Reports

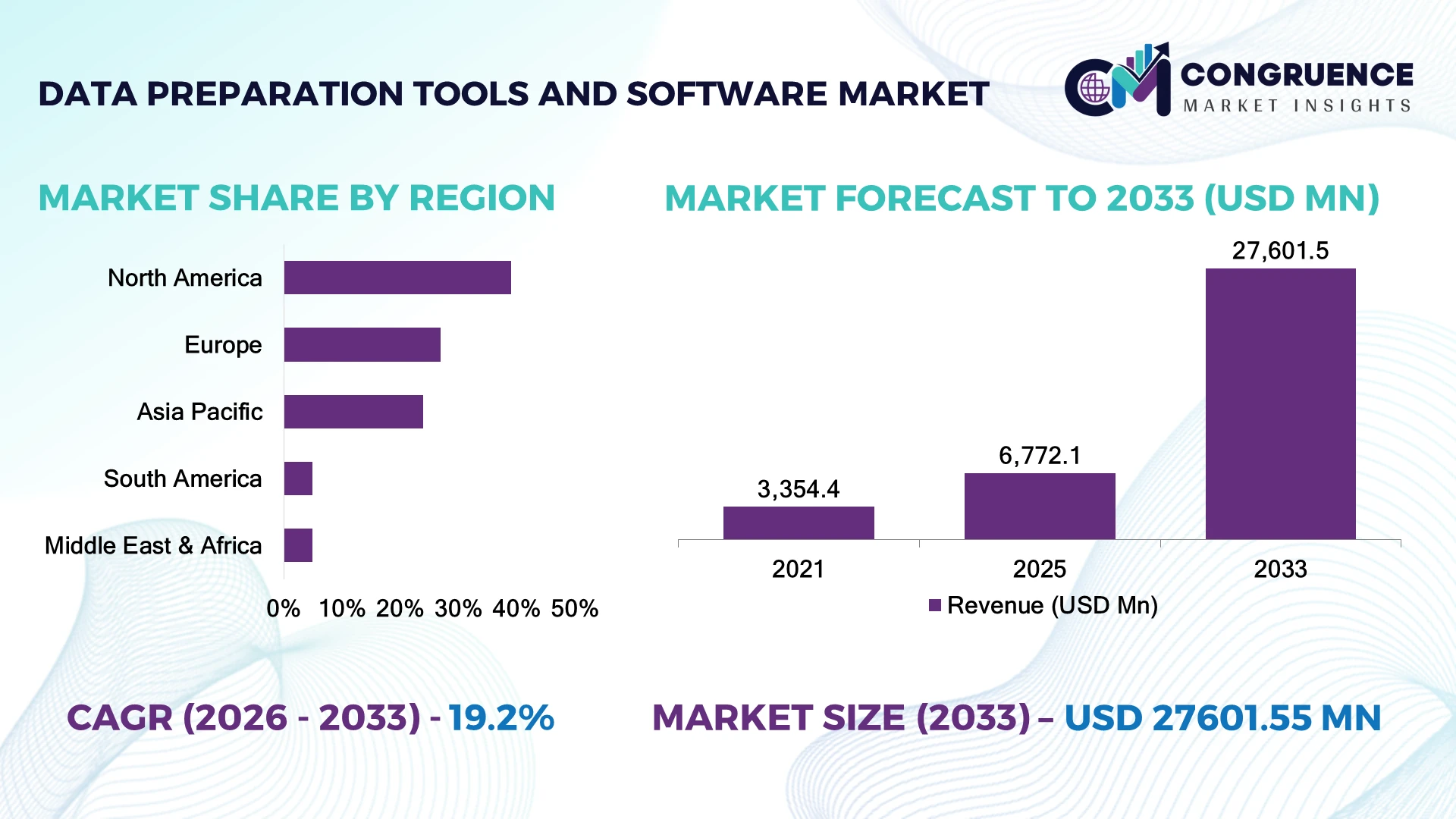

The Global Data Preparation Tools and Software Market was valued at USD 6,772.1 Million in 2025 and is anticipated to reach a value of USD 27,601.5 Million by 2033 expanding at a CAGR of 19.2% between 2026 and 2033. Growing enterprise AI deployments, expanding data governance mandates, and increasing demand for automated data quality management are accelerating adoption of advanced data preparation tools across analytics-driven industries.

The United States leads the global market with approximately 36% share, supported by hyperscale cloud infrastructure, AI investments exceeding USD 90 billion annually, and widespread enterprise analytics adoption across finance, healthcare, and retail. More than 74% of large enterprises have implemented self-service data preparation capabilities, compared with approximately 59% in Germany. Ongoing digital sovereignty initiatives and evolving global AI governance frameworks are further strengthening investment in secure enterprise data platforms.

Organizations investing in AI-enabled, governance-ready data preparation ecosystems are positioned to achieve faster analytics deployment, stronger compliance, and superior competitive agility.

Market Size & Growth: USD 6,772.1 million in 2025 to USD 27,601.5 million by 2033 at 19.2%, driven by enterprise AI adoption.

Top Growth Drivers: AI integration 46%, cloud migration 41%, regulatory compliance initiatives 37%.

Short-Term Forecast: By 2028, data preparation time declines by nearly 45% through automation.

Emerging Technologies: Generative AI, automated data lineage, and intelligent metadata management accelerate workflows.

Regional Leaders: North America leads; Asia-Pacific expands fastest; Europe strengthens governed cloud adoption.

Consumer/End-User Trends: Around 71% of analytics teams prioritize self-service data preparation platforms.

Pilot/Case Example: 2026 enterprise rollout reduced manual data cleansing effort by approximately 52%.

Competitive Landscape: Top five vendors hold nearly 49% share through AI-enabled enterprise platforms.

Regulatory & ESG Impact: Governance automation improves audit readiness by approximately 34% under stricter AI regulations.

Investment & Funding: Enterprise software investment exceeds USD 4.8 billion through cloud and AI partnerships.

Innovation & Future Outlook: Agentic AI and semantic data engineering strengthen enterprise decision intelligence.

Data Preparation Tools and Software solutions are becoming essential for enterprise AI, business intelligence, regulatory reporting, and cloud-native analytics. AI-assisted data profiling and automated transformation now reduce preparation workloads by approximately 48%, while metadata-driven governance improves operational consistency. Growing emphasis on sovereign cloud deployments and enterprise data governance is accelerating platform modernization, establishing the foundation for the strategic developments discussed below.

Data preparation has evolved into a strategic enterprise capability as organizations increasingly depend on trusted, AI-ready datasets to accelerate analytics, automation, and digital decision-making. Competitive advantage now depends on reducing data engineering bottlenecks while maintaining governance, lineage, and regulatory compliance. Enterprise adoption is also being reinforced by expanding AI governance frameworks and cross-border data sovereignty requirements, encouraging organizations to modernize their information management architecture.

AI-powered data preparation platforms now complete profiling, cleansing, and transformation approximately 58% faster than conventional rule-based workflows while reducing manual intervention by nearly 46%. North America continues leading enterprise-scale deployments through mature cloud ecosystems, whereas Asia-Pacific is expanding rapidly as digital transformation investments accelerate across financial services, manufacturing, and telecommunications. More than 68% of new enterprise analytics initiatives are expected to incorporate automated data preparation capabilities within the next two to three years.

Large organizations are increasingly integrating data preparation software with data catalogs, AI development platforms, and cloud warehouses through strategic technology partnerships. Vendors are expanding low-code functionality, embedded governance, and intelligent automation to improve enterprise usability. Companies that combine scalable automation with secure data governance and interoperable architectures will establish stronger long-term competitive positioning in enterprise analytics ecosystems.

Enterprise AI adoption is rapidly increasing demand for automated data preparation platforms capable of handling large-scale, multi-source datasets. Approximately 73% of enterprise AI initiatives now require automated data profiling and transformation, while intelligent preparation tools reduce manual data engineering effort by nearly 48% and improve data quality by approximately 34%. The United States continues expanding enterprise AI infrastructure following strengthened federal AI governance initiatives, accelerating investment in governed data platforms. The resulting shift enables faster analytics deployment and higher model reliability. Software providers are responding through generative AI integration, strategic cloud partnerships, metadata automation, and expanded low-code capabilities, transforming data preparation into a strategic layer supporting enterprise-wide digital intelligence.

Complex regulatory requirements, fragmented enterprise architectures, and inconsistent data governance frameworks continue limiting seamless deployment of data preparation software. Around 46% of organizations still operate disconnected data environments, while interoperability challenges increase implementation effort by approximately 28% and compliance-related operational costs by nearly 19%. Germany's stringent enterprise data governance requirements under evolving European digital regulations increase validation and documentation workloads for multinational deployments. These structural limitations delay enterprise-scale integration and reduce operational efficiency. Vendors are mitigating risks through standardized metadata frameworks, API-first architectures, regional cloud deployments, and long-term technology partnerships that simplify governance while improving interoperability across hybrid enterprise environments.

Agentic AI and autonomous data engineering platforms are creating significant opportunities for next-generation data preparation software. Nearly 61% of enterprise analytics leaders plan to introduce AI-assisted workflow orchestration, while autonomous transformation engines improve preparation efficiency by approximately 37% compared with conventional automation. Singapore continues strengthening national AI infrastructure through enterprise digital innovation programs, encouraging adoption of intelligent data management platforms. Technology companies are increasing investment in semantic data modeling, AI copilots, and enterprise knowledge graphs while expanding ecosystem partnerships. A major strategic opportunity lies in delivering self-optimizing preparation platforms that continuously improve data quality without extensive manual rule creation.

Integrating data preparation platforms across hybrid cloud, on-premise, and multi-cloud environments remains a major execution challenge. Approximately 57% of enterprises maintain mixed data architectures, while integration complexity extends deployment timelines by nearly 24% and increases ongoing administration requirements by approximately 18%. Japan's manufacturing and financial sectors continue modernizing legacy information systems while preserving operational continuity, making platform interoperability increasingly critical. These challenges directly affect governance consistency, AI readiness, and long-term scalability. Vendors must strengthen open integration frameworks, standardized metadata exchange, cybersecurity architecture, and enterprise partnerships while expanding professional services to support sustainable digital transformation.

AI Copilots Transform Preparation Enterprise adoption of AI copilots has surpassed 58% for data engineering workflows, reducing manual transformation effort by approximately 46% and accelerating dataset readiness by nearly 39%. Organizations are embedding generative AI into preparation pipelines while vendors expand strategic partnerships with cloud providers to deliver governed, enterprise-scale automation.

Metadata Intelligence Expands Rapidly Intelligent metadata management is becoming central to enterprise analytics, with automated lineage improving governance accuracy by approximately 33% and reducing compliance verification time by nearly 29%. Tightening AI governance frameworks are encouraging software providers to strengthen catalog integration, semantic modeling, and automated policy enforcement across distributed data environments.

Cloud-Native Pipelines Accelerate Cloud-native preparation platforms now support approximately 64% of newly deployed enterprise analytics environments, lowering infrastructure management effort by nearly 31% while improving workload scalability by approximately 36%. Technology providers are restructuring product portfolios around containerized deployment, multi-cloud compatibility, and API-driven orchestration for operational flexibility.

Low-Code Analytics Matures Low-code data preparation environments have increased business user participation by approximately 41%, while collaborative workflow automation shortens project delivery cycles by nearly 27%. Software vendors are expanding visual development interfaces, enterprise governance controls, and integrated AI recommendations to strengthen self-service analytics without compromising security or operational consistency.

Cloud-based data preparation tools accounted for approximately 58% of the market in 2025, driven by superior scalability, lower infrastructure costs, seamless integration with cloud data warehouses, and enterprise-wide accessibility. Organizations increasingly favor cloud deployments because they simplify data ingestion, governance, and AI workflow integration across distributed business environments. Around 67% of new analytics implementations now prioritize cloud-native data architectures, while deployment time is reduced by nearly 35% compared with conventional infrastructure. Software vendors continue strengthening SaaS offerings through AI-assisted transformation, automated metadata management, and strategic cloud ecosystem partnerships.

On-premise platforms remain important for organizations with strict data residency and regulatory requirements, particularly in government and financial institutions. Hybrid deployments represent the fastest-growing segment as enterprises modernize legacy systems while maintaining operational continuity. Vendors are investing in intelligent orchestration, multi-cloud compatibility, and unified governance capabilities, reflecting a broader shift toward flexible deployment strategies that balance security, performance, and scalability while supporting enterprise AI initiatives.

According to Gartner's enterprise data management research published during 2025, hybrid data management architectures continue expanding as organizations prioritize governed data access across multi-cloud and on-premise environments while supporting enterprise AI initiatives.

Data integration held the largest share of approximately 34% in 2025, supported by rising enterprise demand for unified access to structured and unstructured data across ERP systems, cloud platforms, CRM applications, and external databases. The segment dominates because integrated datasets form the foundation for business intelligence, machine learning, and enterprise reporting. Nearly 72% of enterprise analytics projects now require multi-source data integration, while automated integration workflows reduce manual engineering effort by approximately 38%. Vendors continue expanding API connectivity, intelligent orchestration, and real-time synchronization capabilities.

Data cleansing and quality management is emerging as the fastest-growing application due to increasing AI adoption and stricter governance requirements. Data transformation remains essential for analytics modernization, while data enrichment strengthens predictive modeling and customer intelligence initiatives. Companies are integrating automated profiling, anomaly detection, and semantic mapping into unified platforms, shifting investment priorities toward comprehensive data preparation environments that improve operational efficiency and analytical reliability.

According to findings released by the Data Management Association (DAMA) during 2025, organizations implementing standardized data quality programs consistently achieve higher analytics accuracy and stronger enterprise-wide decision reliability.

The BFSI sector accounted for approximately 26% of the global market in 2025, reflecting extensive adoption of data preparation software for fraud detection, regulatory reporting, customer analytics, and AI-driven risk assessment. Financial institutions require highly governed and trusted datasets to support real-time decision-making and evolving compliance obligations. Around 74% of large banking organizations have automated core data preparation workflows, while AI-enabled preparation improves analytical accuracy by approximately 31%. Software providers continue enhancing governance frameworks, data lineage, and secure cloud capabilities designed specifically for regulated financial environments.

Healthcare is the fastest-growing end-user segment as hospitals, life sciences organizations, and digital health providers accelerate electronic health record integration, clinical analytics, and AI-assisted diagnostics. Retail, manufacturing, IT & telecommunications, and government organizations continue expanding adoption to strengthen operational intelligence and predictive decision-making. Vendors are responding through industry-specific solutions, vertical partnerships, and compliance-focused platform enhancements that improve enterprise usability and competitive differentiation.

According to an enterprise survey released by the International Data Corporation (IDC) during 2025, organizations implementing governed data preparation platforms reported faster AI model deployment and improved enterprise-wide data consistency across regulated industries.

North America accounted for the largest market share at 39.1% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 21.4% between 2026 and 2033.

Enterprise AI adoption strengthens governed data ecosystems

North America maintains its leadership through widespread enterprise cloud adoption, mature AI infrastructure, and strong investment in data governance platforms. Large organizations across financial services, healthcare, retail, and technology sectors continue modernizing analytics environments by integrating automated data preparation with cloud-native architectures. The region contributes approximately 39.1% of global demand, while nearly 72% of enterprise analytics deployments incorporate automated data preparation workflows. Expansion of hyperscale cloud infrastructure and enterprise AI partnerships is accelerating deployment of intelligent data engineering platforms. Vendors continue strengthening metadata management, low-code automation, and enterprise governance capabilities, positioning the region at the forefront of trusted AI-ready data ecosystems.

United States Market Outlook: The United States leads regional deployment through advanced cloud infrastructure, enterprise AI investment, and broad adoption of modern analytics platforms. More than 74% of large enterprises utilize automated data preparation capabilities within enterprise analytics environments. Strong technology ecosystems, expanding AI governance initiatives, and close collaboration between cloud providers and software vendors continue accelerating innovation in intelligent data management, enterprise automation, and governed self-service analytics.

Regulatory governance accelerates platform modernization

Europe continues expanding enterprise adoption through strong regulatory frameworks emphasizing trusted data governance, interoperability, and digital sovereignty. Financial institutions, manufacturers, and public-sector organizations increasingly deploy intelligent data preparation platforms to support AI initiatives while maintaining regulatory compliance. The region represents approximately 27% of the global market, with enterprise metadata governance adoption increasing by nearly 33% during large-scale modernization programs. Vendors are expanding sovereign cloud capabilities, automated lineage management, and secure multi-cloud integration to address evolving enterprise governance requirements while improving operational efficiency.

Germany Market Outlook: Germany remains the region's technology leader through advanced manufacturing digitization, industrial AI adoption, and enterprise software investment. Large manufacturers increasingly integrate automated data preparation into Industry 4.0 environments, enabling trusted analytics across production and supply chain operations. Strong enterprise demand for governed hybrid-cloud architectures continues driving investment in secure, interoperable data management platforms.

Cloud-first transformation accelerates enterprise deployment

Asia-Pacific is emerging as the fastest-expanding regional market, supported by rapid cloud migration, enterprise digitalization, and expanding AI adoption across banking, telecommunications, manufacturing, and e-commerce. The region accounts for approximately 24% of global demand, while cloud-native analytics deployments have increased by nearly 38% over recent years. Governments and enterprises continue investing in national AI infrastructure, hyperscale data centers, and digital economy initiatives that strengthen enterprise data management capabilities. Software providers are expanding regional cloud partnerships and localized AI-enabled platforms to capture accelerating enterprise demand.

China Market Outlook: China leads regional deployment through large-scale digital transformation, strong cloud infrastructure expansion, and rapid enterprise AI implementation. Major financial institutions, internet companies, and manufacturers continue investing in intelligent data engineering capabilities supporting predictive analytics and business automation. Growing deployment of domestic cloud platforms and enterprise AI ecosystems further strengthens demand for scalable data preparation software across large organizations.

Enterprise modernization expands analytics adoption

South America is witnessing increasing implementation of cloud-based data preparation software as organizations modernize business intelligence and digital operations. Banking, retail, and telecommunications sectors are leading enterprise deployments to improve customer analytics and operational visibility. The region contributes approximately 5% of the global market, while cloud-based analytics adoption has increased by nearly 29% among large enterprises. Although infrastructure disparities remain, growing investment in regional cloud services and enterprise software partnerships continues improving deployment capabilities and accelerating digital transformation initiatives.

Brazil Market Outlook: Brazil represents the region's largest enterprise software market, supported by expanding financial technology, digital banking, and retail analytics investments. Large enterprises continue replacing fragmented legacy data environments with governed cloud-based platforms supporting AI-driven decision-making. Strong enterprise demand for automation and regulatory compliance is encouraging software vendors to expand local partnerships and implementation capabilities.

Digital investment strengthens enterprise transformation

The Middle East & Africa market is advancing through government-led digital transformation strategies, expanding cloud infrastructure, and increasing enterprise technology investment. Financial services, public administration, energy, and telecommunications organizations are accelerating deployment of intelligent data management platforms to strengthen analytics and governance. The region accounts for approximately 4.9% of global demand, while enterprise cloud adoption has improved by nearly 31% across major digital economy initiatives. Technology providers continue expanding regional cloud infrastructure, AI partnerships, and localized enterprise services to support long-term modernization.

United Arab Emirates Market Outlook: The United Arab Emirates remains the region's leading technology hub through substantial investment in artificial intelligence, smart government initiatives, and cloud infrastructure. Enterprise organizations increasingly deploy advanced data preparation platforms supporting AI, predictive analytics, and digital public services. National digital transformation programs and international technology partnerships continue strengthening the country's position as a regional center for enterprise data innovation.

Enterprise software leaders including Informatica, Alteryx, Qlik (Talend), IBM, and SAS compete against cloud-native innovators such as Matillion, Dataiku, and Altair, while hyperscale ecosystem providers challenge independent platforms through integrated data engineering capabilities. The top five vendors collectively control approximately 48% of the global market. Competition centers on AI-assisted data preparation, cloud interoperability, governance, and automation, with automated workflow capabilities reducing manual preparation effort by nearly 55% and metadata-driven processing improving data quality by approximately 34%. Vendors increasingly compete through strategic cloud partnerships, acquisitions, embedded generative AI, and unified analytics platforms rather than pricing alone. The competitive landscape is shifting toward AI-native, end-to-end data engineering ecosystems with open architecture replacing isolated preparation tools. High enterprise switching costs, governance requirements, and legacy workflow migration remain significant entry barriers. Winning requires trusted AI, seamless multi-cloud integration, enterprise-grade governance, rapid deployment, and continuous automation innovation.

Informatica

Alteryx

Qlik

IBM

SAS Institute

Altair

Dataiku

Matillion

TIBCO Software

Oracle

Microsoft

SAP

Precisely

KNIME

Artificial intelligence is redefining modern data preparation through automated profiling, transformation recommendations, anomaly detection, and metadata intelligence. Approximately 68% of enterprise deployments now incorporate AI-assisted data preparation, while intelligent automation reduces manual cleansing time by nearly 52%. Low-code workflow orchestration, embedded data quality engines, and natural-language interfaces are enabling business users to prepare trusted datasets without extensive programming, improving operational agility across hybrid cloud environments.

Cloud-native architectures, DataOps pipelines, and metadata-driven automation are replacing traditional desktop-centric preparation environments. Modern AI-powered platforms deliver approximately 37% faster workflow execution than legacy rule-based systems while improving transformation accuracy by nearly 29%. More than 61% of new enterprise implementations emphasize open APIs, lakehouse integration, and real-time streaming support, enabling faster analytics delivery and governed collaboration across distributed data ecosystems. Organizations adopting these integrated technologies achieve stronger scalability, improved governance, and accelerated AI readiness compared with legacy standalone preparation software.

Between 2026 and 2028, generative AI copilots, semantic data layers, autonomous pipeline optimization, and agentic data engineering will reshape enterprise data operations. Technology providers investing in AI-native governance, cloud interoperability, and automated lineage management will gain competitive advantage as organizations prioritize trusted enterprise AI. Early adopters benefit through shorter deployment cycles, lower operational complexity, stronger regulatory compliance, and continuously optimized data preparation workflows supporting advanced analytics and intelligent business decision-making.

April 2025 Informatica introduced new AI-powered cloud integration and master data management capabilities featuring expanded CLAIRE AI functionality to accelerate enterprise pipeline development and improve developer productivity. The release strengthens AI-ready data preparation for enterprise-scale deployments. Source: Informatica

May 2025 Alteryx launched the unified Alteryx One platform, combining AI-powered analytics, low-code data preparation, governance, and cloud capabilities into a single environment, enabling significantly faster enterprise analytics orchestration and scalable workflow automation. Source: Alteryx

May 2025 Informatica expanded its collaboration with Microsoft by introducing native Microsoft Fabric integrations and CLAIRE Copilot capabilities, reducing trusted master data onboarding from weeks to minutes while accelerating enterprise analytics and AI deployment. Source: Informatica

July 2025 Gartner recognized continued enterprise demand for AI-enabled data preparation platforms, highlighting stronger adoption of cloud-native, governed, and self-service solutions as organizations standardized trusted data workflows across modern analytics environments.

The report delivers comprehensive analysis of the global Data Preparation Tools and Software Market across deployment models, enterprise sizes, applications, end users, and major geographic markets between 2026 and 2033. It evaluates cloud and on-premises platforms, AI-assisted automation, metadata management, data quality technologies, governance capabilities, and real-time integration trends while assessing adoption patterns across BFSI, healthcare, manufacturing, retail, IT, telecommunications, and public sector organizations. Regional assessments cover North America, Europe, Asia-Pacific, South America, and the Middle East & Africa with enterprise adoption, deployment intensity, and technology maturity insights.

The study benchmarks leading technology providers, competitive positioning, innovation strategies, ecosystem partnerships, and deployment expansion while examining automation adoption, cloud migration, and enterprise AI readiness. It supports investment prioritization, product strategy, digital transformation planning, vendor evaluation, competitive benchmarking, and long-term business expansion by identifying high-growth technology segments, evolving customer requirements, operational trends, and emerging opportunities shaping the future of intelligent data preparation platforms.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 6,772.1 Million |

|

Market Revenue in 2033 |

USD 27,601.5 Million |

|

CAGR (2026 - 2033) |

19.2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Informatica, Alteryx, Qlik, IBM, SAS Institute, Altair, Dataiku, Matillion, TIBCO Software, Oracle, Microsoft, SAP, Precisely, KNIME |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |