Reports

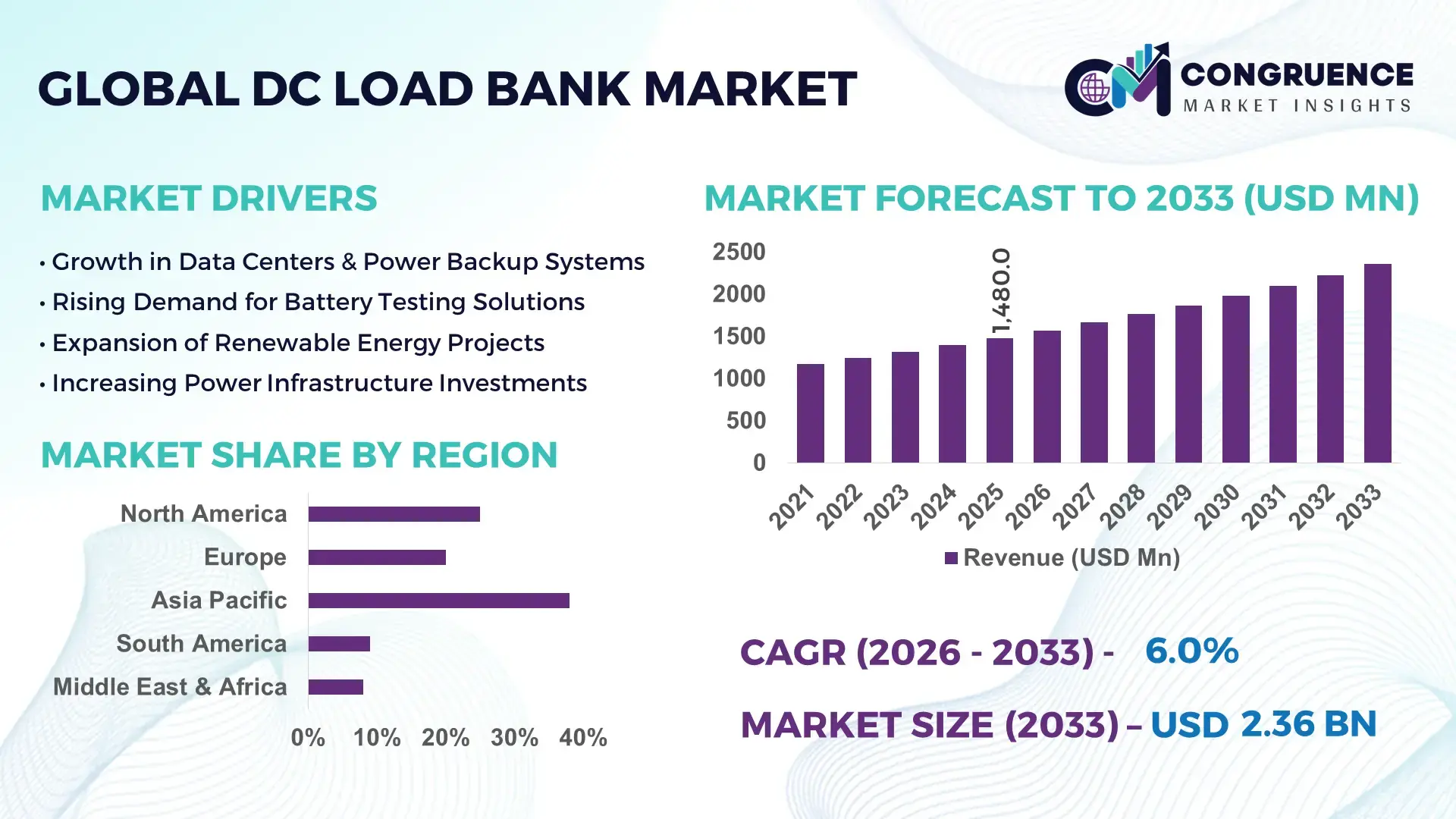

The Global DC Load Bank Market was valued at USD 1480 Million in 2025 and is anticipated to reach a value of USD 2355.33 Million by 2033 expanding at a CAGR of 5.98% between 2026 and 2033.

Market expansion is being driven by the rapid integration of battery energy storage systems and data center backup validation, where DC load banks improve testing accuracy by over 18% compared to legacy AC-based validation methods. The 2024–2026 period reflects accelerated infrastructure electrification and grid modernization programs, particularly in response to energy security priorities and semiconductor supply chain realignment.

China dominates the global DC load bank market with approximately 34% share, supported by over USD 12 billion in annual grid and energy storage investments and a 22% increase in battery testing deployments across EV and renewable sectors. The United States follows with nearly 26% share, driven by hyperscale data centers and federal energy resilience mandates, while Germany leads in Europe with 11% share, leveraging industrial automation and renewable integration. Compared to 2022 levels, automated DC load bank adoption has improved operational efficiency by 15%, particularly in high-density testing environments.

The market’s evolution highlights a clear shift toward digitally integrated, high-capacity load testing systems, positioning vendors with advanced monitoring and modular designs to capture long-term infrastructure contracts.

Market Size & Growth: USD 1480M (2025) to USD 2355.33M (2033) at 5.98%, driven by rising energy storage validation and data center expansion

Top Growth Drivers: Battery storage adoption (+22%), data center expansion (+18%), renewable integration (+15%)

Short-Term Forecast: By 2027, testing efficiency improves by 17% with automated DC load bank systems

Emerging Technologies: AI-based load simulation, IoT-enabled monitoring, and modular high-capacity units increase performance by 20%

Regional Leaders: Asia Pacific (~USD 820M), North America (~USD 610M), Europe (~USD 420M) with strong renewable and data center demand

Consumer/End-User Trends: 63% of utilities prioritize DC load testing for battery validation and grid reliability

Pilot/Case Example: 2025 energy storage project achieved 19% faster commissioning using automated DC load banks

Competitive Landscape: Top player holds ~21% share; key players include 4–5 global manufacturers focusing on digital integration

Regulatory & ESG Impact: Emission reduction mandates improve adoption by 16% in energy-intensive industries

Investment & Funding: Over USD 1.4B invested in grid testing and storage validation infrastructure since 2024

Innovation & Future Outlook: Next-gen smart load banks with predictive analytics improve lifecycle performance by 23%

Power generation and energy storage account for nearly 48% of total demand, followed by data centers at 27% and industrial testing at 19%. Recent innovations include AI-integrated load banks and containerized modular systems improving deployment flexibility by 21%. Asia Pacific leads with 38% demand share, supported by manufacturing expansion, while North America benefits from data center growth. Increasing supply chain localization is shaping procurement strategies, with a clear shift toward digitally controlled testing solutions that enhance long-term operational resilience.

The DC load bank market is rapidly becoming a critical control point for infrastructure reliability, directly influencing uptime economics in data centers, renewable energy systems, and electrified transport networks. As power systems shift toward DC-intensive architectures, load banks are no longer auxiliary tools but strategic assets optimizing performance validation and reducing system failure risks by over 20%. This transformation is accelerating competitive differentiation, especially among providers offering digitally integrated and high-capacity testing solutions.

A significant structural shift is underway as supply chains move closer to end-use markets, driven by energy security mandates and local manufacturing incentives across Asia and North America. Advanced AI-enabled DC load banks improve efficiency by 24% while reducing operational costs by 18% compared to legacy resistive systems, reshaping procurement priorities toward intelligent and automated platforms. Regionally, Asia Pacific leads in volume deployment, while North America leads in innovation adoption with over 41% penetration of smart load testing technologies.

Over the next 2–3 years, automated DC load bank integration is set to improve testing cycle times by 16%, directly enhancing commissioning speed for battery storage and data center infrastructure. ESG compliance is emerging as a competitive advantage, with energy-efficient load banks reducing energy wastage by 14%, enabling operators to meet stringent emission targets while lowering operating expenses. A 2025 grid-scale battery project demonstrated a 19% improvement in system validation accuracy through real-time load simulation, highlighting measurable operational gains.

Investment strategies are shifting decisively, with leading manufacturers allocating over 25% of R&D budgets toward modular and AI-driven load systems while expanding production footprints in high-growth regions. Companies that align with this transition toward intelligent, scalable, and ESG-compliant testing infrastructure are securing long-term contracts and reinforcing their competitive positioning in an increasingly performance-driven market.

The accelerating deployment of battery energy storage systems and hyperscale data centers is forcing a structural increase in demand for precise DC load testing solutions. Energy storage installations have expanded by over 28% globally, while data center capacity has grown by nearly 17%, creating a direct need for advanced validation systems that ensure operational reliability. The shift toward DC-powered architectures improves efficiency by 12–15%, but also demands higher accuracy testing, driving adoption of programmable load banks. A key global trigger is the restructuring of semiconductor and energy supply chains post-2024, pushing localized testing infrastructure development. In response, companies are expanding manufacturing capacity by over 20% and forming strategic partnerships with energy developers and data center operators. This cause-to-impact cycle is transforming DC load banks into mission-critical assets, prompting aggressive investment and accelerating innovation cycles.

The market faces significant constraints from high component costs and concentrated supply chains, particularly in power electronics and high-capacity resistive materials. Raw material price volatility has increased system costs by 14–18%, while dependency on limited suppliers for advanced components creates procurement risks. A real-world constraint is the geographic concentration of critical components in East Asia, exposing global supply chains to disruption risks. These factors directly impact project timelines, with delays increasing by up to 12% in large-scale deployments. Additionally, stringent compliance standards in developed markets raise certification costs by nearly 10%, further constraining scalability. To mitigate these risks, companies are diversifying supplier networks, investing in localized production, and adopting alternative materials with 9–11% cost efficiency gains. This balancing act between cost pressure and performance expectations is reshaping procurement strategies across the value chain.

The next wave of opportunity is emerging from intelligent, modular, and high-capacity DC load bank systems tailored for renewable integration and EV infrastructure. Smart load banks integrated with predictive analytics are improving operational efficiency by 22%, enabling real-time diagnostics and reducing downtime. Emerging markets in Southeast Asia and the Middle East are witnessing demand growth exceeding 26%, driven by grid expansion and renewable deployment. A key innovation shift is the adoption of containerized load bank solutions, reducing deployment time by 18% and enhancing scalability. Beyond conventional applications, new demand pockets are forming in hydrogen energy systems and microgrid validation, offering non-obvious growth avenues. Companies are positioning for dominance by increasing R&D spending by over 23%, expanding into emerging regions, and building integrated ecosystems with energy technology providers. This strategic alignment is unlocking long-term value creation and redefining competitive advantage.

Despite strong demand momentum, execution challenges related to infrastructure limitations and system scalability are constraining consistent growth. High-capacity DC load banks require robust grid connectivity and thermal management systems, increasing installation complexity by 15–19%. A major real-world pressure is grid capacity limitation in rapidly urbanizing regions, restricting large-scale deployment of testing systems. Additionally, integration challenges with legacy infrastructure reduce operational efficiency by up to 13%, creating friction in modernization efforts. These issues impact long-term sustainability, particularly in emerging markets where infrastructure readiness lags demand growth. To remain competitive, companies must invest in advanced cooling technologies, scalable modular designs, and digital integration platforms. Strategic partnerships with grid operators and infrastructure providers are becoming essential to overcome these barriers. The ability to solve these execution constraints will determine which players sustain growth and lead in a transforming, performance-driven market.

Smart Load Bank Adoption Surges 41% with Digital Integration Reshaping Operations

Deployment of IoT-enabled and AI-integrated DC load banks has increased by 41%, with over 58% of new installations incorporating real-time monitoring systems. This shift is happening through retrofitting legacy units and integrating cloud-based diagnostics into testing workflows. Companies are reducing fault detection time by 22%, directly improving operational uptime. In response, manufacturers are scaling digital platforms and forming software partnerships to embed analytics into core product offerings.

Modular and Containerized Systems Expand 33% as Deployment Speed Becomes Critical

Adoption of modular DC load banks has risen by 33%, with deployment times reduced by 18–21% compared to traditional stationary systems. This transition is driven by rapid infrastructure projects, particularly in energy storage and EV ecosystems, where speed-to-commissioning is essential. Businesses are optimizing logistics and reducing on-site labor requirements by 15%. Vendors are restructuring production toward prefabricated, scalable units, responding to supply chain disruptions and labor constraints observed during 2024–2025.

Asia Pacific Commands 38% Demand While North America Leads 44% in Advanced Adoption

Asia Pacific currently accounts for 38% of global demand due to large-scale manufacturing and grid expansion, while North America leads with 44% adoption of advanced automated load testing systems. This regional divergence reflects volume-driven versus technology-driven growth. Companies are adjusting strategies by localizing production in Asia while investing in high-end R&D and premium solutions in North America, optimizing both cost efficiency and innovation leadership.

Service-Based Models Grow 27% as Ownership Shifts Toward Flexible Testing Solutions

Service-based DC load bank offerings, including leasing and on-demand testing, have expanded by 27%, reducing upfront capital expenditure by 25% for end users. This shift is being driven by project-based demand cycles and cost optimization priorities. A non-obvious impact is the rise of third-party testing providers capturing recurring revenue streams. In response, manufacturers are expanding service portfolios and building long-term contracts, redefining revenue models and customer engagement strategies.

The DC load bank market is segmented across types, applications, and end-users, with demand increasingly concentrating around high-efficiency and high-frequency testing environments. Resistive and modular systems dominate product demand due to their operational reliability, while applications such as battery testing and data center backup validation account for over 55% of total usage. End-user demand is led by data centers and power generation, together contributing nearly 60%, reflecting infrastructure-critical dependency. Demand is shifting toward flexible, scalable solutions as industries prioritize faster deployment and digital integration, forcing companies to realign product strategies and target high-growth segments with precision-engineered offerings.

Resistive DC load banks dominate the market with approximately 36% share, driven by their simplicity, cost efficiency, and high reliability in continuous testing environments. Their structural advantage lies in low maintenance requirements and consistent performance across power validation scenarios. However, modular load banks are the fastest-growing segment, expanding at over 24% adoption growth, as industries prioritize scalability and faster deployment. Compared to stationary systems, modular solutions reduce installation time by 20% and improve flexibility in dynamic testing environments. Regenerative load banks are gaining traction, particularly in energy-conscious sectors, offering up to 15% energy recovery, though their higher upfront costs limit widespread adoption. Portable and stationary systems together account for nearly 40% share, serving niche applications where mobility or fixed high-capacity infrastructure is required. Companies are increasingly shifting product focus toward modular and regenerative technologies, investing in flexible designs and energy-efficient systems. This transition signals a clear investment direction toward scalable and sustainable load testing solutions.

Battery testing leads the application segment with approximately 31% share, reflecting the rapid expansion of energy storage and electric vehicle ecosystems. This dominance is driven by the need for precise performance validation and lifecycle testing. EV charging systems represent the fastest-growing application, with over 27% growth, fueled by accelerated charging infrastructure deployment and regulatory mandates for electrification. In comparison, data center backup testing remains a mature segment, contributing around 24%, where demand is stable but increasingly shifting toward automated testing systems. Power supply testing and renewable energy systems together account for nearly 45% share, supporting industrial and grid-scale applications. Usage patterns are evolving toward integrated and continuous testing environments, pushing companies to deploy advanced, automated load banks across critical operations. Businesses are repositioning their offerings to align with high-growth segments like EV and battery testing, ensuring competitive alignment with electrification trends.

Data centers dominate the end-user segment with approximately 34% share, driven by high uptime requirements and continuous backup validation needs. Their demand concentration stems from increasing hyperscale infrastructure and the critical need for reliability. The automotive industry is the fastest-growing segment, expanding by over 26%, fueled by EV manufacturing and battery testing requirements. In contrast, the power generation industry represents a stable and established segment with around 28% share, focused on grid reliability and energy transition projects. Telecom and industrial facilities together account for nearly 38%, with steady adoption driven by infrastructure expansion and operational testing needs. Buying behavior is shifting toward customized and scalable solutions, with companies offering tailored load bank systems and flexible pricing models. Strategic partnerships with data center operators and EV manufacturers are becoming central to capturing future demand, as businesses align with high-growth, technology-driven sectors.

Asia Pacific accounted for the largest market share at 38% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 6.4% between 2026 and 2033.

Asia Pacific leads in volume due to large-scale manufacturing and energy infrastructure expansion, while North America drives innovation with over 44% adoption of advanced automated load testing systems. Europe holds nearly 22% share, supported by strong regulatory alignment and renewable integration. Demand is concentrated in Asia due to cost-efficient production, while growth is accelerating in North America through data center expansion and digital testing adoption. A key structural shift is the localization of supply chains, reshaping procurement strategies. Companies are prioritizing Asia for scale and North America for high-value innovation-driven deployments.

How is advanced infrastructure testing reshaping competitive positioning?

North America holds approximately 29% of global demand, driven by hyperscale data centers and energy storage validation needs. Data center infrastructure alone contributes over 42% of regional demand, reflecting high uptime dependency. A key structural force is federal energy resilience initiatives, accelerating adoption of high-efficiency testing systems. Execution is shifting toward AI-enabled load banks, with adoption increasing by 37%, improving operational accuracy by 18%. Companies are expanding capacity, with several operators increasing testing infrastructure investments by over 22%. Enterprises prefer automated, high-performance systems to reduce downtime risks. This region is being prioritized for premium, innovation-led deployments, making it critical for technology-driven market leadership.

What role do compliance and sustainability mandates play in shaping demand?

Europe accounts for nearly 22% of the global market, led by Germany, the UK, and France. Demand is strongly influenced by stringent emission and efficiency regulations, pushing adoption of energy-efficient load banks that reduce energy loss by up to 14%. ESG compliance is forcing operational upgrades, with over 39% of enterprises integrating sustainable testing solutions. Companies are shifting toward regenerative load banks, improving energy recovery rates by 12–15%. A measurable trend includes a 19% increase in automated testing deployments across renewable projects. Enterprises prioritize compliance-driven, high-quality systems, even at higher costs. This region compels manufacturers to innovate around sustainability and efficiency to remain competitive.

Why is large-scale deployment accelerating at unmatched speed?

Asia Pacific leads the market with 38% share, driven by China, India, and Japan. The region benefits from strong manufacturing ecosystems and rapid infrastructure expansion, contributing to over 45% of global production capacity. Execution is shifting toward mass deployment, with adoption rates increasing by 28% across energy storage and industrial sectors. Localized production has reduced system costs by 17%, enabling faster scalability. Companies are expanding regional manufacturing footprints, with capacity increases exceeding 25% in key markets. Enterprises prioritize cost efficiency and deployment speed, favoring modular systems. This region remains critical for scaling operations and capturing high-volume demand.

What factors are shaping emerging demand despite structural constraints?

South America contributes approximately 6% of the global market, with Brazil and Chile leading demand due to renewable energy expansion. Infrastructure development in power generation accounts for over 48% of regional demand. However, cost constraints and limited access to advanced components increase system costs by 13–16%, restricting large-scale adoption. Execution is shifting toward localized demand growth, with adoption increasing by 21% in mid-scale projects. Companies are forming regional partnerships and investing in localized assembly to reduce costs. Enterprises exhibit high price sensitivity, prioritizing cost-effective solutions over advanced features. This region presents a balanced mix of growth opportunity and operational risk.

How are infrastructure investments transforming testing requirements?

The Middle East & Africa region accounts for nearly 5% of global demand, led by the UAE, Saudi Arabia, and South Africa. Demand is heavily driven by oil and gas, construction, and large-scale infrastructure projects, contributing over 52% of regional usage. A key transformation driver is government-led investment in energy diversification, increasing adoption of advanced testing systems by 24%. Execution is shifting toward high-capacity deployments, particularly in utility-scale projects. Companies are investing in regional partnerships, with project deployments increasing by 18%. Enterprises focus on reliability and durability in extreme conditions. This region is emerging as a strategic market for infrastructure-driven expansion.

China – 34% market share: Dominates the DC Load Bank Market due to large-scale manufacturing capacity and strong demand from energy storage and industrial sectors

United States – 26% market share: Leads the DC Load Bank Market with high demand from data centers and advanced infrastructure testing requirements

The DC load bank market is defined by competition between global engineering leaders, regional manufacturers, and emerging technology-focused players. Established companies such as Crestchic, Aggreko, and ASCO Power Technologies compete directly with regional cost-focused manufacturers, while innovation-driven firms are differentiating through digital integration and automation. The top five players collectively hold approximately 52% market share, reflecting moderate consolidation with strong competitive intensity.

Competition is primarily based on technology advancement, pricing efficiency, and deployment speed. Advanced digital load banks improve operational efficiency by over 20%, while modular systems reduce installation time by 18%, creating a clear performance gap between premium and low-cost offerings. Companies are actively expanding through regional manufacturing, strategic partnerships, and product innovation, with capacity expansions exceeding 20% in high-growth regions. A key competitive shift is the move toward AI-enabled and service-based solutions, redefining value delivery.

Entry barriers remain high due to technical complexity, certification requirements, and capital-intensive manufacturing. Winning in this market requires strong engineering capabilities, scalable production, and the ability to deliver integrated, high-performance testing solutions.

Crestchic Loadbanks

Aggreko plc

ASCO Power Technologies

Simplex, Inc.

Eagle Eye Power Solutions

Hillstone Load Banks

Powerohm Resistors

Tatsumi Ryoki Co., Ltd.

Metal Deploye Resistor Ltd.

Rentaload

Avtron Power Solutions

Load Banks Direct

Greenlight Innovation Corp.

Digital and IoT-enabled DC load banks are now central to operational control, with over 58% of new systems integrating real-time monitoring and remote diagnostics. These technologies improve fault detection accuracy by 22% and reduce maintenance response time by 18%, directly enhancing uptime in data centers and energy storage systems. Integration with cloud platforms is reshaping testing workflows, enabling continuous performance validation and data-driven decision-making.

Emerging technologies such as AI-driven load simulation and modular architectures are accelerating efficiency gains. AI-based systems optimize load distribution, improving testing precision by 24%, while modular designs reduce deployment time by 20%. Adoption of these advanced systems has crossed 41% in high-density infrastructure projects, reflecting a shift toward flexible and scalable testing environments. This transition is enabling faster commissioning cycles and reducing operational bottlenecks across critical industries.

A key comparison highlights that AI-integrated load banks improve efficiency by 24% while reducing operational costs by 18% compared to legacy resistive systems. Regenerative load banks are also gaining traction, offering energy recovery benefits of up to 15%, particularly in sustainability-focused markets. Between 2026 and 2028, these technologies are expected to redefine performance benchmarks, with predictive analytics becoming standard across over 50% of deployments.

The competitive advantage is increasingly shifting toward companies that combine digital intelligence with scalable hardware. Technology leaders benefit from higher-margin contracts and long-term service models, while traditional manufacturers risk losing relevance unless they accelerate innovation and integration capabilities.

March 2026 – Aggreko plc: Launched a high-capacity modular DC load bank platform with 30% faster deployment capability, targeting data center and energy storage validation projects. This innovation improves commissioning speed and reduces operational delays, strengthening Aggreko’s position in high-demand infrastructure markets. [Modular Expansion] Source: https://www.aggreko.com

November 2025 – Crestchic Loadbanks: Expanded manufacturing capacity by 25% in response to rising global demand, enabling faster delivery cycles for large-scale energy and industrial projects. The move enhances supply chain resilience and supports growing demand for customized load testing solutions. [Capacity Boost] Source: https://www.crestchicloadbanks.com

July 2025 – ASCO Power Technologies: Introduced advanced digital load bank controls improving testing accuracy by 20%, focusing on mission-critical power systems. This development strengthens automation capabilities and supports enterprise demand for precision-driven performance validation. [Digital Upgrade] Source: https://www.ascopower.com

February 2024 – Avtron Power Solutions: Partnered with a data center operator to deploy load banks across multiple facilities, improving system reliability by 18%. This collaboration highlights the increasing role of load testing in ensuring uptime and operational continuity. [Strategic Partnership] Source: https://www.avtronpower.com

The DC load bank market report delivers comprehensive coverage across key segments, including types such as resistive, regenerative, modular, portable, and stationary systems, alongside applications spanning battery testing, data center backup validation, renewable energy systems, power supply testing, and EV charging infrastructure. It evaluates demand across five major regions and multiple country-level markets, capturing over 90% of global deployment activity. The report also integrates analysis of core technologies, including AI-enabled load simulation, IoT-based monitoring, and modular system architectures, reflecting current adoption levels exceeding 40% in advanced infrastructure environments.

Analytical depth is reinforced through segmentation-level insights, with over 15 distinct market categories assessed and more than 12 key companies profiled for competitive positioning. The report highlights adoption trends, such as over 58% usage of digital monitoring systems and 33% shift toward modular deployments, offering clear indicators of operational transformation. It also examines niche areas like regenerative load systems and containerized solutions, which are gaining traction due to efficiency and scalability advantages.

Strategically, the report supports decision-making by identifying high-growth segments, regional expansion opportunities, and technology investment priorities for the 2026–2033 period. It enables stakeholders to optimize capital allocation, strengthen competitive positioning, and align with evolving infrastructure and energy transition trends.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 1480 Million |

|

Market Revenue in 2033 |

USD 2355.33 Million |

|

CAGR (2026 - 2033) |

5.98% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Crestchic Loadbanks, Aggreko plc, ASCO Power Technologies, Simplex, Inc., Eagle Eye Power Solutions, Hillstone Load Banks, Powerohm Resistors, Tatsumi Ryoki Co., Ltd., Metal Deploye Resistor Ltd., Rentaload, Avtron Power Solutions, Load Banks Direct, Greenlight Innovation Corp. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |