Reports

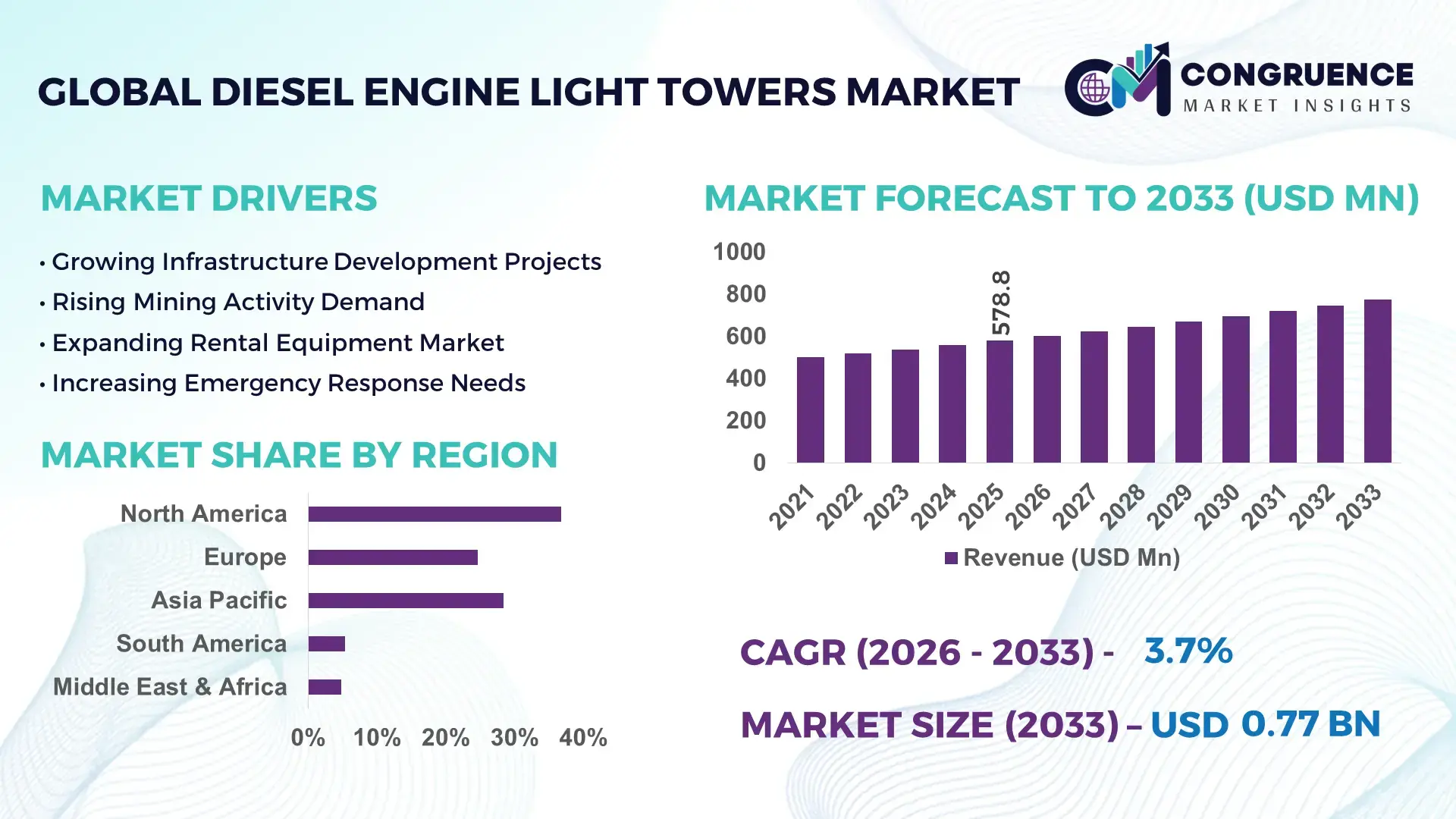

The Global Diesel Engine Light Towers Market was valued at USD 578.8 Million in 2025 and is anticipated to reach a value of USD 774.0 Million by 2033 expanding at a CAGR of 3.7% between 2026 and 2033. Growth is being accelerated by large-scale highway construction, mining expansion, utility maintenance programs, and rising deployment of mobile illumination systems across remote industrial sites requiring uninterrupted nighttime operations.

