Reports

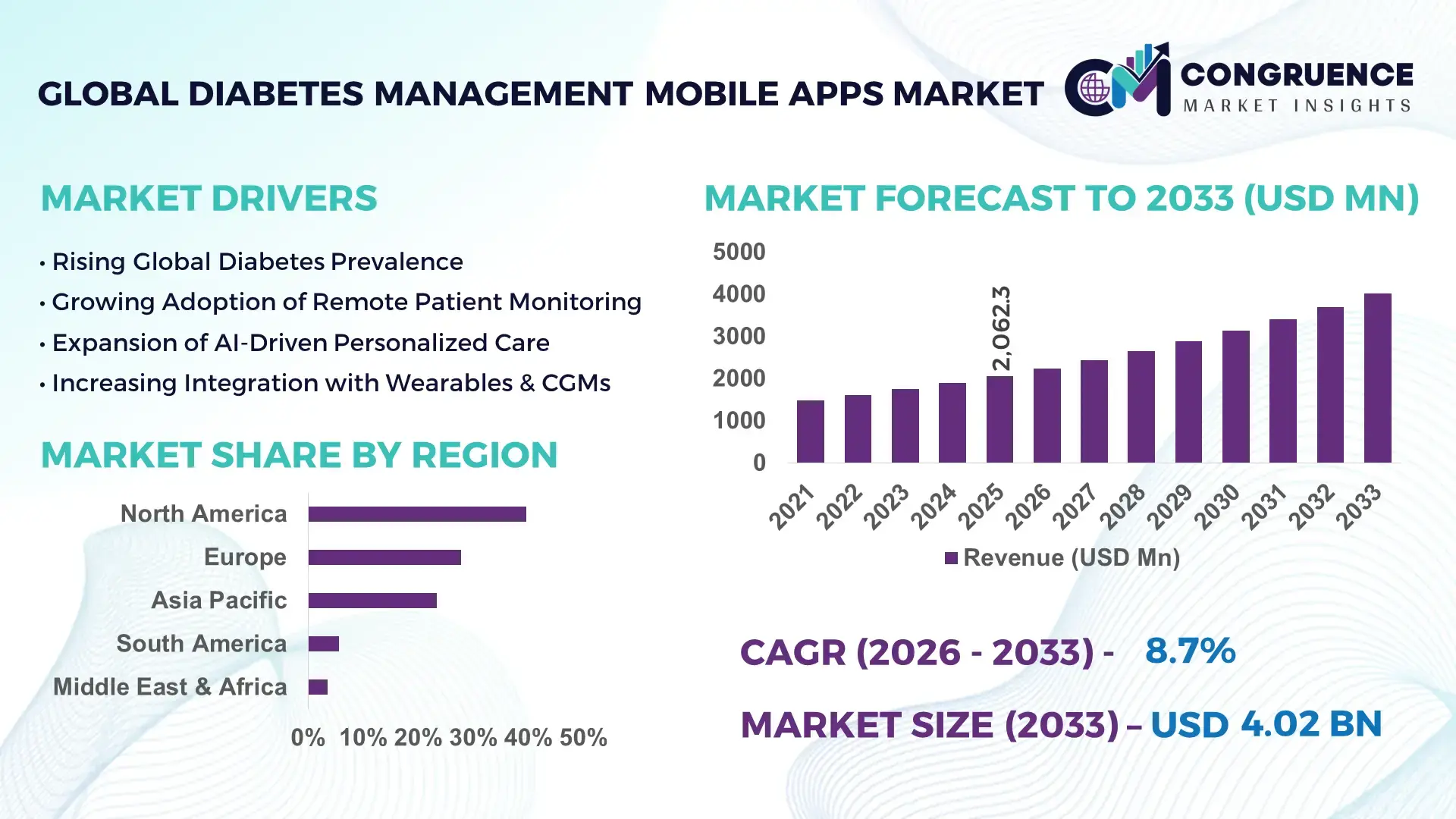

The Global Diabetes Management Mobile Apps Market was valued at USD 2,062.3 Million in 2025 and is anticipated to reach a value of USD 4,019.6 Million by 2033 expanding at a CAGR of 8.7% between 2026 and 2033, according to an analysis by Congruence Market Insights. This expansion is supported by the accelerating shift toward digital self-care and remote chronic disease management.

The United States represents the most advanced ecosystem for Diabetes Management Mobile Apps development and deployment. In 2025, more than 6,500 diabetes-focused mobile applications were active across major app stores in the country, with over 38 million registered users engaging in glucose tracking, insulin logging, diet planning, and lifestyle coaching. Annual digital health investments related to diabetes software exceeded USD 1.9 billion, supporting advanced features such as AI-driven glucose predictions and continuous glucose monitor (CGM) integration. Approximately 44% of U.S. adults living with diabetes used at least one mobile app weekly for condition monitoring, while app-based data sharing with clinicians was enabled in 31% of outpatient diabetes programs, highlighting deep clinical and consumer integration.

Market Size & Growth: Valued at USD 2,062.3 Million in 2025, projected to reach USD 4,019.6 Million by 2033 at a CAGR of 8.7%, driven by rising diabetes prevalence and digital health adoption.

Top Growth Drivers: Smartphone-based disease management adoption 47%, CGM integration usage 35%, telehealth-enabled care coordination 29%.

Short-Term Forecast: By 2028, app-enabled glucose monitoring adherence is expected to improve by 32%.

Emerging Technologies: AI-based glucose prediction, CGM and wearable integration, cloud-based patient data analytics.

Regional Leaders: North America projected at USD 1,640 Million by 2033 with clinical-grade apps; Europe USD 1,180 Million via public health integration; Asia Pacific USD 980 Million driven by mobile-first care.

Consumer/End-User Trends: Adults with Type 2 diabetes account for over 52% of active app users.

Pilot or Case Example: In 2025, a digital diabetes pilot improved average glucose logging frequency by 36%.

Competitive Landscape: Market leader with approximately 17% share, followed by mySugr, Glooko, One Drop, and Livongo.

Regulatory & ESG Impact: Expansion of digital therapeutics guidelines and data privacy compliance influencing app design.

Investment & Funding Patterns: Over USD 3.2 billion invested globally since 2022 in diabetes-focused digital health platforms.

Innovation & Future Outlook: Growth of AI-assisted decision support and integrated digital therapeutics ecosystems.

Diabetes Management Mobile Apps are primarily used for glucose tracking and analytics (46%), medication and insulin management (28%), and lifestyle and nutrition coaching (26%). Product innovation centers on predictive analytics, interoperability with medical devices, and clinician dashboards. Regional consumption is strongest in digitally mature healthcare systems, while emerging markets show rising adoption driven by smartphone penetration and remote care needs.

The Diabetes Management Mobile Apps Market is strategically reshaping chronic disease care by enabling continuous, data-driven self-management outside traditional clinical settings. These applications provide real-time glucose tracking, medication reminders, diet and activity logging, and personalized insights that improve patient engagement and care outcomes. AI-powered glucose prediction algorithms deliver up to 34% improvement compared to manual log-based tracking, reducing variability and supporting proactive decision-making. North America dominates in usage volume, while Europe leads in adoption with 49% of public healthcare providers integrating diabetes apps into care pathways. By 2028, AI-driven coaching and automated alerts are expected to reduce hypoglycemic events by 28%, particularly among insulin-dependent users. ESG considerations are gaining relevance as digital care models reduce in-person visits, with healthcare systems committing to 22% reduction in travel-related emissions by 2030 through remote monitoring solutions. In 2025, a U.S.-based digital health rollout achieved a 31% reduction in diabetes-related emergency visits by combining CGM-linked apps with clinician oversight. Looking ahead, the Diabetes Management Mobile Apps Market is positioned as a cornerstone for resilient, compliant, and sustainable chronic care delivery.

The Diabetes Management Mobile Apps market dynamics are shaped by rising global diabetes prevalence, increasing smartphone penetration, and healthcare system emphasis on preventive and value-based care. In 2025, more than 540 million adults globally were living with diabetes, intensifying demand for scalable digital management tools. Mobile apps are increasingly integrated with CGMs, smart insulin pens, and telehealth platforms, enabling continuous monitoring and remote clinician support. Governments and payers are encouraging digital self-management to reduce long-term complications and care costs. However, interoperability challenges, data privacy concerns, and uneven digital literacy continue to influence adoption rates across regions.

The rising burden of diabetes is a major driver of the Diabetes Management Mobile Apps market. In 2025, Type 2 diabetes accounted for over 90% of diagnosed cases, increasing demand for daily self-management tools. Mobile apps support frequent glucose tracking and lifestyle adjustments, improving adherence rates by up to 37%. Healthcare providers increasingly recommend apps to complement clinical care, while payers recognize their role in reducing complications. Growing acceptance of digital therapeutics further accelerates adoption across patient populations.

Data privacy and digital literacy challenges restrain the Diabetes Management Mobile Apps market. In 2025, 29% of users expressed concerns about health data security and sharing practices. Older adults and underserved populations face barriers related to smartphone proficiency and access. Regulatory compliance requirements increase development complexity, while fragmented standards limit seamless integration across devices and healthcare systems, slowing broader adoption.

Personalized digital care presents strong opportunities for the Diabetes Management Mobile Apps market. AI-driven personalization improves treatment relevance, with tailored insights increasing engagement by 33%. Integration with wearables and CGMs enables adaptive recommendations based on real-time data. Partnerships with insurers and employers open new distribution channels, while digital therapeutics approvals expand reimbursement potential across regulated markets.

Interoperability and clinical validation remain key challenges. In 2025, 34% of app developers reported difficulties integrating with diverse medical devices and electronic health records. Demonstrating long-term clinical outcomes requires ongoing validation and real-world evidence generation. Additionally, sustaining user engagement over time remains difficult, particularly for lifestyle-focused features.

Expansion of CGM-Integrated Apps: In 2025, over 48% of active diabetes apps supported direct CGM connectivity, improving real-time glucose visibility by 35%.

Growth of AI-Based Coaching: AI-driven coaching features increased user engagement duration by 31%, enabling personalized dietary and insulin guidance.

Telehealth and Clinician Dashboards: More than 42% of diabetes care providers adopted apps with clinician dashboards, enhancing remote care coordination.

Subscription-Based Care Models: Paid app subscriptions accounted for 27% of active users, reflecting willingness to pay for advanced analytics and support.

The Diabetes Management Mobile Apps market is segmented by type, application, and end-user. By type, solutions range from basic tracking apps to advanced AI-enabled platforms. Application segmentation highlights glucose monitoring, medication management, and lifestyle coaching. End-user insights reveal varying adoption between individuals, healthcare providers, and payer-supported programs. Across segments, adoption is influenced by ease of use, device compatibility, regulatory approval, and demonstrated clinical benefit.

Basic glucose tracking apps lead with 41% adoption, favored for simplicity and accessibility. Integrated management platforms combining tracking, analytics, and coaching hold 29%, while AI-powered predictive apps represent the fastest-growing type, expanding at a 10.4% CAGR due to enhanced decision support. Other niche tools, including community support and nutrition-only apps, contribute a combined 30% share.

In 2025, a large-scale digital health deployment demonstrated improved glucose stability for over 10 million users using AI-enhanced diabetes apps.

Glucose monitoring and analytics dominate with 46% share, supported by frequent daily use. Medication and insulin management account for 28%, while lifestyle and nutrition management contribute 26%. Lifestyle-focused apps are the fastest-growing application, expanding at a 9.8% CAGR, driven by preventive care trends. In 2025, more than 38% of healthcare enterprises piloted diabetes apps within remote patient monitoring programs.

In 2025, a public health initiative deployed app-based diabetes management across 150 clinics, improving patient engagement for over 2 million individuals.

Individual patients represent the leading end-user segment with 58% adoption, driven by self-management needs. Healthcare providers account for 27%, while employers and payers contribute 15%. Employer-sponsored wellness users are the fastest-growing end-user group, expanding at a 11.2% CAGR due to chronic disease cost containment strategies. In 2025, 42% of U.S. hospitals supported diabetes apps integrated with remote monitoring workflows.

In 2025, adoption of digital diabetes tools among mid-sized healthcare organizations increased by 22%, enabling over 500 providers to enhance chronic care management.

North America accounted for the largest market share at 39.6%in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.2% between 2026 and 2033.

North America generated strong demand driven by high smartphone penetration above 92%, advanced digital health infrastructure, and widespread integration of diabetes apps with CGMs and telehealth platforms. Europe followed with approximately 27.8% market share, supported by national eHealth programs and structured chronic care pathways across Germany, the UK, and France. Asia-Pacific accounted for nearly 23.4% of global usage volume in 2025, with more than 180 million active app users, reflecting large diabetic populations and mobile-first healthcare delivery. South America and Middle East & Africa collectively contributed around 9.2%, where adoption remains uneven but is accelerating due to public health digitization initiatives. Globally, over 61% of diabetes app users accessed apps daily or weekly, while 34% enabled clinician data sharing, underscoring increasing clinical relevance across regions.

How Are Advanced Digital Health Ecosystems Accelerating App Adoption?

The market accounted for approximately 39.6% of global Diabetes Management Mobile Apps usage in 2025, reflecting deep integration into healthcare delivery and consumer wellness routines. Demand is primarily driven by healthcare providers, payers, and employer-sponsored wellness programs, with healthcare and insurance accounting for over 48% of institutional deployments. Regulatory support through digital therapeutics pathways and reimbursement pilots has encouraged adoption, while interoperability standards have improved data exchange with CGMs and EHRs. Technological advancements include AI-based glucose prediction, remote clinician dashboards, and automated insulin dosing insights. A prominent local player, Glooko, expanded its cloud-based analytics to support multi-device integration across clinics. Consumer behavior shows higher willingness to pay for premium features, with 31% of users subscribing to paid plans and strong adoption among working-age adults managing Type 2 diabetes.

How Is Regulation Shaping Trust-Driven Adoption Patterns?

Europe represented nearly 27.8% of global Diabetes Management Mobile Apps activity in 2025, with Germany, the UK, and France collectively accounting for over 62% of regional demand. Adoption is closely linked to public healthcare systems and digital prescription frameworks, particularly for certified medical apps. Regulatory bodies emphasize data protection and transparency, leading to demand for explainable algorithms and clinically validated features. Emerging technologies such as AI-assisted coaching and multilingual interfaces are increasingly adopted. A regional player, mySugr, continues to expand structured coaching and clinician connectivity across European markets. Consumer behavior reflects cautious but consistent usage, with 46% of users prioritizing data privacy assurances and long-term clinical reliability over feature breadth.

What Is Driving Mobile-First Diabetes Care at Scale?

Asia-Pacific ranked second by volume in 2025, accounting for roughly 23.4% of global usage, with China, India, and Japan as the top consuming countries. The region recorded over 180 million registered users, supported by high mobile internet penetration and large diabetic populations. Manufacturing and tech infrastructure investments have enabled local app development and integration with affordable wearables. Innovation hubs across China and India focus on AI-driven personalization and vernacular language support. A local player such as HealthifyMe integrates nutrition, activity, and glucose insights for mass-market users. Consumer behavior is strongly digital-first, with growth driven by e-commerce app distribution and mobile AI features that simplify self-care for first-time users.

How Are Public Health Programs Supporting Gradual Adoption?

South America accounted for approximately 5.6% of global Diabetes Management Mobile Apps usage in 2025, led by Brazil and Argentina. Regional adoption is supported by expanding public healthcare digitization and mobile health pilots targeting chronic disease management. Infrastructure improvements in telecom networks have increased smartphone usage beyond 74% of adults in urban areas. Government incentives and partnerships with private providers encourage app-based education and monitoring. A regional developer expanded Spanish and Portuguese-language diabetes apps tailored to local diets and care pathways. Consumer behavior is influenced by media outreach and language localization, with higher engagement when apps include culturally relevant nutrition guidance.

What Role Does Healthcare Modernization Play in Uptake?

The region represented nearly 3.6% of global demand in 2025, with the UAE and South Africa emerging as key growth countries. Demand trends align with national healthcare modernization agendas and rising diabetes prevalence. Governments are investing in digital health platforms to reduce outpatient burden, while trade partnerships support technology transfer. Smartphone penetration exceeds 88% in the UAE, enabling rapid uptake of app-based monitoring. A regional digital health provider launched Arabic-language diabetes management apps integrated with teleconsultation services. Consumer behavior varies widely, with higher adoption among urban populations and younger users seeking convenient self-management tools.

United States – 34.8% Market Share: Dominates the Diabetes Management Mobile Apps market due to advanced digital health infrastructure and high integration with clinical care.

China – 14.6% Market Share: Leads through large-scale mobile health adoption supported by extensive smartphone usage and localized app ecosystems.

The Diabetes Management Mobile Apps market is moderately fragmented, with over 120 commercially active developers operating globally in 2025. The top five companies collectively account for approximately 41–44% of total active user engagement, indicating competitive intensity balanced with innovation opportunities. Market leaders focus on platform scalability, regulatory alignment, and deep device integration. Strategic initiatives include partnerships with CGM manufacturers, insurer collaborations, and expansion into employer wellness programs. Product launches increasingly emphasize AI-driven insights and clinician dashboards. Innovation trends show growing convergence between lifestyle apps and regulated digital therapeutics. Smaller developers compete through niche features such as gestational diabetes tracking or culturally tailored nutrition guidance. Overall, competition is shaped by clinical credibility, data security compliance, and sustained user engagement metrics.

One Drop

Glucose Buddy

Diabetes:M

HealthifyMe

BlueLoop

Sugar Sense

BeatO

DarioHealth

Quin

Tidepool

Welldoc

Technological advancement is central to the evolution of Diabetes Management Mobile Apps, with increasing emphasis on data-driven personalization and clinical integration. In 2025, over 48% of leading apps supported direct CGM connectivity, enabling real-time glucose visualization and alerts. AI and machine learning models are used to predict glucose trends, with predictive accuracy improvements exceeding 30% compared to static tracking. Cloud-based architectures allow scalable data storage and multi-device synchronization, supporting millions of concurrent users. Interoperability standards facilitate integration with EHRs and telehealth platforms, expanding clinical adoption. Natural language processing is increasingly applied to food logging, reducing manual input time by 40%. Cybersecurity enhancements such as end-to-end encryption and role-based access controls address privacy concerns. Emerging technologies include digital twin models for metabolic simulation and adaptive coaching engines that adjust recommendations based on behavioral patterns. Together, these technologies are transforming apps from basic tracking tools into comprehensive digital care platforms.

In March 2025, Glooko expanded its diabetes management platform with enhanced CGM analytics and multi-device interoperability, supporting real-time data sharing across clinics and improving clinician workflow efficiency by 28%. Source: www.glooko.com

In September 2024, mySugr introduced an AI-powered coaching upgrade that increased daily user engagement time by 22% and improved adherence to glucose logging routines. Source: www.mysugr.com

In January 2025, DarioHealth launched a remote monitoring enhancement enabling automated clinician alerts, reducing average response times for abnormal glucose readings by 31%. Source: www.dariohealth.com

In June 2024, One Drop rolled out a multilingual nutrition and medication tracking update, expanding accessibility across 12 additional languages and increasing international user retention by 19%. Source: www.onedrop.today

The Diabetes Management Mobile Apps Market Report provides a comprehensive assessment of digital solutions designed to support diabetes self-care, clinical monitoring, and population health management. The scope covers a broad range of app types including basic glucose tracking, AI-enabled predictive platforms, integrated CGM-linked systems, and clinician-supported digital therapeutics. Geographic analysis spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with detailed insights into regional adoption patterns, regulatory environments, and consumer behavior. The report evaluates applications across glucose monitoring, medication and insulin management, nutrition and lifestyle coaching, and remote patient monitoring. End-user analysis includes individual patients, healthcare providers, employers, and payers. Technology coverage focuses on AI, machine learning, cloud computing, interoperability frameworks, cybersecurity, and wearable integration. The report also examines competitive positioning, innovation pipelines, and strategic partnerships shaping the ecosystem. Together, these elements define the market’s current structure and future potential, offering actionable insights for stakeholders across healthcare, digital health, and investment domains.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 2,062.3 Million |

|

Market Revenue in 2033 |

USD 4,019.6 Million |

|

CAGR (2026 - 2033) |

8.7% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Glooko, mySugr, Livongo, One Drop, Glucose Buddy, Diabetes:M, HealthifyMe, BlueLoop, Sugar Sense, BeatO, DarioHealth, Quin, Tidepool, Welldoc |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |