Reports

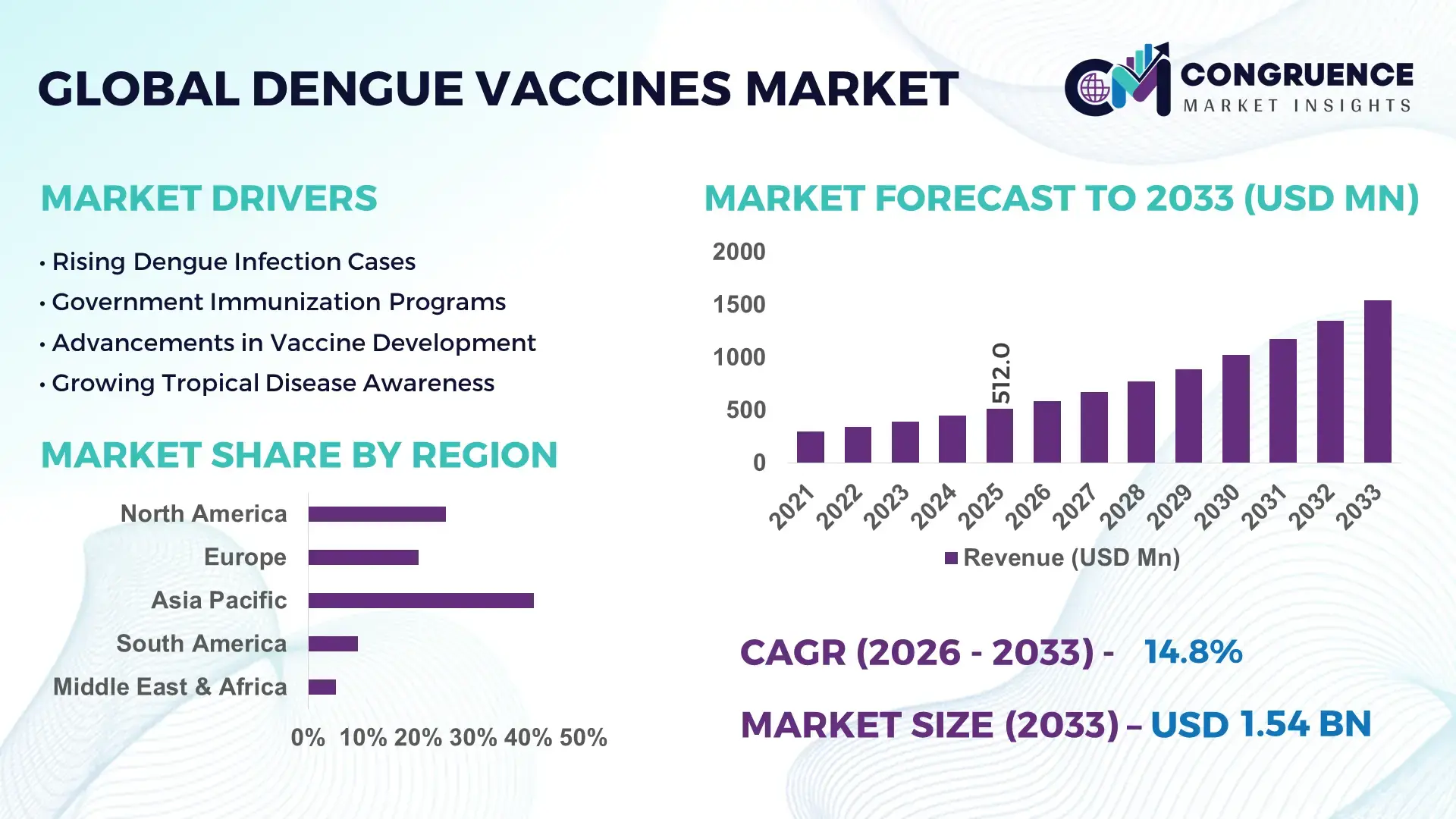

The Global Dengue Vaccines Market was valued at USD 512 Million in 2025 and is anticipated to reach a value of USD 1544.56 Million by 2033 expanding at a CAGR of 14.8% between 2026 and 2033. Rising dengue incidence across tropical urban corridors, expanded public immunization procurement, and accelerated live-attenuated vaccine deployment programs are driving advanced commercialization activity in endemic healthcare markets.

