Reports

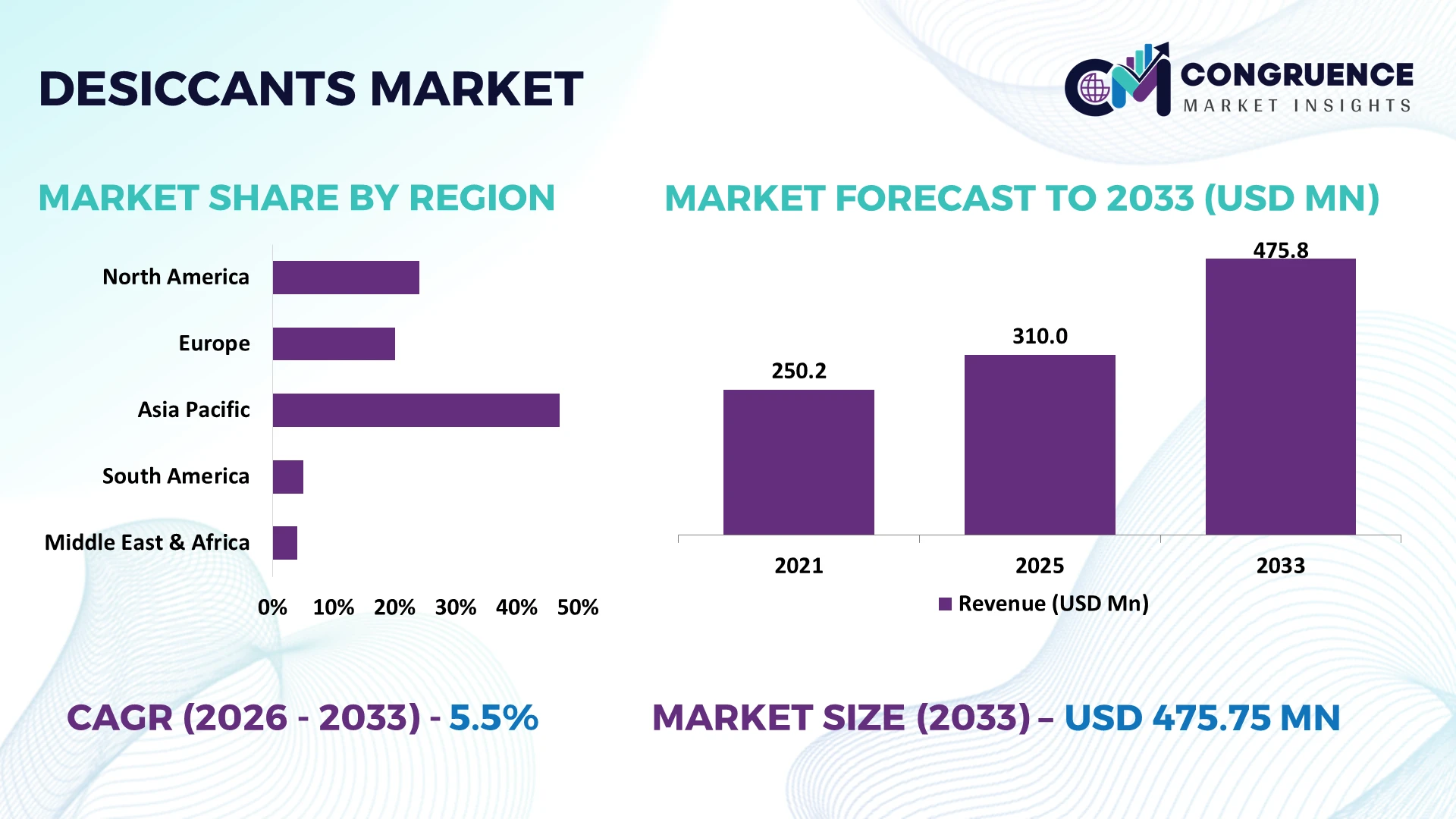

The Global Desiccants Market was valued at USD 310 Million in 2025 and is anticipated to reach a value of USD 475.75 Million by 2033 expanding at a CAGR of 5.5% between 2026 and 2033. Growth is driven by rising moisture-control requirements across pharmaceutical packaging, electronics manufacturing, food preservation, industrial logistics, and high-performance protective packaging solutions.

China remains the dominant country, accounting for approximately 34% of global desiccant production capacity, supported by large-scale electronics, pharmaceutical, and industrial packaging sectors alongside continuous manufacturing investments. The United States follows with nearly 18% market share, emphasizing premium silica gel and molecular sieve applications for healthcare and defense industries. Ongoing supply-chain diversification after Red Sea shipping disruptions has accelerated regional sourcing and automation, while smart packaging adoption has increased by over 20% across export-oriented manufacturers.

Businesses should prioritize regional manufacturing partnerships and advanced desiccant technologies to strengthen supply resilience and capture high-value industrial applications.

Market Size & Growth: USD 310 Million in 2025, reaching USD 475.75 Million by 2033 at 5.5% CAGR, driven by expanding pharmaceutical packaging and advanced electronics manufacturing.

Top Growth Drivers: Pharmaceutical moisture protection (+24%), semiconductor packaging (+19%), and industrial export packaging (+17%) continue accelerating global demand.

Short-Term Forecast: By 2028, automated packaging systems improve moisture-control efficiency by 22% while reducing material waste by 15%.

Emerging Technologies: AI-enabled quality inspection, automated filling systems, and advanced molecular sieve materials improve production consistency and moisture absorption performance.

Regional Leaders: Asia-Pacific exceeds USD 185 Million through electronics expansion, North America approaches USD 96 Million via healthcare adoption, while Europe surpasses USD 82 Million through sustainable packaging initiatives.

Consumer/End-User Trends: Over 63% of pharmaceutical and electronics manufacturers increasingly integrate premium desiccant solutions into protective packaging workflows.

Pilot/Case Example: In 2025, a smart pharmaceutical packaging project reduced moisture-related product losses by 28% using intelligent monitoring and advanced desiccant integration.

Competitive Landscape: The leading supplier holds approximately 14% market share, with competition led by Clariant, Evonik, Sorbead India, W. R. Grace, and Multisorb.

Regulatory & ESG Impact: Sustainable packaging initiatives reduce packaging waste by nearly 18%, encouraging recyclable desiccant materials and lower-carbon manufacturing processes.

Investment & Funding: More than USD 450 Million supports production expansion, automation upgrades, and regional manufacturing diversification amid evolving global supply chains.

Innovation & Future Outlook: High-performance hybrid desiccants, intelligent packaging sensors, and customized adsorption solutions strengthen next-generation industrial moisture management strategies.

Growing demand for desiccants is centered on pharmaceutical packaging, semiconductor manufacturing, lithium battery logistics, and premium food packaging where moisture control directly protects product quality. Advanced molecular sieve formulations and smart indicator technologies are improving operational reliability, while recyclable material adoption has expanded by approximately 16%. Regional manufacturing diversification and stricter packaging standards continue reshaping procurement strategies, setting the stage for deeper strategic market evaluation.

The Desiccants Market has become strategically important as manufacturers strengthen product integrity across pharmaceuticals, semiconductors, electric vehicle batteries, precision electronics, and export packaging. Supply-chain restructuring following global logistics disruptions has accelerated localized sourcing and dual-manufacturing strategies, while stricter packaging quality standards continue raising demand for advanced moisture-control materials. Companies increasingly view desiccants as a value-protection component rather than a low-cost packaging accessory, improving competitiveness through reduced product failures and extended shelf stability.

Advanced molecular sieve desiccants remove moisture up to 35% more efficiently than conventional silica gel in low-humidity industrial environments, reducing package rejection rates and lowering maintenance requirements in high-value production lines. China continues expanding manufacturing capacity for industrial desiccants, whereas Germany focuses on high-performance specialty applications for pharmaceutical and automotive industries through automated production technologies. Over the next two to three years, smart packaging integration is expected to increase by nearly 22%, particularly in regulated export sectors requiring continuous product-quality assurance.

A practical example is pharmaceutical manufacturers integrating humidity-indicating desiccant systems into automated packaging lines, reducing moisture-related quality deviations by approximately 20% while improving compliance efficiency. Companies are responding through production expansion, strategic partnerships with packaging suppliers, and investments in sustainable moisture-control materials. Organizations that combine advanced adsorption technologies with resilient regional supply networks will secure stronger operational performance and long-term competitive differentiation.

Growing production of pharmaceuticals, semiconductor devices, and lithium-ion batteries is increasing demand for advanced desiccant solutions capable of maintaining strict moisture specifications. Pharmaceutical exports from India have expanded steadily, while electronics manufacturing investments in China continue strengthening industrial packaging requirements. Approximately 28% of premium packaging applications now incorporate high-performance desiccants, and automated packaging adoption has increased by nearly 21%, improving production consistency. Stricter quality regulations across healthcare and electronics have accelerated specification upgrades, prompting manufacturers to expand capacity, develop customized adsorption materials, and establish partnerships with packaging companies. This transition enables stronger product protection, reduced rejection rates, and improved operational efficiency across high-value manufacturing environments.

Price fluctuations for activated alumina, specialty silica materials, and energy-intensive processing continue creating cost pressure across the desiccants value chain. Raw material procurement costs have experienced variations exceeding 18% in certain industrial segments, while shipping lead times remain around 15% higher than pre-disruption averages for selected international routes. Manufacturers dependent on imported specialty materials face reduced pricing flexibility and longer production planning cycles. Companies are responding by localizing procurement, negotiating long-term supplier agreements, and qualifying alternative raw material sources to improve supply resilience. The strongest competitive advantage increasingly comes from diversified sourcing strategies rather than simply expanding production capacity.

Demand is expanding beyond conventional packaging toward intelligent moisture-control systems integrating humidity indicators, digital monitoring, and engineered adsorption materials. Smart packaging adoption within regulated pharmaceutical applications is projected to increase by approximately 24% over the next few years, while automated quality monitoring reduces inspection time by nearly 18%. Japan and South Korea continue advancing precision packaging technologies supporting sensitive electronic components and medical products. Companies are increasing R&D investment, collaborating with packaging technology providers, and developing recyclable desiccant solutions aligned with sustainability objectives. The greatest untapped opportunity lies in combining intelligent monitoring with customized moisture-control materials for premium industrial applications.

Deploying next-generation desiccant technologies consistently across multinational manufacturing facilities remains operationally complex because packaging specifications, validation standards, and production infrastructure vary significantly. Around 26% of manufacturers continue operating mixed packaging systems that complicate standardization, while workforce training requirements for automated quality-control processes have increased by approximately 19%. Export-oriented industries must also adapt to evolving packaging compliance requirements without disrupting production schedules. Companies need sustained investment in process digitalization, technical workforce development, standardized validation protocols, and collaborative partnerships with packaging equipment suppliers. Organizations that successfully harmonize technology deployment across multiple production sites will achieve stronger operational consistency and long-term competitive resilience.

Advanced Packaging Automation Automated desiccant dispensing systems are now integrated into over 31% of high-volume pharmaceutical and electronics packaging facilities, reducing packaging cycle times by nearly 18% while improving moisture-control consistency by 23%. Labor shortages and stricter packaging validation are accelerating automation investments, prompting manufacturers to scale smart production lines and strengthen partnerships with packaging equipment providers for higher throughput and quality assurance.

Localized Supply Network Expansion Companies are restructuring procurement by increasing regional raw material sourcing, with localized supplier adoption rising approximately 26% and international dependency declining by nearly 14%. Continued logistics disruptions and geopolitical shipping uncertainty are encouraging production decentralization, enabling shorter lead times, improved inventory planning, and stronger operational resilience through manufacturing expansion across India and Southeast Asia.

Sustainable Desiccant Material Adoption Recyclable and low-emission desiccant products now represent nearly 19% of premium industrial packaging solutions, while process optimization has reduced manufacturing waste by approximately 16%. Sustainability regulations and customer procurement requirements are driving material redesign, leading producers to expand environmentally responsible product portfolios and collaborate with packaging companies to improve circular packaging performance.

High-Performance Industrial Applications Demand for molecular sieves and engineered adsorption materials has increased by around 24% within semiconductor and battery manufacturing, where moisture tolerance remains extremely low. Manufacturers are deploying customized formulations instead of standardized products, improving process reliability while reducing production interruptions by nearly 17%. This specialization is encouraging targeted R&D investment and strategic alliances between desiccant suppliers and advanced manufacturing enterprises.

Silica Gel remains the leading product type, accounting for approximately 42% of the global market because of its cost efficiency, high adsorption performance, and compatibility with pharmaceutical, food, and electronics packaging. Its established manufacturing ecosystem enables large-scale deployment with lower production costs. Activated Alumina continues serving compressed air and industrial gas drying applications, while Clay Desiccants retain importance in cost-sensitive logistics. Calcium Chloride is strengthening its position in shipping containers and long-duration cargo protection through superior moisture absorption in harsh transportation environments.

