among distributed production teams. Real-time synchronization, browser-based editing, and shared project management are enabling geographically dispersed creators to work within unified production environments. Companies with strong cloud integration capabilities are gaining competitive advantages through workflow scalability and customer retention.

Looking toward 2026–2028, immersive audio production, generative audio creation, and AI-driven content orchestration will become key differentiators. Spatial audio deployment has already increased by more than 30% among premium media producers. Organizations investing now in AI-assisted workflows, cloud infrastructure, and immersive production capabilities will achieve stronger operational efficiency, faster content delivery, and superior competitive positioning as digital media production volumes continue expanding.

November 2024 – Steinberg launched Cubase 14, introducing new Modulators, enhanced score-editing technology, and expanded workflow automation capabilities. The release focused on accelerating creative production and improving editing efficiency across professional music workflows. Business impact: strengthened premium DAW competitiveness through deeper workflow integration. Source: www.steinberg.net

April 2025 – Avid showcased integrated cloud-enabled production workflows at NAB Show 2025, combining AI-powered tools, intelligent automation, and AWS-driven collaboration infrastructure. The initiative targeted faster content creation and improved remote production efficiency. Business impact: expanded enterprise adoption of scalable cloud-based production environments.

June 2025 – Avid released Pro Tools 2025.6 with AI-powered Speech-to-Text, advanced MIDI enhancements, and direct Splice integration. The update streamlined music and post-production workflows while accelerating editing operations. Business impact: improved creator productivity and reinforced ecosystem-driven customer retention strategies.

April 2026 – Avid announced a multi-year partnership with Google Cloud to integrate generative and agentic AI capabilities into creative workflows. The initiative enables automated media analysis, metadata generation, and natural-language content discovery. Business impact: accelerated enterprise adoption of AI-assisted production and intelligent content management systems.

The report provides comprehensive analysis of the Digital Audio Workstations (DAWs) Market across major deployment types, applications, end-user categories, and key geographic regions. Coverage includes software-based, cloud-based, on-premise, and hybrid platforms, alongside applications spanning music production, podcasting, broadcasting, film post-production, and gaming audio. The study evaluates adoption patterns across professional studios, independent creators, media organizations, and educational institutions while assessing competitive positioning among leading software providers and emerging technology innovators.

The analysis examines operational trends influencing more than 60% of professional production workflows, including AI-assisted editing, cloud collaboration, immersive audio production, and creator-economy platform development. Regional assessment covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with detailed country-level strategic insights. The report supports investment evaluation, market-entry planning, product development, partnership strategy, and competitive benchmarking while identifying emerging opportunities in cloud-native production environments, AI-driven content creation, and next-generation audio workflow technologies expected to shape market direction between 2026 and 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 4,394.1 Million |

| Market Revenue (2033) | USD 9,015.9 Million |

| CAGR (2026–2033) | 9.4% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Avid Technology; Steinberg Media Technologies GmbH; Ableton AG; Apple Inc.; Cockos Incorporated; Bitwig GmbH; Image-Line Software; MAGIX Software GmbH; Harrison Audio LLC; MOTU Inc.; Tracktion Corporation; Acoustica Inc.; Adobe Inc.; Soundtrap AB |

| Customization & Pricing | Available on Request (10% Customization Free) |