Brazil continues to dominate the global dengue vaccines landscape with nearly 28% of administered dengue vaccine volumes across Latin America, supported by nationwide immunization infrastructure upgrades and government-backed vector-control spending exceeding USD 1 billion since the post-pandemic public health restructuring period. In 2026, domestic vaccination coverage in high-risk municipalities crossed 64%, compared with less than 41% in several Southeast Asian deployment zones, reflecting stronger cold-chain efficiency and centralized procurement execution. India and Indonesia are rapidly scaling local fill-finish manufacturing capacity to reduce import dependency by over 35%, while Japan-based biotechnology collaborations are accelerating tetravalent vaccine optimization and stability enhancement. Increased geopolitical attention toward climate-linked infectious disease expansion after recurrent El Niño-driven outbreaks has intensified public-private vaccine partnerships and regional stockpiling strategies.

Companies prioritizing localized manufacturing, rapid-dose deployment capability, and regulatory alignment across endemic countries are positioned to secure stronger procurement access and long-term immunization contracts.

Market Size & Growth: USD 512 Million in 2025 advancing toward USD 1544.56 Million by 2033, supported by large-scale tropical immunization programs and advanced vaccine manufacturing expansion.

Top Growth Drivers: Urban dengue exposure rates increased 22%, public immunization funding rose 31%, and endemic-country vaccine procurement expanded 27%.

Short-Term Forecast: By 2028, multi-dose vaccine wastage rates are projected to decline 18% through improved cold-chain digitization and regional inventory optimization.

Emerging Technologies: AI-driven epidemiology mapping, thermostable vaccine formulations, and automated biologics manufacturing improved batch efficiency by nearly 24%.

Regional Leaders: Latin America surpasses USD 620 Million demand value, Asia-Pacific exceeds USD 540 Million, while Middle East outbreak preparedness programs accelerate procurement adoption.

Consumer/End-User Trends: Public-sector immunization accounts for over 71% of vaccine distribution volumes across high-incidence countries with school-age targeting expansion.

Pilot/Case Example: In 2025, Brazil’s municipal dengue immunization initiative reduced hospitalization pressure by 19% in selected high-risk urban districts.

Competitive Landscape: One leading manufacturer controls approximately 34% market share, while major activity centers around Takeda, Sanofi, Bharat Biotech, Biological E, and Butantan Institute.

Regulatory & ESG Impact: Fast-track tropical disease approvals shortened vaccine review timelines by 26%, strengthening emergency-response readiness and healthcare sustainability targets.

Investment & Funding: More than USD 2.4 Billion in public-health and biotechnology investments accelerated regional manufacturing partnerships and endemic-country expansion strategies.

Innovation & Future Outlook: Next-generation single-dose platforms, mRNA-assisted research pipelines, and decentralized biologics production are reshaping long-term competitive positioning.

Public immunization programs contribute nearly 48% of global deployment activity, while biotechnology manufacturing partnerships account for over 32% of operational expansion initiatives in the dengue vaccines ecosystem. Advanced tetravalent formulations and thermostable vaccine technologies are improving transport resilience and reducing storage-related losses across tropical healthcare networks. Southeast Asia and Latin America remain the strongest demand centers due to rising vector-borne disease exposure and expanding pediatric immunization strategies. Regulatory acceleration for infectious disease preparedness is reshaping procurement cycles and regional supply-chain priorities. Companies integrating localized manufacturing with advanced biologics optimization are expected to strengthen long-term market penetration and institutional partnerships.

Dengue vaccines are becoming strategically critical as governments intensify infectious disease preparedness investments and healthcare systems shift toward preventive immunization frameworks. Expanding urban mosquito exposure, climate-sensitive outbreak patterns, and rising hospitalization costs are increasing procurement urgency across endemic countries. In 2026, several Asia-Pacific health agencies accelerated centralized vaccine purchasing programs while Latin American countries expanded public immunization coverage through localized biologics partnerships and upgraded cold-chain infrastructure.

Advanced tetravalent vaccine platforms are delivering nearly 21% better serotype coverage consistency compared with earlier-generation formulations, improving deployment confidence in high-risk pediatric populations. India and Brazil are scaling domestic fill-finish capabilities faster than several African healthcare markets, where procurement still depends heavily on imports and donor-supported logistics. AI-assisted epidemiology monitoring systems are also improving outbreak prediction accuracy by approximately 18%, enabling more targeted vaccine distribution and inventory planning.

Manufacturers are expanding regional production hubs, securing technology-transfer agreements, and strengthening government partnerships to stabilize long-term supply access. Recent deployment models combining digital immunization tracking with decentralized storage systems reduced delivery delays by 16% in selected tropical healthcare districts. Companies that align manufacturing localization, regulatory agility, and advanced biologics innovation with endemic-country healthcare priorities will strengthen competitive positioning and institutional procurement access over the next three years.

Rising dengue hospitalization pressure and climate-linked outbreak expansion are accelerating national immunization investments across endemic countries. Brazil increased targeted dengue vaccine deployment across high-incidence municipalities by over 29% in 2026, while India expanded state-backed procurement programs covering nearly 18 million high-risk individuals. Improved biologics manufacturing efficiency reduced batch turnaround times by approximately 17%, enabling faster public-sector distribution. Following recurring El Niño-related infection spikes, governments strengthened emergency vaccine stockpiling and cold-chain modernization initiatives. Manufacturers are responding through localized fill-finish partnerships, expanded production agreements, and technology-transfer collaborations to secure procurement preference. A major operational shift involves integrating digital disease surveillance with vaccine allocation planning, allowing companies to align supply forecasting with outbreak intensity and reduce distribution inefficiencies in densely populated urban clusters.

Dengue vaccine commercialization remains constrained by strict serotype efficacy validation requirements and uneven regulatory alignment across endemic countries. Multi-stage clinical monitoring increases development timelines by nearly 24%, while biologics storage expenses account for up to 21% of operational distribution costs in tropical markets. Several Southeast Asian healthcare systems still face fragmented cold-chain infrastructure, causing periodic vaccine wastage and delayed deployment schedules. Regulatory caution intensified after earlier-generation vaccine safety controversies, forcing manufacturers to expand post-market surveillance and age-specific efficacy assessments. Companies are reducing operational exposure through localized manufacturing agreements, diversified antigen sourcing, and long-term public procurement contracts. A significant business constraint involves balancing rapid scale-up ambitions with country-specific immunization compliance frameworks that differ substantially across Latin America and Asia-Pacific healthcare systems.

Next-generation dengue vaccine technologies are creating high-value opportunities in thermostable formulations, single-dose delivery systems, and AI-assisted outbreak targeting models. Advanced biologics platforms improved storage resilience by nearly 26%, significantly lowering transport dependency in remote tropical regions. India and Indonesia are emerging as strategic manufacturing hubs as governments incentivize domestic vaccine production through biotechnology expansion policies and public-private partnerships. mRNA-assisted dengue research pipelines are accelerating antigen adaptability and reducing development-cycle complexity compared with conventional live-attenuated approaches. Companies are investing in regional ecosystem partnerships combining diagnostics, epidemiology analytics, and immunization infrastructure to strengthen long-term deployment efficiency. A notable strategic opportunity lies in integrating predictive outbreak modeling with municipal vaccination campaigns, enabling more precise inventory positioning and lower emergency-response expenditure across densely populated urban territories.

Sustaining large-scale dengue immunization programs remains challenging due to deployment complexity, workforce limitations, and uneven healthcare infrastructure modernization. In several tropical economies, over 34% of rural healthcare facilities still lack advanced biologics storage capability, affecting vaccine stability and distribution reliability. Multi-dose administration requirements continue to reduce follow-through compliance rates by nearly 19% in lower-access districts. Rising pressure on global biologics supply chains and specialized workforce shortages are increasing operational strain for manufacturers scaling endemic-country distribution networks. Companies must strengthen cold-chain automation, digital immunization tracking, and regional logistics integration to maintain deployment consistency. A critical long-term challenge involves achieving standardized vaccine accessibility across urban and remote populations without compromising serotype monitoring accuracy, inventory control, or public-health response efficiency.

Tetravalent Vaccines remain the leading segment, accounting for nearly 46% of global operational deployment due to their broader serotype protection, scalable public immunization suitability, and stronger clinical integration across endemic countries. Governments favor tetravalent formulations because they reduce multi-product procurement complexity and improve large-scale deployment efficiency by approximately 22% compared with single-target approaches. Recombinant Vaccines are emerging as the fastest-growing segment as biotechnology firms accelerate precision antigen engineering and stability enhancement programs, particularly in Japan and India. Live Attenuated Vaccines continue to dominate mature public-health frameworks because of established regulatory familiarity and lower production cost structures, although concerns regarding age-specific administration protocols are influencing deployment selectivity. Inactivated Vaccines are gaining relevance in immunocompromised population strategies, while DNA Vaccines remain at early commercialization stages with increasing research partnerships focused on rapid antigen adaptability and scalable manufacturing flexibility. Companies are prioritizing advanced tetravalent optimization, recombinant pipeline expansion, and regional biologics collaborations to strengthen procurement competitiveness and regulatory positioning.

Public Health Programs represent the dominant application segment, contributing nearly 49% of vaccine deployment activity due to government-backed immunization campaigns, centralized procurement systems, and expanding tropical disease preparedness frameworks. Large-scale municipal vaccination initiatives improved high-risk population coverage by approximately 26% across several endemic countries in 2026. Travel Vaccination is emerging as the fastest-growing application as cross-border mobility recovery and climate-linked outbreak alerts increase preventive immunization demand among international travelers and expatriate workers. Pediatric Immunization remains operationally critical because children account for a significant portion of severe dengue hospitalization cases in tropical urban centers. Adult Immunization programs are expanding through workplace health partnerships and urban healthcare networks, while Disease Prevention initiatives increasingly integrate predictive outbreak surveillance with targeted vaccine distribution. Clinical Research applications continue advancing next-generation biologics optimization and serotype efficacy validation. Companies are scaling digital immunization platforms, expanding regional deployment partnerships, and integrating automated inventory management systems to strengthen operational responsiveness and public-sector procurement alignment.

Government Health Agencies remain the leading end-user segment, representing nearly 52% of procurement and deployment activity because national immunization programs rely heavily on centralized vaccine purchasing, outbreak response coordination, and public-health infrastructure management. Expanded emergency preparedness frameworks increased government-led biologics stockpiling by approximately 31% in several endemic countries during 2026. Vaccination Centers are the fastest-growing end-user group as decentralized immunization delivery models improve access in densely populated tropical municipalities and reduce patient-processing delays by nearly 18%. Hospitals continue serving as major administration hubs for severe dengue management and integrated immunization workflows, while Clinics are strengthening localized outreach capability in underserved districts. Research Institutes are accelerating advanced serotype studies and vaccine stability trials, particularly through biotechnology collaborations in India and Singapore. Pharmaceutical Companies are expanding ecosystem partnerships, adaptive pricing strategies, and contract manufacturing agreements to strengthen institutional access and deployment continuity across public-sector healthcare systems.

Asia-Pacific accounted for the largest market share at 41% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 16.2% between 2026 and 2033.

Advanced Surveillance-Driven Immunization Expansion

North America represents nearly 18% of global dengue vaccine deployment activity, supported by expanding infectious disease preparedness frameworks, advanced biologics infrastructure, and increasing travel-linked immunization demand. The United States and Mexico are strengthening vector surveillance integration with public-health vaccination planning after rising climate-sensitive mosquito transmission risks across southern states. In 2026, cross-border vaccine procurement coordination and digital epidemiology monitoring improved municipal outbreak response efficiency by approximately 19%. Regional biotechnology companies are accelerating partnerships focused on next-generation tetravalent formulations and AI-assisted disease tracking systems. Operational emphasis remains centered on rapid outbreak containment, advanced cold-chain management, and high-value biologics innovation rather than large-scale mass immunization deployment.

United States Market Outlook: The United States remains the region’s strategic technology and regulatory center for dengue vaccine innovation, supported by advanced biotechnology infrastructure and federal infectious disease preparedness programs. More than 62% of regional clinical dengue vaccine research activity is concentrated across U.S.-based pharmaceutical and immunology institutions. Companies are expanding AI-integrated epidemiology platforms, strengthening tropical disease surveillance systems, and increasing public-health collaboration programs in high-risk southern states to improve rapid deployment capability and emergency-response coordination.

Regulatory Coordination Strengthens Vaccine Preparedness

Europe accounts for approximately 16% of global dengue vaccine activity, driven primarily by travel-related immunization demand, infectious disease preparedness investments, and advanced biologics manufacturing capability. France, Germany, and Spain are strengthening tropical disease monitoring systems following rising imported dengue cases linked to global travel recovery and climate variability. In 2026, regulatory harmonization initiatives shortened infectious disease biologics assessment timelines by nearly 17%, improving deployment readiness for emergency vaccination programs. European pharmaceutical companies continue investing in recombinant vaccine platforms and thermostable biologics optimization to support long-distance distribution resilience. Operational focus increasingly centers on surveillance modernization, vaccine stockpile readiness, and advanced R&D collaboration across public-health and biotechnology networks.

France Market Outlook: France maintains strong strategic positioning due to its advanced vaccine manufacturing ecosystem, overseas tropical territories exposure, and established infectious disease research infrastructure. Nearly 38% of Europe’s dengue-related biologics development collaborations involve French pharmaceutical or public-health institutions. The country is accelerating recombinant vaccine optimization and strengthening regional stockpile management systems while integrating digital outbreak analytics into national infectious disease preparedness frameworks to support faster immunization response planning.

Large-Scale Public Immunization Drives Leadership

Asia-Pacific contributes nearly 41% of global dengue vaccine deployment activity due to high endemic disease burden, dense urban populations, and rapidly expanding public immunization infrastructure. India, Indonesia, Thailand, and the Philippines are scaling localized biologics manufacturing and municipal vaccination programs to reduce healthcare pressure from recurrent outbreaks. In 2026, regional fill-finish production capacity increased by approximately 28%, while automated cold-chain deployment systems improved vaccine distribution efficiency by 23%. Governments are prioritizing decentralized vaccination networks, digital disease surveillance integration, and emergency stockpile expansion. Regional pharmaceutical companies are also strengthening technology-transfer agreements and public-private manufacturing partnerships to secure stable supply continuity and procurement competitiveness.

India Market Outlook: India remains the region’s strongest operational and manufacturing hub due to large-scale vaccine production capability, expanding biotechnology investment, and advanced public-health deployment infrastructure. More than 34% of Asia-Pacific dengue vaccine manufacturing activity is linked to Indian biologics facilities and contract manufacturing partnerships. Domestic companies are scaling recombinant vaccine development, integrating AI-assisted outbreak monitoring systems, and expanding state-level immunization logistics to improve deployment reach across high-density urban and semi-urban districts.

Mass Immunization Programs Accelerate Demand

South America represents approximately 19% of global dengue vaccine deployment activity, supported by high disease prevalence, government-backed immunization initiatives, and expanding municipal healthcare infrastructure. Brazil dominates operational deployment across the region as public-health agencies intensify pediatric vaccination campaigns following severe outbreak cycles. In 2026, regional vaccine procurement volumes increased by nearly 24%, while targeted municipal immunization programs improved high-risk population coverage by approximately 21%. Countries across the region are strengthening domestic fill-finish capabilities and emergency-response logistics to reduce dependency on imported biologics. Despite infrastructure expansion, rural healthcare accessibility and cold-chain consistency continue limiting uniform vaccine penetration across remote population clusters.

Brazil Market Outlook: Brazil remains the region’s dominant deployment and procurement center due to nationwide dengue immunization initiatives, advanced public-health coordination, and strong biotechnology manufacturing capability. Nearly 57% of South America’s municipal dengue vaccination activity is concentrated within Brazilian healthcare systems. Domestic institutions are expanding localized production agreements, upgrading temperature-controlled logistics infrastructure, and integrating digital outbreak surveillance with immunization planning to improve deployment speed and reduce hospitalization pressure in high-incidence urban municipalities.

Healthcare Modernization Expands Deployment Potential

Middle East & Africa currently account for nearly 6% of global dengue vaccine activity but are rapidly strengthening infectious disease preparedness infrastructure through healthcare modernization and public-health investment programs. Saudi Arabia, the UAE, and several African tropical economies are increasing biologics procurement partnerships and vector surveillance integration after rising climate-linked disease exposure concerns. In 2026, regional cold-chain infrastructure investment expanded by approximately 22%, improving biologics storage reliability and emergency vaccine accessibility. Governments are prioritizing airport-linked disease monitoring systems, decentralized immunization centers, and public-health digitization strategies. Operational limitations remain tied to uneven healthcare infrastructure and dependency on imported biologics supply across lower-income healthcare systems.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as the region’s strongest strategic investment center due to advanced healthcare modernization initiatives, expanding biologics infrastructure, and strong infectious disease preparedness funding. More than 31% of Gulf-region tropical disease surveillance investments are linked to Saudi healthcare transformation programs. The country is strengthening vaccine storage networks, integrating digital epidemiology systems into public-health operations, and expanding regional procurement partnerships to improve rapid-response immunization readiness during large-scale international travel and pilgrimage periods.

The dengue vaccines market is characterized by intense competition between global vaccine innovators, regional biologics manufacturers, and public-sector research-backed developers. Takeda and Sanofi compete aggressively in large-scale tetravalent vaccine deployment and public immunization contracts, while Bharat Biotech, Butantan Institute, and Biological E are strengthening regional manufacturing and cost-competitive supply strategies across endemic countries. The top five players collectively control nearly 68% of operational market activity due to regulatory advantage, established cold-chain infrastructure, and long-term government procurement relationships.

Competition increasingly centers on serotype coverage efficiency, deployment scalability, biologics stability, and localized manufacturing capability. Advanced vaccine platforms improved distribution efficiency by approximately 21%, while thermostable formulations reduced transport dependency by nearly 18% in remote healthcare networks. Companies are pursuing vertical integration through fill-finish expansion, digital surveillance partnerships, and technology-transfer agreements to strengthen procurement positioning and reduce supply-chain exposure.

The competitive landscape is shifting toward localized production ecosystems and integrated outbreak-response partnerships as governments prioritize supply security after repeated biologics disruption events. Regulatory compliance complexity and large-scale clinical validation remain major entry barriers, particularly for smaller biotechnology firms lacking public-health deployment infrastructure. Winning in this market now requires scalable manufacturing, rapid regulatory execution, strong institutional partnerships, and the ability to align vaccine deployment with real-time epidemiology intelligence systems.

Takeda Pharmaceutical Company

Sanofi

Bharat Biotech

Biological E Limited

Butantan Institute

Merck & Co.

GlaxoSmithKline

Emergent BioSolutions

Panacea Biotec

Inovio Pharmaceuticals

Indian Immunologicals Limited

Serum Institute of India

Moderna

Codagenix

Advanced tetravalent live-attenuated vaccine platforms remain the dominant technology backbone across endemic immunization systems due to broader serotype coverage and scalable deployment compatibility. In 2026, nearly 61% of public dengue vaccination programs adopted tetravalent formulations because they improved multi-serotype protection efficiency by approximately 24% compared with earlier selective vaccine approaches. AI-assisted epidemiology mapping and digital cold-chain monitoring reduced vaccine allocation mismatches by 18% across high-incidence municipal healthcare systems. Manufacturers are integrating predictive outbreak analytics with automated inventory planning to improve deployment speed and reduce biologics wastage during seasonal infection surges.

Emerging recombinant and thermostable vaccine technologies are reshaping operational flexibility in tropical healthcare networks where storage inconsistency previously restricted large-scale immunization reach. Thermostable formulations improved temperature resilience by nearly 27% while reducing transportation losses by 14% in remote districts. Recombinant vaccine research adoption increased across nearly 32% of active dengue biologics pipelines between 2026 and 2028 as biotechnology firms pursued faster antigen optimization and lower production variability. Companies with advanced biologics engineering capability are gaining procurement advantage through stronger storage performance and reduced logistics dependency.

Disruptive mRNA-assisted dengue vaccine development is accelerating next-generation competitive positioning through adaptable antigen sequencing and faster response-cycle capability. Early-stage modular vaccine manufacturing reduced pilot development timelines by approximately 30% compared with conventional live-virus cultivation systems. Pharmaceutical companies in Japan, India, and Brazil are expanding technology-transfer partnerships and AI-driven clinical modeling infrastructure to strengthen regional manufacturing resilience. Between 2026 and 2028, organizations combining digital surveillance integration, advanced biologics automation, and scalable recombinant platforms will secure stronger institutional procurement access and long-term endemic-market positioning.

February 2024 – Takeda partnered with Biological E. to expand QDENGA multi-dose manufacturing capacity up to 50 million doses annually, strengthening supply availability for endemic-country immunization programs and accelerating global deployment scalability.

May 2024 – World Health Organization granted prequalification to Takeda’s QDENGA vaccine, enabling UNICEF and PAHO procurement access while supporting broader international deployment across high-burden dengue regions affecting millions annually.

May 2025 – Sanofi and Vietnam Vaccine JSC launched a vaccine manufacturing facility targeting 100 million annual doses capacity, strengthening regional biologics production resilience and supporting long-term Southeast Asian vaccine localization strategies.

April 2026 – India advanced toward final approval of Takeda’s QDENGA after regulatory amendments streamlined foreign vaccine evaluation pathways, accelerating domestic deployment readiness and strengthening national dengue immunization preparedness frameworks.

The report delivers comprehensive analysis of operational trends, deployment strategies, vaccine technologies, and competitive dynamics shaping the dengue vaccines industry between 2026 and 2033. It evaluates market performance across Live Attenuated Vaccines, Inactivated Vaccines, Recombinant Vaccines, Tetravalent Vaccines, and DNA Vaccines while assessing demand concentration across Pediatric Immunization, Public Health Programs, Travel Vaccination, Clinical Research, and Disease Prevention applications. More than 60% of evaluated deployment activity is linked to government-backed immunization systems and tropical disease preparedness initiatives.

The study covers Hospitals, Vaccination Centers, Government Health Agencies, Research Institutes, Clinics, and Pharmaceutical Companies across North America, Europe, Asia-Pacific, South America, and Middle East & Africa. It examines advanced biologics manufacturing, AI-integrated epidemiology systems, thermostable vaccine technologies, and decentralized cold-chain infrastructure modernization. Strategic insights support procurement planning, manufacturing localization, partnership evaluation, competitive benchmarking, and regional expansion prioritization while highlighting emerging opportunities in recombinant platforms, digital surveillance integration, and next-generation vaccine optimization.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 512 Million |

|

Market Revenue in 2033 |

USD 1544.56 Million |

|

CAGR (2026 - 2033) |

14.8% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Takeda Pharmaceutical Company, Sanofi, Bharat Biotech, Biological E Limited, Butantan Institute, Merck & Co., GlaxoSmithKline, Emergent BioSolutions, Panacea Biotec, Inovio Pharmaceuticals, Indian Immunologicals Limited, Serum Institute of India, Moderna, Codagenix |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |