Reports

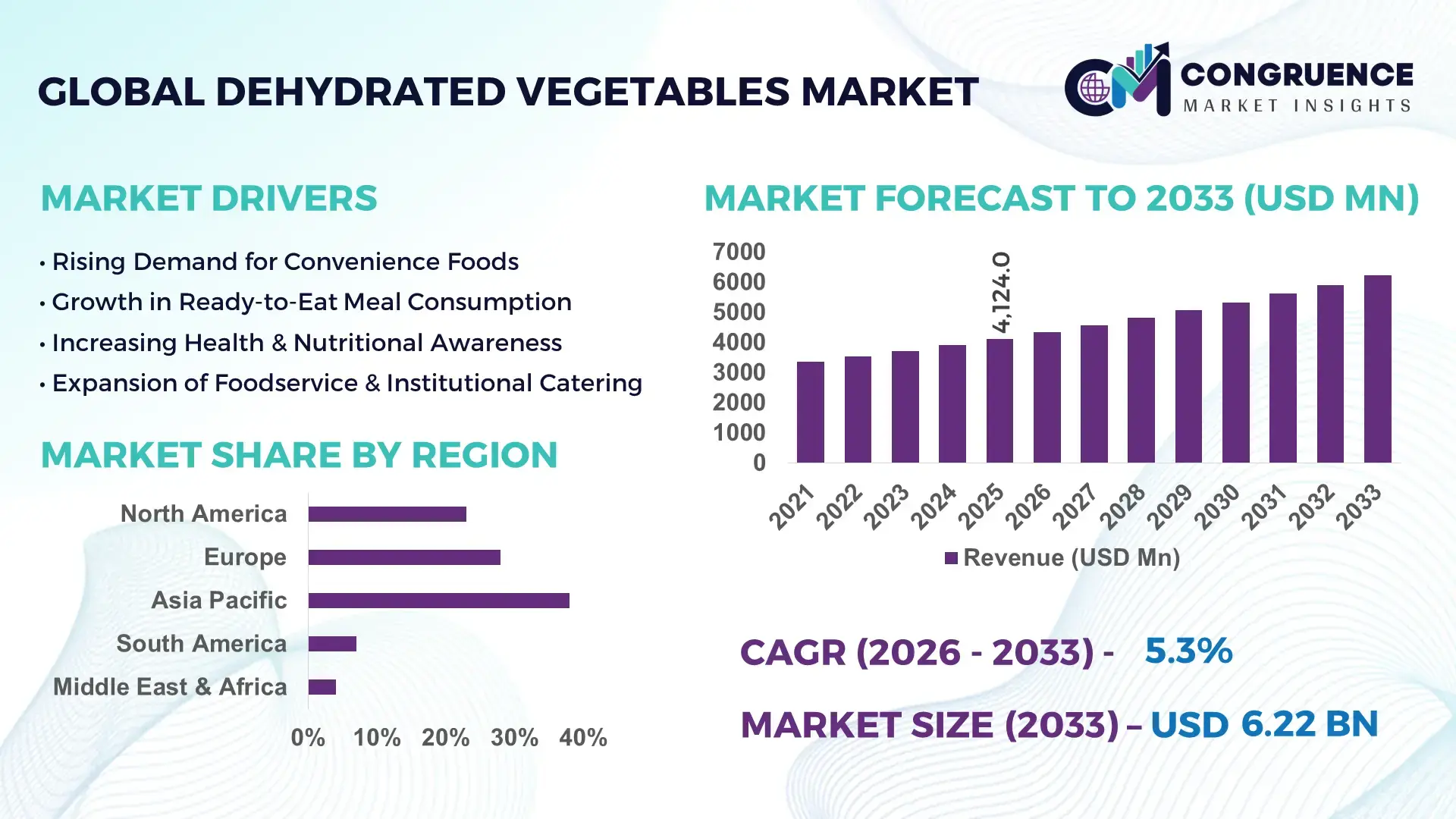

The Global Dehydrated Vegetables Market was valued at USD 4,124.0 Million in 2025 and is anticipated to reach a value of USD 6,219.5 Million by 2033 expanding at a CAGR of 5.27% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is driven by increasing demand for convenience foods and long-shelf-life ingredients across multiple industries.

India leads the Dehydrated Vegetables Market, with a production capacity exceeding 1.2 million tons annually. The country has seen USD 150 million in investments for modern dehydration facilities over the last three years, supporting large-scale supply chains. India’s industrial sector has adopted advanced freeze-drying and vacuum dehydration technologies, increasing product uniformity and reducing moisture content by up to 95%. Key applications include ready-to-eat meals, soups, and snack production, with over 60% of manufacturers integrating automated sorting and packaging systems to improve efficiency.

Market Size & Growth: Market value at USD 4,124.0 Million in 2025; projected USD 6,219.5 Million by 2033; growth fueled by increasing convenience food demand.

Top Growth Drivers: Rapid adoption of automated drying systems 42%, expanding ready-to-eat food segment 38%, increasing cold chain efficiency 33%.

Short-Term Forecast: By 2028, dehydration cost per unit expected to reduce by 12% due to technological advancements.

Emerging Technologies: Freeze-drying automation, vacuum-assisted dehydration, AI-enabled quality control.

Regional Leaders: Asia Pacific USD 2,350 Million by 2033 (high production scale), Europe USD 1,520 Million by 2033 (premium quality adoption), North America USD 980 Million by 2033 (industrial application efficiency).

Consumer/End-User Trends: Increased use in ready-to-eat meals, soups, and packaged snacks; higher acceptance among urban households (65% adoption).

Pilot or Case Example: In 2025, a facility in India achieved 18% reduction in production downtime using AI-assisted drying control.

Competitive Landscape: Market leader McCain Foods ~22% share; other competitors include ConAgra Foods, Olam Group, Bonduelle, and GKN Foods.

Regulatory & ESG Impact: Implementation of food safety standards, government incentives for low-energy dehydration, ESG initiatives targeting 20% water reduction by 2027.

Investment & Funding Patterns: USD 150 Million in recent plant expansions; rising venture funding in automated dehydration technologies.

Innovation & Future Outlook: Expansion of AI-driven process monitoring, integration of energy-efficient dehydration systems, and development of functional vegetable powders.

The Dehydrated Vegetables Market is experiencing rapid innovation in freeze-drying, vacuum dehydration, and automation systems. Key sectors such as ready-to-eat foods, soups, snacks, and food service are integrating these innovations to reduce waste, enhance nutritional retention, and optimize packaging. Regulatory frameworks and environmental initiatives are accelerating the adoption of low-energy, water-efficient technologies, while emerging consumer trends favor convenience and longer shelf life, shaping a resilient and technologically advanced market outlook.

The Dehydrated Vegetables Market holds strategic importance due to its ability to support sustainable food supply chains, reduce post-harvest losses, and cater to the growing demand for convenience foods. Freeze-drying automation delivers 15% higher nutrient retention compared to traditional sun-drying methods. Asia Pacific dominates in production volume, while North America leads in adoption with 65% of enterprises utilizing high-efficiency dehydration technologies. By 2028, AI-enabled drying control systems are expected to improve throughput by 20% and reduce energy consumption by 10%. Firms are committing to ESG improvements, including a 20% reduction in water usage and energy-efficient process integration by 2027. In 2025, a major Indian facility achieved 18% reduction in production downtime through automated quality control initiatives. Looking forward, the Dehydrated Vegetables Market is positioned as a resilient, compliance-driven, and sustainable pillar supporting global food industries and innovation-driven growth strategies.

The Dehydrated Vegetables Market is shaped by evolving consumer preferences, technological advancements, and operational efficiencies. Increased demand for ready-to-eat meals and long-shelf-life products is driving adoption across multiple sectors. Investment in advanced dehydration methods, such as freeze-drying and vacuum-assisted systems, enables higher nutrient retention, lower moisture content, and consistent product quality. Additionally, regulatory emphasis on food safety, energy efficiency, and ESG compliance is influencing operational decisions. The market is further supported by urbanization trends, rising disposable incomes, and growing industrial-scale food processing infrastructure, creating a dynamic environment for manufacturers, technology providers, and end-users.

Consumer preference for convenient, shelf-stable products is directly driving Dehydrated Vegetables Market expansion. Ready-to-eat meals, soups, and snacks now account for 60% of industrial vegetable use. Manufacturers are adopting high-efficiency freeze-drying and vacuum-assisted drying, reducing moisture content by up to 95% and extending product shelf life by 18–24 months. Urban households show 65% adoption of packaged dehydrated vegetables, and industrial kitchens report 12% faster prep times, demonstrating measurable efficiency gains throughout the supply chain.

Seasonal and climate-related fluctuations in raw vegetable availability pose significant challenges to the Dehydrated Vegetables Market. India, despite high production capacity, faces 10–15% annual yield variability due to monsoon dependency. Price volatility can impact production costs, and inconsistent quality may lead to 5–8% higher rejection rates in processing facilities. Small-scale producers often struggle to maintain consistent dehydration efficiency, limiting overall operational scalability and industry-standard uniformity.

Rising interest in functional and fortified foods presents significant opportunities. Manufacturers are integrating high-nutrient dehydrated vegetables into soups, baby foods, and meal kits, contributing to up to 25% enhanced nutritional value. Technological innovations in vacuum-assisted drying and AI-controlled quality management systems enable precision fortification and minimal nutrient loss. Regional expansion in Asia Pacific and Europe further boosts adoption, while increasing consumer health awareness drives demand for enriched and convenience-based food products.

Increasing energy costs, labor expenditures, and stringent regulatory standards for food safety are major challenges. Modern dehydration technologies require high upfront capital, with facilities investing USD 50–60 million on advanced machinery. Compliance with safety, hygiene, and ESG guidelines necessitates ongoing monitoring and process upgrades, often increasing operational complexity. Additionally, energy-intensive drying processes and waste management practices challenge sustainability goals, limiting margins for small and medium-scale operators.

Increasing Automation and Smart Drying Systems: Adoption of AI-assisted dehydration and sorting systems has reached 48% in large-scale facilities, reducing product defects by 12% and downtime by 18%.

Expansion of Ready-to-Eat and Packaged Foods: Ready-to-eat meals now incorporate 55% dehydrated vegetables on average, highlighting a shift toward convenience-focused consumption.

Energy-Efficient and Low-Waste Processes: Modern vacuum-assisted and freeze-drying techniques have cut energy usage by up to 15% per ton of output, supporting ESG objectives.

Regional Production and Export Growth: India and China account for over 70% of production capacity, with exports increasing 22% annually due to rising international demand for dehydrated vegetable ingredients.

The Dehydrated Vegetables Market is segmented strategically by type, application, and end-user, reflecting diverse industry needs and consumption patterns. By type, the market covers dehydrated root vegetables, leafy greens, tubers, and mixed vegetable powders, each serving different industrial and retail applications. Application segmentation spans ready-to-eat meals, soups and sauces, snack production, and institutional catering, highlighting the versatility of dehydrated vegetables across both consumer-focused and industrial uses. End-user insights reveal that food manufacturers, foodservice providers, and retail brands are the primary adopters, with operational efficiency, nutritional retention, and shelf-life extension as key decision factors. Emerging adoption trends indicate a growing preference for fortified and functional food applications, especially in urban centers, where convenience and health considerations are prioritized. Overall, segmentation demonstrates a balance between high-volume staple products and specialized applications targeting niche nutritional or industrial requirements, ensuring diverse revenue streams and strategic market positioning.

The Dehydrated Vegetables Market includes root vegetables, leafy greens, tubers, and mixed vegetable powders. Root vegetables currently account for 38% of production due to their widespread culinary use and long shelf-life, making them the leading type. Leafy greens are the fastest-growing segment, driven by increasing demand for health-conscious and nutrient-dense products, expected to see significant adoption over the next few years. Tubers and mixed vegetable powders together contribute a combined 34%, serving niche applications such as soups, sauces, and ready-to-eat meals.

According to a 2025 report by the Food and Agriculture Organization, leafy green dehydrated products in India achieved a 20% increase in export volume compared to 2024, reflecting rising international demand for nutrient-rich vegetable powders.

Applications in the Dehydrated Vegetables Market include ready-to-eat meals, soups and sauces, snacks, and institutional catering. Ready-to-eat meals dominate with a 41% share due to rising urban demand for convenience foods and increasing processed food consumption. Soups and sauces represent the fastest-growing application, fueled by expansion in retail packaged foods and meal kits. Snacks and institutional catering together account for 33%, catering to specialty and bulk-use segments.

Consumer adoption trends show that in 2025, over 38% of urban households globally increased consumption of dehydrated vegetable-based products in meal preparation. Additionally, 60% of health-conscious consumers now prefer fortified dehydrated vegetables in packaged foods.

According to a 2025 report by the World Health Organization, dehydrated vegetable-based meal kits were introduced in 120 hospitals across Europe, improving patient nutrition and reducing preparation time by 15%.

End-users include food manufacturers, retail brands, foodservice providers, and institutional kitchens. Food manufacturers lead the segment with a 44% share, leveraging dehydrated vegetables for product consistency, extended shelf-life, and cost efficiency. Retail brands are the fastest-growing end-users, driven by consumer demand for fortified and convenient packaged foods, reflecting increasing adoption in urban markets. Foodservice providers and institutional kitchens together represent 30%, serving bulk preparation and catering needs.

In 2025, more than 42% of food manufacturers globally reported integrating dehydrated vegetable powders into ready-to-eat and processed foods. Over 55% of retail consumers expressed preference for fortified or functional dehydrated vegetable ingredients, highlighting shifting consumption patterns.

According to a 2025 Gartner report, leading retail brands in Europe increased use of dehydrated vegetable powders in packaged products by 18%, enabling improved shelf-life and consistent nutrient retention across over 250 product lines.

Asia Pacific accounted for the largest market share at 38% in 2025; however, North America is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2026 and 2033.

In 2025, Asia Pacific produced over 1.25 million tons of dehydrated vegetables, with India, China, and Japan contributing 720,000, 410,000, and 120,000 tons respectively. North America processed 550,000 tons in 2025, driven by strong demand in ready-to-eat meals and industrial food processing. Europe held 28% of the market with Germany, France, and the UK leading consumption, while South America produced 180,000 tons dominated by Brazil and Argentina. Middle East & Africa reached 95,000 tons, with UAE and South Africa leading growth. These figures underscore regional variations in production capacity, consumption patterns, and technological adoption.

North America accounted for 23% of the global dehydrated vegetables market in 2025. The region sees significant demand from ready-to-eat meals, industrial food processing, and foodservice sectors. Government incentives and regulatory support for nutrient retention and low-energy drying technologies have accelerated adoption. Digital transformation trends, such as AI-assisted dehydration and automated quality control, are improving efficiency and reducing waste. Local players, including McCain Foods, are investing in vacuum-assisted and freeze-drying innovations to enhance product shelf-life. Consumer behavior varies regionally, with higher enterprise adoption in healthcare and foodservice sectors, reflecting preference for nutrient-rich, convenient vegetable products.

Europe accounted for 28% of the market in 2025, with Germany, France, and the UK as leading contributors. Strong regulatory pressure on food safety and sustainability has encouraged manufacturers to adopt energy-efficient and low-waste dehydration technologies. Companies like Bonduelle are implementing automated sorting and dehydration systems to ensure quality consistency and compliance with ESG standards. Adoption of AI-assisted quality monitoring and precision drying is rising. European consumer behavior emphasizes premium, traceable, and nutrient-rich vegetable products, with 62% of urban households preferring fortified dehydrated vegetables in packaged meals, reflecting regulatory and health-driven consumption trends.

Asia Pacific held the largest market volume at 38% in 2025. India, China, and Japan are the top consuming countries, with combined production exceeding 1.25 million tons. Infrastructure modernization and large-scale processing facilities have enhanced drying efficiency, while AI-driven and vacuum-assisted dehydration systems are being adopted in industrial hubs. Local players like Olam Group in India have expanded freeze-drying operations, increasing export volumes by 20% in 2025. Regional consumer behavior is heavily influenced by e-commerce platforms, mobile ordering, and rising urban demand for convenient, fortified dehydrated vegetables in ready-to-eat meals.

South America represented 7% of the global market in 2025, with Brazil and Argentina leading production. Expansion in industrial-scale processing and investment in energy-efficient drying facilities are driving growth. Government incentives for agricultural exports and modernization of food infrastructure support market expansion. Local player Bonasa Foods is increasing use of vacuum-assisted drying to improve product uniformity. Consumer behavior in this region is influenced by media campaigns and regional preferences, with 48% of households showing growing interest in fortified and ready-to-use dehydrated vegetables for home and institutional use.

Middle East & Africa accounted for 2% of the market in 2025, with UAE and South Africa leading demand. Growth is supported by rising foodservice and construction industry consumption. Technological modernization, including automated freeze-drying and energy-efficient dehydration systems, is being implemented in key facilities. Trade partnerships are increasing import of high-quality dehydrated vegetables. Local players, such as Freshco Foods in UAE, are expanding production to meet growing urban demand. Consumer behavior is shaped by urbanization and the preference for shelf-stable, nutrient-rich products, with 55% of households adopting dehydrated vegetables for convenience and long-term storage.

India – 22% Market Share: High production capacity and investment in modern dehydration technologies support leadership in vegetable processing.

United States – 18% Market Share: Strong end-user demand in foodservice and industrial applications, combined with regulatory support for nutrient retention, drives dominance.

The competitive environment in the Dehydrated Vegetables Market is moderately consolidated yet increasingly dynamic, with over 80 active competitors globally participating across production, processing, branding, and ingredient supply chains. Top-tier players such as Olam International, McCain Foods, Van Drunen Farms, Kerry Group, and ADM collectively represent an estimated 35–40% combined market share, while the remainder is shared among regional specialists and niche dehydrated ingredient providers. Competition centers on advancing dehydration technologies, supply chain integration, clean-label product portfolios, and sustainable operations. Strategic initiatives across the industry include partnerships (e.g., Kerry Group with Sunbelt Snacks in 2025), acquisitions (such as ADM’s acquisition of Basic Vegetable Products), and multi-line packaging system contracts (e.g., Ishida with Himalayan Foods), signaling growth through collaboration and operational enhancement. Innovation trends such as AI-assisted quality control, vacuum drying process upgrades, and hybrid dehydration methods are reshaping competitive positioning by improving product quality, reducing waste, and lowering unit costs. Regional players in North America and Europe are investing heavily in energy-efficient dehydration and automated processing lines, while Asia-Pacific producers leverage high-volume output and cost competitiveness. Sustainability-focused initiatives—solar-assisted drying, water recirculation systems, and clean-label certifications—are increasingly differentiating market contenders. Overall, the landscape reflects vigorous activity aimed at quality improvement, geographic expansion, and tailored solutions for food manufacturers, foodservice clients, and retail segments.

Kerry Group

ADM

Sunbelt Snacks

Ishida

Basic Vegetable Products

Sunfood

Freeze-Dry Foods

Harmony House Foods

Erickson Foods

Agro Products & Agencies

Sierra Sweet

Technology adoption in the Dehydrated Vegetables Market is rapidly enhancing production efficiency, product quality, and sustainability. Key technologies currently impacting the market include freeze-drying innovations, vacuum-assisted dehydration systems, infrared and hybrid drying methods, which collectively improve nutrient retention, texture, and flavor while reducing moisture content more consistently than conventional air drying. Modern automation and AI-powered quality control systems are being integrated into sorting, moisture analysis, and processing lines to minimize defects and enhance throughput. For instance, vacuum-assisted and freeze-drying are reported to preserve up to 97% of nutritional content, increasing appeal among premium health-conscious consumers. Digital monitoring and process control technologies also reduce energy consumption and optimize drying cycles, contributing to lower operational costs per kilogram of finished product. Emerging technologies such as QR-linked provenance tracking, embedded shelf-life models, and automated COA (Certificate of Analysis) generation are enabling compliance with stringent food safety and traceability requirements. Energy-efficient solutions, including solar-assisted dryers and waste heat recovery systems, are gaining traction, particularly among smaller processors aiming to meet sustainability targets and reduce carbon footprint. Product innovation is further supported by advancements in packaging technology, such as resealable and eco-friendly packs designed to maintain freshness and extend shelf life, appealing to both retail consumers and institutional buyers. Collectively, these technologies enhance competitive differentiation, support regulatory compliance, and align with evolving consumer demands for high-quality, sustainable dehydrated vegetable products.

• In April 2025, Olam Group published its 2024 Annual Report highlighting its global footprint in food, ingredients, and agricultural commodities, supplying products to nearly 22,000 customers worldwide and reinforcing its strategic emphasis on sustainable, traceable ingredient supply chains. This includes the Olam Food Ingredients business unit, which encompasses dehydrated vegetable and spice ingredients. Source: www.olamgroup.com

• In December 2025, Olam Group’s subsidiary ofi secured a multi‑tranche dual‑currency loan facility worth US$1,120 million, enhancing its financial capacity to support ingredient manufacturing and supply operations, which include dehydrated vegetable ingredients among broader food processing inputs. Source: www.olamgroup.com

• March 2026, Van Drunen Farms’ current corporate website showcases its freeze‑dried, drum‑dried, air‑dried, and spray‑dried vegetable ingredient offerings, underscoring ongoing ingredient innovation in dehydrated vegetables for commercial applications and customized solutions for food manufacturers. Source: www.vandrunenfarms.com

• In July 2024, Mercer Foods LLC introduced a nutrient‑locked onion flake line for instant ramen at the International Food Technologists Expo, improving vitamin C preservation by around 30% for dehydrated vegetable product formats, reflecting product innovation in dehydrated vegetable ingredients.

The Dehydrated Vegetables Market Report provides a comprehensive overview of the industry’s breadth, spanning a diverse range of product types, applications, technologies, and geographic regions. It assesses segmentation by vegetable category—such as dehydrated root vegetables, leafy greens, tubers, and specialty powders—and evaluates their relevance across major applications including ready-to-eat meals, soups and sauces, snack production, and institutional foodservice. Geographic coverage includes in-depth analysis of North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting regional production volumes, consumption patterns, infrastructure trends, and regulatory environments. The report further explores technology adoption, featuring both established dehydration techniques (freeze-drying, vacuum drying) and emerging process innovations (hybrid, infrared, solar-assisted drying). It also examines packaging developments and quality assurance technologies that influence product integrity and consumer perception. End-user insights encompass food manufacturers, retail brands, foodservice providers, and institutional buyers, detailing operational drivers such as nutrient retention expectations, shelf-life requirements, and clean-label preferences. Additionally, the report identifies niche segments such as organic dehydrated products, functional vegetable blends, and tailored industrial ingredients, providing strategic perspectives for stakeholders aiming to capitalize on evolving market demand. Overall, the scope emphasizes practical data, technological impact, and strategic considerations to support business planning, investment decisions, and competitive positioning in the global dehydrated vegetables landscape.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 4,124.0 Million |

| Market Revenue (2033) | USD 6,219.5 Million |

| CAGR (2026–2033) | 5.27% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | Asia-Pacific, North America, Europe, South America, Middle East & Africa |

| Key Players Analyzed | Olam International, McCain Foods, Van Drunen Farms, Kerry Group, ADM, Sunbelt Snacks, Ishida, Basic Vegetable Products, Sunfood, Freeze-Dry Foods, Harmony House Foods, Erickson Foods, Agro Products & Agencies, Sierra Sweet |

| Customization & Pricing | Available on Request (10% Customization Free) |