Reports

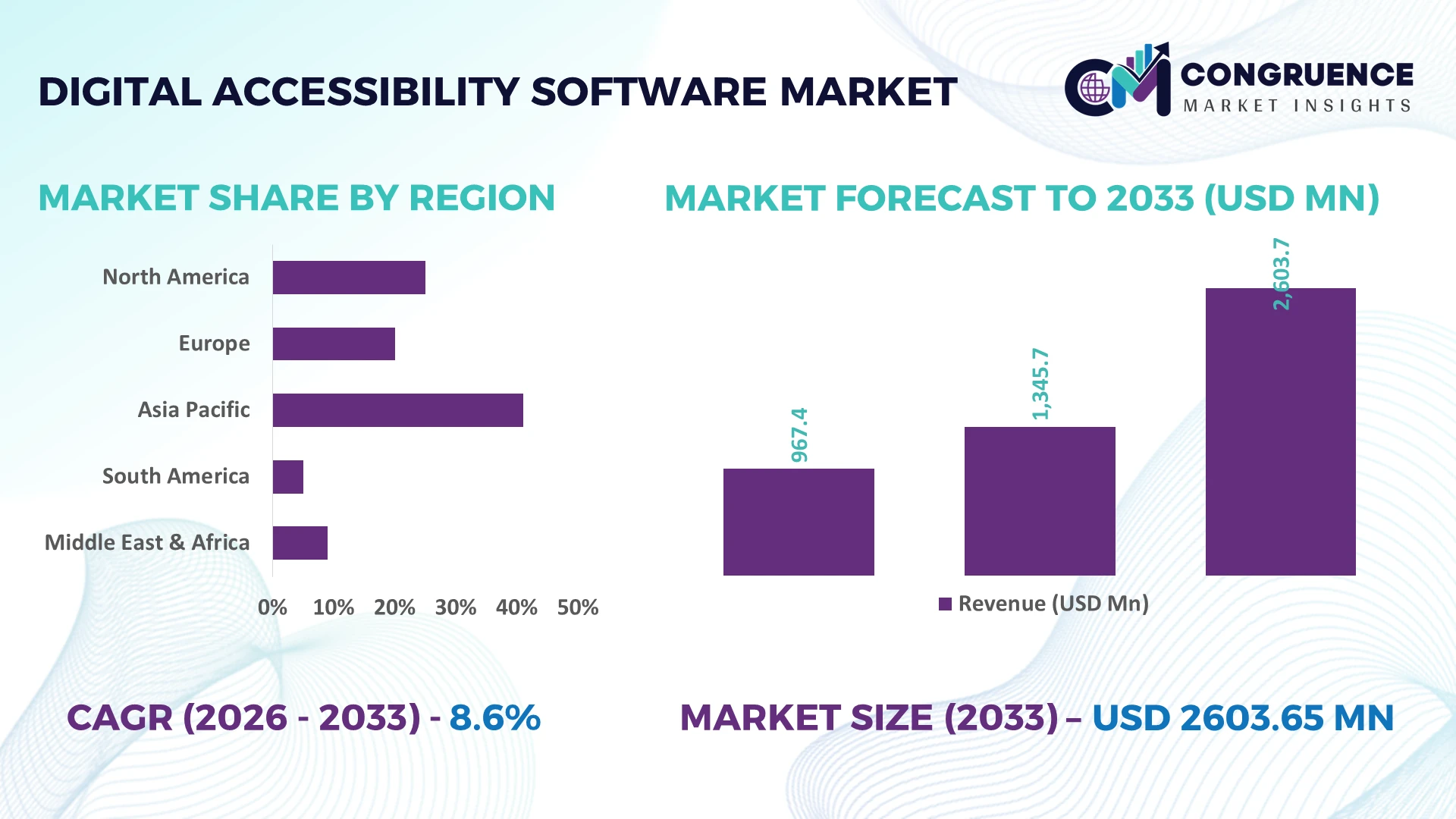

The Global Digital Accessibility Software Market was valued at USD 1345.69 Million in 2025 and is anticipated to reach a value of USD 2603.65 Million by 2033 expanding at a CAGR of 8.6% between 2026 and 2033. Growth is driven by stricter digital accessibility regulations, enterprise-wide AI-powered accessibility testing, expanding inclusive digital transformation programs, and continuous integration of accessibility compliance into software development workflows.

The United States leads the global digital accessibility software market with approximately 39% market share, supported by extensive enterprise digitalization, federal accessibility mandates, and strong adoption across healthcare, banking, education, and public services. More than 72% of large enterprises have integrated automated accessibility testing into DevSecOps pipelines by 2026, compared with around 45% in Germany, while continued enforcement of accessibility legislation strengthens implementation across North America despite evolving global regulatory frameworks.

Organizations prioritizing scalable, AI-enabled accessibility platforms with continuous compliance capabilities are positioned to strengthen regulatory readiness, digital inclusion, and long-term enterprise competitiveness.

Market Size & Growth: USD 1345.69 Million (2025) to USD 2603.65 Million (2033) at 8.6% CAGR, driven by AI-powered compliance automation and enterprise digital transformation.

Top Growth Drivers: AI accessibility tools (+34%), regulatory compliance adoption (+28%), cloud deployment (+31%) accelerate global market expansion.

Short-Term Forecast: By 2028, automated accessibility audits reduce manual testing time by 45% while improving remediation efficiency by 38%.

Emerging Technologies: Generative AI, machine learning, automated WCAG testing, and real-time accessibility monitoring redefine advanced compliance workflows.

Regional Leaders: North America exceeds USD 980 Million, Europe surpasses USD 720 Million, Asia-Pacific approaches USD 540 Million with rapid enterprise cloud adoption.

Consumer/End-User Trends: More than 68% of large enterprises embed accessibility validation into software development and digital customer experience strategies.

Pilot/Case Example: In 2026, enterprise AI accessibility deployment improved issue detection accuracy by 41% and reduced remediation cycles by 36%.

Competitive Landscape: Leading vendors hold nearly 44% combined share, supported by Level Access, AudioEye, Siteimprove, Deque Systems, and Crownpeak.

Regulatory & ESG Impact: Accessibility compliance programs improve digital inclusion by over 30% while strengthening governance across multinational organizations.

Investment & Funding: More than USD 1.4 Billion supports acquisitions, AI platform expansion, and regional accessibility solution development amid global digital infrastructure growth.

Innovation & Future Outlook: AI copilots, predictive accessibility analytics, and continuous compliance orchestration accelerate next-generation enterprise accessibility platforms.

Growing demand across government, financial services, healthcare, education, and retail continues to reshape the Digital Accessibility Software Market as organizations integrate AI-driven accessibility testing, real-time monitoring, and developer-focused remediation tools into software lifecycles. More than 60% of enterprise accessibility initiatives now prioritize continuous compliance, supported by expanding digital regulations and standardized procurement requirements, creating a strong foundation for the strategic market discussion.

Digital accessibility software has become a strategic enterprise priority as organizations integrate compliance, customer experience, and digital transformation into a single operational framework. The enforcement of stricter accessibility legislation, expansion of cloud-native applications, and modernization of public digital infrastructure are reshaping procurement priorities. Enterprises increasingly evaluate accessibility capabilities alongside cybersecurity and privacy requirements, making accessibility platforms a competitive differentiator rather than a standalone compliance tool.

AI-powered accessibility platforms now identify and prioritize compliance issues approximately 55% faster than traditional manual audits while reducing repetitive testing workloads by nearly 40%. The United States leads large-scale enterprise deployment through mature regulatory enforcement and software ecosystem investment, whereas Japan is accelerating adoption through smart public services and enterprise digital modernization. Over the next two to three years, automated accessibility validation is expected to exceed 70% adoption among large organizations integrating continuous software delivery practices.

Financial institutions increasingly deploy accessibility monitoring across customer portals and mobile banking applications to maintain uninterrupted regulatory compliance and improve digital engagement. Software vendors are expanding AI capabilities, forming cloud partnerships, and investing in developer-centric automation to strengthen implementation efficiency. Organizations that embed accessibility into software engineering, procurement, and governance frameworks will achieve stronger operational resilience, higher customer retention, and sustained competitive positioning.

Enterprise adoption is increasingly driven by AI-enabled accessibility testing integrated directly into software development pipelines. More than 72% of large organizations now include accessibility verification within DevSecOps workflows, while automated testing reduces issue identification time by nearly 50% and lowers remediation effort by approximately 35%. The implementation of stronger digital accessibility regulations in the United States and Europe has shifted accessibility from post-release correction to continuous development practice. Software providers are expanding AI capabilities, acquiring specialist accessibility firms, and strengthening cloud partnerships to deliver scalable compliance platforms. A significant strategic advantage emerges from combining accessibility analytics with software quality assurance, enabling organizations to improve customer experience while reducing long-term compliance costs.

Legacy enterprise infrastructure remains a significant barrier to large-scale accessibility implementation. Nearly 48% of enterprise web applications still operate on architectures requiring extensive customization before automated accessibility tools can be fully integrated, while remediation costs for older platforms are typically 30% higher than cloud-native environments. Large organizations in Germany and Japan continue facing interoperability challenges across multiple software vendors and outdated content management systems. To reduce operational disruption, companies are adopting phased modernization strategies, negotiating long-term technology contracts, and localizing implementation services. Businesses that successfully standardize accessibility across legacy and modern environments gain stronger governance while avoiding fragmented compliance management.

The convergence of generative AI, predictive analytics, and real-time accessibility monitoring is creating substantial opportunities beyond regulatory compliance. AI-assisted remediation can reduce manual coding effort by nearly 45%, while intelligent content analysis improves accessibility validation accuracy by over 35%. Australia and Singapore are expanding digital government initiatives that require accessibility-by-design across public digital services, encouraging broader enterprise adoption. Software vendors are investing in API-driven ecosystems, developer toolkits, and strategic cloud collaborations to simplify deployment across multi-platform environments. An emerging opportunity lies in integrating accessibility intelligence with customer experience analytics, enabling organizations to improve digital engagement while optimizing operational efficiency across diverse user populations.

Maintaining consistent accessibility across rapidly expanding digital ecosystems presents a long-term execution challenge. Large enterprises typically manage more than 200 interconnected digital assets, while over 60% of accessibility issues originate from continuous application updates and third-party software integrations. Organizations in the United States increasingly face pressure to maintain accessibility across AI-generated content, mobile applications, and cloud services without disrupting release cycles. Companies are responding through investment in centralized governance platforms, developer training, automated quality controls, and specialized implementation partnerships. Long-term competitiveness will depend on embedding accessibility into enterprise architecture and software engineering processes rather than relying on isolated compliance assessments.

AI-Powered Compliance Workflows: Enterprises are embedding AI-driven accessibility validation directly into development pipelines, reducing manual testing effort by nearly 45% and accelerating issue detection by over 50%. Following stricter digital accessibility regulations in the United States and Europe, more than 70% of large software teams now automate recurring compliance checks. Vendors are expanding cloud-native platforms, integrating developer tools, and forming technology partnerships to deliver continuous accessibility management with shorter software release cycles.

Accessibility Integrated Into DevSecOps: Accessibility testing is becoming a standard quality assurance requirement rather than a final compliance review. Around 68% of enterprise software releases now include automated accessibility scans before deployment, lowering remediation costs by approximately 30%. Large organizations in Germany and Canada are restructuring software engineering workflows by integrating accessibility with cybersecurity and performance testing, enabling faster product launches while maintaining regulatory consistency across digital platforms.

Expansion Of Real-Time Monitoring: Continuous monitoring platforms are replacing periodic accessibility audits as enterprises manage expanding digital ecosystems. Organizations deploying real-time monitoring report nearly 35% fewer recurring compliance issues and approximately 28% faster remediation cycles. Financial institutions and public agencies are scaling centralized accessibility dashboards across websites, mobile applications, and digital documents, while software providers enhance analytics capabilities through automation and predictive issue prioritization instead of reactive correction models.

Enterprise Accessibility Platform Consolidation: Organizations are reducing fragmented accessibility tools by adopting unified enterprise platforms that combine testing, reporting, remediation guidance, and governance. More than 40% of multinational enterprises have consolidated accessibility software portfolios since 2025, improving operational visibility and reducing duplicate licensing costs by roughly 22%. Growing demand for standardized digital governance is encouraging vendors to expand API ecosystems, strengthen cloud interoperability, and deliver integrated compliance management across distributed global operations.

Accessibility Testing represents the leading segment because it delivers scalable compliance automation, seamless DevSecOps integration, and lower enterprise remediation costs. Nearly 48% of accessibility software deployments now prioritize automated testing platforms as organizations shift toward continuous compliance instead of periodic audits. Screen Readers remain essential for end-user accessibility, particularly across government and education environments, while Accessibility Widgets support rapid website enhancements without extensive redevelopment. Companies continue strengthening testing platforms through AI-assisted code analysis, cloud deployment, and developer workflow integration to improve operational efficiency across large digital portfolios.

Voice Recognition is the fastest-growing segment as conversational interfaces, AI assistants, and hands-free digital experiences become standard across enterprise applications. Adoption has increased by approximately 33% since 2025, while Captioning Software gains momentum through expanding video communication and digital learning environments. Vendors are investing in multilingual speech recognition, automated caption generation, and integrated accessibility ecosystems, shifting investment priorities toward intelligent, real-time accessibility capabilities that extend beyond traditional compliance requirements.

Website Accessibility remains the dominant application because corporate websites, government portals, and customer service platforms represent the highest compliance priority. More than 62% of enterprise accessibility investments focus on web environments, supported by stricter procurement requirements and continuous digital service modernization. Document Accessibility continues expanding across regulated industries managing contracts, reports, and public records, while Digital Content solutions improve accessibility for multimedia assets and enterprise communications. Companies are integrating automated scanning, remediation workflows, and cloud-based governance to maintain consistent compliance across high-volume digital assets.

Mobile Applications are the fastest-growing application segment as financial services, retail, and healthcare organizations prioritize accessible mobile customer experiences. Mobile accessibility deployments have increased by nearly 36% since 2025, driven by AI-powered testing and responsive interface optimization. E-Learning platforms continue strengthening accessibility through automated captioning and adaptive learning technologies, while vendors expand unified accessibility management across web and mobile ecosystems to improve operational consistency and customer engagement.

Government represents the leading end-user because public digital services require comprehensive accessibility compliance across websites, citizen portals, and digital documentation. Approximately 34% of enterprise-scale accessibility deployments support government modernization initiatives, where procurement standards increasingly mandate continuous accessibility validation. Healthcare follows with growing implementation across patient portals and telehealth platforms, while Education maintains stable demand through accessible digital learning environments. Software vendors are developing sector-specific compliance modules, expanding implementation partnerships, and strengthening cloud deployment strategies to meet institutional requirements.

Banking is the fastest-growing end-user segment as digital financial services increasingly prioritize inclusive customer experiences and regulatory readiness. Accessibility investment across banking platforms has expanded by roughly 31% since 2025, supported by AI-driven monitoring and secure mobile application development. Retail organizations continue adopting accessibility platforms to improve digital commerce experiences and reduce transaction barriers. Companies are differentiating through customized compliance services, subscription-based deployment models, and ecosystem partnerships that simplify implementation across highly regulated enterprise environments.

North America accounted for the largest market share at 39.0% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a 10.4% between 2026 and 2033.

Enterprise Compliance Automation Drives Market Leadership

North America maintains the highest deployment concentration through mature enterprise software ecosystems, advanced cloud infrastructure, and stringent accessibility regulations. Nearly 39% of global implementations are concentrated across the region, with financial services, healthcare, education, and public administration accounting for most enterprise contracts. More than 72% of large organizations have embedded automated accessibility testing into software development pipelines, improving release consistency and reducing remediation cycles. Technology vendors continue expanding AI-enabled accessibility platforms through strategic acquisitions, cloud integrations, and developer-focused automation, positioning accessibility as a core component of enterprise governance rather than a standalone compliance requirement.

United States Market Outlook: The United States remains the region's operational center due to strong enterprise software adoption, federal accessibility standards, and continuous digital modernization across public and private sectors. More than 75% of Fortune 500 organizations maintain formal digital accessibility programs integrated with cybersecurity and DevSecOps initiatives. Enterprise investment increasingly targets AI-assisted compliance automation, real-time monitoring, and unified governance platforms, enabling organizations to improve operational efficiency while strengthening digital inclusion across customer-facing applications.

Regulatory Harmonization Strengthens Enterprise Adoption

Europe continues expanding accessibility software deployment through harmonized digital accessibility legislation and enterprise digital transformation initiatives. Approximately 29% of global adoption originates from the region, supported by extensive modernization across government services, banking, transportation, and education. Organizations increasingly integrate accessibility validation into procurement and software quality assurance processes, while automated compliance platforms reduce manual audit effort by nearly 35%. Vendors are strengthening regional delivery capabilities through localized cloud services, multilingual accessibility solutions, and partnerships addressing evolving regulatory requirements.

Germany Market Outlook: Germany leads regional enterprise implementation through its advanced manufacturing economy, strong enterprise software ecosystem, and emphasis on digital compliance. More than 60% of large enterprises now incorporate automated accessibility assessment within software lifecycle management. Companies continue investing in AI-enabled testing platforms and integrated governance solutions to improve operational consistency while supporting large-scale digital transformation across industrial and public-sector organizations.

Digital Infrastructure Expansion Accelerates Deployment

Asia-Pacific is rapidly strengthening its market position through large-scale digital infrastructure investment, cloud adoption, and expanding enterprise software ecosystems. Around 23% of global deployments are now concentrated across the region, with banking, e-commerce, education, and public digital services driving implementation. Enterprise adoption of automated accessibility platforms has increased by nearly 38% since 2025 as organizations modernize customer-facing digital channels. Technology providers continue expanding regional cloud infrastructure, developer ecosystems, and AI-enabled accessibility capabilities to support growing digital economies.

Japan Market Outlook: Japan remains the region's most strategically significant market through advanced enterprise digitization, smart government initiatives, and high software quality standards. More than 65% of major enterprises integrate accessibility validation into digital product development and customer service platforms. Organizations continue investing in AI-assisted testing, multilingual accessibility technologies, and cloud-native compliance management to strengthen operational excellence while supporting an aging population and highly digital consumer environment.

Public Digital Services Stimulate Adoption

South America is experiencing steady expansion as governments and enterprises modernize digital services while improving accessibility compliance. Regional adoption represents approximately 5% of global deployments, led by banking, education, and public administration. Cloud-based accessibility platforms have shortened deployment timelines by nearly 30%, supporting organizations with limited internal compliance resources. Although infrastructure disparities remain across several markets, software providers are increasing local partnerships, managed services, and implementation support to improve operational scalability and reduce deployment complexity.

Brazil Market Outlook: Brazil leads regional demand through extensive digital banking, expanding public digital services, and growing enterprise cloud adoption. Approximately 58% of large organizations implementing accessibility software prioritize customer-facing digital channels and mobile applications. Vendors continue strengthening local implementation capabilities, strategic alliances, and compliance-focused service offerings, helping enterprises standardize accessibility practices while improving digital engagement across diverse user populations.

Government Digital Transformation Expands Investment

The Middle East & Africa market is advancing through national digital transformation programs, cloud infrastructure investment, and modernization of government services. Regional deployment accounts for approximately 4% of global implementation activity, with public administration, healthcare, and financial services leading adoption. Accessibility automation has reduced compliance assessment time by nearly 32% for organizations implementing centralized digital governance platforms. Software vendors continue expanding regional partnerships, cloud availability, and localized implementation expertise to support evolving enterprise and public-sector accessibility requirements.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional adoption through advanced smart government programs, high digital service penetration, and sustained technology investment. More than 60% of major government digital platforms incorporate accessibility requirements during software development and procurement. Enterprises increasingly deploy AI-enabled accessibility monitoring alongside cloud modernization initiatives, strengthening operational efficiency while supporting inclusive digital service delivery across rapidly expanding public and private digital ecosystems.

The competitive landscape is shaped by Level Access, AudioEye, Siteimprove, Deque Systems, Crownpeak, and EqualWeb, where global accessibility platform providers compete directly with regional compliance specialists and AI-focused software innovators. The top five companies collectively control approximately 44% of the market through enterprise-scale platforms, while regional vendors compete through localized compliance expertise and implementation services. Competition centers on AI automation, deployment speed, customization, and integration with enterprise development environments. Automated remediation reduces manual compliance effort by nearly 45%, while cloud-native deployment shortens implementation time by approximately 35% compared with legacy accessibility solutions. Vendors strengthen market positions through strategic acquisitions, cloud partnerships, developer tool integration, and accessibility governance platforms spanning websites, mobile applications, and digital documents. The competitive shift increasingly favors AI-enabled continuous compliance over standalone accessibility testing, accelerating market consolidation. New entrants face high barriers from enterprise trust requirements, regulatory expertise, and integration complexity. Winning requires scalable AI-driven automation, seamless DevSecOps integration, strong compliance intelligence, and long-term enterprise platform partnerships.

Level Access

AudioEye

Siteimprove

Deque Systems

Crownpeak

EqualWeb

UserWay

accessiBe

Silktide

DubBot

Monsido

TPGi

UsableNet

Artificial intelligence has become the core technology driving digital accessibility software evolution. AI-powered accessibility testing, natural language processing, computer vision, and automated code remediation now identify accessibility issues nearly 55% faster than traditional rule-based tools while reducing manual validation effort by approximately 40%. More than 70% of large enterprises have integrated accessibility validation into DevSecOps workflows, allowing continuous compliance throughout software development. Organizations adopting cloud-native accessibility platforms achieve faster release cycles and improved governance across websites, mobile applications, and enterprise digital content.

Emerging technologies include generative AI for remediation guidance, predictive accessibility analytics, real-time accessibility monitoring, and API-first compliance orchestration. Compared with legacy manual audit processes, intelligent accessibility platforms improve issue prioritization accuracy by roughly 35% while reducing repetitive testing workloads. Enterprise software providers, financial institutions, and government organizations benefit most because integrated accessibility management strengthens operational consistency, accelerates regulatory readiness, and improves digital customer experiences across multiple digital channels.

Between 2026 and 2028, accessibility platforms will increasingly integrate AI copilots, intelligent developer assistants, and unified governance dashboards with cybersecurity and software quality ecosystems. Automated compliance orchestration is expected to exceed 75% deployment among mature enterprises, enabling predictive issue prevention instead of reactive correction. Vendors investing in explainable AI, multilingual accessibility intelligence, and enterprise workflow integration will secure stronger competitive positioning as organizations prioritize scalable digital governance and continuous accessibility management.

October 2025 – Siteimprove was recognized as a Leader in a major digital accessibility platform evaluation, achieving the highest scores across multiple innovation and partner ecosystem criteria among 10 evaluated vendors. The recognition strengthened enterprise credibility and accelerated large-scale accessibility platform adoption. Source: siteimprove.com

February 2026 – AudioEye announced an independent study showing its automated accessibility technology detected 89–253% more WCAG issues than competing tools. The validation reinforced demand for AI-driven accessibility automation and strengthened the company's competitive positioning within enterprise compliance programs. Source: audioeye.com

March 2026 – AudioEye introduced its next-generation digital accessibility platform, combining AI detection, expert audits, and custom code fixes into a unified solution delivering 3–4× stronger legal protection than alternative approaches. The launch improved enterprise compliance efficiency while simplifying large-scale accessibility management. Source: nasdaq.com

May 2026 – Siteimprove announced its Global Accessibility Customer Awards, highlighting organizations achieving measurable accessibility outcomes, including one healthcare customer exceeding 90% WCAG Level AA compliance. The initiative demonstrated enterprise-scale operational success and reinforced AI-enabled accessibility as a strategic business capability. Source: siteimprove.com

This report delivers a comprehensive assessment of the Digital Accessibility Software Market across five major solution types, five core application areas, and five primary end-user industries. It evaluates market performance across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa while examining enterprise deployment trends, AI-enabled accessibility testing, cloud-based compliance platforms, real-time monitoring, developer workflow integration, and accessibility governance. More than 70% of enterprise implementations now emphasize continuous accessibility validation, making operational readiness a key evaluation criterion.

The report provides strategic analysis of technology adoption, competitive positioning, regional deployment patterns, investment priorities, and enterprise purchasing behavior between 2026 and 2033. It also assesses emerging opportunities across mobile accessibility, AI-assisted remediation, multilingual accessibility solutions, and integrated compliance ecosystems. Detailed segmentation, regional benchmarking, company analysis, and operational insights support expansion planning, product strategy, partnership evaluation, competitive differentiation, and long-term business decision-making across evolving digital accessibility environments.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 1345.69 Million |

Market Revenue in 2033 | USD 2603.65 Million |

CAGR (2026 - 2033) | 8.6% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Level Access, AudioEye, Siteimprove, Deque Systems, Crownpeak, EqualWeb, UserWay, accessiBe, Silktide, DubBot, Monsido, TPGi, UsableNet |

Customization & Pricing | Available on Request (10% Customization is Free) |