Reports

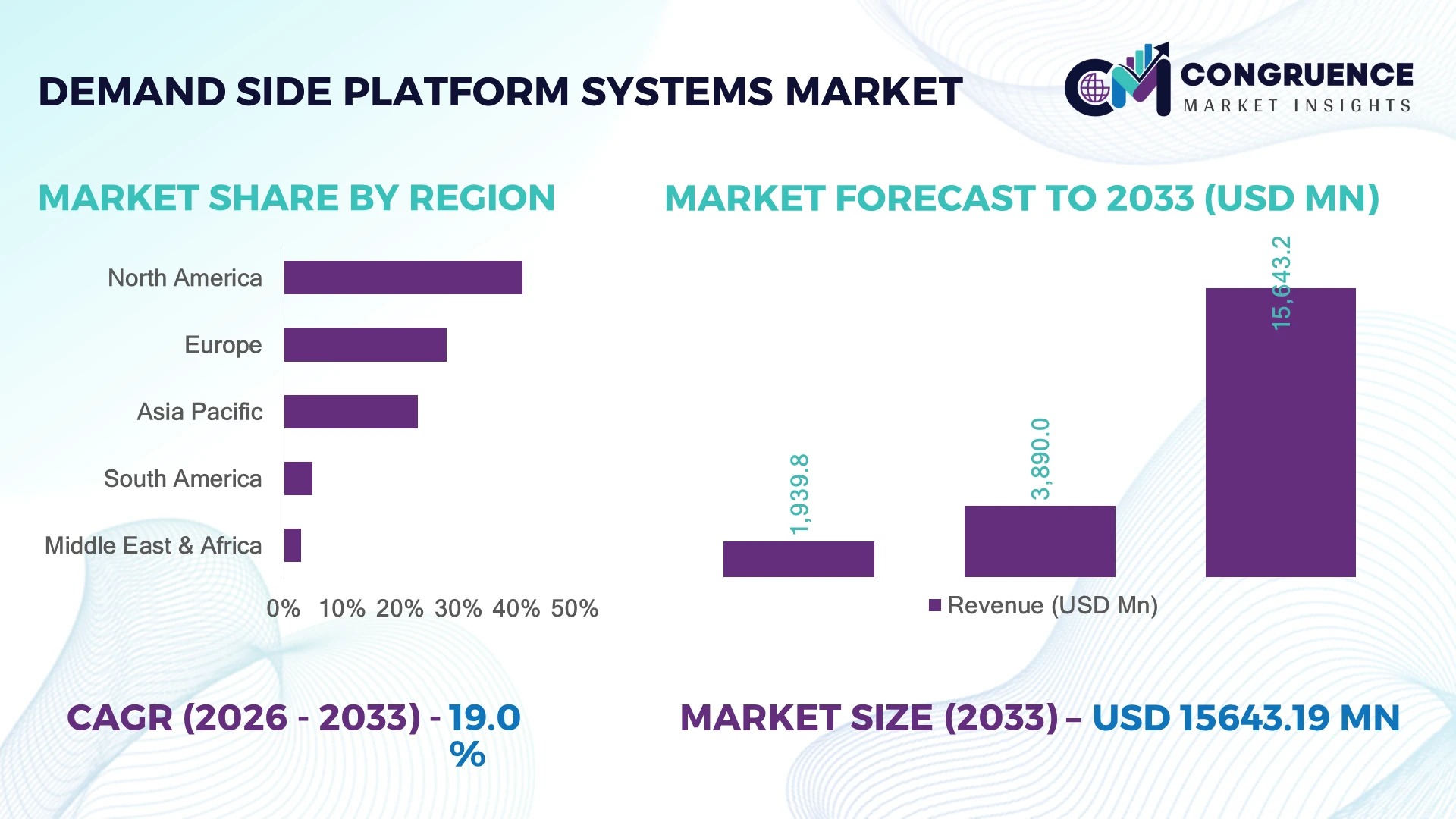

The Global Demand-Side Platform Systems Market was valued at USD 3,890.0 Million in 2025 and is anticipated to reach a value of USD 15,643.2 Million by 2033 expanding at a CAGR of 19% between 2026 and 2033. AI-driven programmatic advertising optimization and real-time bidding efficiency across omnichannel digital inventory are accelerating DSP adoption in high-intent ad ecosystems.

The United States dominates with nearly 42% share, supported by over USD 1.2 billion in annual adtech infrastructure spending and CTV penetration above 78%, while China follows at ~18% driven by mobile-first ecosystems; India records 23% faster DSP adoption growth than the US due to rapid digital commerce expansion. The competitive gap highlights North America’s scale advantage versus Asia’s acceleration in mobile advertising.

Strategic implication: advertisers are shifting budget control toward automated, data-rich bidding ecosystems to maximize ROI precision.

Market Size & Growth: USD 3,890M (2025) → USD 15,643.2M (2033) with 19% CAGR driven by AI-based programmatic bidding expansion

Top Growth Drivers: Connected TV 34%, mobile advertising 29%, retail media integration 22% accelerating DSP penetration

Short-Term Forecast: By 2027, ad spend efficiency improves 28% and campaign latency reduces 31% through real-time bidding automation

Emerging Technologies: AI predictive bidding, cookieless identity graphs, and automated audience segmentation reshape targeting accuracy

Regional Leaders: North America USD 1.55B (CTV-led adoption), Asia-Pacific USD 1.21B (mobile-first scaling), Europe USD 0.89B (privacy-driven DSP upgrades)

Consumer/End-User Trends: 64% of advertisers prioritize automated multi-channel DSP campaigns over manual ad buying workflows

Pilot/Case Example: 2026 retail media pilot reduced acquisition cost by 27% using AI-optimized DSP bidding in omnichannel campaigns

Competitive Landscape: The Trade Desk holds ~12% share, with Google, Amazon Ads, Adobe, and MediaMath driving platform consolidation

Regulatory & ESG Impact: Privacy regulations improved data compliance efficiency by 33% while reducing third-party cookie dependency across markets

Investment & Funding: Over USD 5.8B in DSP-adjacent adtech funding driven by cloud partnerships and AI infrastructure scaling

Innovation & Future Outlook: Shift toward cookieless DSP ecosystems and unified ID frameworks improving targeting accuracy by 40%

The Demand-Side Platform Systems Market is witnessing strong demand across retail media networks, connected TV advertising, and mobile programmatic ecosystems, where over 72% of global ad impressions are now processed through automated bidding systems. Key innovation trends include AI-based audience segmentation, cookieless identity resolution, and cross-device attribution modeling, enabling up to 35% improvement in targeting efficiency. A notable trend is the 21% rise in privacy-compliant DSP integrations across regulated digital markets, driven by evolving data governance frameworks in North America and Europe. This shift is reshaping how advertisers optimize budget allocation and performance tracking, creating a more transparent and measurable digital advertising ecosystem that strengthens operational control and campaign precision.

The Demand-Side Platform Systems Market has become strategically critical as digital advertising shifts toward fully automated, data-driven decision ecosystems that directly influence brand competitiveness and customer acquisition efficiency. Increasing fragmentation of media channels and stricter privacy regulations are forcing enterprises to centralize ad buying through DSPs, enhancing control over cross-platform campaign execution. Over 60% of global advertisers are reallocating budgets toward programmatic channels, reflecting a structural shift in digital marketing investments.

From a technology standpoint, AI-enabled DSPs deliver up to 38% higher bidding efficiency compared to traditional rule-based ad buying systems, significantly reducing wasted impressions. North America leads in high-scale enterprise adoption, while Asia-Pacific demonstrates faster deployment cycles due to mobile-first ecosystems and lower infrastructure transition barriers, with adoption growing nearly 1.4x faster in retail-heavy markets.

In practice, companies are increasingly forming partnerships with cloud providers and retail media networks to unify audience data and improve attribution accuracy. For example, integrated DSP deployments in omnichannel retail campaigns have reduced customer acquisition costs by over 25% within 12–18 months. Over the next 2–3 years, competitive advantage will depend on privacy-compliant data integration, AI orchestration, and ecosystem interoperability across global advertising infrastructures.

AI-powered programmatic advertising adoption is accelerating DSP system penetration as enterprises prioritize automated bidding efficiency and cross-channel attribution. Nearly 68% of digital advertisers in the United States now rely on AI-optimized DSP workflows, while mobile ad automation in China has increased by 54%, driven by retail media and super-app ecosystems. Connected TV adoption in the UK has risen 37%, further expanding high-value inventory demand. This structural shift from manual ad buying to real-time bidding ecosystems is improving targeting accuracy and reducing media waste. In response, companies such as Google Ads and The Trade Desk are expanding AI bidding models, investing in unified data layers, and forming partnerships with retail media networks to strengthen cross-platform optimization capabilities and secure higher advertiser retention.

DSP scalability is constrained by fragmented data ecosystems and tightening privacy regulations that restrict cross-platform tracking efficiency. Around 61% of advertisers in Europe report reduced targeting precision following GDPR enforcement, while third-party cookie deprecation has impacted nearly 49% of programmatic campaign measurement accuracy in the United States. Additionally, interoperability gaps between legacy ad exchanges and modern DSP stacks slow integration cycles by up to 28%. These limitations increase operational costs and reduce campaign ROI predictability. To mitigate risks, companies are shifting toward first-party data architectures, localized data centers in Germany and Japan, and privacy-safe identity solutions through strategic partnerships with cloud providers such as Amazon Web Services and Adobe Experience Cloud ecosystems.

The transition to cookieless advertising frameworks presents significant growth opportunities as 73% of global marketers accelerate investment in first-party identity graphs and contextual targeting models. Retail media networks in India have expanded DSP-based ad inventory usage by 42%, while Southeast Asia shows 33% growth in commerce-led programmatic campaigns. This shift is enabling advertisers to unlock untapped high-intent consumer segments across digital commerce platforms. Emerging innovations such as federated learning-based targeting and AI-driven contextual mapping are improving audience match rates by up to 36%. Companies are responding by expanding R&D in identity resolution technologies and forming ecosystem partnerships with e-commerce platforms like Amazon Ads and Walmart Connect to secure long-term data-driven advertising advantages.

DSP systems face execution challenges due to increasing integration complexity across fragmented advertising ecosystems, where 57% of enterprises report delays in unified campaign attribution across mobile, CTV, and desktop channels. Cross-device tracking inconsistencies reduce performance measurement accuracy by nearly 31%, particularly in markets like the United States and South Korea with high multi-screen usage. Cybersecurity risks in real-time bidding environments have also increased by 26%, exposing vulnerabilities in programmatic data exchanges. These issues hinder consistent scalability and enterprise-wide deployment efficiency. To address these challenges, companies are investing in secure API frameworks, advanced attribution modeling powered by AI, and strategic cloud-native infrastructure upgrades to ensure seamless interoperability and strengthen long-term operational resilience.

AI-Driven Bid Optimization Scaling AI-based bidding systems now handle nearly 71% of programmatic transactions in the United States, while Japan shows a 39% rise in automated budget allocation tools across DSP stacks. Real-time latency has dropped by 33% due to cloud-native DSP deployment, improving ad placement accuracy and reducing wasted impressions. This shift is reshaping operational efficiency as enterprises replace rule-based bidding with predictive algorithms. Companies are responding by embedding machine-learning modules into DSP pipelines and expanding cloud partnerships with AWS and Google Cloud to strengthen computational scalability and reduce decision-cycle delays.

Cookieless Identity Transition Acceleration Third-party cookie restrictions have pushed 64% of advertisers in Germany toward first-party identity frameworks, while South Korea reports a 46% increase in contextual targeting adoption. Campaign measurement accuracy has improved by 28% in privacy-safe environments using unified ID solutions. This structural transition is improving compliance but increasing integration complexity across platforms. Firms are investing in identity resolution startups and forming cross-industry data alliances with telecom and retail platforms to maintain targeting precision without violating regulatory constraints.

Retail Media DSP Convergence Growth Retail media DSP integration has expanded by 52% in the United States and 44% in India, driven by e-commerce platforms embedding advertising marketplaces into transaction ecosystems. Conversion rates in retail-linked DSP campaigns are 31% higher than traditional display ads due to intent-driven targeting. This convergence is reshaping inventory distribution and shifting ad budgets toward commerce ecosystems. Companies are responding by partnering with Amazon Ads, Walmart Connect, and regional e-commerce leaders to secure closed-loop attribution capabilities and high-intent audience access.

Cross-Channel Attribution Modernization Push Multi-device attribution adoption has increased by 57% in the UK, while Australia reports a 35% improvement in campaign ROI tracking through unified analytics dashboards. However, inconsistent mobile-to-CTV tracking still causes up to 29% measurement variance across campaigns. This has created pressure for standardized data frameworks and interoperability protocols. Companies are responding by deploying AI-based attribution engines and integrating DSPs with CDPs to unify customer journey tracking across fragmented digital touchpoints.

Cloud-based DSP platforms dominate the market due to superior scalability, real-time processing capability, and seamless integration with AI-driven bidding systems. Nearly 62% of global advertisers prefer cloud-native DSP infrastructure for its ability to reduce campaign latency by 34% and improve cross-channel targeting efficiency by 29%. On-premise DSP systems remain relevant in regulated industries but are declining in preference due to higher maintenance costs and slower upgrade cycles. Hybrid DSP architectures are gaining traction, particularly in financial services and telecom sectors, growing adoption by 41% as enterprises seek data sovereignty with performance flexibility. Fastest growth is observed in cloud-native DSP stacks driven by mobile-first advertising ecosystems in India and Southeast Asia, where adoption is expanding 1.3x faster than legacy systems. Companies are investing in API-first DSP architectures and expanding cloud partnerships to strengthen real-time bidding efficiency and reduce infrastructure bottlenecks.

Programmatic advertising remains the leading application due to its high-volume automated transaction capability, accounting for nearly 74% of DSP-driven digital ad executions in the United States. Mobile advertising is the fastest-growing application, expanding rapidly in China and India with a 48% increase in in-app ad spending driven by e-commerce and super-app ecosystems. Connected TV advertising is also rising, with a 36% growth in ad impressions across the UK and Germany, reflecting shifting consumer viewing patterns. Display and video advertising continue to serve mature use cases but are gradually being integrated into unified omnichannel DSP workflows. Businesses are scaling cross-platform campaign orchestration and adopting AI-based audience segmentation tools to improve engagement efficiency by up to 30%.

Advertisers represent the dominant end-user group due to high-volume media buying requirements and dependence on automated bidding systems, contributing to over 66% of DSP system utilization globally. Media agencies follow closely, leveraging DSP platforms to manage multi-client campaigns, with adoption increasing by 42% in North America due to centralized campaign optimization needs. Retailers are the fastest-growing end-user segment, especially in India and Southeast Asia, where DSP adoption is expanding by 45% driven by retail media network integration and first-party data utilization. Publishers are gradually integrating DSP capabilities to optimize yield management, though adoption remains moderate due to infrastructure constraints. Companies are responding by offering customized DSP interfaces, flexible pricing models, and API-based integrations to cater to enterprise advertisers, agencies, and retail ecosystems differently.

North America accounted for the largest market share at 41% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 19% between 2026 and 2033.

North America leads DSP deployment due to advanced programmatic infrastructure, strong cloud penetration, and high CTV monetization. The region contributes nearly 41% share, driven by the United States where over 72% of digital ad transactions flow through automated DSP systems. Real-time bidding latency has improved by 34% following large-scale cloud migration across adtech stacks. Strategic partnerships between enterprise advertisers and platforms like Amazon Ads and The Trade Desk are expanding retail media integration, with over 38% of brands in the U.S. now using unified DSP ecosystems for cross-channel optimization. Increasing investment in privacy-safe identity frameworks is further strengthening enterprise adoption.

United States Market Outlook: The U.S. remains the core innovation hub, supported by advanced AI-driven ad infrastructure and large-scale retail media expansion. Over 78% of advertisers in the country now use automated bidding systems integrated with cloud-native DSP platforms. Continuous investment in CTV advertising and first-party data ecosystems has improved campaign targeting efficiency by nearly 29%, reinforcing its leadership in high-performance programmatic advertising environments.

Europe’s DSP market is shaped by strict data governance frameworks and accelerated adoption of privacy-compliant advertising technologies. The region holds approximately 28% share, with strong adoption in Germany, the UK, and France. GDPR-driven constraints have pushed 63% of advertisers toward first-party data strategies and contextual targeting models. DSP integration with identity resolution platforms has improved campaign attribution accuracy by 27%. Partnerships between adtech firms and telecom providers in Germany and the Netherlands are strengthening secure data ecosystems. Investment in cookieless infrastructure is accelerating as enterprises focus on compliance-led innovation and cross-border data interoperability.

Germany Market Outlook: Germany leads Europe’s DSP modernization with strong enterprise adoption across automotive, retail, and manufacturing sectors. Nearly 69% of digital advertisers in the country have transitioned to privacy-first DSP frameworks. Deployment of secure data clean rooms has improved targeting efficiency by 24%, while enterprise partnerships with cloud providers are enabling scalable programmatic infrastructure across regulated industries.

Asia-Pacific is the fastest-expanding DSP region, driven by mobile-first ecosystems, e-commerce dominance, and rapid digital infrastructure scaling. The region accounts for around 23% share, with China, India, and Japan leading adoption. Mobile programmatic advertising volumes have increased by 48% across major APAC markets, while retail media DSP integration in India has expanded by 44%. Cloud-based DSP deployment has reduced campaign latency by 31%, enabling faster ad delivery across high-traffic platforms. Strategic investments in super-app ecosystems and digital payment integration are further accelerating real-time ad monetization.

China Market Outlook: China remains the largest APAC DSP hub, powered by integrated super-app ecosystems and high-frequency mobile engagement. Over 81% of digital ads are processed through programmatic systems, with retail-linked DSP campaigns growing by 36%. Strong AI infrastructure investment and domestic adtech platforms continue to enhance targeting precision and scale across digital commerce ecosystems.

South America’s DSP market is in a developing phase, driven by rising digital advertising penetration and increasing mobile-first consumer behavior. The region holds around 5% share, with Brazil and Argentina leading adoption. Programmatic ad spending has increased by 39% in Brazil, supported by growing e-commerce and fintech ecosystems. However, limited cloud infrastructure and fragmented data ecosystems slow large-scale DSP deployment. Strategic partnerships between global adtech firms and local telecom providers are improving accessibility and reducing integration costs by nearly 21%. Market expansion is increasingly tied to digital payment ecosystem growth and retail digitization.

Brazil Market Outlook: Brazil dominates South America’s DSP landscape with strong digital commerce growth and expanding mobile advertising adoption. Nearly 67% of digital ad inventory in the country is now programmatic, supported by rising retail media integration. Investments in cloud infrastructure and AI-based targeting tools are improving campaign efficiency by 26%, positioning Brazil as the primary growth hub in the region.

The Middle East & Africa DSP market is expanding steadily due to digital transformation initiatives, smart city investments, and rising mobile advertising adoption. The region holds approximately 3% share, with the UAE, Saudi Arabia, and South Africa leading adoption. Programmatic advertising usage has increased by 42% across GCC countries, driven by government-backed digital economy programs. Cloud-based DSP integration has improved campaign delivery efficiency by 28%, while partnerships between telecom operators and global adtech platforms are strengthening data connectivity. However, infrastructure disparity across African markets remains a limiting factor for uniform adoption.

United Arab Emirates Market Outlook: The UAE leads regional DSP development through advanced digital infrastructure and strong government-backed AI initiatives. Over 74% of digital advertising in the country is now programmatic, supported by smart city and retail media expansion. Investment in cloud-based advertising ecosystems has improved targeting precision by 25%, reinforcing the UAE’s position as the primary innovation hub in the MEA digital advertising landscape.

The DSP market is dominated by Amazon DSP, Google Display & Video 360, The Trade Desk, Adobe Advertising Cloud, and Yahoo DSP, competing against regional adtech specialists and retail media networks. Competition is primarily global walled-garden ecosystems (Amazon, Google) versus independent DSPs (The Trade Desk, Adobe), with Amazon aggressively capturing CTV and retail inventory. The top 5 players collectively control ~62% combined share, driven by ecosystem integration advantages. Competition is shifting on technology (42% influence), inventory access (33%), and pricing efficiency (21%), with Amazon and Google leveraging proprietary data advantages. In practice, Amazon is expanding DSP reach via CTV partnerships, while The Trade Desk strengthens open-internet positioning through publisher alliances. Market consolidation is accelerating as platforms integrate supply and demand layers vertically. Entry barriers remain high due to data ownership constraints, identity infrastructure, and AI bidding scale requirements. Winning requires control over first-party data, cross-channel inventory access, and real-time AI optimization superiority.

Amazon Ads (DSP)

Adobe Advertising Cloud

Yahoo DSP

MediaMath

StackAdapt

Xandr (Microsoft Advertising)

Magnite

Criteo

PubMatic

Adform

Viant Technology

Nexxen

AI-driven bidding engines now define DSP performance, with predictive models improving bid efficiency by nearly 38% and reducing wasted impressions by 27%. Adoption is accelerating, with over 70% of enterprise advertisers deploying machine-learning-based audience segmentation integrated into DSP workflows. Legacy rule-based bidding systems are being replaced due to slower response times and lower conversion accuracy, creating a 31% performance gap in campaign optimization outcomes. Companies like Google and Amazon benefit most due to access to proprietary behavioral datasets and cloud-scale compute infrastructure.

Cookieless identity resolution and federated learning are emerging as critical technologies, improving targeting accuracy by 26% while maintaining regulatory compliance in Europe and Japan. Meanwhile, cross-device attribution systems integrated with CDPs enhance ROI measurement precision by 33%, enabling unified campaign tracking across CTV, mobile, and desktop environments. These integrations are now deployed in over 55% of large-scale DSP environments, signaling rapid modernization of advertising stacks.

Looking toward 2026–2028, DSP platforms will shift toward autonomous campaign orchestration, where AI agents dynamically allocate budgets in real time. This transition is expected to reduce manual campaign management costs by 40% while increasing conversion efficiency. Early adopters will gain a significant competitive advantage as real-time autonomous bidding becomes the industry standard.

October 2025 | Amazon Ads expanded DSP integration through a strategic partnership with Microsoft Advertising, enabling migration of Microsoft Invest customers across global markets and improving cross-platform streaming inventory access by ~30% efficiency gain, strengthening CTV dominance and advertiser consolidation strategy. Source: www.advertising.amazon.com

June 2025 | Roku & Amazon Ads formed a joint CTV inventory partnership covering nearly 80% of U.S. streaming device reach, enabling unified audience targeting across The Roku Channel and Prime Video, significantly improving cross-device attribution accuracy and advertiser reach scalability.

September 2025 | Netflix & Amazon Ads integrated Netflix ad-supported inventory into Amazon DSP across multiple global markets, expanding premium streaming ad access and improving advertiser conversion visibility across high-intent audiences while intensifying DSP ecosystem consolidation.

November 2025 | Amazon Ads enhanced DSP capabilities with AI-driven multi-touch attribution models combining ML and experimental data, improving conversion credit allocation precision by ~25%+, strengthening full-funnel measurement and reducing performance attribution errors for advertisers.

The Demand-Side Platform Systems Market report covers detailed segmentation across platform types, applications, end-users, and major geographic regions, including North America, Europe, Asia-Pacific, South America, and Middle East & Africa. It evaluates cloud-based, hybrid, and on-premise DSP architectures along with programmatic advertising, retail media, and connected TV applications.

The study provides insights into adoption patterns across advertisers, agencies, retailers, and publishers, highlighting over 60% enterprise reliance on automated bidding systems. It also examines AI-driven optimization, cookieless identity frameworks, and cross-channel attribution technologies shaping next-generation DSP ecosystems. The report supports strategic investment planning, competitive benchmarking, and expansion strategies for stakeholders targeting high-growth digital advertising infrastructures between 2026 and 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 3,890.0 Million |

| Market Revenue (2033) | USD 15,643.2 Million |

| CAGR (2026–2033) | 19% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | The Trade Desk; Google Marketing Platform (DV360); Amazon Ads (DSP); Adobe Advertising Cloud; Yahoo DSP; MediaMath; StackAdapt; Xandr (Microsoft Advertising); Magnite; Criteo; PubMatic; Adform; Viant Technology; Nexxen |

| Customization & Pricing | Available on Request (10% Customization Free) |