Molecular Sieves are the fastest-growing type, supported by semiconductor fabrication, lithium battery manufacturing, and specialty pharmaceutical production requiring ultra-low humidity. Industrial adoption has increased by approximately 23%, while customized desiccant solutions have expanded by nearly 18% across precision manufacturing facilities. Companies are investing in specialty production lines, developing application-specific adsorption materials, and partnering with packaging solution providers to strengthen premium product portfolios. Investment priorities continue shifting toward engineered desiccants capable of supporting increasingly demanding industrial processes.

Pharmaceutical Packaging represents the largest application, accounting for approximately 36% of global demand due to strict moisture-control requirements for medicines, vaccines, biologics, and diagnostic products. Increasing packaging validation requirements and product stability standards continue supporting large-scale deployment. Food Packaging remains a mature segment focused on shelf-life optimization, while Air Drying and Industrial Processing maintain consistent demand for compressed air systems, chemical plants, and manufacturing operations where humidity directly affects equipment performance.

Electronics is the fastest-growing application as semiconductor manufacturing, EV battery production, and precision electronic assemblies require advanced moisture protection during production and logistics. Electronics-related desiccant adoption has increased by approximately 25%, while automated packaging integration has expanded by nearly 20%. Companies are scaling manufacturing capacity, integrating automated dispensing systems, and collaborating with electronics manufacturers to develop customized packaging solutions that improve operational reliability and reduce product rejection.

Pharmaceuticals remain the largest end-user group, accounting for approximately 34% of market demand due to stringent quality standards, regulated packaging requirements, and expanding medicine production. Large-scale deployment across manufacturing, storage, and distribution sustains consistent purchasing volumes. Food & Beverage continues investing in moisture-control packaging for shelf-life protection, while Chemicals and Manufacturing rely on desiccants to maintain equipment efficiency, protect raw materials, and improve production reliability.

Electronics is the fastest-growing end-user segment as semiconductor fabrication, battery manufacturing, and precision component production require highly controlled humidity conditions. Procurement from electronics manufacturers has increased by approximately 24%, while customized desiccant adoption has expanded by nearly 19% across advanced production facilities. Companies are strengthening long-term supply agreements, developing industry-specific products, and expanding technical support capabilities to improve customer retention and operational performance in high-value manufacturing sectors.

Asia-Pacific accounted for the largest market share at 44% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2026 and 2033.

Advanced Manufacturing and High-Value Packaging Drive Market Expansion

North America represents approximately 24% of the global Desiccants Market, supported by advanced pharmaceutical production, semiconductor manufacturing, and premium food packaging industries. The region continues strengthening automated packaging infrastructure, where integrated moisture-control systems are becoming standard across regulated production environments. More than 35% of newly commissioned pharmaceutical packaging lines now incorporate automated desiccant dispensing technologies to improve product stability and compliance efficiency. Investment in battery manufacturing and electronics assembly is further expanding demand for molecular sieves and specialty adsorption materials. Companies are increasing production efficiency through digital quality control, regional supply-chain optimization, and partnerships with packaging technology providers to reduce operational risks while improving manufacturing consistency.

United States Market Outlook: The United States remains the regional leader because of its extensive pharmaceutical manufacturing capacity, advanced semiconductor ecosystem, and highly regulated packaging industry. More than 40% of North America's pharmaceutical packaging facilities utilize automated humidity-control systems, encouraging broader adoption of high-performance desiccants. Domestic manufacturers continue investing in specialty adsorption materials, expanding technical partnerships, and modernizing production infrastructure to support healthcare, defense electronics, and battery manufacturing applications requiring strict moisture protection.

Sustainability Standards Reshape Industrial Packaging

Europe accounts for approximately 22% of global market activity, supported by advanced pharmaceutical manufacturing, industrial chemicals, and premium food processing industries. Sustainability regulations continue encouraging recyclable packaging materials and lower-emission production processes, accelerating innovation across desiccant manufacturing. Nearly 28% of industrial packaging suppliers have expanded environmentally focused product portfolios to meet evolving procurement requirements. Advanced automation across packaging facilities and investments in specialty manufacturing improve product consistency while supporting export-oriented industries. Companies are prioritizing recyclable desiccant technologies, production modernization, and collaborative research initiatives to strengthen competitive positioning within regulated industrial markets.

Germany Market Outlook: Germany leads the regional market through its strong pharmaceutical, automotive, and industrial manufacturing sectors. Automated production facilities continue integrating advanced moisture-control technologies, while industrial equipment manufacturers increasingly deploy specialty desiccants in compressed air and process systems. Approximately 32% of premium industrial desiccant demand within Europe originates from German manufacturing activities, reinforcing the country's leadership in precision engineering and sustainable industrial production.

Manufacturing Scale Strengthens Global Leadership

Asia-Pacific contributes approximately 44% of global market demand through its extensive electronics manufacturing, pharmaceutical production, industrial packaging, and export-driven supply chains. China, India, Japan, and South Korea continue expanding manufacturing infrastructure supporting moisture-sensitive products across multiple industries. More than 34% of global desiccant production capacity is concentrated in China, while electronics manufacturing investments continue increasing demand for molecular sieves and silica gel products. Companies are expanding regional manufacturing facilities, improving raw material integration, and strengthening distribution networks to support rising industrial packaging requirements and cross-border trade.

China Market Outlook: China maintains the strongest competitive position through its integrated manufacturing ecosystem, large electronics production base, and expanding pharmaceutical industry. Industrial packaging automation continues advancing, while specialty desiccant production supports semiconductor, battery, and export packaging applications. Approximately 45% of the country's high-value electronics exports utilize advanced moisture-control packaging, encouraging manufacturers to expand production capacity and develop customized adsorption technologies for premium industrial customers.

Industrial Modernization Expands Packaging Demand

South America represents approximately 6% of global demand, supported by growing pharmaceutical manufacturing, food exports, agricultural processing, and industrial chemicals. Rising investments in modern packaging infrastructure are improving moisture-control standards across export industries. Automated packaging deployment has increased by nearly 18% within selected manufacturing sectors, improving operational efficiency and reducing product losses during transportation. Infrastructure limitations and logistics costs remain operational constraints, encouraging companies to localize inventory, strengthen distributor partnerships, and optimize regional production planning for improved supply reliability.

Brazil Market Outlook: Brazil dominates the regional market through its large food processing industry, pharmaceutical manufacturing base, and expanding industrial production. Export-oriented businesses increasingly adopt advanced desiccant packaging to protect agricultural products, processed foods, and healthcare goods. Approximately 30% of regional industrial packaging demand is generated by Brazilian manufacturers, prompting continued investment in automated packaging technologies and localized production capabilities.

Industrial Diversification Supports New Investment

The Middle East & Africa accounts for approximately 4% of global demand, driven by expanding pharmaceutical production, petrochemical processing, industrial logistics, and food packaging investments. Economic diversification programs are encouraging modernization of manufacturing infrastructure and logistics facilities requiring reliable moisture-control solutions. Industrial warehouse capacity has expanded by nearly 20% across major logistics hubs, increasing demand for container desiccants and industrial drying applications. Companies are establishing regional distribution centers, expanding strategic partnerships, and improving localized technical support to strengthen market access and operational responsiveness.

Saudi Arabia Market Outlook: Saudi Arabia leads regional market development through industrial diversification, pharmaceutical investment, and expanding logistics infrastructure. New manufacturing zones continue integrating advanced packaging technologies to improve product protection across domestic and export industries. Industrial development initiatives have increased demand for high-performance moisture-control solutions by approximately 17%, encouraging suppliers to strengthen regional partnerships, technical service capabilities, and localized inventory management for faster industrial deployment.

The Desiccants Market is characterized by competition between global specialty material leaders including Clariant, Evonik Industries, W. R. Grace, and Multisorb, and regional manufacturers such as Sorbead India and Qingdao Makall Group. The top five players collectively control approximately 48% of global market share, while regional suppliers compete aggressively on pricing and localized delivery. Global leaders differentiate through engineered adsorption materials, customized formulations, and integrated technical services, whereas regional producers focus on cost-efficient manufacturing and faster fulfillment. Premium desiccant products deliver nearly 22% higher moisture-control efficiency, while automated production reduces manufacturing costs by approximately 15% and shortens delivery cycles by around 18%. Competition increasingly centers on production expansion, strategic packaging partnerships, specialty product innovation, and vertical integration across raw materials and distribution. The competitive landscape is shifting toward application-specific solutions for pharmaceuticals, semiconductors, and battery manufacturing. High technical validation requirements and long customer qualification cycles remain significant entry barriers. Winning requires scalable manufacturing, advanced adsorption technology, resilient supply networks, rapid customization, and consistent regulatory compliance.

Clariant AG

Evonik Industries AG

W. R. Grace & Co.

Multisorb Technologies

Sorbead India

AGM Container Controls Inc.

Absortech Group

Fuji Silysia Chemical Ltd.

OhE Chemicals Ltd.

Desiccare Inc.

Qingdao Makall Group Inc.

Sinchem Silica Gel Co., Ltd.

Delta Adsorbents

Hengye Inc.

Advanced adsorption technologies are transforming the Desiccants Market through engineered molecular sieves, premium silica gel formulations, and automated dispensing systems. Modern molecular sieve materials improve low-humidity moisture removal by approximately 35% compared with conventional silica gel in critical industrial environments, while automated packaging integration reduces filling errors by nearly 20%. Around 38% of newly installed pharmaceutical and electronics packaging lines now incorporate intelligent desiccant handling systems, improving product consistency and reducing operational downtime. These technologies are becoming essential for manufacturers serving high-value industries with strict humidity specifications.

Emerging innovation focuses on smart desiccants integrated with humidity indicators, IoT-enabled monitoring, and recyclable adsorption materials. Intelligent moisture-monitoring solutions improve packaging inspection efficiency by approximately 24%, while advanced material engineering reduces replacement frequency by nearly 18%. Global technology leaders benefit through premium product differentiation, whereas industrial manufacturers gain improved product protection, lower quality losses, and enhanced process reliability. Companies are increasingly combining automation, material science, and digital monitoring within integrated packaging ecosystems.

Between 2026 and 2028, hybrid adsorption materials, AI-assisted process optimization, and sustainable desiccant technologies will accelerate industrial deployment. Adoption of intelligent moisture-control platforms is expected to exceed 45% across regulated pharmaceutical and semiconductor packaging operations. Organizations investing early in digital quality assurance, specialty adsorption materials, and automated manufacturing will strengthen competitive positioning through faster production, superior product protection, and greater supply-chain resilience.

April 2026 Clariant expanded its continuous-strip Desi Pak™, Sorb-It™, and Tri-Sorb™ desiccant packet production for high-speed automated packaging lines across the Americas, supporting reel-fed automation that reduces labor costs and inventory complexity while improving packaging throughput. Source: https://www.clariant.com

November 2025 Clariant completed an CHF 80 million expansion at its Daya Bay, China facility, strengthening pharmaceutical excipient and specialty chemicals manufacturing capabilities. The investment enhanced regional production capacity and reinforced supply reliability for moisture-sensitive packaging applications. Source: https://www.pressreleasefinder.com

February 2026 Clariant published its 2025 Integrated Report, confirming continued alignment with GRI and European Sustainability Reporting Standards while expanding sustainability-focused operations. The report supports customers seeking compliant, lower-impact packaging materials across regulated industries.

June 2026 Clariant strengthened its global adsorbents and desiccants portfolio by highlighting expanded sustainable bentonite-based desiccant production supported by a globally integrated mining and logistics network. The initiative improves supply security and lowers environmental impact through responsible mine recultivation practices. Source: https://www.clariant.cn

This report provides comprehensive analysis across Silica Gel, Activated Alumina, Molecular Sieves, Clay Desiccants, and Calcium Chloride, covering major applications including Food Packaging, Pharmaceutical Packaging, Electronics, Air Drying, and Industrial Processing. It evaluates demand across Food & Beverage, Pharmaceuticals, Electronics, Chemicals, and Manufacturing while assessing operational trends across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. More than 45% of market activity is concentrated within moisture-sensitive industrial applications, reflecting increasing deployment of advanced adsorption technologies.

The report examines competitive positioning, technology adoption, manufacturing strategies, supply-chain evolution, and regional investment priorities between 2026 and 2033. It analyzes deployment patterns, innovation pipelines, sustainability initiatives, and enterprise expansion strategies across leading manufacturers. Strategic insights support investment planning, capacity expansion, partnership evaluation, procurement optimization, and competitive benchmarking while identifying emerging opportunities in smart packaging, automated dispensing systems, specialty adsorption materials, and precision industrial moisture-control applications.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 310 Million |

Market Revenue in 2033 | USD 475.75 Million |

CAGR (2026 - 2033) | 5.5% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Clariant AG, Evonik Industries AG, W. R. Grace & Co., Multisorb Technologies, Sorbead India, AGM Container Controls Inc., Absortech Group, Fuji Silysia Chemical Ltd., OhE Chemicals Ltd., Desiccare Inc., Qingdao Makall Group Inc., Sinchem Silica Gel Co., Ltd., Delta Adsorbents, Hengye Inc. |

Customization & Pricing | Available on Request (10% Customization is Free) |