The United States dominates the global Diesel Engine Light Towers Market, accounting for nearly 28% of installed fleet capacity, supported by over USD 1.2 trillion in infrastructure modernization initiatives and extensive deployment across construction, oil & gas, and emergency response sectors. Compared with Germany, where diesel-powered mobile lighting adoption remains concentrated in industrial maintenance projects, the U.S. records over 35% higher utilization rates in large-scale infrastructure operations. The continued implementation of the Infrastructure Investment and Jobs Act is reinforcing equipment replacement cycles and operational deployment intensity.

Strategically, manufacturers that align product portfolios with infrastructure-led procurement programs and fleet modernization requirements are best positioned to strengthen long-term market penetration and utilization efficiency.

Market Size & Growth: USD 578.8 Million in 2025, reaching USD 774.0 Million by 2033 at 3.7% CAGR, supported by expanding infrastructure and mining project activity.

Top Growth Drivers: Infrastructure spending contributes 38% of demand growth, mining operations 27%, and utility maintenance projects 21%.

Short-Term Forecast: By 2028, advanced engine management systems are expected to improve fuel efficiency by 12% while reducing operating costs by 9%.

Emerging Technologies: IoT monitoring, remote fleet diagnostics, and hybrid power integration are improving asset utilization by over 15%.

Regional Leaders: North America (~USD 235 Million), Asia Pacific (~USD 185 Million), and Europe (~USD 145 Million) lead deployment through infrastructure expansion and industrial modernization.

Consumer/End-User Trends: More than 62% of rental fleet operators prioritize telematics-enabled light towers for utilization tracking and maintenance planning.

Pilot/Case Example: A 2024 highway modernization project in Texas reported a 14% reduction in nighttime operational delays through upgraded mobile lighting deployment.

Competitive Landscape: Atlas Copco holds approximately 18% market share alongside Generac, Allmand, Trime, and Wacker Neuson in a highly competitive global market.

Regulatory & ESG Impact: New off-road emission compliance requirements are reducing particulate emissions by up to 25% across upgraded fleets.

Investment & Funding: More than USD 450 Million has been directed toward manufacturing expansion, localization, and product modernization initiatives since 2023.

Innovation & Future Outlook: Smart-connected fleets, hybrid diesel systems, and predictive maintenance platforms are reshaping competitive differentiation amid global supply-chain realignment.

Diesel Engine Light Towers Market demand remains closely linked to infrastructure construction, surface mining, disaster recovery operations, and utility maintenance activities where reliable off-grid illumination is critical. Manufacturers are introducing telematics-enabled systems, advanced fuel management controls, and hybrid configurations that improve operating efficiency by nearly 15%. Increasing procurement requirements for lower-emission equipment and resilient field operations are encouraging fleet modernization, creating a favorable environment for strategic technology adoption and equipment differentiation.

The Diesel Engine Light Towers Market is becoming strategically important as governments, contractors, utilities, and industrial operators prioritize operational continuity across infrastructure modernization and remote project environments. Competitive differentiation is increasingly tied to equipment uptime, fuel efficiency, and digital fleet visibility. The ongoing restructuring of global construction supply chains and accelerated public infrastructure investment programs are reinforcing demand for dependable mobile lighting solutions that can operate in challenging field conditions.

Technology adoption is reshaping operational economics. Modern telematics-enabled diesel light towers deliver approximately 10–15% higher fleet utilization and reduce unplanned maintenance events by nearly 20% compared with conventional units lacking remote diagnostics. North America continues to lead large-scale deployment through transportation and utility projects, while India and Southeast Asia are experiencing faster equipment adoption due to expanding industrial corridors, renewable energy construction, and urban infrastructure development.

A practical example can be seen in large highway and transmission-line projects where connected light towers support centralized fleet management and improve nighttime work scheduling. Manufacturers are responding through strategic dealer expansion, digital service partnerships, and localized assembly capabilities. Over the next two to three years, increased adoption of predictive maintenance platforms and hybrid-ready architectures will strengthen operational performance. Companies that combine equipment reliability, digital capabilities, and service responsiveness will secure stronger competitive positioning across industrial and infrastructure ecosystems.

Global infrastructure modernization is creating sustained demand for diesel engine light towers across transportation, mining, and utility sectors. More than 60% of major highway projects worldwide now incorporate extended nighttime construction schedules to accelerate completion timelines, increasing dependence on portable illumination systems. Mining operators have also expanded mobile equipment deployment by approximately 18% across remote extraction sites. The U.S. Infrastructure Investment and Jobs Act and India's National Infrastructure Pipeline continue to support long-duration project activity requiring reliable lighting assets. This demand directly improves fleet utilization and replacement cycles, prompting manufacturers to expand production capacity, strengthen rental partnerships, and integrate telematics solutions. A notable strategic insight is that contractors increasingly evaluate light towers based on lifecycle productivity rather than upfront acquisition cost, shifting competition toward performance-driven product differentiation.

Rising emission standards and fluctuating diesel fuel costs remain significant constraints on market expansion. Compliance-related upgrades can increase equipment acquisition costs by 10–15%, while fuel expenses represent nearly 35% of total operating expenditure for intensive deployment applications. In Germany and other industrialized markets, stricter off-road engine regulations are accelerating replacement requirements and increasing procurement complexity. These factors directly affect rental fleet profitability and purchasing decisions among cost-sensitive contractors. To reduce exposure, manufacturers are diversifying supplier networks, localizing component sourcing, and introducing fuel-optimized engine platforms. An important operational insight is that buyers increasingly prioritize total cost of ownership calculations, forcing suppliers to balance regulatory compliance with competitive pricing and equipment reliability.

The strongest emerging opportunity lies in connected fleet ecosystems and hybrid power configurations. Telematics adoption among mobile equipment fleets has increased by more than 30% over the past several years, while predictive maintenance systems can reduce service-related downtime by approximately 20%. India, Saudi Arabia, and Indonesia are expanding infrastructure and industrial developments that create demand for advanced fleet management capabilities. Hybrid diesel-battery architectures are also gaining traction by lowering fuel consumption by nearly 15% during intermittent operation. Manufacturers are increasing R&D investments, forming software partnerships, and developing smart asset-management platforms to capture these opportunities. A less obvious advantage is the growing value of operational data, enabling fleet owners to optimize deployment strategies, improve utilization rates, and strengthen project-level productivity outcomes.

Long-term market expansion faces challenges associated with technical workforce shortages, dispersed project locations, and increasingly sophisticated equipment architectures. Service response times can account for up to 12% of project-related operational delays in remote industrial environments. At the same time, connected equipment deployments require additional technician training, with digital diagnostic requirements increasing service complexity by nearly 25% compared with conventional units. Large mining and infrastructure projects in Australia, Canada, and remote regions of Africa highlight the importance of dependable maintenance ecosystems. Failure to maintain service consistency can reduce equipment availability and weaken customer retention. To address this challenge, manufacturers are investing in technician training programs, dealer-network expansion, remote diagnostics platforms, and predictive service models that enhance long-term operational reliability and competitive resilience.

Smart Fleet Monitoring Expansion Advanced telematics integration is transforming fleet management across construction and mining sites. More than 45% of newly deployed light towers now include remote diagnostics and asset-tracking functionality, while maintenance-related downtime has declined by nearly 20%. Labor shortages and increasing equipment utilization targets are driving adoption. Manufacturers are embedding cloud-based monitoring systems and predictive service tools to improve uptime, optimize deployment schedules, and reduce field maintenance costs.

Hybrid Power Configuration Adoption Hybrid diesel-battery systems are gaining traction as fleet operators seek lower fuel consumption and extended operating flexibility. Fuel usage reductions of 12–18% and engine runtime declines of approximately 25% are being recorded in intermittent-use environments. Stricter emissions requirements and contractor sustainability targets are accelerating this transition. Equipment suppliers are expanding hybrid product portfolios and redesigning power management systems to support longer operating cycles without compromising illumination performance.

Rental Fleet Modernization Acceleration Rental companies are increasingly replacing aging fleets with digitally connected and fuel-efficient equipment. Nearly 35% of fleet renewal programs initiated since 2024 prioritize telematics-ready models, while utilization rates have improved by approximately 14%. Large infrastructure projects are demanding higher equipment availability and operational visibility. In response, manufacturers are strengthening rental partnerships, offering service-based contracts, and increasing localized inventory availability to support faster deployment.

Localized Manufacturing Strategies Supply-chain resilience has become a strategic priority as procurement teams seek shorter lead times and improved component availability. Lead-time reductions of nearly 22% have been achieved through regional sourcing initiatives, while localized assembly operations have increased by approximately 15% among major suppliers. Continued logistics disruptions and procurement uncertainty are encouraging manufacturers to diversify supplier networks, establish regional production hubs, and improve inventory planning to maintain deployment consistency.

Diesel-powered light towers remain the leading segment, accounting for approximately 68% of total deployments, supported by their proven reliability, extended runtime capabilities, and suitability for remote construction, mining, and oilfield operations. Their ability to operate continuously in off-grid environments makes them the preferred option for large infrastructure projects where uninterrupted illumination is critical. Fleet operators continue to prioritize diesel-powered units due to established fueling networks and lower operational disruption risks. Manufacturers are enhancing these systems through fuel-efficient engines, telematics integration, and improved lighting performance to maintain competitiveness. Hybrid diesel-powered light towers represent the fastest-growing segment, with adoption increasing by nearly 16% annually across rental and infrastructure fleets. Organizations are seeking equipment that balances operational reliability with reduced fuel consumption and maintenance requirements. Solar-assisted and battery-supported variants are gaining visibility in temporary worksites, although they remain a smaller portion of overall deployment volumes. Companies are increasing investment in hybrid product development, strategic partnerships, and intelligent power management technologies. This shift is influencing procurement priorities, encouraging customers to evaluate long-term operating efficiency alongside traditional performance metrics.

Construction remains the dominant application segment, representing approximately 42% of market demand due to extensive use in road development, bridge construction, rail projects, and urban infrastructure modernization. Nighttime construction scheduling has expanded significantly as contractors seek to accelerate project completion and minimize traffic disruptions. High equipment utilization rates and continuous operational requirements sustain strong demand. Manufacturers are responding by introducing durable, high-output lighting systems capable of supporting demanding construction environments and extended operating cycles. Mining is the fastest-growing application segment, supported by increasing mineral extraction activity and expansion of remote-site operations. Deployment across mining environments has increased by nearly 18%, reflecting rising investment in critical minerals and resource development projects. Oil & gas, emergency response, and event management applications continue to maintain strategic importance, particularly in regions with large-scale industrial activity. Companies are adapting through specialized product configurations, enhanced mobility features, and remote monitoring capabilities. Demand is increasingly shifting toward applications requiring greater operational visibility, workforce safety, and equipment productivity during nighttime operations.

Rental companies represent the largest end-user segment, accounting for approximately 48% of total equipment purchases due to the growing preference for asset-light procurement models among contractors and industrial operators. Construction firms increasingly rely on rental fleets to manage project variability and control capital expenditure. Large rental providers are prioritizing fleet modernization programs featuring telematics-enabled and fuel-efficient equipment. Manufacturers are strengthening channel partnerships and expanding after-sales support to capture long-term rental fleet demand. Infrastructure contractors are emerging as the fastest-growing end-user group, with deployment activity increasing by approximately 15% as governments accelerate transportation, utility, and urban development projects. Mining companies continue to represent a significant buyer segment due to the need for reliable illumination across remote operational sites. Utility providers and emergency response organizations are also increasing procurement of advanced mobile lighting systems to improve operational readiness. Companies are responding through customized product offerings, flexible financing arrangements, and service-oriented business models. Competitive positioning increasingly depends on delivering equipment tailored to the operational requirements of distinct end-user categories.

North America accounted for the largest market share at 36.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 4.5% between 2026 and 2033.

North America maintains the leading position in the Diesel Engine Light Towers Market due to extensive infrastructure rehabilitation programs, utility-grid upgrades, energy-sector investments, and large-scale construction activity. The region contributes approximately 36.8% of global demand, with deployment heavily concentrated across transportation corridors, mining operations, and emergency response networks. Nighttime construction activity has increased by nearly 18% across major highway modernization projects, supporting stronger equipment utilization rates. Rental companies remain critical procurement channels, accounting for a significant share of fleet acquisitions. Manufacturers are expanding telematics-enabled product offerings and strengthening dealer-service networks to improve uptime, asset visibility, and lifecycle efficiency across increasingly complex project environments.

United States Market Outlook: The United States represents the largest country market due to its extensive infrastructure base, large rental fleet ecosystem, and high construction equipment utilization. More than 45% of regional mobile lighting deployments are linked to transportation, utility, and energy infrastructure projects. Federal investment programs continue to accelerate road, bridge, and transmission-line upgrades, creating sustained demand for high-performance lighting systems. Equipment providers are prioritizing digital fleet management capabilities, localized service support, and product modernization to meet increasingly sophisticated contractor requirements.

Europe remains a strategically important market, accounting for approximately 24.6% of global demand, supported by industrial maintenance, transportation infrastructure upgrades, and regulatory-driven equipment replacement cycles. The region is witnessing increased adoption of fuel-efficient and lower-emission light tower platforms as environmental compliance requirements become more stringent. Nearly 30% of fleet replacement programs initiated since 2024 have focused on improving operational efficiency and emission performance. Rental operators and infrastructure contractors are increasingly integrating connected equipment solutions to optimize maintenance scheduling and utilization rates. Manufacturers continue to invest in advanced engine technologies and hybrid-ready platforms to align with evolving procurement expectations.

Germany Market Outlook: Germany leads the European market through its strong industrial foundation, engineering expertise, and extensive infrastructure maintenance activity. Industrial facilities, logistics hubs, and transportation networks account for a substantial share of equipment deployments. Approximately 35% of large infrastructure contractors have expanded investments in digitally monitored mobile equipment to improve operational planning and maintenance efficiency. German enterprises continue to prioritize durable, compliant, and technologically advanced lighting solutions that support long-duration projects and industrial modernization objectives.

Asia-Pacific accounts for approximately 28.4% of global market activity and represents the fastest-evolving deployment environment for diesel engine light towers. Rapid urbanization, industrial expansion, transportation corridor development, and energy-sector investments continue to strengthen equipment demand. Infrastructure construction activity across key economies has increased by nearly 20% over recent years, driving greater reliance on mobile lighting assets for extended work schedules. Manufacturing expansion and mining development are also contributing to stronger fleet deployment. Suppliers are increasing regional assembly capabilities, distribution partnerships, and localized product customization to capture expanding demand across diverse project environments.

China Market Outlook: China remains the most influential country market due to its unmatched infrastructure construction scale, industrial capacity, and manufacturing ecosystem. Large transportation, logistics, and industrial development programs continue to support significant deployment volumes. More than 40% of regional large-scale infrastructure projects require extended nighttime operations, reinforcing demand for dependable lighting solutions. Domestic manufacturers are expanding production capabilities and integrating smart monitoring technologies to strengthen competitiveness while supporting increasingly complex construction and industrial applications.

South America contributes approximately 5.4% of global demand, with mining operations serving as the primary deployment driver across the region. Copper, lithium, iron ore, and energy-sector projects continue to create sustained requirements for mobile illumination systems capable of operating in remote environments. Equipment utilization across mining applications has increased by approximately 16%, reflecting continued investment in resource development. However, infrastructure constraints and procurement volatility remain important operational considerations. Manufacturers are addressing these challenges through distributor expansion, localized inventory strategies, and enhanced aftermarket support to improve equipment availability and service responsiveness.

Brazil Market Outlook: Brazil represents the region's largest market due to its diversified industrial base, extensive infrastructure network, and growing mining activity. Construction projects, logistics developments, and energy-sector investments continue to strengthen deployment opportunities. Nearly 38% of national equipment demand is linked to large-scale infrastructure and industrial projects requiring reliable nighttime operations. Suppliers are increasingly focusing on service-network expansion and fleet modernization initiatives to support rising customer expectations around equipment productivity and operational continuity.

The Middle East & Africa region accounts for approximately 4.8% of global market activity, supported by large-scale infrastructure development, energy-sector expansion, and industrial modernization initiatives. Construction megaprojects, transportation upgrades, and mining operations continue to generate substantial demand for high-capacity lighting systems. Deployment volumes associated with major development programs have increased by nearly 22% in recent years. Equipment providers are strengthening regional partnerships, expanding service capabilities, and introducing advanced fleet-management solutions to support increasingly sophisticated project requirements. Operational reliability remains a key procurement factor due to harsh environmental conditions and remote deployment locations.

Saudi Arabia Market Outlook: Saudi Arabia leads the regional market through extensive infrastructure investments, industrial diversification programs, and large-scale development initiatives. Major construction and energy projects continue to require substantial mobile lighting capacity to support continuous operations. More than 30% of regional megaproject-related deployments are concentrated within the country, reflecting its strategic importance. Companies are expanding local partnerships, equipment inventories, and technical support capabilities to align with accelerating project execution timelines and growing demand for advanced field-deployment solutions.

The Diesel Engine Light Towers Market is led by global manufacturers such as Atlas Copco, Generac Holdings, Wacker Neuson, Trime, and Allmand Bros.. Global leaders compete against regional manufacturers on technology, fleet support, and product reliability, while regional players challenge through aggressive pricing and localized service networks. The top five companies collectively control approximately 52–58% of global market activity. Competition is increasingly centered on telematics integration, fuel efficiency, and lifecycle operating costs. Connected fleet solutions improve utilization rates by nearly 15%, while advanced LED systems reduce energy consumption by 20–30% compared with older configurations. Companies are expanding rental partnerships, strengthening dealer networks, localizing assembly operations, and introducing hybrid-powered platforms to improve market reach and operational differentiation. The competitive landscape is shifting toward digital fleet management and hybrid energy integration. Supply-chain resilience and aftermarket service capabilities have become critical pressure points. Success increasingly depends on delivering high-uptime equipment, strong service infrastructure, intelligent monitoring capabilities, and cost-efficient ownership models that outperform both premium global brands and low-cost regional alternatives.

Generac Holdings Inc.

Wacker Neuson SE

Trime S.r.l.

Allmand Bros., Inc.

Multiquip Inc.

Doosan Portable Power

J C Bamford Excavators (JCB)

LARSON Electronics LLC

Chicago Pneumatic

Progress Solar Solutions

Himoinsa S.L.

The market is undergoing a technology transition from conventional metal-halide lighting systems toward LED-based intelligent lighting platforms. Modern LED light towers reduce energy consumption by 25–35% while improving illumination consistency and lowering maintenance requirements. More than 60% of newly procured units now incorporate LED technology due to longer service life and improved operational efficiency. Contractors and rental companies benefit through reduced fuel consumption, longer operating intervals, and lower ownership costs.

Connected fleet technologies are becoming mainstream across infrastructure and mining operations. Telematics-enabled towers improve fleet utilization by approximately 15% and reduce maintenance-related downtime by nearly 20% through predictive diagnostics. Remote asset monitoring, geofencing, and performance analytics are increasingly integrated into fleet management workflows. Global fleet operators and rental providers gain a competitive advantage through improved deployment visibility, asset tracking, and maintenance planning capabilities.

Between 2026 and 2028, hybrid diesel-battery systems and intelligent energy management platforms are expected to become key differentiators. Hybrid architectures can lower fuel usage by 12–18% compared with conventional diesel-only systems while reducing engine runtime substantially. Manufacturers investing in smart controls, battery integration, and digital service ecosystems will strengthen competitive positioning as procurement priorities shift toward efficiency, operational intelligence, and sustainability-focused equipment performance.

June 2024 – Atlas Copco launched the HiLight V4W light tower designed for operation above 2,000 meters altitude and temperatures exceeding 40°C, strengthening its position in mining and infrastructure projects requiring extreme-environment performance and higher operational reliability. Source: www.atlascopco.com

January 2024 – Atlas Copco introduced the HiLight BI+ 4 hybrid light tower integrating lithium-ion batteries with a Stage V diesel engine, enabling multi-mode operation and improved fuel efficiency. The innovation supports lower operating costs and greater deployment flexibility across construction and emergency-response applications.

April 2025 – Generac Holdings expanded its energy equipment portfolio through new high-capacity power solutions targeting critical infrastructure markets. The initiative strengthens integration capabilities across energy ecosystems and enhances Generac’s position in advanced mobile and backup power applications.

March 2025 – Wacker Neuson reported free cash flow growth to EUR 184.6 million, enabling stronger investment capacity for product development, dealer support, and operational efficiency initiatives. The financial improvement supports future equipment innovation and competitive market expansion strategies.

The report provides comprehensive coverage of the Diesel Engine Light Towers Market across major product types, applications, end-user groups, and geographic regions. The analysis evaluates diesel-powered, hybrid-powered, and emerging lighting solutions across construction, mining, oil & gas, infrastructure development, emergency response, and industrial maintenance environments. More than 60% of market demand is concentrated in infrastructure and industrial applications, while rental fleets continue to represent a major procurement channel influencing deployment trends and equipment specifications.

The study examines North America, Europe, Asia-Pacific, South America, and Middle East & Africa, incorporating operational deployment patterns, technology adoption rates, competitive positioning, and evolving procurement priorities. It assesses developments in telematics integration, LED lighting systems, hybrid power architectures, and predictive maintenance platforms. Strategic insights support investment planning, market-entry evaluation, product development decisions, partnership opportunities, expansion strategies, and long-term competitive positioning across the 2026–2033 forecast period, while identifying high-potential growth pockets and emerging operational requirements across global end-user industries.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 578.8 Million |

| Market Revenue (2033) | USD 774.0 Million |

| CAGR (2026–2033) | 3.7% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Atlas Copco; Generac Holdings Inc.; Wacker Neuson SE; Trime S.r.l.; Allmand Bros., Inc.; Multiquip Inc.; Doosan Portable Power; J C Bamford Excavators (JCB); LARSON Electronics LLC; Chicago Pneumatic; Progress Solar Solutions; Himoinsa S.L. |

| Customization & Pricing | Available on Request (10% Customization Free) |