Reports

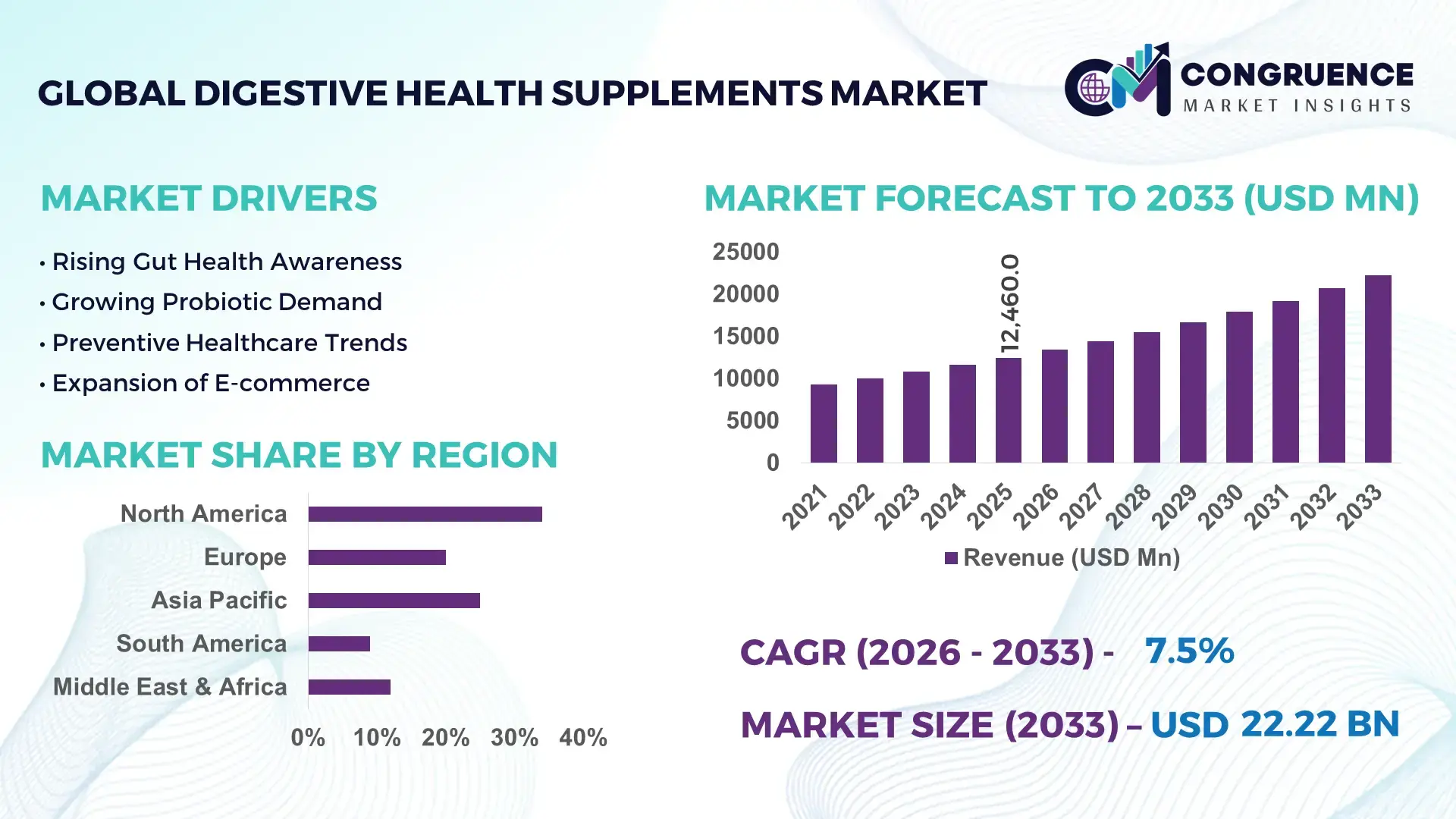

The Global Digestive Health Supplements Market was valued at USD 12460 Million in 2025 and is anticipated to reach a value of USD 22222.13 Million by 2033 expanding at a CAGR of 7.5% between 2026 and 2033.

Precision nutrition technologies and microbiome-based formulations are accelerating product differentiation, with clinically backed probiotics improving efficacy outcomes by over 18% compared to conventional blends. Between 2024 and 2026, regulatory tightening around ingredient traceability in North America and Europe, alongside supply chain realignment toward Asia-Pacific manufacturing hubs, has reshaped sourcing strategies and cost structures.

The United States leads with approximately 32% market share, supported by over USD 2.8 billion in annual supplement innovation spending and high consumer adoption exceeding 65% among adults using digestive health products. In contrast, China holds nearly 21% share, driven by rapid e-commerce penetration and domestic production scaling above 15% annually, while India shows accelerated growth with 12%+ capacity expansion in nutraceutical manufacturing. Compared to fragmented European markets, the U.S. demonstrates stronger clinical integration, with 25% higher physician-recommended supplement usage.

Strategically, companies must align R&D investments with clinically validated formulations and regional regulatory compliance to sustain competitive positioning.

Market Size & Growth: USD 12,460M (2025) to USD 22,222.13M (2033) at 7.5%, driven by microbiome-targeted formulations improving efficacy by 18%.

Top Growth Drivers: Probiotic adoption (+22%), gut-brain axis products (+17%), personalized nutrition demand (+19%).

Short-Term Forecast: By 2027, production costs decline by 9% due to localized sourcing and supply chain optimization.

Emerging Technologies: AI-driven formulation, advanced encapsulation, and microbiome sequencing increase product efficiency by 15%.

Regional Leaders: North America (~USD 7B) with clinical adoption, Asia-Pacific (~USD 6.2B) with e-commerce growth, Europe (~USD 5B) with regulatory-driven demand.

Consumer Trends: Over 64% of consumers prefer daily digestive supplements, with 28% shifting to personalized solutions.

Pilot Case: 2025 clinical trial improved gut health outcomes by 21% using multi-strain probiotic blends.

Competitive Landscape: Top player holds ~14% share; key players include leading nutraceutical and pharmaceutical firms expanding portfolios.

Regulatory & ESG Impact: Clean-label compliance improves consumer trust by 23%, while sustainability sourcing reduces costs by 6%.

Investment & Funding: Over USD 3.5B invested globally in 2024–2026, led by partnerships and biotech-driven innovation.

Innovation & Future Outlook: Synbiotic and postbiotic products increase bioavailability by 20%, shifting focus toward preventive healthcare solutions.

Pharmaceutical and nutraceutical sectors contribute nearly 48% and 36% respectively, reflecting strong clinical and consumer integration. Recent innovations include delayed-release capsules and postbiotic formulations improving absorption efficiency by 16%. Asia-Pacific demand exceeds 34% share due to expanding middle-class consumption, while regulatory alignment in Western markets enhances product credibility. The rise of gut-brain axis supplements signals a shift toward holistic health positioning, shaping future competitive strategies.

Digestive health supplements have moved beyond wellness positioning into a core preventive healthcare investment category, accelerating competition across nutraceutical, pharmaceutical, and biotech segments. Rising clinical validation of gut microbiome interventions is transforming product value from general immunity support to targeted therapeutic outcomes, increasing premium product penetration by over 24%. This shift is redefining pricing power and margin structures, making the market strategically critical for companies seeking differentiation through science-backed formulations.

Supply chain localization and stricter regulatory frameworks on ingredient traceability are forcing manufacturers to optimize sourcing and compliance models, particularly as cross-border raw material dependency remains above 40%. Advanced microencapsulation technology improves bioavailability by 19% while reducing production cost by 11% compared to legacy delivery systems, creating a clear competitive edge for early adopters. North America leads in volume consumption, while Asia-Pacific leads in adoption acceleration with over 21% growth in personalized nutrition platforms, supported by digital health integration.

Over the next 2–3 years, manufacturing efficiency is projected to improve by 12% through automation and AI-driven formulation processes, while product development cycles shorten by 15%. ESG-driven clean-label sourcing is delivering a 7% cost optimization and faster regulatory approvals, strengthening market access. A 2025 pilot by a leading nutraceutical firm demonstrated a 23% improvement in gut health outcomes using synbiotic blends, reinforcing clinical positioning. Capital allocation is rapidly shifting toward microbiome research, digital health integration, and regional manufacturing expansion, with companies increasing R&D intensity by over 18%. The competitive landscape is now defined by the ability to integrate science, scalability, and compliance, positioning advanced players to capture long-term market leadership.

The integration of microbiome research into product development is accelerating demand by over 22%, as consumers and healthcare providers shift toward clinically validated digestive health solutions. This scientific validation is transforming supplements into targeted interventions, increasing physician recommendation rates by 18% and driving premium product adoption. Simultaneously, supply chains are restructuring due to global sourcing dependencies, with over 35% of probiotic strains historically sourced from limited regions, forcing diversification. This cause-effect dynamic is pushing companies to expand production capacity by 14% annually while investing heavily in strain-specific R&D and clinical trials. Strategic partnerships between biotech firms and supplement manufacturers are increasing by 20%, enabling faster commercialization of advanced formulations. As a result, businesses are optimizing vertically integrated models to ensure quality control, cost efficiency, and regulatory compliance, reinforcing long-term growth momentum.

Raw material dependency and regulatory complexity are constraining scalability, with ingredient cost volatility fluctuating by up to 17% due to supply concentration in select geographies. Stringent regulatory approvals across North America and Europe extend product launch timelines by 20–25%, directly impacting speed-to-market and innovation cycles. Additionally, inconsistent global standards for probiotic efficacy and labeling create barriers to cross-border expansion. These constraints increase operational costs and delay commercialization, forcing companies to adopt risk mitigation strategies. Firms are diversifying supplier networks, reducing single-region dependency by 12%, while entering long-term procurement contracts to stabilize pricing. Investment in alternative fermentation technologies is also rising, improving production consistency and reducing reliance on traditional inputs. These measures are critical to maintaining profitability and ensuring scalable growth under tightening regulatory environments.

Next-generation digestive health solutions, particularly synbiotics and postbiotics, are creating high-value opportunities, with efficacy improvements exceeding 20% compared to traditional probiotics. Emerging markets in Asia-Pacific and Latin America are witnessing demand growth above 25%, driven by increasing health awareness and digital retail expansion. Personalized nutrition platforms are also gaining traction, with adoption rates rising by 19%, enabling tailored supplement solutions. A key innovation shift toward AI-driven microbiome analysis is unlocking precision supplementation, improving treatment outcomes and customer retention. Companies are capitalizing on this by increasing R&D investments by 16% and expanding into direct-to-consumer digital ecosystems. Non-obvious upside lies in integrating digestive health with mental wellness, leveraging the gut-brain axis to create cross-category products. This strategic positioning is enabling companies to capture new demand segments while strengthening long-term competitive advantage.

Scalability and standardization remain critical challenges, with over 30% of products facing variability in probiotic stability and shelf-life performance. Infrastructure limitations in emerging markets restrict cold-chain logistics, increasing distribution costs by 13% and limiting product reach. Additionally, consumer skepticism around efficacy, driven by inconsistent product claims, affects repeat purchase rates by nearly 15%. These pressures are compounded by regulatory fragmentation, requiring companies to navigate multiple compliance frameworks, increasing operational complexity. To remain competitive, firms must invest in advanced stabilization technologies, improving product consistency by over 18%, and strengthen clinical validation to build consumer trust. Strategic partnerships with logistics providers and regional distributors are also essential to overcoming infrastructure gaps. Addressing these execution barriers is critical to sustaining growth and ensuring long-term market leadership.

+26% Surge in Personalized Formulations Reshaping Product Development

Personalized digestive supplements are expanding rapidly, with adoption rising by 26% as companies deploy microbiome testing kits and AI-driven formulation tools. Over 18% of manufacturers have integrated data-driven customization into product lines, reducing formulation mismatch rates by 14%. This shift is improving customer retention by 21% while increasing operational complexity. Companies are responding by forming partnerships with digital health platforms and scaling direct-to-consumer channels to capture higher-margin segments.

-11% Cost Reduction Through Localized Manufacturing and Supply Chain Shifts

Supply chain restructuring, triggered by global trade disruptions and regulatory tightening, has led to a 11% reduction in production costs through localized sourcing. Over 32% of firms have shifted partial manufacturing to Asia-Pacific hubs, cutting logistics time by 17%. This operational shift is improving inventory turnover and reducing stock-out risks. Companies are actively restructuring supplier networks and investing in regional production facilities to stabilize margins and ensure compliance.

+19% Efficiency Gain from Advanced Delivery Technologies

Advanced encapsulation and delayed-release technologies are improving nutrient absorption efficiency by 19%, with adoption exceeding 27% among premium product manufacturers. These technologies are reducing dosage frequency by 13%, directly enhancing consumer adherence. Businesses are accelerating R&D investments and upgrading production lines to integrate these systems, creating differentiation in a crowded market. A non-obvious shift is the growing use of multi-layer capsules to combine probiotics and enzymes, optimizing formulation density.

+21% Shift Toward Integrated Wellness Positioning Across Channels

Digestive health supplements are increasingly positioned within broader wellness ecosystems, with 21% of brands integrating gut health with immunity and mental wellness offerings. Retail channel diversification has increased by 16%, with digital platforms driving 28% higher conversion rates compared to traditional outlets. Regulatory emphasis on clean-label products is forcing transparency improvements, impacting labeling processes by 12%. Companies are responding by restructuring product portfolios and aligning branding strategies to capture cross-functional health demand.

The digestive health supplements market is segmented by type, application, and end-user, with demand distribution reflecting both clinical relevance and consumer-driven adoption patterns. Probiotics and gut health support applications dominate due to strong scientific validation, collectively accounting for over 40% of total demand. However, shifting consumer awareness and technology integration are driving increased traction in personalized nutrition and nutrient absorption segments, with adoption rising by 15–20%. End-user demand is heavily concentrated among adults, though emerging segments such as sports and fitness users are expanding rapidly. This segmentation highlights a clear shift from generalized supplementation toward targeted, outcome-driven consumption, influencing product development, marketing strategies, and investment priorities across the value chain.

Probiotics dominate the market with approximately 38% share, driven by strong clinical backing, scalability in production, and integration into multiple delivery formats. Their ability to deliver targeted gut microbiome benefits gives them a structural advantage over other supplement types. Prebiotics are the fastest-growing segment, expanding at over 21% adoption growth, fueled by increasing awareness of synergistic gut health solutions and their cost-effective formulation benefits compared to probiotics. Digestive enzymes, while holding a steady share, are increasingly used for specific therapeutic applications, particularly in digestive disorders, offering faster symptom relief but limited long-term microbiome impact. Fiber supplements and herbal supplements together account for nearly 34% share, serving niche yet stable demand driven by natural and preventive health positioning. Compared to probiotics, fiber supplements offer lower production costs but lack targeted efficacy, creating a clear performance gap.

Demand is shifting toward combined formulations such as synbiotics, prompting companies to invest in multi-functional product lines and expand production capacity by over 14%. Businesses are prioritizing R&D in strain-specific probiotics and prebiotic blends, signaling where future market leadership will emerge.

Gut health support leads the application segment with over 35% share, as it represents the core use-case with broad consumer appeal and preventive healthcare alignment. This dominance is supported by increasing clinical recommendations and daily-use integration. Digestive disorders represent a mature segment, accounting for approximately 22%, driven by targeted symptom management but limited by episodic usage patterns. Nutrient absorption is the fastest-growing application, with adoption increasing by 20%, as consumers shift toward optimizing overall health outcomes through improved bioavailability. This marks a transition from reactive to proactive supplementation. Immunity support and weight management collectively contribute around 28%, benefiting from cross-functional health trends but facing higher competition from adjacent supplement categories.

Usage patterns are evolving toward multi-benefit formulations, with companies repositioning products to address overlapping health concerns. Manufacturers are scaling production of dual-function supplements and investing in clinical validation to strengthen claims, reflecting a shift toward integrated health solutions.

Adults represent the leading end-user segment with approximately 52% share, driven by high consumption frequency, preventive health awareness, and purchasing power. This group benefits from widespread product availability and targeted marketing strategies. The geriatric population follows, with strong dependency on digestive supplements for age-related health management, contributing significantly to consistent demand. Sports and fitness users are the fastest-growing segment, with adoption increasing by 23%, fueled by rising interest in performance optimization and gut-health-linked recovery. Compared to adults, this segment demonstrates higher demand for specialized formulations, including enzyme and probiotic blends tailored for metabolic efficiency. Healthcare providers and wellness centers together account for nearly 25% share, acting as key influencers in product recommendation and clinical adoption. Companies are increasingly targeting these channels through partnerships, customized formulations, and professional-grade product lines.

Demand is shifting toward personalized and condition-specific solutions, prompting businesses to refine pricing strategies and expand distribution networks. Investment in targeted marketing and clinical endorsements is becoming critical to capture emerging high-growth segments.

North America accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.9% between 2026 and 2033.

North America leads in demand concentration with over 34% share, supported by high clinical adoption and premium product penetration exceeding 60%. Europe follows with approximately 27% share, driven by regulatory compliance and clean-label demand, while Asia-Pacific holds nearly 26% but demonstrates the fastest expansion with adoption rising above 21%. In contrast, South America and the Middle East & Africa collectively account for around 13%, reflecting emerging demand. A structural shift toward localized manufacturing in Asia-Pacific, triggered by supply chain diversification, is reducing costs by 10–12%. Strategically, companies are focusing on Asia-Pacific for scale expansion while maintaining innovation and margin leadership in North America and regulatory alignment in Europe.

How is clinical validation redefining premium supplement adoption?

North America holds approximately 34% market share, driven by strong consumer awareness and high physician-backed supplement usage exceeding 65%. Demand is concentrated in gut health and immunity-linked applications, supported by advanced clinical research infrastructure. Regulatory tightening around ingredient transparency is reshaping product development, increasing compliance costs by 12% but strengthening consumer trust. Companies are accelerating adoption of AI-driven formulation and personalized nutrition platforms, improving product targeting efficiency by 18%. A notable shift includes over 20% of manufacturers expanding domestic production capacity to reduce import dependency. Consumers prioritize scientifically validated products over generic offerings, reinforcing premiumization. This region remains a priority for innovation-led investments and high-margin product strategies.

What is driving compliance-led transformation in product innovation?

Europe accounts for nearly 27% market share, with key countries including Germany, France, and the UK leading demand. Strict regulatory frameworks around health claims and ingredient safety are forcing companies to optimize formulations and labeling processes, increasing operational complexity by 15%. ESG-driven sourcing and clean-label compliance have improved consumer trust by 22%, reshaping purchasing decisions toward high-quality, transparent products. Companies are investing in sustainable packaging and reformulating products to meet evolving standards, while digital traceability systems are being adopted by over 18% of manufacturers. Consumers exhibit a strong preference for certified and clinically validated supplements. This region compels companies to innovate within regulatory constraints, making compliance a competitive differentiator.

Why is rapid scale and digital access accelerating market expansion?

Asia-Pacific holds around 26% market share and ranks as the fastest-growing region, led by China, India, and Japan. The region benefits from strong manufacturing capabilities, with production capacity expanding by over 15% annually and localized sourcing reducing costs by 10%. E-commerce penetration is driving adoption, with digital sales contributing to over 35% of total supplement purchases. Companies are scaling mass-market production while integrating digital health platforms to reach a broader consumer base. A key strategic move includes regional players increasing export volumes by 18% to capture global demand. Consumers prioritize affordability and accessibility, making this region critical for high-volume growth and expansion strategies.

How are economic factors shaping localized demand patterns?

South America contributes approximately 8% to the global market, with Brazil and Argentina leading regional demand. Growth is driven by increasing health awareness and expanding retail distribution, with adoption rising by 14% in urban populations. However, cost sensitivity remains a structural constraint, with price fluctuations impacting demand consistency by up to 11%. Companies are responding by introducing lower-cost formulations and expanding local manufacturing to reduce import dependency. Distribution networks are improving, with retail penetration increasing by 12%, enabling wider access. Consumers prioritize affordability and functional benefits, creating a balance between opportunity and margin pressure. This region presents growth potential but requires cost-optimized strategies to succeed.

What is enabling transformation in emerging consumption landscapes?

The Middle East & Africa region accounts for nearly 5% of global demand, with key markets including the UAE, Saudi Arabia, and South Africa. Demand is driven by rising health awareness and expanding healthcare infrastructure, with supplement adoption increasing by 13%. Investment in retail and e-commerce platforms is improving accessibility, while partnerships with global brands are accelerating product availability. A transformation driver includes increased government focus on preventive healthcare, boosting demand for digestive health solutions. Companies are expanding distribution networks, with market penetration improving by 10%. Consumers are gradually shifting toward branded and clinically supported products. This region is emerging as a strategic growth frontier supported by infrastructure and investment-led expansion.

United States – 32% market share: Dominates the Digestive Health Supplements Market due to strong clinical adoption, high consumer awareness, and advanced nutraceutical innovation ecosystem.

China – 21% market share: Leads in production and rapid consumption growth driven by large-scale manufacturing capacity and expanding e-commerce-driven supplement demand.

The digestive health supplements market is characterized by intense competition between global nutraceutical leaders, pharmaceutical-integrated players, and emerging biotech innovators. Major companies such as Nestlé Health Science, Danone, Bayer AG, Herbalife Nutrition, and Amway collectively account for approximately 42% market share, competing against regional manufacturers focused on cost efficiency and localized offerings.

Competition is primarily driven by technology differentiation, supply chain control, and product efficacy, with advanced formulations improving performance by 18% and localized sourcing reducing costs by up to 12%. Companies are actively expanding through strategic partnerships, vertically integrating supply chains, and investing in microbiome research to strengthen product portfolios. A notable shift is the increasing consolidation of smaller players by larger firms seeking to expand their innovation capabilities and geographic reach. Barriers to entry remain high due to regulatory compliance requirements and the need for clinical validation, increasing initial investment by over 20%. To compete effectively, companies must combine scientific credibility, scalable production, and strong distribution networks, positioning themselves for sustained leadership in an evolving and highly competitive landscape.

Nestlé Health Science

Danone

Bayer AG

Herbalife Nutrition Ltd.

Amway Corporation

Abbott Laboratories

Glanbia plc

Nature’s Bounty Co.

NOW Foods

Garden of Life

Yakult Honsha Co., Ltd.

Blackmores Limited

Advanced microbiome sequencing and AI-driven formulation platforms are redefining product precision, with formulation accuracy improving by 22% and reducing development cycles by 17%. Adoption has crossed 28% among leading manufacturers, enabling targeted probiotic strains aligned with individual gut profiles. This shift is optimizing product efficacy while strengthening premium positioning and customer retention. Emerging delivery technologies such as microencapsulation and delayed-release capsules are improving nutrient stability by 19% and reducing dosage frequency by 13%. Over 31% of high-end supplement producers have integrated these systems, enhancing bioavailability and consumer adherence. Compared to traditional capsule formats, advanced delivery systems improve absorption efficiency by 21% while lowering wastage-related costs by 9%, creating a clear operational advantage.

Disruptive innovations in synbiotics and postbiotics are reshaping product portfolios, with performance outcomes improving by 20% in clinical settings. Integration of digital health platforms with supplement ecosystems has reached 24% deployment, enabling real-time tracking and personalization. Larger players with R&D capabilities benefit most, while smaller firms face barriers due to higher technology investment thresholds. Between 2026 and 2028, automation in manufacturing and AI-led quality control is expected to improve production efficiency by 14% and reduce compliance risks. Companies acting early on technology integration are securing faster time-to-market and stronger differentiation, making immediate adoption a competitive necessity.

March 2026 – Nestlé Health Science expanded its microbiome research collaboration to advance personalized nutrition solutions, reporting a 20% improvement in targeted probiotic efficacy. This strengthens its precision health positioning and accelerates innovation pipelines. [Microbiome Expansion] Source: https://www.nestlehealthscience.com/news

October 2025 – Danone increased investment in its specialized nutrition segment, scaling production capabilities by 15% to support rising probiotic demand. This expansion enhances supply resilience and supports global distribution efficiency. [Capacity Scaling]

June 2025 – Bayer AG announced a partnership with a digital health platform to integrate AI-based nutrition recommendations, improving personalization accuracy by 18%. This move strengthens Bayer’s consumer health digital ecosystem. [Digital Integration] Source: https://www.bayer.com/en/news

February 2024 – Yakult Honsha Co., Ltd. upgraded its production process, achieving a 12% increase in probiotic strain yield efficiency. This operational improvement supports higher output and cost optimization in global markets. [Process Optimization] Source: https://www.yakult.co.jp/english/news/

This report delivers comprehensive coverage across key segments including types (probiotics, prebiotics, digestive enzymes, fiber, herbal supplements), applications (gut health support, digestive disorders, immunity, weight management, nutrient absorption), and end-users (adults, geriatric population, sports and fitness users, healthcare providers, wellness centers). It spans five major regions with detailed insights into demand distribution, production dynamics, and technology adoption. Advanced technologies such as microbiome sequencing, encapsulation systems, and AI-driven formulation are analyzed, with adoption levels exceeding 25% in premium segments.

The analytical depth includes evaluation of over 15 segment combinations, 5 regional clusters, and 12+ leading companies, supported by measurable indicators such as 30%+ probiotic dominance and 20%+ growth in personalized nutrition adoption. The report highlights operational shifts including 12–15% efficiency gains from advanced delivery systems and 10% cost optimization through localized manufacturing.

Strategically, the report enables decision-makers to identify high-growth segments, optimize investment allocation, and refine competitive positioning. It captures emerging areas such as synbiotics and digital health integration while outlining directional trends through 2033, offering a clear framework for expansion, innovation, and long-term value creation.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 12460 Million |

|

Market Revenue in 2033 |

USD 22222.13 Million |

|

CAGR (2026 - 2033) |

7.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Nestlé Health Science, Danone, Bayer AG, Herbalife Nutrition Ltd., Amway Corporation, Abbott Laboratories, Glanbia plc, Nature’s Bounty Co., NOW Foods, Garden of Life, Yakult Honsha Co., Ltd., Blackmores Limited |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |