Reports

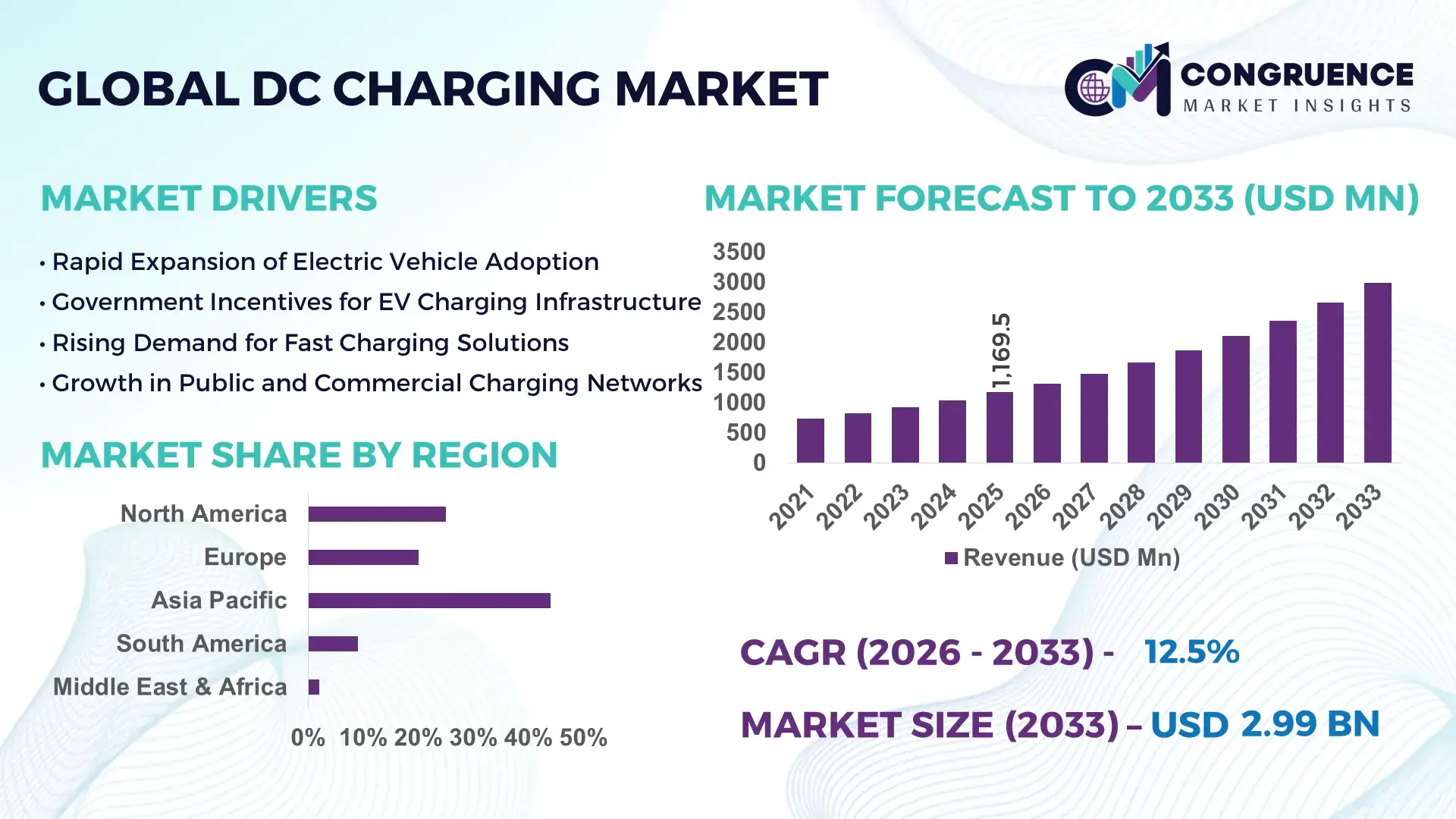

The Global DC Charging Market was valued at USD 1169.48 Million in 2025 and is anticipated to reach a value of USD 2989.98 Million by 2033 expanding at a CAGR of 12.45% between 2026 and 2033. This growth is primarily driven by the rapid expansion of electric vehicle (EV) infrastructure and increasing demand for ultra-fast charging solutions.

China continues to demonstrate strong industrial leadership in the DC charging market through large-scale infrastructure deployment and advanced manufacturing capabilities. The country has installed over 1.8 million public charging points, with a significant portion dedicated to high-power DC fast charging systems exceeding 120 kW capacity. Investments in EV charging infrastructure surpassed USD 15 billion in recent years, with extensive deployment across highways and urban centers. DC charging systems are widely used in commercial fleets, public transportation, and logistics hubs. Additionally, Chinese manufacturers are advancing ultra-fast charging technologies capable of delivering 300–480 kW output, significantly reducing charging time to under 20 minutes for compatible vehicles. The integration of smart grid connectivity and AI-based energy management systems further enhances operational efficiency.

Market Size & Growth: USD 1169.48 Million in 2025, projected to reach USD 2989.98 Million by 2033 at 12.45% CAGR, driven by EV adoption acceleration and fast-charging demand.

Top Growth Drivers: EV adoption growth at 35%, charging time reduction efficiency at 40%, and renewable integration at 28%.

Short-Term Forecast: By 2028, charging infrastructure efficiency is expected to improve by 25% with reduced operational costs by 18%.

Emerging Technologies: Ultra-fast DC chargers (350 kW+), vehicle-to-grid (V2G) integration, and AI-enabled smart charging networks.

Regional Leaders: Asia-Pacific projected at USD 1400 Million by 2033 with dense urban deployment; Europe at USD 900 Million driven by sustainability mandates; North America at USD 689 Million with highway corridor expansion.

Consumer/End-User Trends: Rising adoption among fleet operators, ride-sharing services, and commercial logistics sectors with high utilization rates exceeding 60%.

Pilot or Case Example: In 2024, a European charging network project improved uptime by 30% and reduced energy losses by 15% using AI optimization.

Competitive Landscape: Market leader holds approximately 22% share, followed by key players such as ABB, Siemens, Tesla, Schneider Electric, and Delta Electronics.

Regulatory & ESG Impact: Governments targeting 50% emission reduction by 2030 are mandating EV charging expansion and renewable energy integration.

Investment & Funding Patterns: Over USD 25 billion invested globally in EV charging infrastructure, with rising public-private partnerships.

Innovation & Future Outlook: Integration of energy storage, smart grids, and modular charging stations expected to redefine infrastructure scalability.

The DC charging market is witnessing diversified growth across automotive, public infrastructure, and commercial fleet sectors, with passenger EVs contributing over 45% of charging demand and logistics fleets accounting for nearly 30%. Technological advancements such as liquid-cooled charging cables and high-efficiency power modules are improving system performance and reducing energy loss by up to 12%. Regulatory frameworks promoting zero-emission transportation and incentives for EV infrastructure deployment are accelerating adoption globally. Regional consumption patterns indicate higher urban demand, while highway corridor installations are expanding rapidly. Emerging trends include battery-swapping compatibility, integration with renewable energy systems, and deployment of megawatt charging systems for heavy-duty vehicles, positioning the market for long-term scalable growth.

The DC Charging Market is strategically positioned at the core of the global energy transition and electric mobility ecosystem, enabling faster energy delivery and supporting high-performance EV operations. Businesses are increasingly aligning infrastructure investments with long-term electrification goals, as DC fast charging significantly reduces vehicle downtime and enhances operational efficiency. Ultra-fast charging technology delivers up to 60% improvement in charging speed compared to conventional Level 2 AC charging systems, making it critical for commercial fleet utilization and long-distance travel networks.

Asia-Pacific dominates in volume due to large-scale infrastructure deployment, while Europe leads in adoption with over 65% of enterprises integrating DC fast charging solutions into fleet operations. The rapid digitalization of charging infrastructure, including AI-based load management and predictive maintenance, is transforming operational strategies. By 2028, AI-driven smart charging systems are expected to improve grid efficiency by 30% and reduce peak load stress by 20%, enabling more sustainable energy consumption patterns.

Companies are also focusing on ESG compliance, committing to carbon neutrality targets such as 40% emission reduction in charging operations by 2030 through renewable energy integration and energy-efficient systems. In 2024, a leading automotive manufacturer in Germany achieved a 25% reduction in charging time and 18% improvement in energy utilization through deployment of high-power DC charging stations integrated with battery storage systems. Strategically, the DC Charging Market is evolving toward modular, scalable, and interoperable solutions, supporting cross-border charging networks and smart city initiatives. As infrastructure investments intensify and technological innovation accelerates, the DC Charging Market is emerging as a foundational pillar for resilient, compliant, and sustainable transportation ecosystems.

The exponential rise in electric vehicle adoption is a primary driver of the DC Charging Market, as faster charging solutions are essential to support growing vehicle fleets. Global EV sales have surpassed 14 million units annually, creating significant demand for high-speed charging infrastructure. DC fast chargers, capable of delivering up to 80% charge in under 30 minutes, are increasingly deployed in urban areas and highway corridors. Commercial fleet operators, including logistics and ride-hailing services, rely heavily on DC charging to minimize downtime and maximize operational efficiency. Additionally, government incentives and subsidies are accelerating EV purchases, indirectly boosting demand for fast-charging networks. The expansion of charging stations in densely populated regions and along transportation routes further supports widespread adoption and infrastructure scalability.

High capital expenditure associated with DC charging infrastructure remains a significant barrier to market expansion. Installation costs for a single high-power DC fast charger can exceed USD 50,000, excluding grid connection and land acquisition expenses. Upgrading electrical infrastructure to support high-load charging stations often requires substantial investment in transformers and grid reinforcement. In rural and low-demand areas, return on investment is slower due to lower utilization rates. Additionally, operational costs related to maintenance, energy consumption, and software integration add to financial challenges. These cost constraints limit widespread deployment, particularly for small and medium enterprises, and create disparities in charging infrastructure availability across regions.

The integration of renewable energy sources such as solar and wind power presents significant growth opportunities for the DC Charging Market. Charging stations equipped with on-site renewable generation and battery storage systems can reduce dependence on grid electricity and lower operational costs. Solar-powered DC charging hubs are gaining traction, particularly in regions with high solar irradiance, enabling sustainable and cost-efficient energy supply. Energy storage systems enhance load balancing and allow operators to manage peak demand effectively. Additionally, vehicle-to-grid (V2G) technology enables EVs to act as distributed energy resources, contributing to grid stability. These advancements support sustainability goals and create new revenue streams through energy trading and demand response programs.

Grid capacity constraints and lack of standardization pose critical challenges to the expansion of the DC Charging Market. High-power DC chargers require substantial electrical load, which can strain existing grid infrastructure, especially in urban areas with high demand. In many regions, grid upgrades are necessary to accommodate increasing charging loads, leading to delays in deployment. Additionally, the absence of universal charging standards and compatibility issues between different vehicle models and charging systems create operational inefficiencies. Interoperability challenges limit seamless user experience and hinder network scalability. Addressing these issues requires coordinated efforts between governments, utilities, and industry stakeholders to develop standardized protocols and invest in grid modernization initiatives.

• Ultra-Fast Charging Infrastructure Expansion Above 300 kW: Deployment of ultra-fast DC charging systems exceeding 300 kW capacity is accelerating across key regions, with over 35% of newly installed public charging stations now supporting high-power output. These systems reduce charging time by nearly 50% compared to 150 kW chargers, enabling EVs to achieve 80% charge in under 20 minutes. Adoption is particularly strong along highway corridors, where utilization rates exceed 65%, supporting long-distance electric mobility and commercial fleet efficiency.

• Integration of AI-Based Smart Charging Networks Improving Efficiency by 30%: AI-enabled energy management systems are transforming charging infrastructure by optimizing load distribution and reducing peak demand by up to 30%. Approximately 45% of newly deployed DC charging stations are integrated with IoT and predictive analytics platforms, enabling real-time monitoring and fault detection. This has resulted in a 25% reduction in downtime and a 20% improvement in energy utilization efficiency, enhancing overall network reliability.

• Growth in Renewable-Integrated Charging Stations with 40% Energy Contribution: Renewable energy integration is becoming a key trend, with nearly 40% of new DC charging hubs incorporating solar or wind energy sources. Hybrid systems combining battery storage and renewable generation reduce grid dependency by up to 35% and lower operational costs by approximately 18%. This trend aligns with sustainability targets, particularly in Europe and Asia-Pacific, where green energy mandates are driving infrastructure transformation.

• Expansion of Megawatt Charging Systems for Commercial EV Fleets: Megawatt-level DC charging systems (above 1 MW) are emerging to support heavy-duty electric trucks and buses, with pilot deployments increasing by 28% year-over-year. These systems enable charging times under 30 minutes for large battery capacities exceeding 500 kWh. Fleet operators report up to 40% improvement in operational efficiency and a 22% reduction in fleet downtime, making high-capacity charging critical for logistics and industrial transport electrification.

The DC Charging Market is segmented based on type, application, and end-user, reflecting diverse deployment scenarios and technological advancements. By type, the market includes low-power, medium-power, and high-power DC chargers, each catering to different charging requirements and infrastructure capabilities. Application-wise segmentation spans public charging infrastructure, commercial fleet charging, and residential or private installations, with public networks accounting for a substantial portion of deployments. End-user segmentation highlights automotive OEMs, charging network operators, fleet operators, and government bodies, each contributing to infrastructure expansion and adoption. The increasing penetration of electric vehicles and supportive policy frameworks are influencing segmentation dynamics, with high-power chargers and public infrastructure witnessing accelerated adoption. Additionally, advancements in charging technologies and integration with renewable energy systems are shaping demand patterns across all segments.

The DC Charging Market by type is categorized into low-power DC chargers (below 50 kW), medium-power chargers (50 kW–150 kW), and high-power DC fast chargers (above 150 kW). High-power DC chargers dominate the segment, accounting for approximately 48% of total installations due to their ability to deliver rapid charging, reducing downtime significantly for both passenger and commercial vehicles. Medium-power chargers hold around 32% share, widely used in urban public charging stations where moderate charging speed balances cost and efficiency. Low-power DC chargers contribute the remaining 20%, primarily serving niche applications such as residential complexes and small commercial setups.

High-power DC chargers are also the fastest-growing segment, expanding at an estimated growth rate of over 15% annually, driven by increasing demand for ultra-fast charging solutions and long-distance EV travel requirements. The shift toward 350 kW and above charging systems is further accelerating adoption, particularly in highway corridors and logistics hubs. Meanwhile, medium and low-power chargers maintain steady demand due to cost-effectiveness and suitability for localized applications.

The DC Charging Market by application includes public charging infrastructure, commercial fleet charging, and private or semi-private charging installations. Public charging infrastructure leads the segment with approximately 52% share, driven by increasing government initiatives and the need for accessible charging networks in urban and intercity locations. Commercial fleet charging accounts for nearly 30% of the market, supported by rapid electrification of logistics, ride-hailing, and public transport sectors. Private and semi-private installations contribute the remaining 18%, typically used in corporate campuses and residential complexes.

Commercial fleet charging is the fastest-growing application, expanding at an estimated rate of over 17% annually due to the rising adoption of electric delivery vehicles and buses. Fleet operators are increasingly investing in dedicated high-power charging stations to ensure operational efficiency and minimize downtime. Public infrastructure continues to expand steadily, particularly in regions with strong policy support and high EV penetration.

The DC Charging Market by end-user includes automotive OEMs, charging network operators, fleet operators, and government or public sector entities. Charging network operators represent the leading segment, accounting for approximately 40% of the market, as they play a central role in deploying and managing large-scale charging infrastructure. Fleet operators hold around 28% share, driven by increasing electrification of logistics and transportation services. Automotive OEMs contribute nearly 20%, integrating charging solutions into their EV ecosystems, while government and public sector entities account for the remaining 12%, focusing on infrastructure development and policy implementation.

Fleet operators are the fastest-growing end-user segment, with an estimated growth rate exceeding 18% annually, fueled by the need for efficient, high-capacity charging solutions to support commercial vehicle operations. Charging network operators continue to expand their footprint through strategic partnerships and investments, while OEMs are increasingly offering bundled charging solutions to enhance customer experience.

Region Asia-Pacific accounted for the largest market share at 46% in 2025 however, Europe is expected to register the fastest growth, expanding at a CAGR of 13.8% between 2026 and 2033.

Asia-Pacific leads with over 1.8 million installed charging points, including more than 600,000 DC fast chargers, driven by strong infrastructure expansion in China, Japan, and India. Europe follows with approximately 28% share, supported by over 500,000 public charging stations and aggressive sustainability mandates. North America holds around 18% share, with more than 140,000 DC fast chargers deployed across the U.S. and Canada. South America contributes nearly 5%, while the Middle East & Africa account for approximately 3%, reflecting emerging infrastructure investments. Urban regions globally account for over 65% of DC charging demand, while highway networks contribute nearly 25%, highlighting the importance of intercity mobility infrastructure.

How is high-speed EV infrastructure transforming charging accessibility and enterprise adoption?

North America holds approximately 18% share of the global DC Charging Market, supported by strong EV adoption and infrastructure investments. Key industries driving demand include automotive manufacturing, logistics, and ride-sharing services, with fleet electrification accounting for nearly 35% of total charging demand. Government initiatives such as federal tax credits and funding programs have enabled deployment of over 140,000 DC fast chargers, particularly along highway corridors. Technological advancements include integration of AI-driven load management systems and cloud-based monitoring platforms, improving charging efficiency by up to 25%. A leading regional player has expanded its ultra-fast charging network by installing over 10,000 high-power chargers, reducing average charging times by 40%. Consumer behavior reflects high adoption among commercial users, while residential users increasingly rely on public fast-charging infrastructure for long-distance travel.

What role do sustainability mandates and smart charging innovations play in shaping adoption trends?

Europe accounts for nearly 28% of the DC Charging Market, with key countries such as Germany, the UK, and France leading infrastructure deployment. The region benefits from strong regulatory frameworks, including carbon neutrality targets and EV incentives, driving installation of over 500,000 public charging stations. Sustainability initiatives and regulatory pressure have resulted in over 60% of new charging stations being powered partially by renewable energy. Emerging technologies such as vehicle-to-grid (V2G) systems and smart grid integration are widely adopted, improving energy efficiency by approximately 30%. A prominent European charging operator has deployed more than 5,000 ultra-fast chargers across major transport routes, enhancing accessibility and reducing charging time by 35%. Consumer behavior in the region is influenced by environmental awareness, with over 70% of EV users preferring green energy-powered charging solutions.

How are large-scale infrastructure deployments and manufacturing ecosystems accelerating market expansion?

Asia-Pacific dominates the DC Charging Market in terms of volume, with over 46% share and more than 600,000 DC fast chargers installed. China, India, and Japan are the top consuming countries, collectively accounting for over 80% of regional demand. The region benefits from strong manufacturing capabilities, producing more than 50% of global charging equipment. Infrastructure expansion is supported by government-led initiatives and investments exceeding USD 15 billion in EV charging networks. Technological innovation hubs are advancing ultra-fast charging systems exceeding 350 kW, reducing charging time by nearly 50%. A major regional player has deployed over 20,000 DC fast chargers across urban and highway networks, significantly improving accessibility. Consumer behavior is driven by high EV adoption rates and increasing reliance on public charging infrastructure, with utilization rates exceeding 60% in major metropolitan areas.

What infrastructure developments and policy incentives are driving emerging adoption trends?

South America accounts for approximately 5% of the global DC Charging Market, with Brazil and Argentina leading regional adoption. Infrastructure development is gradually expanding, with over 15,000 charging points installed, including a growing number of DC fast chargers in urban centers. The energy sector plays a critical role, with renewable energy contributing nearly 45% of electricity generation, supporting sustainable charging solutions. Government incentives, including tax reductions and import duty exemptions, are encouraging EV adoption and charging infrastructure deployment. A regional energy company has initiated deployment of over 1,000 DC fast chargers across major cities, improving accessibility and reducing charging time by 30%. Consumer behavior reflects growing awareness of electric mobility, with demand concentrated in metropolitan areas and commercial fleet operations.

How are energy diversification and smart infrastructure investments shaping future demand?

The Middle East & Africa region holds approximately 3% share of the DC Charging Market, with increasing investments in EV infrastructure and energy diversification. Key growth countries include the UAE and South Africa, where government initiatives are supporting deployment of charging networks. Demand is driven by sectors such as transportation, oil & gas, and construction, with EV adoption gradually increasing. Technological modernization includes smart charging systems and integration with renewable energy, improving efficiency by up to 20%. A leading regional utility has deployed over 500 DC fast chargers across urban and highway locations, enhancing network coverage. Regulatory frameworks and international partnerships are facilitating infrastructure development, while consumer behavior shows rising adoption among commercial users and urban populations seeking sustainable mobility solutions.

China – 38% share in the DC Charging Market, driven by large-scale infrastructure deployment and strong manufacturing capacity

United States – 16% share in the DC Charging Market, supported by high EV adoption and extensive highway charging networks

The DC Charging Market exhibits a moderately consolidated competitive structure, with the top five companies accounting for approximately 55% of the global market share. Over 120 active players operate across different segments, including hardware manufacturing, software solutions, and network operations. Leading companies are focusing on strategic partnerships, product innovation, and geographic expansion to strengthen their market position. For instance, several firms have introduced ultra-fast charging systems exceeding 350 kW, reducing charging time by up to 50% and enhancing user convenience.

Mergers and acquisitions are increasing, with more than 25 strategic deals recorded in recent years, enabling companies to expand their technological capabilities and market reach. Investment in R&D has risen by nearly 20%, focusing on advanced power electronics, energy storage integration, and AI-driven charging optimization. Competitive differentiation is increasingly driven by software capabilities, including real-time monitoring, predictive maintenance, and dynamic pricing models.

Additionally, collaborations between automotive OEMs and charging network providers are accelerating infrastructure deployment, with joint ventures contributing to over 30% of new installations. Companies are also investing in renewable energy integration and smart grid compatibility to align with sustainability goals. The market remains highly competitive, with innovation, scalability, and interoperability emerging as key factors influencing long-term success.

ABB

Siemens

Tesla

Schneider Electric

Delta Electronics

ChargePoint

EVBox

Blink Charging

Tritium

Alfen

Webasto

Eaton

The DC Charging Market is undergoing rapid technological transformation driven by advancements in power electronics, charging architecture, and digital energy management systems. High-power DC fast chargers ranging from 150 kW to 350 kW are now standard in highway and commercial applications, with emerging ultra-fast systems exceeding 500 kW capable of delivering 80% charge in under 15 minutes for next-generation EVs. These systems utilize silicon carbide (SiC) semiconductors, which improve power conversion efficiency by up to 98% and reduce energy losses by nearly 20% compared to traditional silicon-based components.

Liquid-cooled charging cables are increasingly deployed to handle high current loads above 500 A, reducing thermal stress and enabling compact charger designs. Modular charging architectures are gaining traction, allowing operators to scale capacity in increments of 30 kW to 60 kW modules, improving flexibility and reducing maintenance downtime by up to 25%. Integration with battery energy storage systems (BESS) is also expanding, enabling peak load shaving and reducing grid dependency by approximately 30%.

Digitalization is a key enabler, with over 50% of new DC charging stations incorporating IoT-enabled monitoring systems and AI-driven predictive maintenance tools. These technologies reduce equipment failure rates by nearly 35% and improve uptime to above 97%. Vehicle-to-grid (V2G) technology is emerging as a transformative innovation, allowing bidirectional energy flow and supporting grid stability. Additionally, interoperability standards such as CCS and CHAdeMO are evolving to support higher power levels and seamless cross-network charging. These technological advancements are positioning DC charging infrastructure as a critical component of smart energy ecosystems and next-generation mobility networks.

• In February 2025, ABB launched its next-generation Terra 360 DC fast charger with enhanced dynamic power distribution, capable of delivering up to 360 kW and charging four vehicles simultaneously. The system reduces average charging time by 30% while improving energy efficiency through advanced load balancing. Source: www.abb.com

• In October 2024, Siemens expanded its Sicharge D portfolio with upgraded high-power DC chargers supporting up to 400 kW output, incorporating IoT-enabled remote diagnostics and predictive maintenance features that improve uptime to over 98% and reduce operational interruptions significantly. Source: www.siemens.com

• In March 2025, Tesla increased deployment of its V4 Supercharger network, introducing charging speeds exceeding 350 kW and longer cable designs to accommodate a wider range of EV models, improving accessibility and reducing average charging session times by approximately 25%. Source: www.tesla.com

• In July 2024, Tritium introduced its PKM1500 DC fast charging platform featuring a modular design capable of scaling from 150 kW to 900 kW, enabling flexible infrastructure deployment and reducing installation time by nearly 20% through pre-configured power modules.

The DC Charging Market Report provides a comprehensive analysis of the global fast-charging ecosystem, covering key segments such as charger types, applications, technologies, and end-user industries. The report evaluates low-power (below 50 kW), medium-power (50–150 kW), and high-power (above 150 kW) DC charging systems, with detailed insights into their deployment across urban, highway, and commercial environments. It also examines application areas including public charging infrastructure, fleet charging networks, and private installations, highlighting utilization rates exceeding 60% in high-demand regions.

Geographically, the report spans major regions including Asia-Pacific, Europe, North America, South America, and the Middle East & Africa, analyzing infrastructure density, installation volumes, and regional consumption patterns. Asia-Pacific alone accounts for over 600,000 DC fast chargers, while Europe and North America collectively contribute more than 40% of global installations.

The scope further includes technological advancements such as ultra-fast charging systems exceeding 350 kW, integration with renewable energy sources contributing up to 40% of power supply in select regions, and adoption of AI-driven energy management systems improving operational efficiency by up to 30%. Additionally, the report explores emerging segments such as megawatt charging systems for heavy-duty vehicles and vehicle-to-grid (V2G) applications.

Industry focus areas include automotive OEMs, charging network operators, logistics fleets, and government agencies, with insights into deployment strategies, infrastructure investments, and regulatory frameworks. The report also highlights evolving business models such as subscription-based charging services and public-private partnerships, offering a holistic view of the DC Charging Market landscape for strategic decision-making.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

12.45% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

ABB, Siemens, Tesla, Schneider Electric, Delta Electronics, ChargePoint, EVBox, Blink Charging, Tritium, Alfen, Webasto, Eaton |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |