Reports

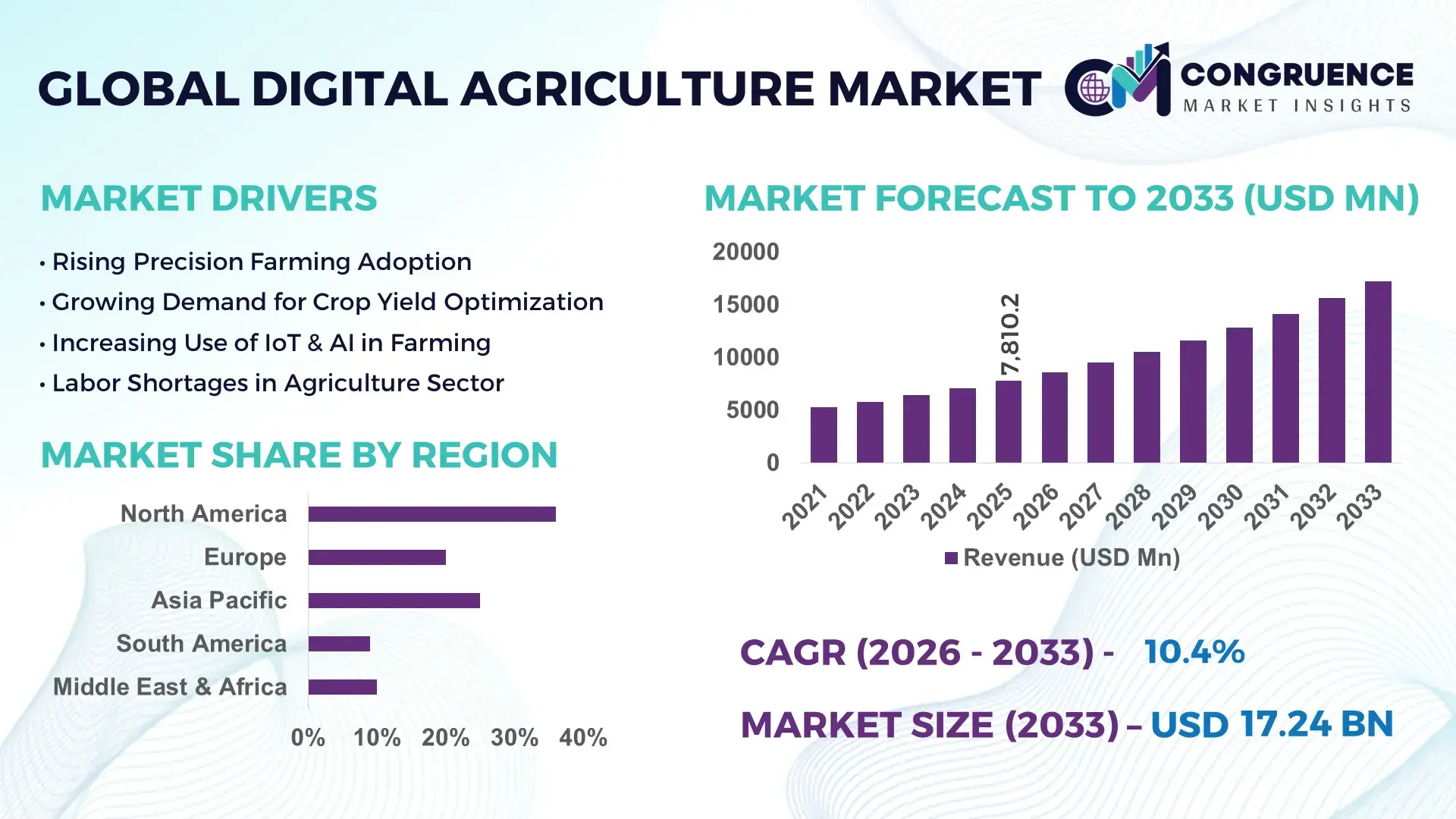

The Global Digital Agriculture Market was valued at USD 7810.17 Million in 2025 and is anticipated to reach a value of USD 17235.07 Million by 2033 expanding at a CAGR of 10.4% between 2026 and 2033. This growth is driven by expanding adoption of precision farming, Internet of Things (IoT) sensors, artificial intelligence (AI)-based crop monitoring systems, and data-driven decision support tools that optimize yields and reduce input costs.

In the United States — a leading country in digital agriculture — investment in advanced agri‑tech solutions such as AI analytics, autonomous machinery, and smart irrigation has surged, with over 58% of large-scale farms integrating satellite crop monitoring and variable rate technologies by 2024. The U.S. deployment of GPS-enabled smart tractors and drone fleets supports extensive field automation, and annual venture funding for agri‑tech startups exceeded hundreds of millions USD in recent years, bolstering scalable precision farming applications across major crop belts such as the Midwest and California.

Market Size & Growth: Valued at ~USD 7.81B in 2025; projected ~USD 17.21B by 2033; CAGR ~10.4% driven by precision agriculture, smart irrigation, and AI tools adoption.

Top Growth Drivers: Precision farming adoption ~58%; satellite crop monitoring ~41%; AI‑integrated crop management ~36%.

Short‑Term Forecast: By 2028, digital adoption is expected to improve yield forecasting accuracy by 30% and reduce input costs by ~20%.

Emerging Technologies: AI/ML analytics platforms, autonomous machinery, IoT sensor networks.

Regional Leaders: North America ~USD 5.3B (by 2033) with advanced automation uptake; Europe ~USD 4.5B with precision greenhouse systems; Asia‑Pacific ~USD 3.8B driven by mobile farm management tools.

Consumer/End‑User Trends: Large commercial farms increasingly deploy cloud‑based decision support systems and mobile agri apps; smallholder adoption is rising via affordable IoT solutions.

Pilot or Case Example: 2024 U.S. pilot of autonomous planters with real‑time analytics reported an 18% yield increase on corn operations.

Competitive Landscape: Market leader enabling ~30–35% share includes John Deere, followed by Bayer CropScience, Trimble Inc., BASF SE, and Topcon.

Regulatory & ESG Impact: Government incentives for sustainable farming tech and carbon‑neutral agriculture regulations enhance digital solution uptake.

Investment & Funding Patterns: Recent global investments in digital agriculture technologies exceed USD 500M annually, with growing venture funding and ag‑tech startup activity.

Innovation & Future Outlook: Integration of real‑time IoT analytics, AI predictive models, and autonomous robotics create robust forecasting and resource optimization platforms shaping future market landscapes.

The Digital Agriculture market encompasses precision farming, farm management software, drone‑based monitoring, and IoT‑enabled irrigation systems that increasingly influence decision‑making and operational efficiency in agriculture. Segments such as precision farming account for a significant portion of technological deployments due to their ability to reduce input costs and enhance yields, while mobile‑based farm management tools are gaining traction in emerging economies. Regulatory incentives for sustainable agriculture and climate‑smart practices further stimulate adoption, and regional consumption patterns reveal strong demand in North America, Europe, and Asia‑Pacific driven by modernized infrastructure, government support, and increasing investments in agri‑tech innovation.

The Digital Agriculture Market is strategically pivotal for modernizing global food production, enhancing farm efficiency, and supporting sustainability objectives. AI-driven crop monitoring platforms deliver up to 25% improvement in yield prediction accuracy compared to traditional scouting methods. North America dominates in volume, while Europe leads in adoption with over 42% of enterprises using cloud-based farm management systems. By 2028, autonomous machinery and IoT-integrated precision irrigation are expected to reduce water and fertilizer usage by approximately 18%, enhancing resource efficiency. Firms are committing to ESG improvements such as a 20% reduction in chemical runoff and enhanced soil carbon sequestration by 2030, aligning with climate-smart agriculture initiatives.

In 2025, John Deere’s deployment of AI-assisted planters in the Midwest achieved a 17% reduction in operational downtime through real-time data optimization. The integration of predictive analytics, satellite imagery, and robotics enables decision-makers to reduce input costs, optimize labor, and respond swiftly to environmental stressors. Forward-looking strategies in the Digital Agriculture Market emphasize interoperability of digital platforms, investment in AI/ML-based decision support systems, and expansion of connected farm infrastructure. Collectively, these pathways position the Digital Agriculture Market as a pillar of resilience, regulatory compliance, and sustainable growth, capable of transforming agricultural operations globally while addressing ecological and resource-efficiency challenges.

Precision farming adoption is a critical driver for the Digital Agriculture Market, enabling farms to apply water, fertilizers, and pesticides more efficiently. Modern IoT-enabled sensors and AI algorithms allow real-time monitoring of soil health, crop conditions, and weather patterns. Drone-assisted aerial monitoring reduces crop scouting time by up to 35%, while satellite-based variable rate technologies optimize fertilizer application, cutting input usage by 20%. These improvements reduce operational costs and increase crop productivity, making precision agriculture a strategic tool for scaling sustainable farming practices. Increasing awareness and regulatory support for environmental compliance further reinforce the adoption of these technologies across commercial and mid-sized farms globally.

High capital expenditures for advanced digital agriculture solutions present a barrier, particularly for smallholder and mid-sized farms. Equipment such as autonomous tractors, AI-based monitoring systems, and drones can cost tens of thousands of dollars per unit. Integrating multiple digital platforms requires skilled personnel, which is scarce in emerging markets. Complexity in data analytics and software management can also impede adoption, with over 28% of farms reporting difficulties in system interoperability. Inconsistent internet connectivity in rural regions limits real-time data collection and decision-making, slowing broader implementation despite the potential for long-term efficiency gains and productivity improvements.

The integration of AI and IoT technologies presents substantial opportunities for optimizing farm operations and improving sustainability metrics. Smart irrigation systems leveraging predictive analytics can reduce water consumption by up to 18%, while crop health monitoring via drones allows early detection of disease outbreaks, potentially reducing yield loss by 12%. Emerging markets, particularly in Asia-Pacific and Latin America, offer untapped potential as mobile-based farm management solutions gain traction among smallholder farms. Blockchain-enabled supply chain tracking is creating transparency in produce quality and provenance, opening avenues for premium market pricing and regulatory compliance. Affordable sensors, cloud analytics, and autonomous machinery are creating scalable solutions that strengthen efficiency, profitability, and environmental sustainability.

Operational costs, including investment in hardware, software, and skilled labor, pose significant challenges to the Digital Agriculture Market. Compliance with environmental regulations—such as restrictions on chemical usage and water management—adds complexity and increases upfront costs for technology deployment. Fragmented regulatory frameworks across regions make cross-border adoption and scaling difficult. Data privacy and cybersecurity concerns challenge digital system deployment, as farms increasingly rely on cloud-based solutions for sensitive operational data. These factors, combined with fluctuating energy prices and maintenance expenses for IoT and autonomous equipment, require farms to carefully evaluate return on investment, limiting rapid adoption despite clear efficiency benefits.

• Expansion of AI-Driven Crop Monitoring: AI-based monitoring platforms are increasingly deployed across farms, with over 48% of large-scale farms using machine learning algorithms to predict crop health and nutrient deficiencies. These systems reduce scouting time by 30% and increase yield accuracy by 22%, enabling data-driven interventions that minimize resource wastage and enhance operational efficiency.

• Proliferation of IoT-Enabled Smart Irrigation: IoT-connected irrigation systems are gaining traction, with 41% of mid-sized farms adopting real-time soil moisture sensors. These systems optimize water usage, cutting consumption by up to 18% while maintaining crop productivity. Adoption is highest in arid regions, including parts of North America and the Middle East, where water efficiency is crucial for sustainable operations.

• Drone and Autonomous Machinery Integration: Drone fleets and autonomous tractors are being increasingly deployed, reducing labor dependency by 25% and improving operational uptime by 20%. In 2025, more than 35% of precision farms in Europe reported measurable gains in planting accuracy and pest management efficiency due to automated aerial surveillance and robotic operations.

• Adoption of Digital Supply Chain Tracking: Blockchain and cloud-based traceability solutions are being integrated into farm-to-market supply chains, with 38% of enterprises using these systems to track produce quality and logistics. This has led to a 15% reduction in product loss during transportation and enhanced transparency, supporting regulatory compliance and premium pricing opportunities.

The Digital Agriculture Market is segmented to address diverse technological, operational, and end-user requirements, providing decision-makers with actionable insights for strategic planning. By type, solutions range from precision farming platforms and AI-driven monitoring tools to drone-based surveying and IoT-enabled irrigation systems, each addressing specific operational needs. Applications focus on crop management, livestock monitoring, supply chain optimization, and resource efficiency, allowing measurable improvements in yield, water conservation, and traceability. End-user insights indicate significant adoption by large commercial farms, agricultural cooperatives, and smallholder enterprises, with varying adoption rates based on regional infrastructure, technology accessibility, and farm scale. Understanding these segmentation dynamics helps industry players identify strategic entry points, prioritize investments, and optimize deployment of technology solutions tailored to operational and regional requirements.

Precision farming platforms currently account for 42% of adoption, providing comprehensive data analytics for soil health, crop monitoring, and resource management. Drone-based monitoring holds 25% of the market share, primarily due to its ability to provide aerial imaging and early pest detection. However, adoption of IoT-enabled smart irrigation systems is rising fastest, expected to surpass 30% of installations by 2033, driven by increasing water scarcity and sustainability regulations. Other types, including autonomous machinery and AI-driven predictive platforms, contribute a combined 33% of the market, serving niche or specialized farm operations with automated planting, harvesting, and yield forecasting capabilities.

Crop management solutions currently dominate the Digital Agriculture Market with 45% adoption, offering real-time insights into soil, weather, and pest conditions, enabling optimized input allocation. Supply chain optimization applications account for 28%, while livestock monitoring contributes 20%. Smart irrigation adoption is rising fastest, expected to exceed 30% of applications by 2033, driven by increasing demand for water efficiency and precision input management. Other applications, including predictive analytics for disease management and post-harvest storage optimization, make up a combined 15% of usage.

Large commercial farms lead adoption with 50% market share, benefiting from economies of scale and investment capacity in advanced digital platforms. Agricultural cooperatives represent 28%, leveraging shared resources to implement IoT-enabled monitoring and precision tools. Smallholder farms are the fastest-growing end-user segment, expected to surpass 30% adoption by 2033, driven by mobile-based platforms and affordable sensor technologies. Other end-users, including research institutions and government demonstration farms, account for a combined 22%, primarily focused on pilot projects and innovation testing.

North America accounted for the largest market share at 36% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11.2% between 2026 and 2033.

In 2025, North America deployed over 58% of commercial farms with AI-based crop monitoring systems, while Europe adopted cloud-based farm management platforms across 42% of large agricultural enterprises. Asia-Pacific accounted for 28% of total farm IoT installations, with China alone integrating over 1.2 million smart irrigation sensors. South America held 12% of the market volume, with Brazil leading in precision agriculture adoption covering 620,000 hectares. Middle East & Africa represented 6% of the global deployment, focusing on water-efficient digital irrigation technologies. Across these regions, technological adoption varies significantly, reflecting regulatory frameworks, infrastructure readiness, and end-user investment capacity, highlighting both opportunities and operational focus areas for digital agriculture stakeholders.

How is farm digitization transforming large-scale operations?

North America accounts for 36% of the global digital agriculture market, with strong adoption in large-scale commercial farms and agribusinesses. Key industries driving demand include corn, soybean, and wheat production, supported by government incentives for precision farming and sustainability initiatives. Regulatory updates promoting carbon reduction and efficient water usage have accelerated adoption of smart irrigation and AI-driven crop monitoring. Technological advancements include autonomous tractors, drone surveillance, and predictive analytics platforms. Local players like John Deere have implemented AI-integrated machinery that reduces field downtime by 17% and improves planting accuracy. Regional consumer behavior shows higher enterprise adoption in precision agriculture, cloud-based analytics, and data-driven crop management, emphasizing efficiency, compliance, and cost reduction.

What factors are driving digital farming adoption across key European nations?

Europe holds 29% of the digital agriculture market, with Germany, France, and the UK being major contributors. Regulatory frameworks emphasizing sustainable agriculture and carbon-neutral farming have fueled technology adoption, while EU incentives promote precision farming and digital traceability. Emerging technologies such as drone surveillance, AI-driven crop analytics, and smart irrigation platforms are being integrated into commercial and cooperative farming operations. Local players like BASF SE are deploying digital crop protection systems that reduce chemical use by 15%. Regional consumer behavior is shaped by regulatory compliance and sustainability demands, leading to widespread adoption of explainable and accountable digital agriculture solutions.

How is mobile and AI technology reshaping farming in emerging economies?

Asia-Pacific represents 28% of the market by volume, with China, India, and Japan as top consuming countries. Infrastructure developments such as improved rural connectivity and modern irrigation systems support digital agriculture adoption. Mobile-based AI apps, cloud platforms, and IoT-enabled sensors are transforming smallholder and commercial farm operations. Companies like DJI in China are supplying drone solutions for crop monitoring and spraying, impacting over 500,000 hectares of farmland. Regional consumer behavior is characterized by strong reliance on mobile technology, affordability-driven adoption, and government-backed digitization programs, contributing to rapid expansion and innovation.

What are the key drivers of digital agriculture growth in South American farms?

South America holds 12% of the global market, with Brazil and Argentina as leading contributors. Large-scale commercial farming operations and expanding agribusiness infrastructure drive demand. Government incentives and trade policies encourage adoption of precision irrigation and AI-assisted crop management. Local players, such as AgroTools in Brazil, are implementing satellite-based monitoring solutions covering thousands of hectares. Regional consumer behavior reflects interest in technology-enabled efficiency and sustainability, with increasing adoption among medium and large-scale farm operators seeking measurable yield improvements.

How are digital solutions addressing resource challenges in arid regions?

Middle East & Africa account for 6% of the market, with major growth in UAE, Saudi Arabia, and South Africa. Demand is driven by agriculture modernization initiatives in water-scarce regions, supported by advanced irrigation technologies and AI-based crop analytics. Technological modernization includes IoT sensor deployment, drone-assisted monitoring, and precision farming machinery. Local players are piloting autonomous irrigation projects that reduce water usage by 20%. Regional consumer behavior reflects focus on sustainability, efficiency, and compliance with water conservation regulations, with higher adoption in commercial and government-backed agricultural projects.

United States – 36% market share; high production capacity, strong enterprise adoption, and advanced AI/IoT integration.

Germany – 15% market share; strong regulatory support for sustainable agriculture, high technology adoption, and precision farming infrastructure.

The Digital Agriculture market exhibits a moderately consolidated competitive environment, with approximately 120 active competitors globally, ranging from multinational agritech corporations to specialized AI and IoT solution providers. The top five companies—including John Deere, Trimble Inc., Bayer CropScience, BASF SE, and AG Leader—together account for around 52% of total market adoption, reflecting significant influence in precision farming, drone deployment, and smart irrigation technologies. Strategic initiatives such as partnerships with AI analytics firms, launch of autonomous machinery, and acquisition of agri-tech startups are shaping the competitive landscape. For example, 2025 saw John Deere expand its AI-integrated planting solutions to cover over 2.5 million hectares across North America. Trimble introduced cloud-based farm management systems to over 400,000 farms in Europe, while Bayer CropScience deployed satellite-guided crop protection tools in Latin America. Innovation trends such as IoT sensor proliferation, machine learning for yield prediction, and blockchain-enabled supply chain tracking are intensifying competition, with mid-tier players capturing niche segments in emerging economies. Market fragmentation in Asia-Pacific and South America allows new entrants to leverage affordable mobile and IoT-based solutions, increasing competitive pressure across regions.

BASF SE

AG Leader

DJI Innovations

Topcon Corporation

AGCO Corporation

Raven Industries

Syngenta

The Digital Agriculture Market is being profoundly shaped by the integration of advanced technologies that enhance farm efficiency, resource management, and crop yield accuracy. AI-driven analytics platforms are deployed on over 45% of large-scale farms, enabling predictive modeling for soil health, pest detection, and irrigation scheduling. Machine learning algorithms provide real-time recommendations, reducing fertilizer and pesticide use by up to 18%, while improving overall crop productivity by 22%.

IoT-enabled sensors and smart irrigation systems are transforming water management practices, with more than 1.5 million hectares globally monitored through soil moisture and climate-adaptive sensors. These technologies allow precise allocation of water and nutrients, optimizing input usage and minimizing environmental impact. Drones and UAVs are increasingly used for aerial crop surveillance, covering over 2 million hectares worldwide, reducing labor requirements by 25% and enabling early detection of disease outbreaks or nutrient deficiencies.

Autonomous machinery, including self-driving tractors and robotic planters, now operate on 38% of precision farms in North America and Europe, offering measurable reductions in downtime and manual labor costs. Blockchain and cloud-based platforms are being integrated into supply chain management, ensuring traceability for over 500,000 tons of produce annually and reducing post-harvest losses by 15%.

Emerging technologies, such as satellite imaging with AI-powered interpretation and augmented reality (AR) farm planning tools, are gaining traction. These innovations allow farms to simulate crop growth scenarios, optimize land use, and improve operational efficiency, reinforcing digital agriculture as a data-driven, sustainable, and highly precise industry for the future.

• In January 2025, John Deere unveiled its second‑generation autonomous agriculture machines at CES 2025, equipped with advanced computer vision, AI, and 360‑degree camera systems. These autonomous tractors and equipment are designed to reduce labor dependency and improve field operational efficiency in large‑scale agriculture. (John Deere)

• In December 2024, Bayer launched its digital agriculture platform FieldView in Mexico, extending data‑driven crop management tools to more than 27 countries and enabling farmers to collect and analyse real‑time field data for improved resource optimisation and decision‑making. (Mexico Business News)

• In April 2025, PTx Trimble introduced the NAV‑960 guidance controller, offering up to 50% improved positioning accuracy and uptime over its predecessor, enhancing precision autoguidance for complex field operations and increasing overall productivity on precision farms. (AGCO Newsroom)

• In Q1 2025, AgroScout, an AI‑powered crop monitoring firm, closed a $25 million Series C funding round to expand its digital agriculture offerings into Asian markets, accelerating the deployment of AI‑based crop health analytics and monitoring tools across diverse agricultural landscapes.

The scope of the Digital Agriculture Market report encompasses an extensive examination of technological, geographic, and application‑based segments shaping modern agricultural practices. The report covers key product types including precision farming platforms, IoT sensor networks, autonomous machinery, drone‑based monitoring, and cloud‑based analytics systems, highlighting their impacts on farm operations, input optimisation, and sustainability. Geographic analysis spans major regions—North America, Europe, Asia‑Pacific, South America, and Middle East & Africa—evaluating deployment trends, infrastructure readiness, regulatory influences, and consumer behaviours that drive regional adoption and investment patterns.

Within application segments, the report delves into crop management, yield monitoring, soil health analytics, livestock monitoring, smart irrigation, and supply chain optimisation, detailing how each supports operational efficiency, traceability, and resource management. Technology focus areas include AI and machine learning for predictive insights, IoT and sensor integration for real‑time field data, autonomous navigation systems for labour‑saving tasks, and blockchain‑enabled traceability for enhanced transparency. Industry focus areas further cover adoption across large commercial farms, mid‑sized cooperatives, and smallholder farms, highlighting variations in technology uptake and digital literacy.

Emerging and niche segments such as mobile‑first farm management tools, AR/VR decision support interfaces, and integrated climatic advisory systems are also examined, offering insights into future pathways for innovation. The report provides decision‑makers with comprehensive insights into competitive strategies, user adoption patterns, and regional technology ecosystems to inform strategic planning, investment decisions, and product development priorities.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

10.4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

John Deere, Trimble Inc., Bayer CropScience, BASF SE, AG Leader, DJI Innovations, Topcon Corporation, AGCO Corporation, Raven Industries, Syngenta |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |