Reports

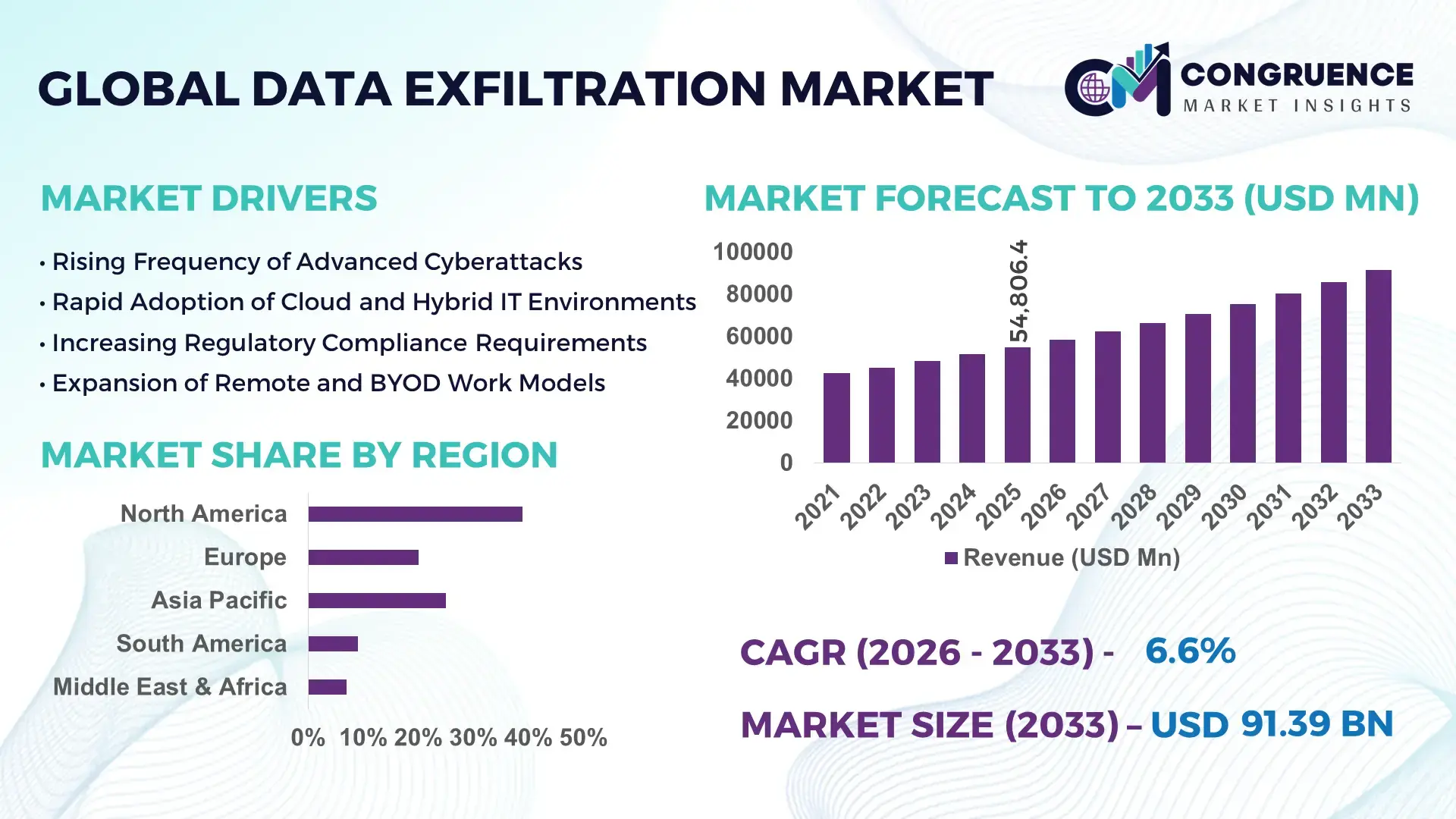

The Global Data Exfiltration Market was valued at USD 54806.44 Million in 2025 and is anticipated to reach a value of USD 91388.02 Million by 2033 expanding at a CAGR of 6.6% between 2026 and 2033. The growth is primarily driven by the rapid rise in sophisticated cyberattacks targeting sensitive enterprise and government data across cloud, endpoint, and hybrid network environments.

The United States represents the most advanced and technologically intensive market for data exfiltration prevention and detection solutions. In 2025, over 72% of large enterprises in the country deployed advanced data loss prevention (DLP) platforms integrated with AI-based anomaly detection tools. Annual enterprise cybersecurity investments in the U.S. exceeded USD 90 billion, with a significant allocation toward insider threat monitoring, encrypted traffic inspection, and zero-trust architecture deployment. Financial services, healthcare, and federal defense agencies account for more than 55% of enterprise-grade exfiltration prevention deployments. The country also leads in cloud-native security adoption, with over 65% of enterprises implementing secure access service edge (SASE) frameworks to monitor outbound data flows. Advanced SOC automation, behavioral analytics, and machine learning-based network monitoring systems continue to strengthen real-time data leakage detection across critical infrastructure and high-value digital ecosystems.

Market Size & Growth: Valued at USD 54,806.44 Million in 2025, projected to reach USD 91,388.02 Million by 2033 at 6.6% CAGR, fueled by rising ransomware incidents and cloud data exposure risks.

Top Growth Drivers: Cloud adoption expansion (68%), increase in insider threat incidents (52%), and regulatory compliance enforcement growth (47%).

Short-Term Forecast: By 2028, AI-powered data exfiltration detection tools are expected to reduce breach response time by 35% and operational costs by 22%.

Emerging Technologies: Zero Trust Architecture (ZTA), AI-driven behavioral analytics, Secure Access Service Edge (SASE), and advanced encryption monitoring platforms.

Regional Leaders: North America projected to exceed USD 34 Billion by 2033 with strong BFSI adoption; Europe expected above USD 24 Billion driven by strict compliance frameworks; Asia-Pacific anticipated to surpass USD 21 Billion with rapid digital transformation investments.

Consumer/End-User Trends: BFSI, healthcare, and IT services represent over 60% of solution deployments, prioritizing encrypted data monitoring and cloud-native DLP integration.

Pilot Example: In 2024, a multinational banking institution implemented AI-based outbound traffic monitoring, reducing unauthorized data transfers by 41% within 12 months.

Competitive Landscape: Broadcom leads with approximately 18% share, followed by IBM, Cisco, Palo Alto Networks, and McAfee in enterprise-grade data protection solutions.

Regulatory & ESG Impact: Compliance with GDPR, CCPA, and global data privacy mandates is accelerating secure data governance frameworks and encryption adoption.

Investment & Funding Patterns: Global cybersecurity venture investments exceeded USD 18 Billion in 2024, with a growing focus on AI-driven insider threat prevention startups.

Innovation & Future Outlook: Integration of generative AI threat modeling, quantum-resistant encryption research, and autonomous SOC automation platforms is shaping next-generation data exfiltration prevention strategies.

Across industry verticals, banking and financial services contribute nearly 28% of total enterprise spending on data exfiltration detection solutions, followed by healthcare at 19% and government and defense at 16%. Recent innovations include AI-powered user and entity behavior analytics (UEBA), encrypted traffic inspection without decryption, and API-level data flow monitoring in multi-cloud environments. Stringent global data protection laws, cross-border data transfer regulations, and rising digitalization in emerging economies are accelerating enterprise adoption. Asia-Pacific demonstrates the fastest consumption growth, driven by 60%+ cloud migration rates among mid-sized enterprises. The market outlook emphasizes proactive threat hunting, automated containment workflows, and integrated risk-based security orchestration to address complex cyber risk landscapes.

The Data Exfiltration Market holds strategic relevance as organizations transition toward hyper-connected digital ecosystems and cloud-first infrastructure models. With over 80% of enterprise workloads projected to operate in cloud or hybrid environments by 2027, safeguarding outbound data flows has become a board-level priority. AI-driven anomaly detection delivers 45% faster threat identification compared to signature-based legacy monitoring systems, enabling enterprises to minimize data leakage exposure and regulatory penalties. North America dominates in volume of enterprise deployments, while Asia-Pacific leads in adoption momentum with nearly 63% of large enterprises implementing next-generation data loss prevention tools in digitally transforming economies. By 2028, predictive AI-based behavioral analytics is expected to cut incident response time by 40% and reduce false positives by 30%, significantly improving SOC efficiency and cybersecurity ROI.

Firms are committing to ESG-linked cybersecurity governance metrics, targeting 25% reduction in data breach-related financial losses and integrating energy-efficient security infrastructure by 2029. In 2024, a leading U.S.-based financial institution achieved a 38% reduction in insider-driven data leak incidents through deployment of machine learning-powered user behavior analytics and encrypted traffic monitoring systems. Strategically, enterprises are embedding zero-trust frameworks, automated policy enforcement engines, and continuous risk scoring models into core IT architecture. The Data Exfiltration Market is evolving into a foundational pillar supporting digital resilience, regulatory compliance, secure cloud migration, and long-term sustainable growth across critical global industries.

The accelerated migration to cloud and hybrid infrastructures is a primary growth driver in the Data Exfiltration market. More than 80% of enterprise workloads are expected to operate in cloud environments by 2027, increasing exposure to data leakage risks through APIs, SaaS platforms, and remote endpoints. Cloud misconfigurations account for nearly 45% of data exposure incidents, prompting enterprises to implement advanced data loss prevention (DLP) and secure access service edge (SASE) solutions. Furthermore, remote and hybrid work models have expanded attack surfaces by over 30% compared to traditional on-premise setups. Organizations are deploying AI-driven behavioral analytics that improve detection accuracy by 40% compared to rule-based monitoring systems. In regulated sectors such as banking and healthcare, compliance mandates require continuous data flow visibility and encryption monitoring. As a result, enterprises are integrating automated threat response systems to reduce unauthorized data transfers and minimize compliance risks, directly stimulating sustained market demand.

Despite strong demand, implementation complexity remains a significant restraint in the Data Exfiltration market. Large-scale enterprises operate an average of 45 to 60 distinct security tools, making integration with new exfiltration detection platforms technically challenging. Legacy infrastructure incompatibility increases deployment timelines by up to 25%, particularly in highly regulated industries. Additionally, encrypted traffic inspection without compromising performance requires advanced hardware and software optimization. Decrypting and analyzing SSL/TLS traffic can increase network latency by 15–20% if not properly configured. Small and medium enterprises often face skill gaps, with nearly 3.5 million unfilled cybersecurity positions globally, limiting effective deployment and management of sophisticated DLP and UEBA systems. These operational and financial barriers slow adoption, especially among cost-sensitive organizations seeking scalable, cloud-native solutions.

Artificial intelligence and zero-trust security architectures present significant growth opportunities in the Data Exfiltration market. AI-powered user and entity behavior analytics (UEBA) systems can reduce false positives by up to 30% while improving anomaly detection rates by 45%. As enterprises transition from perimeter-based security to identity-centric models, zero-trust frameworks enable continuous authentication and granular data access controls. Global adoption of zero-trust strategies has surpassed 60% among large enterprises, opening opportunities for integrated exfiltration monitoring within identity and access management ecosystems. Cloud-native DLP solutions tailored for SaaS and Infrastructure-as-a-Service environments are also gaining traction, particularly in Asia-Pacific, where over 65% of mid-sized enterprises are accelerating digital transformation initiatives. Furthermore, the emergence of quantum-resistant encryption and automated security orchestration tools offers innovation-driven pathways for advanced data protection capabilities across critical infrastructure sectors.

The evolving sophistication of cyberattack techniques poses a persistent challenge to the Data Exfiltration market. Advanced persistent threats increasingly use encrypted channels, steganography, and covert DNS tunneling to bypass traditional monitoring systems. Nearly 60% of data exfiltration incidents involve compromised credentials rather than malware, complicating detection efforts. Regulatory fragmentation further intensifies compliance burdens for multinational enterprises. Organizations operating across multiple jurisdictions must comply with more than 100 distinct data protection and privacy regulations, increasing administrative overhead and governance complexity. Non-compliance penalties can reach up to 4% of global annual turnover in certain regions, pushing companies to invest heavily in audit-ready security infrastructures. Additionally, balancing privacy rights with deep packet inspection and behavioral monitoring creates operational tension, requiring carefully calibrated security architectures to maintain both compliance and performance efficiency.

• 42% Increase in AI-Based Behavioral Monitoring Deployment: Enterprises are rapidly integrating AI-driven anomaly detection into data exfiltration prevention frameworks. In 2025, approximately 68% of large organizations deployed machine learning-based user behavior analytics, up from 26% five years earlier. These platforms have reduced insider-related data leakage incidents by nearly 38% through continuous monitoring of over 10,000+ daily user activity logs in mid-sized enterprises.

• 57% Adoption of Zero-Trust Data Access Controls: Zero-trust architecture implementation has expanded across critical sectors, with 57% of global enterprises enforcing identity-based access controls for sensitive data repositories. Organizations adopting micro-segmentation policies reported a 33% decrease in unauthorized lateral movement within networks. Financial institutions processing more than 5 million daily transactions are prioritizing continuous authentication to secure outbound data flows.

• 49% Growth in Encrypted Traffic Inspection Solutions: With over 85% of global internet traffic now encrypted, enterprises are investing in high-performance SSL/TLS inspection tools capable of analyzing traffic at speeds exceeding 100 Gbps. Deployment of encrypted traffic analytics has improved detection rates of covert exfiltration attempts by 41%, particularly in sectors managing intellectual property and confidential health records.

• 36% Expansion in Cloud-Native Data Loss Prevention Tools: Cloud-native DLP platforms integrated into SaaS ecosystems have seen a 36% surge in enterprise adoption. More than 60% of organizations managing multi-cloud workloads now use API-level data flow monitoring, enabling automated quarantine of suspicious transfers within less than 5 seconds. This trend reflects the growing reliance on secure cloud migration strategies and real-time policy enforcement automation.

The Data Exfiltration market is segmented by type, application, and end-user, reflecting diverse deployment models and risk mitigation priorities across industries. By type, organizations adopt network-based, endpoint-based, and cloud-based data exfiltration prevention solutions to secure outbound traffic and sensitive data flows. Network-centric platforms remain foundational for monitoring high-volume data transfers across enterprise infrastructures, while cloud-native and endpoint-focused tools address distributed workforce and SaaS exposure risks.

By application, the market spans banking and financial services (BFSI), healthcare, government and defense, IT and telecom, retail, and manufacturing. BFSI and healthcare collectively account for over 45% of enterprise-grade deployments due to high-value transaction data and strict regulatory obligations. Government and defense sectors emphasize classified information security, while IT and telecom focus on intellectual property protection and customer data privacy.

From an end-user perspective, large enterprises dominate adoption due to complex digital ecosystems and regulatory compliance demands, whereas small and medium enterprises are increasingly adopting managed detection and response services to mitigate insider threats and ransomware-driven data leakage risks.

The Data Exfiltration market by type includes Network-Based Data Loss Prevention (DLP), Endpoint DLP, Cloud-Based DLP, and Integrated User and Entity Behavior Analytics (UEBA) platforms. Network-based solutions currently account for approximately 38% of overall deployments, as enterprises prioritize monitoring outbound data packets across firewalls, gateways, and secure web proxies. These solutions are particularly dominant in sectors handling high transaction volumes, where traffic visibility exceeding 100 Gbps is required.

Cloud-based DLP solutions represent the fastest-growing segment, expanding at a CAGR of 9.4%, driven by multi-cloud adoption rates exceeding 65% among mid-to-large enterprises. Organizations increasingly require API-level data flow visibility within SaaS platforms and Infrastructure-as-a-Service environments to prevent unauthorized uploads or data transfers. Endpoint DLP and UEBA platforms together contribute nearly 34% of deployments, offering granular control over employee devices and behavioral risk scoring systems.

By application, the Data Exfiltration market is led by the BFSI sector, accounting for approximately 28% of total enterprise deployments. Financial institutions process millions of transactions daily and face compliance mandates requiring real-time monitoring of sensitive customer data. Advanced encryption inspection and anomaly detection systems reduce fraudulent data transfers by nearly 35% in high-volume banking environments.

Healthcare represents the fastest-growing application segment, expanding at a CAGR of 8.7%, supported by the digitization of electronic health records and telemedicine platforms. Hospitals and healthcare networks manage more than 50 petabytes of patient data annually in large national systems, increasing exposure to ransomware and insider misuse. Government and defense, IT and telecom, and manufacturing collectively contribute around 44% of deployments, focusing on intellectual property protection and classified data security.

Large enterprises dominate the Data Exfiltration market, representing nearly 62% of total deployments due to expansive IT infrastructures, cross-border operations, and stringent regulatory compliance requirements. These organizations manage thousands of endpoints and multiple cloud environments, necessitating automated risk scoring, encrypted traffic analysis, and continuous data flow auditing systems.

Small and medium enterprises (SMEs) represent the fastest-growing end-user group, expanding at a CAGR of 10.2%, as affordable cloud-native DLP platforms and managed security services reduce deployment complexity. SMEs now account for roughly 24% of enterprise cybersecurity tool adoption, with 48% prioritizing data leakage prevention to address ransomware risks. Government agencies, educational institutions, and research organizations collectively contribute about 14% of market deployments, focusing on intellectual property and citizen data protection.

North America accounted for the largest market share at 39% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.1% between 2026 and 2033.

North America’s dominance is supported by over 75% enterprise cloud penetration and more than 68% adoption of advanced data loss prevention (DLP) platforms among large organizations. Europe follows with approximately 27% market share, driven by stringent cross-border data protection frameworks and compliance-driven enterprise investments. Asia-Pacific represents nearly 23% of global demand, with digital transformation spending in cybersecurity increasing by over 30% in key economies such as China, India, and Japan. South America holds around 6% share, while the Middle East & Africa collectively account for 5%, supported by national cybersecurity modernization programs. Across regions, more than 70% of large enterprises are integrating AI-powered user behavior analytics into security operations centers, while over 60% of regulated organizations have implemented encrypted traffic inspection exceeding 40 Gbps network capacity, indicating a globally accelerating focus on advanced data exfiltration prevention infrastructure.

North America commands approximately 39% of the global Data Exfiltration market share, supported by high cybersecurity spending intensity and mature digital infrastructure. The United States alone accounts for over 80% of regional demand, with more than 72% of large enterprises deploying AI-driven DLP and insider threat detection systems. Key industries driving adoption include BFSI, healthcare, defense, and technology, collectively representing over 60% of regional enterprise security investments. Regulatory frameworks such as data breach notification laws and evolving privacy mandates have compelled organizations to implement real-time outbound traffic monitoring and zero-trust security architectures. More than 65% of enterprises have adopted secure access service edge (SASE) models to control cloud data movement. A prominent regional cybersecurity provider, Palo Alto Networks, expanded its AI-powered security operations platform in 2024, enabling automated detection across more than 2,000 enterprise environments. Consumer behavior reflects high sensitivity toward financial and healthcare data breaches, with 58% of enterprises prioritizing encrypted traffic inspection to secure sensitive digital transactions.

Europe accounts for nearly 27% of the global Data Exfiltration market, with Germany, the United Kingdom, and France representing over 60% of regional deployments. Strict data governance and privacy regulations have accelerated enterprise investment in explainable AI-based monitoring systems and audit-ready DLP frameworks. More than 70% of large enterprises in Western Europe conduct routine outbound data flow audits to ensure compliance with cross-border transfer rules. The region demonstrates strong adoption of zero-trust architecture, with approximately 54% of enterprises implementing identity-based access controls. Sustainability initiatives also influence procurement decisions, as nearly 40% of organizations prioritize energy-efficient data centers and security solutions with reduced power consumption. A leading European cybersecurity firm, Darktrace, expanded autonomous response capabilities across more than 8,000 organizations globally, strengthening behavioral analytics adoption. Regional consumer behavior is compliance-centric, with enterprises favoring transparent monitoring systems that align with privacy-preserving security standards.

Asia-Pacific holds around 23% of global Data Exfiltration market volume and ranks as the fastest-expanding regional segment. China, India, and Japan collectively contribute over 65% of regional demand, supported by accelerating cloud adoption rates exceeding 60% among mid-to-large enterprises. Rapid e-commerce growth and mobile-first digital ecosystems have increased sensitive data generation by more than 40% over the past five years. Regional technology hubs are investing heavily in AI-driven cybersecurity innovation, with over 50% of large enterprises deploying automated threat detection platforms. Infrastructure modernization programs and national cybersecurity strategies in countries such as India and Singapore are strengthening enterprise-level data monitoring standards. A leading regional technology company, Trend Micro, expanded its cloud-native security offerings in 2024, enhancing API-level data inspection capabilities. Consumer behavior reflects strong reliance on mobile applications and digital payments, driving heightened demand for endpoint-based data exfiltration controls.

South America represents approximately 6% of the global Data Exfiltration market, with Brazil and Argentina accounting for over 70% of regional deployments. Financial services, energy, and telecommunications sectors are key drivers, as digital banking transactions have grown by more than 35% across major urban markets. Increasing adoption of cloud-based enterprise resource planning systems has elevated exposure to outbound data risks. Government-backed cybersecurity strategies and trade modernization initiatives have encouraged enterprise security upgrades, particularly in Brazil where national digital transformation programs target enhanced infrastructure resilience. Regional enterprises are integrating managed detection and response services to compensate for cybersecurity talent shortages, which exceed 150,000 skilled professionals across the region. Consumer behavior shows rising awareness of digital fraud, prompting financial institutions to prioritize AI-based anomaly detection systems capable of monitoring over 1 million transactions per day.

The Middle East & Africa region accounts for nearly 5% of the global Data Exfiltration market, with the United Arab Emirates and South Africa leading adoption. Demand is closely linked to oil & gas, construction, banking, and government sectors, where large-scale infrastructure projects generate high volumes of sensitive operational data. Over 50% of enterprises in Gulf Cooperation Council countries have initiated cybersecurity modernization programs aligned with national digital strategies. Technological advancements include deployment of AI-based security operations centers capable of processing more than 20,000 security alerts daily. Local data protection regulations and regional trade partnerships are encouraging stronger encryption standards and cross-border monitoring frameworks. A regional telecom operator in the UAE implemented automated DLP solutions in 2024, reducing unauthorized outbound data transfers by 33% within one year. Consumer behavior varies across markets, with urban financial centers prioritizing advanced encryption monitoring while emerging economies focus on scalable cloud-based security platforms.

United States – 32% market share: The Data Exfiltration market in the United States leads due to high enterprise cybersecurity spending, advanced cloud infrastructure, and strong regulatory enforcement.

China – 14% market share: The Data Exfiltration market in China is driven by rapid digital economy expansion, large-scale cloud deployments, and national cybersecurity modernization programs.

The Data Exfiltration market exhibits a moderately consolidated competitive structure, with the top five companies collectively accounting for approximately 48% of global deployments. More than 120 active cybersecurity vendors operate across network security, endpoint protection, and cloud-native DLP segments. Market leaders differentiate through AI-driven behavioral analytics, zero-trust architecture integration, and automated incident response capabilities.

Strategic initiatives include over 35 notable product launches in 2024 focused on encrypted traffic inspection exceeding 100 Gbps throughput and API-level SaaS monitoring enhancements. Partnerships between cloud service providers and cybersecurity vendors increased by nearly 28% to strengthen integrated security ecosystems. Mergers and acquisitions remain active, with at least 18 cybersecurity-focused transactions completed globally in 2024 to expand AI-driven threat intelligence portfolios.

Innovation intensity remains high, with approximately 62% of leading vendors investing in machine learning-based anomaly detection and quantum-resistant encryption research. Competitive positioning increasingly depends on cloud-native scalability, managed security service integration, and regulatory compliance automation. The market’s competitive dynamics emphasize performance efficiency, low false-positive rates below 5%, and real-time threat containment under 10 seconds, reflecting a strong focus on measurable enterprise security outcomes.

IBM

Cisco Systems

Palo Alto Networks

Broadcom

McAfee

Trend Micro

Check Point Software Technologies

Fortinet

Darktrace

Forcepoint

Advanced artificial intelligence and machine learning models are redefining detection accuracy in the Data Exfiltration market. Modern User and Entity Behavior Analytics (UEBA) platforms process over 100,000 behavioral events per second in large enterprises, enabling anomaly detection with false-positive rates below 5%. Deep learning algorithms analyze contextual risk signals such as login frequency, device fingerprinting, geolocation mismatch, and abnormal file transfer volumes, improving insider threat identification by nearly 40% compared to rule-based legacy systems.

Zero Trust Architecture (ZTA) has become a core technological framework, with more than 60% of large enterprises implementing identity-based micro-segmentation and continuous authentication. Advanced Secure Access Service Edge (SASE) solutions integrate cloud access security brokers (CASB), firewall-as-a-service, and secure web gateways to monitor encrypted outbound traffic at speeds exceeding 100 Gbps. Encrypted traffic inspection technologies now handle over 85% of enterprise internet traffic, reflecting the global shift toward SSL/TLS-based communication.

Cloud-native Data Loss Prevention (DLP) systems are increasingly API-driven, enabling real-time scanning of SaaS platforms and Infrastructure-as-a-Service environments. Automated incident response tools can isolate compromised endpoints in under 10 seconds, reducing mean time to respond by approximately 35%. Emerging innovations include quantum-resistant encryption, confidential computing environments, and AI-assisted security orchestration that autonomously prioritizes high-risk exfiltration attempts. Collectively, these technologies are transforming enterprise data protection into an integrated, predictive, and scalable cybersecurity capability aligned with digital transformation objectives.

• In February 2025, Palo Alto Networks announced enhancements to its Cortex XSIAM platform, integrating advanced AI-driven analytics to automate security operations workflows and reduce incident response time by up to 50%. The update strengthens detection of insider-driven data exfiltration across hybrid cloud environments. Source: www.paloaltonetworks.com

• In April 2025, IBM expanded its QRadar Suite capabilities by embedding generative AI assistants to accelerate threat investigation and automate anomaly detection across multi-cloud infrastructures, improving analyst productivity and enabling faster containment of unauthorized data transfers. Source: www.ibm.com

• In October 2024, Cisco introduced new features within its Secure Access platform, enhancing zero-trust network access and encrypted traffic inspection capabilities to protect against sophisticated outbound data exfiltration techniques in distributed enterprise networks. Source: www.cisco.com

• In November 2024, Fortinet upgraded its FortiDLP solution with enhanced endpoint visibility and cloud application monitoring, enabling enterprises to identify sensitive data movement across SaaS platforms and reduce insider-related data leakage risks. Source: www.fortinet.com

The Data Exfiltration Market Report provides comprehensive coverage across technology types, deployment models, applications, and end-user segments. It evaluates network-based DLP, endpoint protection, cloud-native DLP, and AI-driven behavioral analytics solutions, highlighting performance benchmarks such as encrypted traffic inspection capacity exceeding 100 Gbps and automated response times under 10 seconds. The report analyzes on-premise, hybrid, and fully cloud-based deployments, with cloud-native architectures representing over 60% of new enterprise implementations.

Geographically, the report examines five key regions—North America, Europe, Asia-Pacific, South America, and Middle East & Africa—covering more than 30 major economies and assessing enterprise adoption rates exceeding 70% in highly regulated industries. Industry focus areas include BFSI, healthcare, government and defense, IT and telecom, manufacturing, retail, and energy, collectively accounting for over 85% of global enterprise cybersecurity spending.

The scope also addresses emerging segments such as API-level SaaS monitoring, quantum-resistant encryption, AI-powered security orchestration, and managed detection and response services. Special emphasis is placed on compliance-driven demand, including more than 100 active global data protection regulations influencing enterprise procurement strategies. By integrating quantitative insights, technology benchmarks, and industry-specific adoption patterns, the report delivers a structured and decision-oriented perspective for stakeholders evaluating risk mitigation, digital resilience, and long-term cybersecurity investments.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

6.6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

IBM, Cisco Systems, Palo Alto Networks, Broadcom, McAfee, Trend Micro, Check Point Software Technologies, Fortinet, Darktrace, Forcepoint |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |