Reports

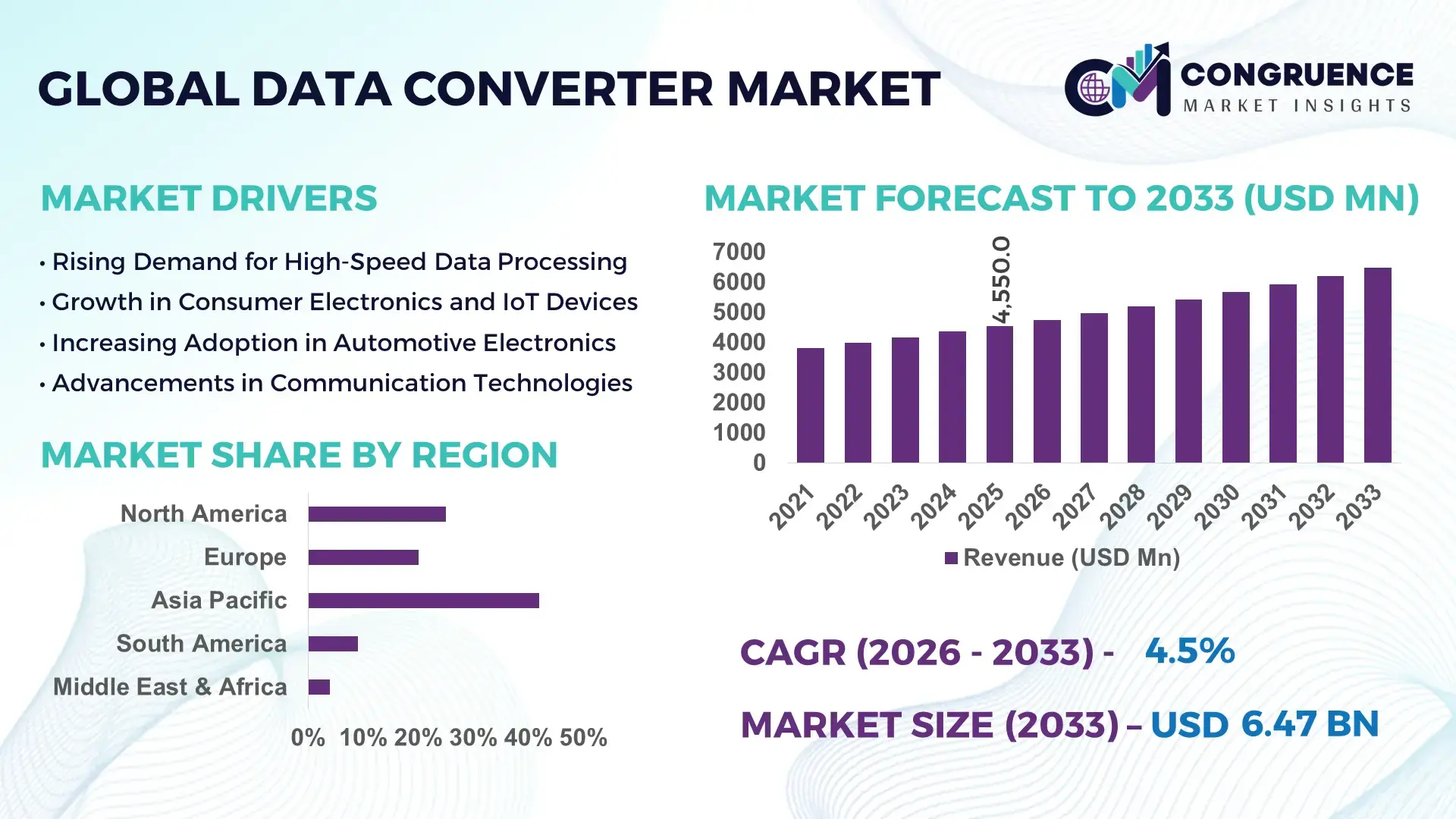

The Global Data Converter Market was valued at USD 4550 Million in 2025 and is anticipated to reach a value of USD 6470.55 Million by 2033 expanding at a CAGR of 4.5% between 2026 and 2033. This growth is driven by the rising demand for high-speed data processing across communication, automotive, and industrial automation sectors.

The United States continues to lead the data converter market with significant advancements in semiconductor fabrication and mixed-signal integrated circuits. The country hosts over 40% of the global high-performance analog semiconductor design activity, supported by annual R&D investments exceeding USD 70 billion across chip manufacturing firms. Data converters are extensively deployed in 5G infrastructure, aerospace electronics, and autonomous vehicle systems, with over 65% of advanced driver assistance systems integrating high-resolution ADCs and DACs. Additionally, the U.S. contributes to large-scale production capacity through advanced wafer fabrication facilities, with over 30 operational fabs supporting analog and mixed-signal chip production. The integration of AI-enabled edge processing has further boosted adoption in industrial IoT applications, where converter precision and latency reduction are critical performance metrics.

Market Size & Growth: USD 4550 Million in 2025, projected to reach USD 6470.55 Million by 2033 at a CAGR of 4.5%, driven by increasing demand for high-speed signal processing in 5G and IoT ecosystems.

Top Growth Drivers: 60% rise in IoT device integration, 45% increase in automotive electronics adoption, 35% improvement in industrial automation efficiency.

Short-Term Forecast: By 2028, advanced converter architectures are expected to improve signal accuracy by 25% and reduce power consumption by 18%.

Emerging Technologies: AI-assisted signal processing, ultra-low power ADCs, and high-speed RF data converters for 5G and satellite communication.

Regional Leaders: North America projected at USD 2100 Million by 2033 with strong aerospace adoption; Asia-Pacific at USD 2600 Million driven by consumer electronics manufacturing; Europe at USD 1500 Million with automotive innovation focus.

Consumer/End-User Trends: High adoption in telecom, automotive, and healthcare sectors with increasing demand for precision measurement and real-time data conversion.

Pilot or Case Example: In 2024, a semiconductor firm achieved 30% latency reduction using AI-optimized ADC architecture in telecom infrastructure.

Competitive Landscape: Market leader holds approximately 18% share, followed by major players including Texas Instruments, Analog Devices, Infineon Technologies, STMicroelectronics, and NXP Semiconductors.

Regulatory & ESG Impact: Energy efficiency mandates and RoHS compliance are driving development of low-power, eco-friendly converter solutions.

Investment & Funding Patterns: Over USD 12 billion invested globally in semiconductor innovation and analog chip design facilities.

Innovation & Future Outlook: Integration of converters with edge AI and advanced packaging technologies is shaping next-generation high-performance computing systems.

The data converter market is strongly influenced by key industry sectors such as telecommunications, automotive electronics, healthcare diagnostics, and industrial automation, contributing approximately 30%, 25%, 15%, and 20% respectively to overall demand. Technological advancements such as 16-bit and 24-bit high-resolution converters, along with sampling rates exceeding 10 GSPS, are enhancing system performance across critical applications. Regulatory frameworks emphasizing energy-efficient electronics and reduced electromagnetic interference are accelerating product innovation. Asia-Pacific dominates consumption due to large-scale electronics manufacturing hubs, while Europe focuses on automotive-grade converters for electric vehicles. Emerging trends include integration with AI processors, miniaturization of components, and increased deployment in edge computing environments, positioning the market for sustained technological evolution.

The strategic relevance of the Data Converter Market lies in its foundational role in enabling digital transformation across high-growth industries such as telecommunications, automotive, and industrial automation. Data converters serve as critical components bridging analog signals and digital systems, directly impacting performance efficiency and data accuracy. Advanced architectures such as pipeline ADCs and sigma-delta converters deliver up to 35% improvement in signal resolution compared to traditional successive approximation register (SAR) designs, making them essential for precision-driven applications.

Asia-Pacific dominates in production volume due to large-scale semiconductor manufacturing, while North America leads in adoption with over 55% of enterprises integrating high-performance converters in AI and 5G systems. By 2028, AI-driven signal processing technologies are expected to reduce latency by 20% and improve energy efficiency by 15%, particularly in edge computing applications. Firms are committing to ESG goals, targeting up to 25% reduction in power consumption of semiconductor devices by 2030 through energy-efficient converter designs.

In 2024, Japan achieved a 28% improvement in automotive sensor accuracy through the deployment of next-generation high-speed ADCs in electric vehicles, demonstrating measurable performance gains. Strategic investments in advanced packaging, chiplet integration, and low-power design are shaping future pathways. The Data Converter Market is increasingly positioned as a pillar of resilience, enabling compliance with evolving standards while supporting sustainable growth across digital infrastructure ecosystems.

The rapid deployment of 5G infrastructure and next-generation communication systems is significantly accelerating the demand for high-performance data converters. These systems require converters capable of handling frequencies above 6 GHz with sampling rates exceeding 10 GSPS to ensure real-time signal processing. Over 70% of telecom equipment manufacturers are integrating advanced ADCs and DACs to enhance signal fidelity and reduce noise interference. Additionally, the expansion of satellite communication and radar systems is increasing the need for wideband converters with high dynamic range. The growing adoption of cloud computing and data centers further contributes to demand, as high-speed data transmission relies heavily on efficient signal conversion. This trend is supported by continuous innovation in semiconductor technology, enabling improved power efficiency and performance.

The development of high-resolution and high-speed data converters involves significant design complexity and cost-intensive manufacturing processes. Advanced converters require precision analog circuitry, which increases fabrication challenges and reduces yield rates in semiconductor production. Approximately 30% of design costs in mixed-signal ICs are attributed to validation and testing processes, which are more complex compared to purely digital components. Additionally, the need for specialized materials and advanced lithography techniques increases production expenses. Small and medium-scale manufacturers often face barriers to entry due to high capital requirements and limited access to advanced fabrication facilities. These factors restrict market expansion, particularly in cost-sensitive regions, and slow down the adoption of cutting-edge converter technologies.

The rapid growth of electric vehicles (EVs) and Industry 4.0 initiatives presents substantial opportunities for the Data Converter Market. EV systems rely heavily on precise sensor data for battery management, motor control, and autonomous driving features, with over 80% of advanced EV platforms integrating high-resolution converters. Similarly, smart manufacturing environments utilize data converters in robotics, predictive maintenance systems, and real-time monitoring applications. The adoption of industrial IoT is expected to increase device connectivity by over 50% in the next five years, driving demand for efficient signal conversion solutions. Emerging applications such as smart grids and renewable energy systems also require advanced converters to manage variable power inputs and ensure system stability, creating new growth avenues.

One of the key challenges in the Data Converter Market is achieving optimal integration while maintaining power efficiency and performance. As devices become smaller and more complex, integrating high-performance converters into compact systems becomes increasingly difficult. Power consumption remains a critical concern, particularly in battery-operated devices and edge computing applications, where converters can account for up to 25% of total system power usage. Thermal management issues further complicate design, as high-speed converters generate significant heat, affecting reliability and lifespan. Additionally, ensuring compatibility with diverse system architectures and communication protocols requires continuous design optimization. These challenges necessitate ongoing innovation in low-power design techniques and advanced materials to meet evolving industry requirements.

• Rapid Adoption of High-Speed Data Converters in 5G Infrastructure: The expansion of 5G networks is significantly increasing demand for high-speed data converters capable of operating above 10 GSPS, with over 75% of telecom equipment manufacturers now integrating RF ADCs and DACs into base station architectures. Advanced converters supporting bandwidths beyond 1 GHz are enabling faster signal processing and reduced latency by up to 30%. In Asia-Pacific, more than 60% of newly deployed telecom infrastructure incorporates next-generation converters, highlighting a clear shift toward ultra-fast data processing technologies.

• Rising Integration of AI-Optimized Signal Processing Architectures: The use of artificial intelligence in signal processing is transforming converter efficiency, with AI-enabled converters improving signal accuracy by nearly 25% and reducing noise distortion by 20%. Approximately 50% of semiconductor companies are investing in AI-assisted mixed-signal design to enhance performance in real-time applications. Edge AI integration has grown by over 40% in industrial IoT deployments, where adaptive converters dynamically optimize power consumption and data throughput.

• Increasing Demand for Low-Power and Energy-Efficient Designs: Power efficiency has become a critical priority, particularly in battery-operated and portable devices, where data converters can account for up to 25% of system power usage. Recent advancements have reduced power consumption in high-resolution converters by 18% while maintaining performance levels above 16-bit resolution. Over 65% of consumer electronics manufacturers are prioritizing low-power converter integration to comply with energy efficiency regulations and extend device battery life.

• Expansion of Automotive Electronics and Autonomous Systems: The automotive sector is witnessing significant adoption of high-precision data converters, with over 70% of advanced driver assistance systems relying on ADCs for sensor data processing. Electric vehicles require converters with accuracy levels exceeding 18-bit resolution for battery monitoring and motor control systems. Adoption of automotive-grade converters has increased by 45% in the past three years, driven by the growing demand for autonomous driving capabilities and real-time data analytics in modern vehicles.

The Data Converter Market segmentation is structured around product types, application areas, and end-user industries, each contributing distinctively to overall demand patterns. Analog-to-digital converters (ADCs) and digital-to-analog converters (DACs) form the primary product categories, with ADCs dominating due to their widespread use in signal acquisition systems. Applications span telecommunications, automotive electronics, healthcare devices, and industrial automation, with telecom accounting for a significant portion due to 5G expansion. From an end-user perspective, semiconductor manufacturers, OEMs, and system integrators play a pivotal role in market growth. Approximately 65% of demand originates from high-performance computing and communication sectors, while emerging applications in edge computing and smart infrastructure are expanding rapidly. The segmentation highlights a strong alignment between technological innovation and industry-specific requirements, driving targeted adoption across global markets.

The Data Converter Market by type includes Analog-to-Digital Converters (ADCs), Digital-to-Analog Converters (DACs), and other specialized converters such as time-to-digital converters. ADCs currently dominate the segment, accounting for approximately 58% of total adoption due to their critical role in converting real-world analog signals into digital data for processing in communication systems, industrial sensors, and medical devices. In comparison, DACs hold around 32% share, primarily driven by applications in audio systems, wireless communication, and signal reconstruction. However, high-speed ADCs represent the fastest-growing segment, expanding at an estimated CAGR of 6.2%, supported by increasing deployment in 5G infrastructure and radar systems requiring sampling rates above 10 GSPS.

Other niche converter types collectively contribute about 10% of the market, serving specialized applications such as time measurement in scientific instrumentation and quantum computing. These segments are gaining attention due to advancements in precision electronics and research-driven innovations.

In terms of application, telecommunications leads the Data Converter Market with approximately 35% share, driven by the expansion of 5G networks and increasing demand for high-speed data transmission. Automotive electronics follow with around 25%, as modern vehicles rely heavily on data converters for sensor integration, battery management, and advanced driver assistance systems. Industrial automation accounts for nearly 20%, where converters are essential for real-time monitoring and control in manufacturing processes. Healthcare applications contribute about 12%, leveraging converters in diagnostic imaging and patient monitoring systems.

While telecommunications remains dominant, automotive electronics is the fastest-growing application segment, expanding at an estimated CAGR of 6.8% due to rapid electrification and autonomous vehicle development. The increasing adoption of electric vehicles, where over 80% of systems depend on precise signal conversion, is a major growth driver.

The Data Converter Market is primarily driven by semiconductor manufacturers and original equipment manufacturers (OEMs), which together account for approximately 45% of total demand due to their role in designing and integrating converters into electronic systems. Telecommunications companies represent around 20% of the market, leveraging converters for network infrastructure and signal processing. Automotive manufacturers contribute nearly 18%, reflecting the growing reliance on electronic systems in modern vehicles. Industrial enterprises and healthcare providers collectively account for the remaining 17%, driven by increasing adoption of automation and precision diagnostics.

Among these, automotive manufacturers are the fastest-growing end-user segment, with an estimated CAGR of 6.5%, fueled by the rapid transition toward electric and autonomous vehicles. Semiconductor firms continue to dominate in terms of volume, with over 70% of advanced converter designs originating from leading chip manufacturers.

Region Asia-Pacific accounted for the largest market share at 42% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2026 and 2033.

Asia-Pacific leads due to its extensive semiconductor manufacturing base, with China, Japan, and South Korea collectively contributing over 65% of global electronics production volume. China alone accounts for nearly 28% of global demand for data converters due to its large-scale consumer electronics and telecom sectors. North America follows with approximately 27% market share, driven by high adoption in aerospace, defense, and 5G infrastructure, where over 70% of telecom systems integrate high-speed converters. Europe holds around 18%, supported by automotive electronics and industrial automation, particularly in Germany and France, where over 60% of manufacturing systems rely on precision signal conversion. South America and the Middle East & Africa collectively contribute about 13%, with growing adoption in energy, telecommunications, and infrastructure modernization projects. Increasing deployment of IoT devices, projected to exceed 30 billion connected units globally by 2030, continues to shape regional demand patterns.

How is advanced digital infrastructure accelerating high-performance signal processing demand?

North America accounts for approximately 27% of the Data Converter Market, supported by strong demand across telecommunications, aerospace, defense, and healthcare sectors. Over 75% of telecom infrastructure upgrades in the region incorporate high-speed ADCs and DACs to support 5G and satellite communication systems. Government-backed semiconductor initiatives, including funding exceeding USD 50 billion for domestic chip manufacturing, are strengthening production capabilities and reducing supply chain dependencies. The region is also witnessing rapid adoption of AI-driven signal processing, with more than 55% of enterprises integrating advanced converters into edge computing systems. A key industry participant has introduced converters with sampling rates exceeding 12 GSPS, improving signal fidelity by over 30% in high-frequency applications. Consumer behavior reflects high enterprise adoption, particularly in healthcare and financial services, where precision data acquisition is critical for diagnostics and real-time analytics.

Why is regulatory-driven innovation shaping precision electronics adoption trends?

Europe holds approximately 18% share in the Data Converter Market, with major contributions from Germany, the United Kingdom, and France. The region’s strong automotive and industrial base drives demand, with over 65% of automotive electronic systems relying on high-resolution converters for electric and autonomous vehicles. Regulatory frameworks focused on energy efficiency and sustainability, including directives targeting a 30% reduction in electronic waste by 2030, are influencing product design and innovation. Adoption of advanced technologies such as 16-bit and 18-bit converters has increased by 40% in industrial automation systems. A prominent regional semiconductor company has developed low-power converters that reduce energy consumption by 20% in automotive applications. Consumer behavior is influenced by strict compliance requirements, leading to increased demand for reliable and energy-efficient data converter solutions across industries.

What factors are driving large-scale manufacturing and high-volume adoption of signal conversion technologies?

Asia-Pacific dominates the Data Converter Market with a 42% share, driven by high-volume production and consumption across China, Japan, South Korea, and India. The region accounts for over 60% of global semiconductor manufacturing capacity, with China alone producing more than 25% of consumer electronics globally. Rapid expansion of 5G infrastructure has resulted in over 65% of telecom deployments utilizing advanced data converters. Japan and South Korea lead in innovation, focusing on ultra-high-speed converters exceeding 10 GSPS for advanced communication systems. A leading regional manufacturer has scaled production of high-resolution converters, increasing output capacity by 35% to meet rising demand. Consumer behavior is heavily influenced by mobile technology and digital ecosystems, with over 70% of applications centered around smartphones, IoT devices, and AI-enabled consumer electronics.

How are infrastructure and digital media demands influencing signal processing adoption trends?

South America represents approximately 7% of the Data Converter Market, with Brazil and Argentina as key contributors. The region is experiencing growth in telecommunications and energy sectors, where over 50% of new infrastructure projects integrate digital signal processing technologies. Government initiatives promoting digital transformation and renewable energy adoption are driving demand for efficient data converters, particularly in smart grid applications. Trade policies supporting electronics imports have increased availability of advanced converter components by 20% in recent years. A regional electronics firm has implemented data converters in broadcast and media systems, improving signal clarity by 25% across digital transmission networks. Consumer behavior is largely influenced by media consumption and language localization, with increasing demand for high-quality audio and video processing solutions.

Why is technological modernization accelerating demand for precision electronic components?

The Middle East & Africa region accounts for nearly 6% of the Data Converter Market, with significant demand emerging from the UAE, Saudi Arabia, and South Africa. Growth is driven by investments in oil and gas, telecommunications, and smart city initiatives, where over 45% of new projects incorporate advanced electronic systems. Infrastructure modernization programs have increased adoption of data converters in industrial automation and energy management systems by 30%. Regional trade partnerships and government policies supporting digital transformation are further enhancing market growth. A local technology provider has deployed high-performance converters in smart grid systems, improving energy monitoring accuracy by 22%. Consumer behavior reflects growing reliance on digital services and mobile connectivity, with increasing adoption of IoT-enabled devices across urban centers.

United States Data Converter Market – 24% share: Strong semiconductor R&D ecosystem and high adoption in aerospace, defense, and 5G infrastructure.

China Data Converter Market – 28% share: Large-scale electronics manufacturing base and extensive demand from consumer electronics and telecom sectors.

The Data Converter Market is moderately consolidated, with over 45 active global and regional competitors competing across analog and mixed-signal semiconductor segments. The top five companies collectively account for approximately 52% of the total market share, reflecting a competitive yet innovation-driven landscape. Leading players focus on high-performance product portfolios, particularly in high-speed ADCs and DACs exceeding 10 GSPS, to cater to telecommunications, automotive, and industrial automation sectors. Strategic initiatives such as mergers, partnerships, and product launches are shaping competition, with more than 20 major collaborations recorded in the past two years aimed at enhancing semiconductor design capabilities and expanding production capacity.

Innovation remains a key differentiator, with over 60% of companies investing heavily in research and development to improve signal accuracy, reduce power consumption, and enable AI-driven signal processing. Advanced packaging technologies and chiplet-based architectures are being adopted to enhance integration and performance. Additionally, companies are expanding manufacturing footprints, with more than 15 new semiconductor fabrication facilities announced globally to address supply chain constraints. Competitive positioning is further influenced by the ability to deliver customized solutions for specific applications such as 5G infrastructure, electric vehicles, and industrial IoT, where performance requirements are increasingly stringent.

Texas Instruments

Analog Devices

Infineon Technologies

STMicroelectronics

NXP Semiconductors

Microchip Technology

Renesas Electronics

ON Semiconductor

Maxim Integrated

Rohm Semiconductor

Technological advancements in the Data Converter Market are centered on improving speed, resolution, power efficiency, and integration capabilities to meet the evolving demands of high-performance electronic systems. High-speed analog-to-digital converters (ADCs) now exceed sampling rates of 12 GSPS, enabling real-time processing in 5G base stations, radar systems, and satellite communication. At the same time, resolution capabilities have advanced significantly, with 16-bit and 18-bit converters becoming standard in precision applications such as medical imaging and industrial instrumentation, while 24-bit sigma-delta converters are widely used in audio and measurement systems for enhanced accuracy.

Low-power design has become a critical innovation area, with recent converter architectures achieving up to 20% reduction in power consumption through advanced CMOS scaling and dynamic voltage optimization. Approximately 65% of new converter designs now incorporate power management features to support battery-operated and edge devices. Additionally, integration of artificial intelligence into signal processing is gaining traction, with AI-assisted calibration improving signal-to-noise ratio by nearly 15% and reducing distortion in high-frequency applications.

Emerging technologies such as RF data converters are enabling direct conversion architectures, eliminating intermediate frequency stages and reducing system complexity by over 25%. Advanced packaging techniques, including system-in-package (SiP) and chiplet-based integration, are enhancing performance density while minimizing footprint, with over 40% of new semiconductor designs adopting these approaches. Furthermore, the adoption of FinFET and 7nm process nodes is enabling higher transistor density, allowing improved converter performance without increasing power consumption.

Another key trend is the development of time-interleaved ADCs, which combine multiple converter cores to achieve higher effective sampling rates, improving throughput by up to 3x in high-bandwidth applications. Digital calibration techniques are also being widely implemented, reducing mismatch errors by 30% and enhancing overall system reliability. These technological advancements are positioning data converters as essential components in next-generation digital ecosystems, supporting applications ranging from autonomous vehicles to smart manufacturing and advanced communication networks.

• In March 2025, Analog Devices expanded its high-speed RF data converter portfolio with the introduction of a new mixed-signal front-end platform designed for 5G and aerospace applications, supporting sampling rates above 12 GSPS and improving signal bandwidth efficiency by 20%. Source: www.analog.com

• In October 2024, Texas Instruments launched a new series of low-power precision ADCs featuring 24-bit resolution and integrated digital filtering, reducing system power consumption by up to 30% in industrial and healthcare monitoring applications. Source: www.ti.com

• In January 2025, STMicroelectronics introduced advanced automotive-grade data converters optimized for electric vehicle systems, achieving 18-bit resolution and enhancing battery monitoring accuracy by 25%, supporting next-generation EV safety and performance requirements. Source: www.st.com

• In July 2024, Infineon Technologies announced the development of a new generation of high-speed data converters integrated with AI-assisted signal processing, enabling a 15% improvement in noise reduction and supporting real-time analytics in industrial automation systems. Source: www.infineon.com

The Data Converter Market Report provides a comprehensive evaluation of industry dynamics, covering a wide range of product types, applications, technologies, and regional markets. The report analyzes key segments including analog-to-digital converters (ADCs), digital-to-analog converters (DACs), and specialized converter architectures such as time-to-digital and RF data converters. It encompasses performance classifications based on resolution levels ranging from 8-bit to 24-bit and sampling speeds exceeding 10 GSPS, addressing diverse use cases across high-speed communication and precision measurement systems.

From an application perspective, the report examines deployment across telecommunications, automotive electronics, industrial automation, healthcare, aerospace, and consumer electronics. Telecommunications alone accounts for over one-third of total demand due to rapid 5G infrastructure expansion, while automotive applications represent a significant portion driven by increasing electronic content in vehicles. The report also highlights emerging use cases such as edge computing, smart grids, and AI-enabled industrial systems, where data converters play a crucial role in real-time signal processing.

Geographically, the scope includes detailed analysis across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with Asia-Pacific contributing over 40% of global demand due to its manufacturing dominance. The report further evaluates technological advancements such as AI-integrated converters, low-power architectures, and advanced semiconductor fabrication processes, with over 60% of new product innovations focusing on performance optimization and energy efficiency.

Additionally, the report covers competitive benchmarking, supply chain analysis, and regulatory frameworks influencing market adoption, including energy efficiency standards and environmental compliance requirements. It also explores niche segments such as automotive-grade converters, RF data converters, and miniaturized components for wearable devices, providing a holistic view for stakeholders seeking strategic insights and informed decision-making.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

4.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Texas Instruments, Analog Devices, Infineon Technologies, STMicroelectronics, NXP Semiconductors, Microchip Technology, Renesas Electronics, ON Semiconductor, Maxim Integrated, Rohm Semiconductor |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |