Reports

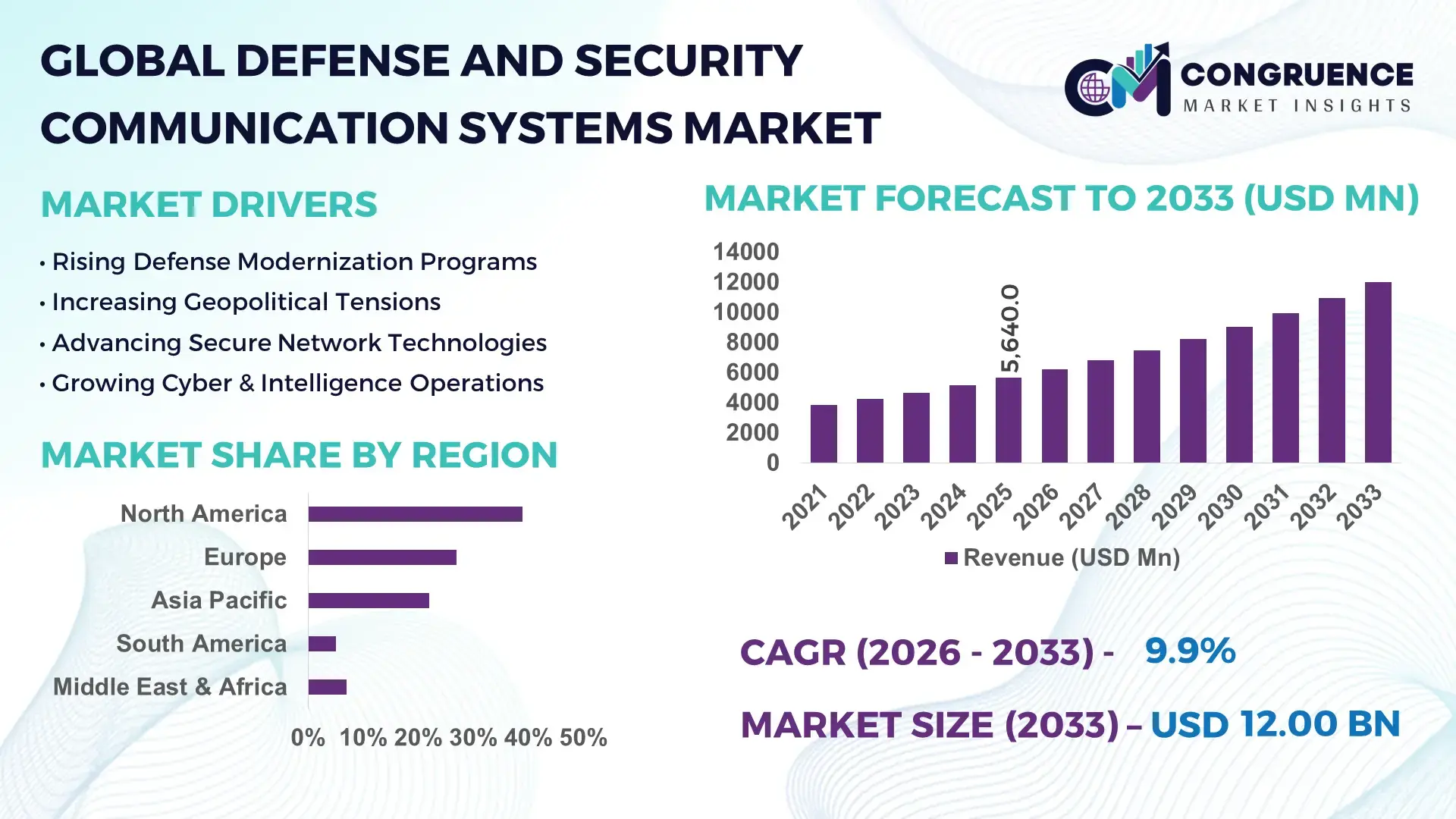

The Global Defense and Security Communication Systems Market was valued at USD 5,640.0 Million in 2025 and is anticipated to reach a value of USD 12,002.2 Million by 2033 expanding at a CAGR of 9.9% between 2026 and 2033, according to an analysis by Congruence Market Insights. The growth is primarily driven by increasing modernization of military communication infrastructure and rapid integration of secure digital and satellite-based communication technologies across defense forces worldwide.

The United States represents the dominant country in the Defense and Security Communication Systems Market, supported by its defense budget exceeding USD 880 billion in 2025, of which over 12% is allocated to C4ISR (Command, Control, Communications, Computers, Intelligence, Surveillance, and Reconnaissance) systems. The U.S. Department of Defense operates more than 30 military satellite communication constellations, including advanced SATCOM and secure tactical radio networks. Over 65% of active-duty units utilize software-defined radios (SDRs) for encrypted battlefield communication. Domestic production capacity includes large-scale manufacturing facilities operated by leading contractors delivering thousands of encrypted communication terminals annually. Investments in AI-enabled battlefield networking and 5G-enabled tactical communications exceeded USD 4 billion in recent defense modernization programs, supporting rapid deployment and interoperability across land, air, naval, cyber, and space operations.

Market Size & Growth: Valued at USD 5,640.0 Million in 2025, projected to reach USD 12,002.2 Million by 2033 at a CAGR of 9.9%, driven by military digitization and secure network modernization initiatives.

Top Growth Drivers: Secure SDR adoption 68%, satellite-based communication expansion 54%, AI-enabled network optimization 47%.

Short-Term Forecast: By 2028, AI-based network management systems are expected to reduce communication latency by 30% and improve operational efficiency by 25%.

Emerging Technologies: AI-driven tactical networking, quantum-encrypted communication systems, and 5G-enabled battlefield connectivity platforms.

Regional Leaders: North America projected at USD 4,600 Million by 2033 with high SATCOM penetration; Europe at USD 3,100 Million driven by NATO interoperability upgrades; Asia-Pacific at USD 2,900 Million supported by defense digitization programs.

Consumer/End-User Trends: Over 70% of military modernization programs prioritize encrypted mobile communication devices and integrated command systems.

Pilot or Case Example: In 2024, a NATO tactical networking pilot improved real-time battlefield data exchange speed by 35% and reduced signal disruptions by 22%.

Competitive Landscape: Market leader holds approximately 24% share, followed by major players including Lockheed Martin, Northrop Grumman, Thales Group, and BAE Systems.

Regulatory & ESG Impact: Governments mandate encrypted communication compliance standards; defense agencies target 20% energy efficiency improvements in communication hardware by 2030.

Investment & Funding Patterns: Over USD 15 billion allocated globally toward next-generation secure communication and satellite modernization programs.

Innovation & Future Outlook: Integration of AI, edge computing, and interoperable multi-domain communication systems is reshaping mission-critical defense operations.

Defense communication systems serve land forces (42%), naval operations (28%), air forces (24%), and homeland security agencies (6%). Recent innovations include AI-powered spectrum management tools improving bandwidth utilization by 30% and compact encrypted SDRs reducing device weight by 18%. Regulatory mandates emphasize cyber-resilience and NATO STANAG compliance. North America leads in consumption, while Asia-Pacific records strong procurement growth. Emerging trends include space-based communication integration and multi-domain command platforms.

The Defense and Security Communication Systems Market plays a critical strategic role in enabling secure, real-time coordination across multi-domain military operations. Modern defense doctrines increasingly rely on network-centric warfare, where seamless data exchange determines operational superiority. AI-enabled communication platforms now deliver 40% faster data processing compared to legacy analog radio networks, significantly enhancing situational awareness and command efficiency.

North America dominates in deployment volume due to extensive modernization programs, while Europe leads in adoption intensity with over 72% of NATO-aligned enterprises integrating interoperable encrypted communication frameworks. Asia-Pacific nations are accelerating procurement cycles, with defense digitalization budgets increasing by more than 18% annually in key economies.

By 2028, AI-powered spectrum management and predictive network analytics are expected to reduce communication downtime by 28% and improve mission readiness metrics by 22%. Firms are committing to ESG targets, including 25% energy reduction in communication hardware manufacturing by 2030 and increased recycling of electronic components.

In 2024, the U.S. Department of Defense implemented AI-based battlefield network optimization, achieving a 33% improvement in bandwidth allocation efficiency across deployed units. Similarly, European defense agencies reported a 20% reduction in signal interference following secure 5G tactical integration pilots.

Looking ahead, the Defense and Security Communication Systems Market will remain a pillar of resilience, compliance, and sustainable defense modernization, underpinning secure connectivity across cyber, space, land, sea, and air domains while aligning with regulatory and environmental standards.

The Defense and Security Communication Systems Market is influenced by rapid technological advancement, geopolitical tensions, and evolving cyber-threat landscapes. Governments are prioritizing secure, interoperable communication frameworks to support joint operations and multinational defense alliances. Increasing reliance on satellite communication, tactical radios, and encrypted mobile networks has accelerated procurement cycles across defense ministries. Digital battlefield transformation initiatives are promoting integration of AI, cloud computing, and edge processing to enhance real-time decision-making capabilities. Furthermore, rising cross-border security collaborations are encouraging standardized communication protocols. Cybersecurity resilience remains central, with over 60% of defense IT investments allocated toward secure communication and network protection systems.

Global defense forces are upgrading C4ISR infrastructure to enhance interoperability and battlefield awareness. Over 70% of modernization programs include replacement of legacy analog systems with encrypted digital communication networks. Tactical software-defined radios have improved secure communication range by 35% compared to older VHF systems. Additionally, satellite-based command networks enable real-time coordination across thousands of kilometers, improving mission execution efficiency by nearly 30%. Increased deployment of integrated communication terminals across naval fleets and airborne platforms further strengthens operational continuity and data-sharing capacity.

Advanced communication systems require complex integration with legacy infrastructure, increasing implementation costs by 20–30% in large-scale deployments. Encryption compliance, interoperability testing, and cybersecurity certifications add significant development timelines. Additionally, secure satellite bandwidth procurement and maintenance contracts increase long-term operational expenditures. Training personnel for AI-enabled and 5G-integrated tactical systems further elevates defense budgets. Budgetary constraints in emerging economies limit large-scale procurement despite rising security needs, slowing adoption rates in price-sensitive regions.

The integration of space-based low-earth orbit (LEO) satellite constellations provides latency reductions of up to 45% compared to traditional geostationary systems. AI-driven network optimization improves spectrum utilization efficiency by 30%, enabling higher data throughput for real-time surveillance and reconnaissance. Defense agencies are investing in hybrid communication architectures combining terrestrial 5G, satellite, and edge computing networks. Growing focus on autonomous systems and unmanned platforms further creates demand for secure, low-latency communication links.

Electronic warfare technologies can disrupt or jam communication signals, reducing operational effectiveness by up to 25% during high-intensity conflicts. Cyberattacks targeting defense communication networks increased by over 40% in recent years, requiring continuous system upgrades. Ensuring quantum-resistant encryption standards demands significant R&D investment. Additionally, cross-border interoperability requirements complicate system standardization, while regulatory compliance across allied nations increases deployment complexity and validation timelines.

AI-Enabled Tactical Networking Improving Data Throughput by 35%: Defense agencies are deploying AI-driven network management systems capable of increasing bandwidth efficiency by 35% and reducing latency by 30%. Over 60% of newly procured tactical radios now include embedded AI-based signal optimization modules.

Expansion of Secure SATCOM and LEO Integration by 45%: Integration of LEO satellite systems has reduced communication latency by 40–45% compared to traditional GEO satellites. More than 50% of new defense satellite contracts involve hybrid multi-orbit architectures to ensure redundancy and resilience.

Rapid Adoption of 5G-Enabled Battlefield Communication with 28% Performance Gain: Tactical 5G deployments across military bases have demonstrated 28% faster data transmission and 22% improvement in real-time situational awareness. Over 35% of advanced defense installations have initiated private 5G network pilots.

Transition to Energy-Efficient and Modular Communication Hardware Reducing Power Use by 20%: Next-generation communication terminals consume 20% less power and reduce device weight by 18%, improving field mobility. Modular hardware designs shorten deployment time by 25% and simplify maintenance cycles across multi-domain operations.

The Defense and Security Communication Systems Market is strategically segmented by type, application, and end-user, reflecting the complexity of modern defense operations. Product diversification spans tactical radios, satellite communication systems, secure networking platforms, and integrated command communication suites. Applications range from land-based battlefield communication and naval fleet coordination to airborne data exchange and homeland security surveillance networks. End-users include military forces, homeland security agencies, intelligence organizations, and defense contractors.

Technological evolution is driving integration across these segments, with over 65% of defense modernization programs prioritizing interoperable, encrypted, and AI-enabled systems. Tactical mobility, multi-domain operations, and real-time intelligence sharing are central to procurement strategies. Decision-makers increasingly evaluate systems based on interoperability compliance, latency reduction metrics, cybersecurity resilience, and scalability across joint command structures.

The market by type includes Tactical Radio Systems, Satellite Communication (SATCOM) Systems, Secure Networking & Cyber Communication Platforms, and Integrated Command & Control Communication Systems. Tactical Radio Systems currently account for approximately 38% of total adoption due to their widespread deployment across infantry units and armored divisions. These systems provide encrypted, real-time voice and data communication with mobility advantages and up to 35% extended operational range compared to legacy analog radios.

Satellite Communication Systems hold nearly 27% share, driven by beyond-line-of-sight connectivity requirements in naval and airborne operations. However, Secure Networking & Cyber Communication Platforms represent the fastest-growing type, expanding at an estimated 11.8% CAGR, fueled by increasing cyber warfare threats and demand for AI-driven spectrum management. Adoption of these platforms is accelerating in multi-domain command environments where secure cloud-based and edge-enabled communication ensures 30% faster data processing speeds.

Integrated Command & Control Communication Systems and other niche secure hardware collectively contribute around 35% of the market, supporting interoperability across land, sea, air, and cyber units.

Key application areas include Land Forces Communication, Naval Communication Systems, Airborne Communication Systems, Cyber & Intelligence Communication, and Homeland Security Operations. Land Forces Communication dominates with nearly 41% share due to the extensive deployment of tactical radios and secure battlefield networking across ground units. Modern infantry operations rely on encrypted mobile communication terminals integrated with surveillance drones and command centers, enhancing situational awareness by 28%.

Naval Communication Systems account for around 23%, supporting secure SATCOM-based fleet coordination across long-range maritime operations. Airborne Communication Systems represent approximately 19%, integrating high-frequency secure links and data relay platforms within fighter aircraft and surveillance drones. However, Cyber & Intelligence Communication applications are expanding fastest, projected to grow at nearly 12.5% CAGR, driven by AI-powered threat detection and encrypted intelligence-sharing platforms. Homeland Security and border surveillance applications collectively contribute about 17%.

In 2025, more than 45% of NATO-aligned defense agencies reported piloting AI-integrated battlefield communication platforms. Additionally, over 52% of advanced air forces globally are upgrading to encrypted multi-band communication systems to counter electronic warfare threats.

The primary end-users include Military & Armed Forces, Homeland Security Agencies, Intelligence Agencies, and Defense Contractors & System Integrators. Military & Armed Forces account for approximately 62% of total deployment, reflecting large-scale procurement of tactical radios, satellite communication terminals, and integrated command systems across army, navy, and air force divisions. Over 70% of modernization budgets in developed economies prioritize encrypted battlefield communication upgrades.

Homeland Security Agencies represent about 18%, focusing on border surveillance networks and emergency response communication systems. Intelligence Agencies contribute nearly 12%, utilizing secure cyber communication and encrypted data-sharing platforms. However, Defense Contractors & System Integrators are the fastest-growing end-user segment, expanding at around 10.9% CAGR, as governments increasingly outsource system integration and lifecycle management services. Combined, the remaining segments account for roughly 20% of deployments in specialized and civilian security applications.

In 2025, approximately 48% of defense contractors globally reported integrating AI-based communication optimization tools into military projects. Furthermore, 55% of homeland security agencies in advanced economies are testing encrypted 5G-enabled emergency communication systems.

North America accounted for the largest market share at 39% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11.7% between 2026 and 2033.

North America’s dominance is supported by defense communication modernization budgets exceeding USD 100 billion allocated to C4ISR and secure networking upgrades, with over 70% of military units equipped with encrypted digital radios. Europe follows with 27% share, driven by NATO interoperability programs across more than 20 member states and joint communication standardization initiatives. Asia-Pacific holds approximately 22% share, supported by rapid procurement in China, India, Japan, and South Korea, where defense digital transformation budgets increased by over 18% in recent cycles. The Middle East & Africa account for 7%, with rising investment in border security and oil & gas infrastructure protection systems. South America represents nearly 5%, led by Brazil and Argentina focusing on satellite-enabled defense coordination and national security network upgrades.

North America represents approximately 39% of the global Defense and Security Communication Systems Market, supported by large-scale modernization of tactical radios, satellite communication systems, and AI-enabled command networks. The region’s defense sector allocates over 12% of total military expenditure toward C4ISR and secure communication upgrades. Key demand originates from land forces, naval fleets, aerospace defense units, and homeland security agencies, with over 65% of new procurement contracts focusing on encrypted multi-band communication devices. Regulatory mandates emphasize zero-trust cybersecurity frameworks and compliance with advanced encryption standards. Technological transformation includes integration of private 5G military networks, AI-driven spectrum management improving bandwidth efficiency by 30%, and quantum-resistant encryption pilots. A major regional defense contractor recently deployed next-generation software-defined radios across multiple brigades, enhancing interoperability for more than 50,000 personnel. Enterprise-level adoption is highest in defense and aerospace sectors, reflecting strong institutional procurement behavior and rapid digital transformation cycles.

Europe accounts for approximately 27% of the global Defense and Security Communication Systems Market, with Germany, the UK, and France representing over 60% of regional demand. NATO-aligned communication upgrades across 20+ member states emphasize standardized encrypted tactical networking. Regulatory frameworks prioritize cross-border interoperability and cybersecurity resilience, increasing demand for compliant, secure communication hardware. Adoption of AI-integrated command platforms and secure SATCOM systems has improved multinational exercise coordination efficiency by 28%. Sustainability initiatives aim to reduce defense communication hardware energy consumption by 20% by 2030, encouraging modular and energy-efficient system designs. A prominent European defense manufacturer has advanced encrypted naval communication suites supporting secure long-range maritime operations across thousands of kilometers. Procurement behavior reflects regulatory-driven purchasing decisions, with over 55% of defense agencies prioritizing explainable and standards-compliant communication technologies.

Asia-Pacific holds nearly 22% of the global Defense and Security Communication Systems Market and ranks as the fastest-growing region by volume expansion. China, India, Japan, and South Korea collectively account for more than 75% of regional procurement activity. Infrastructure expansion includes deployment of advanced tactical radios across thousands of border units and integration of secure satellite communication for naval fleets operating in high-traffic maritime corridors. Manufacturing capacity for communication hardware has expanded by over 20% in key defense production hubs, strengthening domestic supply chains. Innovation hubs are accelerating AI-enabled battlefield networking and cyber-secure cloud-based command platforms. A leading regional defense electronics firm recently introduced compact encrypted communication terminals reducing device weight by 18%, enhancing mobility for field units. Adoption behavior reflects strong government-led procurement, with over 60% of defense modernization initiatives prioritizing digital and AI-integrated communication frameworks.

South America contributes approximately 5% to the global Defense and Security Communication Systems Market, led by Brazil and Argentina. Brazil accounts for over 45% of regional demand, supported by satellite communication upgrades and modernization of naval command networks. Infrastructure investments focus on border monitoring and maritime surveillance systems covering more than 7,000 kilometers of coastline. Government defense initiatives promote secure communication standardization and public–private partnerships to strengthen national cybersecurity infrastructure. Local defense electronics firms are expanding encrypted tactical radio production capacity to meet rising domestic demand. Regional procurement behavior emphasizes cost-efficient, modular systems, with nearly 40% of defense contracts targeting upgrade of legacy analog communication networks to digital encrypted platforms. Adoption trends remain closely tied to national security priorities and critical infrastructure protection requirements.

The Middle East & Africa account for nearly 7% of the global Defense and Security Communication Systems Market, driven by rising demand for secure communication in oil & gas infrastructure, border security, and counterterrorism operations. The UAE and Saudi Arabia represent over 50% of regional procurement, while South Africa leads in sub-Saharan modernization programs. Technological modernization includes integration of encrypted SATCOM systems for cross-border military coordination and adoption of AI-driven surveillance communication platforms improving real-time response efficiency by 25%. Trade partnerships and defense offset agreements support local manufacturing expansion. A regional defense technology firm recently deployed secure mobile communication units enhancing encrypted connectivity for rapid-response teams across remote desert regions. Procurement behavior emphasizes resilience, mobility, and secure cross-agency interoperability.

United States – 34% Market Share: The United States leads the Defense and Security Communication Systems Market due to high production capacity, advanced C4ISR deployment across all armed forces divisions, and large-scale encrypted communication modernization programs.

China – 16% Market Share: China maintains strong positioning in the Defense and Security Communication Systems Market supported by rapid domestic manufacturing expansion, large-scale military digitization initiatives, and significant investment in secure satellite and tactical communication systems.

The Defense and Security Communication Systems Market is moderately consolidated, characterized by the presence of approximately 40–50 active global and regional competitors, including large defense primes and specialized communication technology providers. The top five companies collectively account for nearly 58% of the total market share, reflecting strong positioning in tactical radios, SATCOM terminals, and integrated C4ISR platforms.

Market leaders differentiate through vertically integrated production capabilities, long-term government framework contracts, and proprietary encryption technologies. Over 65% of leading players invest heavily in R&D focused on AI-enabled networking, quantum-resistant encryption, and multi-domain interoperability. Strategic initiatives in 2024–2025 include joint ventures for secure satellite constellations, partnerships for private 5G military base deployment, and mergers enhancing cyber-secure communication portfolios.

Product innovation cycles have shortened by nearly 20% over the past three years, driven by evolving electronic warfare threats and rapid digital transformation within armed forces. Competitive intensity is highest in North America and Europe, where procurement standards demand strict interoperability compliance. Emerging players in Asia-Pacific are expanding domestic manufacturing capacity by over 15% annually, intensifying competition in software-defined radios and secure networking modules. Overall, innovation speed, cybersecurity resilience, and integration expertise remain decisive competitive differentiators.

Thales Group

L3Harris Technologies

Raytheon Technologies

General Dynamics Mission Systems

Leonardo S.p.A.

Airbus Defence and Space

Elbit Systems

Saab AB

Rohde & Schwarz

Cobham Advanced Electronic Solutions

Viasat Inc.

Honeywell Aerospace

Technological innovation in the Defense and Security Communication Systems Market is centered on secure, resilient, and multi-domain communication architectures. Software-defined radios (SDRs) now represent over 60% of newly deployed tactical communication devices, enabling frequency agility, enhanced encryption, and interoperability across allied forces. These SDRs improve secure transmission range by up to 35% compared to legacy fixed-frequency systems.

Low-Earth Orbit (LEO) satellite integration has reduced latency by approximately 40%, supporting real-time intelligence and surveillance operations. Hybrid communication architectures combining terrestrial 5G, SATCOM, and edge computing are increasingly adopted, with over 50% of advanced military bases piloting private 5G secure networks. AI-driven spectrum management platforms enhance bandwidth efficiency by nearly 30%, reducing signal congestion in high-density operational zones.

Quantum-resistant encryption algorithms are being tested in next-generation secure networks to counter emerging cyber threats. Meanwhile, modular hardware architectures have reduced system deployment time by 25%, supporting rapid field integration. Edge-enabled communication nodes process mission-critical data locally, lowering response times by up to 28% in tactical environments.

Cybersecurity integration is now embedded in over 70% of new defense communication procurement contracts, reflecting the priority placed on zero-trust frameworks and intrusion detection systems. These technological advancements collectively strengthen operational resilience, data integrity, and multi-domain coordination capabilities.

• In April 2025, L3Harris Technologies announced a strategic partnership with Kuiper Government Solutions (KGS) to deliver integrated resilient satellite communications (SATCOM) solutions for military and government customers, combining L3Harris’ tactical network technology with KGS’ low-Earth-orbit satellite network to enhance secure, low-latency global connectivity. Source: www.l3harris.com

• In December 2025, L3Harris showcased a first-of-its-kind interoperable network demonstration connecting tactical communications, counter-UAS systems, advanced imaging, and 5G gateway solutions, enabling instant communication across U.S. government agencies and improving connectivity in degraded, contested environments. Source: www.l3harris.com

• In May 2025, Honeywell’s JetWave™ X high-speed SATCOM system was selected for use in advanced U.S. Army aircraft, enhancing connectivity and resilient multi-network architecture for airborne reconnaissance and electronic warfare missions. Source: www.aerospace.honeywell.com

• In March 2025, Comtech Telecommunications secured multiple sole-source contracts from L3Harris worth over USD 26 million to supply modem technologies for next-generation protected SATCOM programs (A3M anti-jam modems) that support U.S. Air Force and U.S. Army secure communications operations. Source: www.markets.financialcontent.com

The Defense and Security Communication Systems Market Report provides comprehensive coverage across product types, applications, technologies, and geographic regions. The scope includes tactical radio systems, satellite communication platforms, secure networking solutions, integrated command and control systems, and emerging AI-enabled communication architectures. Over 65% of defense modernization initiatives globally involve upgrades to encrypted digital communication systems, underscoring the report’s focus on secure and interoperable technologies.

Geographically, the report evaluates North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, collectively accounting for 100% of global defense communication deployment activity. Key consuming countries such as the United States, China, Germany, India, and the UAE are analyzed in detail, representing over 70% of worldwide procurement volume.

Application coverage spans land forces, naval fleets, airborne units, cyber defense, intelligence agencies, and homeland security operations. The report also examines emerging segments such as private 5G military networks, LEO satellite integration, quantum-resistant encryption systems, and edge-enabled battlefield communication nodes.

In addition to hardware, the scope incorporates software-defined networking, AI-driven spectrum optimization, cybersecurity integration, and modular system design trends. The analysis supports strategic planning by offering quantitative benchmarks on adoption rates, interoperability standards, deployment patterns, and innovation intensity shaping future defense communication ecosystems.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 5,640.0 Million |

| Market Revenue (2033) | USD 12,002.2 Million |

| CAGR (2026–2033) | 9.9% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Lockheed Martin; Northrop Grumman; BAE Systems; Thales Group; L3Harris Technologies; Raytheon Technologies; General Dynamics Mission Systems; Leonardo S.p.A.; Airbus Defence and Space; Elbit Systems; Saab AB; Rohde & Schwarz; Viasat Inc.; Honeywell Aerospace |

| Customization & Pricing | Available on Request (10% Customization Free) |