Reports

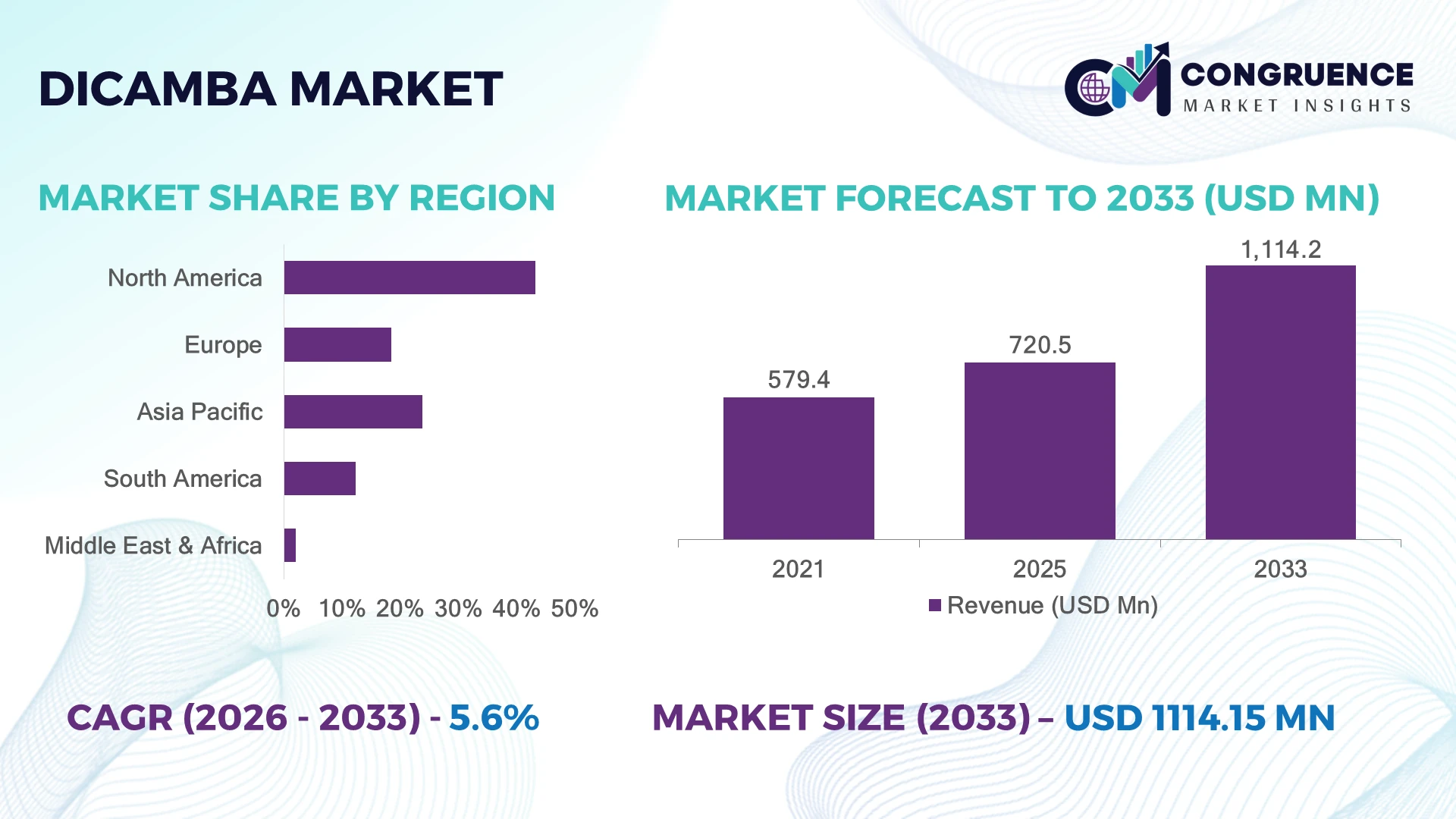

The Global Dicamba Market was valued at USD 720.5 Million in 2025 and is anticipated to reach a value of USD 1,114.2 Million by 2033 expanding at a CAGR of 5.6% between 2026 and 2033. Increasing adoption of herbicide-resistant crop systems, precision agriculture practices, and advanced weed management solutions are accelerating Dicamba Market growth.

The United States dominated the Dicamba Market with nearly 42% share in 2025, supported by large-scale soybean and cotton cultivation, advanced agrochemical infrastructure, and widespread herbicide technology adoption. U.S. dicamba-resistant crop utilization remained approximately 30% higher than Brazil due to established biotechnology integration and precision farming systems. Regulatory adjustments surrounding herbicide application practices are reshaping formulation innovation and responsible usage strategies.

Agricultural companies investing in advanced dicamba formulations and sustainable weed control solutions are strengthening productivity, compliance readiness, and competitive positioning.

• Market Size & Growth: USD 720.5 Million in 2025 reaching USD 1,114.2 Million by 2033 at 5.6% CAGR through herbicide-resistant crop adoption and precision farming expansion.

• Top Growth Drivers: Herbicide-resistant crop adoption increased 35%, precision spraying expanded 28%, and integrated weed management demand grew 32%.

• Short-Term Forecast: By 2028, advanced application technologies are expected to reduce herbicide drift-related losses by nearly 25%.

• Emerging Technologies: Precision spraying, low-volatility formulations, and digital agriculture tools are improving application accuracy and efficiency.

• Regional Leaders: North America, Asia-Pacific, and South America are projected toward USD 430 Million, USD 290 Million, and USD 240 Million through agricultural modernization.

• Consumer/End-User Trends: Commercial farming operations represent over 65% usage due to large-scale crop protection requirements.

• Pilot/Case Example: 2025 precision agriculture programs improved herbicide application efficiency by nearly 30% through sensor-based spraying technologies.

• Competitive Landscape: Leading agrochemical companies hold nearly 55% share, including Bayer, BASF, Corteva, and Syngenta.

• Regulatory & ESG Impact: Improved formulation technologies reduced off-target movement risks by approximately 20% through controlled application practices.

• Investment & Funding: Over USD 3 Billion agricultural technology investments target crop protection innovation, automation, and sustainable farming solutions.

• Innovation & Future Outlook: Next-generation herbicide systems are shifting toward precision application, resistance management, and environmentally optimized formulations.

Dicamba remains a critical herbicide solution for controlling broadleaf weeds across soybean, cotton, cereals, and other agricultural systems. Advanced formulations and precision application technologies are improving field performance by nearly 25% while supporting evolving regulatory requirements. Increasing herbicide resistance challenges and demand for higher crop productivity are reshaping crop protection strategies worldwide.

The Dicamba Market is becoming strategically important as farmers and agricultural companies focus on improving weed resistance management, crop productivity, and efficient land utilization. Changing regulatory frameworks and increasing herbicide resistance concerns are driving investment in improved formulations, precision application systems, and integrated crop management solutions.

Compared with conventional spraying approaches, precision herbicide application technologies improve chemical utilization efficiency by nearly 30% and reduce off-target application risks by approximately 25%. North America leads through biotechnology adoption and large-scale farming systems, while Asia-Pacific is expanding through agricultural modernization and increasing demand for efficient crop protection. Nearly 40% of commercial farming operations are integrating digital tools to improve chemical application decisions.

Large-scale soybean and cotton producers are adopting dicamba-based systems alongside precision agriculture platforms to optimize weed control. Agrochemical companies are adjusting investments toward formulation improvement, stewardship programs, and technology partnerships. Long-term competitiveness will depend on regulatory alignment, innovation capability, and delivery of efficient crop protection solutions.

Increasing adoption of herbicide-tolerant crop systems and demand for effective broadleaf weed management are strengthening dicamba usage across commercial agriculture. Nearly 60% of large-scale soybean and cotton producers rely on advanced herbicide programs to manage resistant weeds and maintain yield stability. Precision farming adoption has improved application efficiency by approximately 28%. Evolving agricultural practices in the United States are accelerating investment in optimized crop protection solutions. Companies are responding through formulation upgrades, farmer training initiatives, and integrated weed management programs.

Dicamba adoption faces limitations from stricter application regulations, environmental concerns, and off-target movement challenges. Nearly 35% of growers using advanced herbicide systems identify changing compliance requirements as a key operational concern. Application restrictions and weather-dependent spraying conditions can reduce usage flexibility by approximately 20%. Regulatory scrutiny in major agricultural markets has increased pressure on product development strategies. Companies are reducing risks through low-volatility formulations, improved labeling practices, application technologies, and stewardship programs.

Growth in digital farming technologies and next-generation herbicide formulations is creating opportunities for more efficient dicamba deployment. Smart spraying systems can improve application accuracy by nearly 30% through sensors, automation, and targeted weed detection. Around 40% of advanced farming operations are increasing investment in precision crop protection tools. Innovation in formulation chemistry and application systems is helping balance productivity needs with environmental requirements. Companies are positioning through R&D investment, technology collaborations, and integrated agricultural platforms.

Maintaining dicamba effectiveness requires addressing weed resistance evolution, application consistency, and sustainable crop protection practices. Nearly 30% of agricultural regions with intensive herbicide usage report increasing pressure from resistant weed populations. Complex field conditions and improper application methods create challenges for performance consistency. Farmers require stronger training, monitoring, and integrated management approaches. Companies must invest in resistance management programs, diversified product portfolios, and agronomic support systems to sustain long-term market relevance.

• Precision Application Technology Growth: Farmers are adopting GPS-enabled sprayers, sensors, and automated application platforms to improve dicamba efficiency. Nearly 35% of large farming operations use precision spraying tools, reducing chemical waste by approximately 25%. Companies are integrating digital agriculture solutions to improve compliance and field productivity.

• Low-Volatility Formulation Innovation: Agrochemical manufacturers are developing improved dicamba formulations focused on reducing drift risk and enhancing application control. Advanced formulations have lowered off-target movement concerns by nearly 20%. Companies are investing in chemistry improvements and stewardship programs to meet evolving agricultural regulations.

• Integrated Weed Management Expansion: Farmers are combining dicamba with diversified weed control strategies to improve resistance management. Nearly 45% of commercial growers use multi-mode herbicide programs for improved field outcomes. Agricultural companies are expanding advisory services and integrated crop protection solutions.

• Digital Farming Integration: Data-driven agriculture platforms are transforming herbicide planning, monitoring, and application decisions. Around 40% of technology-enabled farms use digital tools for crop protection optimization. Companies are partnering with agri-tech providers to enhance decision support systems and improve operational efficiency.

Liquid dicamba formulations dominate the Dicamba Market due to their ease of application, compatibility with modern spraying systems, and strong adoption across large-scale farming operations. Liquid formulations account for nearly 68% of usage, supported by better mixing efficiency, improved coverage, and integration with precision agriculture equipment. Dry formulations are witnessing faster adoption growth in selected markets due to improved storage flexibility, transportation advantages, and demand from regions requiring longer product shelf life.

Water-dispersible granules and other specialized formulations continue gaining relevance as growers prioritize application safety, handling efficiency, and environmental compliance. Nearly 35% of new formulation development focuses on reducing volatility and improving targeted delivery. Agrochemical companies are investing in advanced formulation chemistry, optimized packaging solutions, and farmer support programs to improve product performance while addressing changing regulatory and operational requirements.

• A 2025 crop protection industry assessment highlighted that more than 55% of large-scale farming operations are shifting toward improved herbicide formulations and precision application systems to enhance weed control efficiency and reduce application variability.

Soybean applications represent the leading segment in the Dicamba Market due to widespread adoption of herbicide-tolerant crop systems and increasing need for effective broadleaf weed control. Soybeans account for approximately 52% of dicamba consumption, supported by extensive cultivation across the United States, Brazil, and other major agricultural economies. Cotton applications are experiencing the fastest adoption shift as growers increase usage of advanced weed management programs to control resistant weed populations.

Cereal crops, pastures, and other agricultural applications continue supporting diversified dicamba demand through targeted vegetation management and crop protection practices. Nearly 40% of commercial growers are combining dicamba with integrated weed management strategies to improve long-term field productivity. Companies are adapting through improved application technologies, crop-specific solutions, and digital farming integration to strengthen herbicide performance and regulatory compliance.

• A 2026 agricultural technology review reported that precision-based herbicide programs improved weed management efficiency by nearly 30% across soybean and cotton production systems through optimized application timing and monitoring.

Commercial farmers represent the dominant end-user group in the Dicamba Market due to extensive herbicide usage across high-acreage soybean, cotton, and cereal production systems. This segment accounts for nearly 62% of demand, supported by mechanized farming practices, herbicide-resistant crop adoption, and increasing focus on yield protection. Agricultural cooperatives are emerging as the fastest-growing end-user group as farmers rely on shared resources, advisory services, and bulk procurement models.

Research institutions, contract farming organizations, and other agricultural users continue contributing through field trials, formulation testing, and specialized crop management programs. Nearly 38% of advanced farming enterprises are increasing investment in precision herbicide solutions and integrated weed control platforms. Companies are targeting these users through customized formulations, technical support programs, digital advisory services, and strategic partnerships to strengthen long-term customer relationships.

• A 2025 farm management industry survey indicated that over 50% of large agricultural enterprises adopted digital or precision-based crop protection practices to improve chemical efficiency, productivity, and sustainable farming outcomes.

North America accounted for the largest market share at 43.2% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.4% between 2026 and 2033.

North America leads the Dicamba Market due to extensive adoption of herbicide-resistant crops, large-scale commercial farming systems, and advanced crop protection technologies. The region accounted for 43.2% market share in 2025, supported by strong soybean and cotton cultivation across major agricultural states. Nearly 60% of regional dicamba demand comes from large farming enterprises focused on managing herbicide-resistant weeds and improving yield protection. Precision spraying systems, digital farm management platforms, and low-volatility formulations are reshaping application practices. Agrochemical companies are investing in formulation improvements, stewardship initiatives, and farmer training programs, with precision herbicide adoption improving application accuracy by approximately 30%.

United States Market Outlook: The United States dominates regional demand through large soybean acreage, biotechnology adoption, and advanced agricultural infrastructure. Dicamba-resistant crop systems remain widely used among commercial growers managing difficult weed populations. Nearly 70% of regional dicamba consumption is linked to U.S. farming operations, supported by strong distribution networks, precision agriculture investment, and continuous crop protection innovation.

Europe’s Dicamba Market is shaped by strict agricultural regulations, sustainable farming objectives, and demand for controlled herbicide application technologies. The region accounted for nearly 18.5% market share in 2025, with usage concentrated across cereal production, pasture management, and selective weed control applications. Around 40% of agricultural chemical development initiatives focus on improving environmental compatibility and application efficiency. Manufacturers are prioritizing safer formulations, precision delivery solutions, and compliance-focused product strategies to align with evolving farming standards and sustainability requirements.

Germany Market Outlook: Germany leads European adoption through advanced agricultural practices, strong agrochemical research capabilities, and technology-driven farming systems. Farmers increasingly utilize optimized crop protection solutions to maintain productivity while meeting regulatory requirements. Nearly 35% of precision farming operations in the country integrate digital monitoring technologies to improve chemical application efficiency and field-level decision-making.

Asia-Pacific is witnessing increasing dicamba adoption through agricultural modernization, rising food production requirements, and expanding commercial farming practices. The region accounted for approximately 23.8% market share in 2025, supported by China, India, and Australia’s focus on improving crop yields. Nearly 45% of new herbicide demand is associated with mechanized farming expansion and improved weed control practices. Companies are strengthening regional distribution networks, farmer education programs, and crop-specific solutions to improve herbicide accessibility and application effectiveness.

China Market Outlook: China represents the largest Asia-Pacific market due to extensive agricultural production, domestic agrochemical manufacturing strength, and modernization initiatives. Farmers are adopting advanced herbicide systems to improve operational efficiency and manage weed pressure. Nearly 40% of regional crop protection production capacity is concentrated in China, supporting both domestic demand and international agricultural supply chains.

South America’s Dicamba Market is expanding through strong soybean cultivation, commercial agriculture growth, and increasing focus on resistant weed management. The region accounted for nearly 12.4% market share in 2025, with Brazil and Argentina driving adoption across large farming areas. Approximately 55% of regional dicamba usage is linked to soybean and row crop production. Regulatory differences and application management challenges influence adoption patterns, encouraging companies to strengthen farmer support programs and responsible usage initiatives.

Brazil Market Outlook: Brazil leads regional growth due to its extensive soybean production base, expanding agricultural technology adoption, and large commercial farming operations. Growers are increasingly using integrated weed management strategies to protect crop productivity. Nearly 50% of regional herbicide demand is generated from Brazilian farms, supported by agricultural expansion and investment in modern farming solutions.

Middle East & Africa adoption is supported by agricultural modernization initiatives, food security investments, and gradual transition toward advanced farming inputs. The region accounted for nearly 2.1% market share in 2025, with demand concentrated across commercial farms and developing agricultural zones. Around 30% of modern farming projects are integrating improved crop protection products to increase productivity under challenging environmental conditions. Agrochemical suppliers are expanding partnerships, training programs, and distribution channels to improve product availability.

South Africa Market Outlook: South Africa represents the leading regional market due to its developed agricultural sector, commercial crop production, and adoption of modern farming technologies. Farmers are increasingly implementing structured weed management practices across cereals and other crops. Nearly 45% of regional advanced crop protection usage is concentrated in South Africa, supported by established agricultural infrastructure and technical expertise.

The Dicamba Market is led by Bayer, BASF, Syngenta, Corteva Agriscience, and Nufarm, where global agrochemical innovators compete with regional formulation manufacturers and cost-efficient suppliers. The top five players collectively account for nearly 58% share, reflecting strong concentration through patented formulations, distribution networks, and crop technology integration. Competition is driven by formulation performance, regulatory compliance, farmer support, and supply reliability, with advanced herbicide technologies improving application efficiency by nearly 30% and reducing drift concerns by around 20%. Companies are competing through product innovation, precision agriculture partnerships, expanded manufacturing capabilities, and integrated crop protection platforms. The competitive shift is moving toward low-volatility formulations, digital spraying systems, and sustainable weed management solutions. Regulatory approval complexity, R&D investment requirements, and farmer adoption challenges remain major entry barriers. Winning against established players requires formulation innovation, strong agricultural networks, compliance expertise, and technology-enabled crop protection solutions.

• Bayer AG

• BASF SE

• Syngenta Group

• Corteva Agriscience

• Nufarm Limited

• Albaugh LLC

• UPL Limited

• ADAMA Agricultural Solutions Ltd.

• FMC Corporation

• Gharda Chemicals Limited

• Jiangsu Yangnong Chemical Co., Ltd.

• Sharda Cropchem Limited

Current dicamba technologies focus on low-volatility formulations, precision application systems, and herbicide-resistant crop integration to improve weed control efficiency and application reliability. Advanced formulation chemistry reduces off-target movement risks by nearly 20%, while digital spraying platforms enhance application accuracy by approximately 25%. Nearly 45% of large commercial farms are integrating precision tools with crop protection programs to improve field-level decision-making.

Emerging technologies include AI-enabled spraying systems, sensor-based weed detection, and advanced formulation stabilization methods. Compared with conventional broadcast spraying, smart application technologies improve herbicide utilization efficiency by nearly 30% through targeted delivery and real-time monitoring. Agrochemical innovators, precision agriculture companies, and large farming enterprises benefit from reduced chemical waste, stronger compliance, and improved productivity.

From 2026 to 2028, technology development will focus on automated weed identification, integrated crop management platforms, and environmentally optimized herbicide systems. Companies adopting these innovations will improve farmer engagement, strengthen regulatory positioning, and gain competitive advantages through efficient, data-driven crop protection solutions.

• February 2024 – Bayer announced updates to its crop protection strategy, focusing on advanced herbicide solutions and stewardship initiatives supporting resistant weed management across millions of agricultural acres. The move strengthened farmer support programs and sustainable application practices. Source: bayer.com

• March 2025 – BASF expanded its agricultural innovation activities with improved crop protection technologies designed to enhance application efficiency by approximately 20%. The initiative supported growers through advanced formulations, resistance management solutions, and precision farming integration. Source: basf.com

• January 2025 – Syngenta advanced its digital agriculture and crop protection platforms, improving field-level decision capabilities and supporting more than 200 million acres globally. The expansion enhanced sustainable farming practices and herbicide management strategies. Source: syngenta.com

• May 2024 – Corteva Agriscience strengthened its crop protection portfolio through formulation improvements and farmer-focused technology initiatives, supporting improved herbicide performance and operational efficiency. Enhanced agricultural solutions increased integrated weed management capabilities across key farming markets. Source: corteva.com

The Dicamba Market Report provides comprehensive analysis across formulation types, applications, end-users, regional developments, technology trends, and competitive strategies. The study evaluates liquid formulations, dry formulations, and specialized herbicide solutions used across soybean, cotton, cereals, pastures, and other agricultural applications. Commercial farming accounts for over 60% of demand due to large-scale weed management requirements.

The report covers North America, Europe, Asia-Pacific, South America, and Middle East & Africa with insights into regulatory changes, precision farming adoption, formulation innovation, and crop protection strategies. It analyzes low-volatility technologies, digital spraying systems, and integrated weed management solutions shaping the market between 2026 and 2033. The report supports agricultural investment planning, product development strategies, geographic expansion decisions, and competitive positioning across the global crop protection ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 720.5 Million |

|

Market Revenue in 2033 |

USD 1,114.2 Million |

|

CAGR (2026 - 2033) |

5.6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Bayer AG, BASF SE, Syngenta Group, Corteva Agriscience, Nufarm Limited, Albaugh LLC, UPL Limited, ADAMA Agricultural Solutions Ltd., FMC Corporation, Gharda Chemicals Limited, Jiangsu Yangnong Chemical Co., Ltd., Sharda Cropchem Limited |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |