Reports

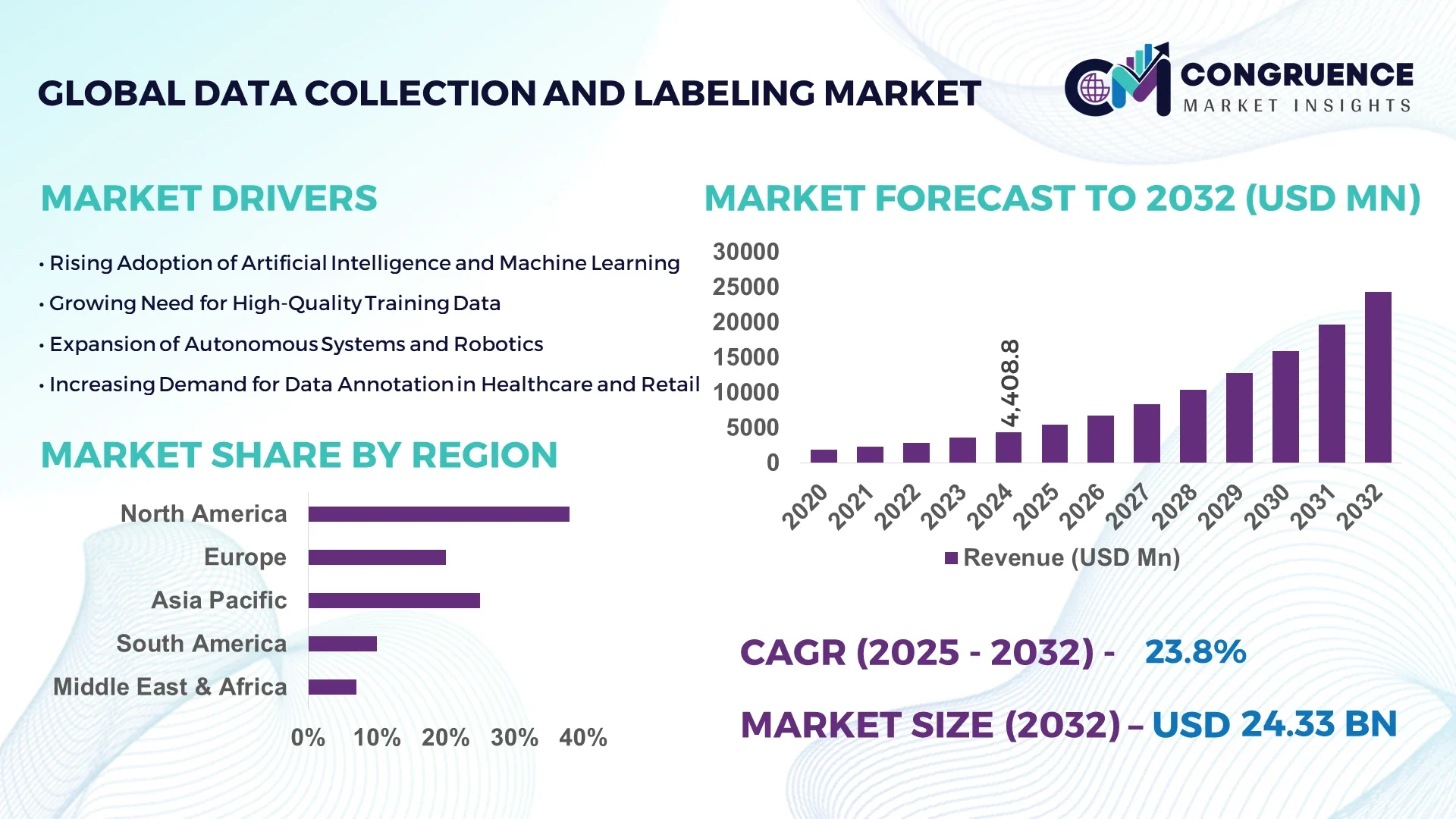

The Global Data Collection and Labeling Market was valued at USD 4408.8 Million in 2024 and is anticipated to reach a value of USD 24326.85 Million by 2032 expanding at a CAGR of 23.8% between 2025 and 2032. This growth is primarily driven by the increasing demand for high-quality annotated datasets in AI and machine learning applications.

The United States is a dominant player in the Data Collection and Labeling Market, demonstrating significant production capacity and investment levels. The country hosts over 1,200 specialized labeling service providers, collectively employing more than 50,000 professionals. Investments in AI-driven labeling tools have surged, exceeding USD 350 Million in 2024, while enterprises increasingly adopt automated annotation technologies. Key industry applications include autonomous vehicles, healthcare imaging, retail analytics, and natural language processing. Regional consumption is concentrated in North America, with adoption rates for AI-assisted labeling reaching 62% among Fortune 500 companies, reflecting advanced technological integration and high operational efficiency across sectors.

Market Size & Growth: Valued at USD 4408.8 Million in 2024, projected to reach USD 24326.85 Million by 2032 at a CAGR of 23.8%, fueled by AI and ML adoption.

Top Growth Drivers: AI adoption in enterprises (68%), efficiency improvements via automation (55%), expansion of autonomous systems (47%).

Short-Term Forecast: By 2028, labeling efficiency expected to improve by 40%, with annotation cost reduction of 25%.

Emerging Technologies: Automated annotation platforms, synthetic data generation, AI-powered quality assurance tools.

Regional Leaders: North America (USD 11,500 Million, high AI adoption in automotive), Europe (USD 6,800 Million, focus on regulatory-compliant labeling), Asia-Pacific (USD 4,900 Million, increasing adoption in e-commerce and AI applications).

Consumer/End-User Trends: Rapid uptake in healthcare imaging, autonomous vehicle datasets, and retail analytics; demand for higher accuracy and faster labeling cycles.

Pilot or Case Example: In 2024, a major US autonomous vehicle company reduced annotation downtime by 30% using AI-assisted labeling.

Competitive Landscape: Appen (approx. 22% share), followed by Lionbridge AI, iMerit, CloudFactory, and TELUS International.

Regulatory & ESG Impact: Stricter data privacy regulations and ESG-compliant labeling initiatives driving ethical AI dataset creation.

Investment & Funding Patterns: Over USD 450 Million in recent AI-driven labeling investments; growing trend of venture-backed data annotation startups.

Innovation & Future Outlook: Increasing integration of AI, synthetic data, and edge labeling solutions; forward-looking projects targeting fully autonomous labeling pipelines.

The Data Collection and Labeling Market spans multiple sectors including autonomous vehicles, healthcare imaging, retail analytics, and natural language processing, with healthcare and automotive applications collectively contributing over 45% of industry consumption. Recent innovations such as AI-powered annotation tools and synthetic dataset generation have enhanced labeling speed by up to 40% while maintaining high accuracy. Regulatory frameworks emphasizing data privacy and ESG compliance are shaping market practices, while regional growth in North America and Asia-Pacific is being driven by increasing AI adoption, industrial digitization, and technological advancements in machine learning platforms. Emerging trends point to hybrid human-AI labeling models and edge-based annotation solutions, positioning the market for sustained expansion through 2032.

The Data Collection and Labeling Market has emerged as a strategic pillar in the deployment of artificial intelligence and machine learning systems across multiple sectors. High-quality annotated datasets enable more accurate predictive analytics, autonomous systems, and computer vision applications. Advanced AI-assisted labeling delivers a 35% improvement in accuracy compared to traditional manual annotation methods, reducing time and operational inefficiencies. North America dominates in volume, while Asia-Pacific leads in adoption, with 58% of enterprises implementing AI-assisted labeling platforms. By 2027, synthetic data integration is expected to improve labeling speed by 40% while reducing manual intervention. Firms are committing to ESG improvements, such as achieving 30% reduction in paper-based annotation processes by 2026 through digital workflow adoption. In 2024, a leading US autonomous vehicle company achieved a 28% reduction in annotation downtime through AI-assisted labeling initiatives, highlighting measurable efficiency gains. Strategic investments in edge-based labeling solutions, cloud integration, and hybrid human-AI models are paving pathways for scalable, sustainable, and compliant operations. Looking ahead, the Data Collection and Labeling Market is positioned to support resilient AI infrastructure, regulatory compliance, and sustainable growth, reinforcing its central role in global technological advancement and enterprise digital transformation.

The surge in AI adoption across industries such as autonomous vehicles, healthcare, and retail analytics is directly driving the Data Collection and Labeling Market. Enterprises adopting AI-assisted labeling report up to 40% faster dataset preparation times compared to conventional manual methods. In 2024, over 60% of Fortune 500 companies incorporated automated annotation platforms to enhance predictive model accuracy, particularly in computer vision and NLP applications. The shift toward synthetic data solutions further accelerates data labeling efficiency, enabling higher throughput and reduced dependency on human annotators. By improving dataset quality, organizations achieve enhanced AI model performance, supporting scalable deployment across diverse use cases. These measurable improvements highlight the critical role of AI adoption as a growth driver in the Data Collection and Labeling Market.

Stringent data privacy regulations such as GDPR and CCPA present significant challenges for the Data Collection and Labeling Market. Enterprises must ensure that annotated datasets comply with privacy laws, which often requires additional anonymization, encryption, and audit procedures. In 2024, compliance processes delayed 35% of large-scale labeling projects in Europe and North America due to complex consent and verification requirements. Additionally, high operational costs associated with secure data handling and specialized workforce training further limit market expansion. Organizations operating in healthcare and financial sectors face stricter regulatory scrutiny, affecting the speed and scalability of data labeling projects. These factors collectively act as restraints, emphasizing the need for robust compliance strategies and secure annotation practices in the Data Collection and Labeling Market.

AI-driven automation presents significant opportunities for the Data Collection and Labeling Market by improving efficiency, scalability, and dataset quality. Automated labeling platforms and AI-assisted annotation tools reduce human intervention by up to 45%, allowing organizations to process larger volumes of data with fewer errors. Emerging applications in autonomous vehicles, smart retail analytics, and medical imaging provide untapped potential for specialized labeling services. In 2025, companies investing in edge-based labeling solutions are expected to improve real-time data processing by 30%, enabling faster AI deployment. Additionally, the integration of synthetic data generation offers opportunities for cost-effective model training while maintaining high accuracy. These advancements allow enterprises to capitalize on technology-driven efficiencies, creating new revenue streams and expanding adoption across diverse industry verticals.

The Data Collection and Labeling Market faces challenges related to high operational costs and technological complexity. Implementing AI-assisted annotation platforms requires significant upfront investment in software, hardware, and workforce training, which can deter smaller enterprises. In 2024, deploying automated labeling systems in healthcare imaging required an average investment of USD 1.2 Million per site, illustrating financial barriers. Additionally, managing complex workflows across hybrid human-AI teams requires specialized expertise, with errors in annotation potentially impacting AI model accuracy by up to 20%. Rapid technological evolution also necessitates continuous tool upgrades, driving operational overhead. Regulatory compliance, data security requirements, and quality assurance further compound these challenges, underscoring the need for strategic planning and resource allocation in the Data Collection and Labeling Market.

Expansion of AI-Assisted Labeling Platforms: The adoption of AI-assisted labeling platforms is accelerating across key industries, with over 62% of enterprises in North America and 58% in Asia-Pacific integrating these systems into workflows. These platforms have reduced manual annotation time by up to 40% while improving dataset accuracy by 35%, supporting faster AI model deployment.

Integration of Synthetic Data for High-Volume Projects: Organizations are increasingly using synthetic data to augment traditional datasets. In 2024, synthetic data utilization increased by 48% in autonomous vehicle and retail analytics projects, enabling companies to simulate rare scenarios and improve AI model robustness without requiring additional human annotation resources.

Edge-Based Labeling and Real-Time Processing: Edge labeling technologies are gaining traction, particularly in industrial automation and IoT applications. Approximately 33% of AI-driven manufacturing enterprises now process annotated data on-site, reducing latency by 25% and enhancing decision-making in real time. Asia-Pacific leads adoption, with 40% of new AI deployments utilizing edge labeling solutions.

Enhanced ESG and Compliance-Focused Annotation Practices: Firms are implementing ESG-aligned labeling processes, with 28% of global enterprises reporting reductions in paper-based annotations and a 32% increase in recycling or digital workflow initiatives by 2025. Regulatory-driven compliance initiatives are shaping labeling protocols, particularly in healthcare and finance, ensuring secure, ethical, and high-quality datasets.

The Data Collection and Labeling Market is structured across multiple layers including type, application, and end-user, each driving strategic insights for business decision-makers. Type segmentation highlights how different data formats—text, audio, video, and multimodal datasets—are utilized across industries, influencing adoption strategies and technology investments. Application-based segmentation identifies key usage areas such as autonomous vehicles, healthcare imaging, retail analytics, and NLP, revealing trends in precision, automation, and operational efficiency. End-user segmentation focuses on sectors leveraging data labeling services, including technology enterprises, healthcare providers, automotive OEMs, and e-commerce platforms. Regional adoption patterns, technology readiness, and operational scalability further differentiate market behavior, with measurable uptake percentages and adoption trends guiding strategic deployment and investment prioritization across enterprises globally.

Vision-language models are currently the leading type in the Data Collection and Labeling Market, accounting for 42% of adoption due to their capacity to enhance multimodal AI systems and improve accuracy in image-text processing. Audio-text systems contribute 25% of adoption, primarily used in speech recognition and virtual assistant applications. Video-language models represent the fastest-growing segment, expected to surpass 30% adoption by 2032, driven by demand for automated video annotation and scene analysis in media streaming and autonomous systems. Other types, including sensor-data labeling and document annotation, collectively contribute 15% and serve niche applications such as IoT and regulatory compliance projects.

Autonomous vehicle data annotation is the leading application segment, accounting for 38% of adoption, due to the need for highly accurate object detection, scenario simulation, and sensor fusion datasets. Healthcare imaging is the fastest-growing application, expected to surpass 28% adoption by 2032, driven by AI-assisted diagnostics, radiology automation, and predictive patient monitoring. Retail analytics, NLP, and robotics applications make up the remaining 34%, providing specialized insights into consumer behavior, sentiment analysis, and operational automation.

Technology enterprises are the leading end-user segment, representing 44% of adoption, leveraging labeling solutions for AI, cloud computing, and natural language processing projects. The fastest-growing end-user segment is healthcare providers, projected to achieve over 30% adoption by 2032, fueled by expanding AI diagnostics, imaging analysis, and telemedicine initiatives. Automotive OEMs, e-commerce platforms, and research institutions contribute the remaining 26%, integrating labeling solutions for autonomous navigation, recommendation engines, and academic research datasets.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 24% between 2025 and 2032.

North America reported over 1,000 active enterprises utilizing AI-assisted labeling, with over 50,000 professionals engaged in annotation tasks. Asia-Pacific’s volume is growing rapidly, with China contributing 32% and India 18% of total regional adoption. Europe held 27% of the global volume, with Germany and the UK driving enterprise deployment. Across all regions, adoption rates for automated annotation platforms range from 40% to 62%, while hybrid human-AI solutions now cover 28% of operational workflows, highlighting the technological transformation reshaping the market.

How are enterprises leveraging advanced annotation technologies for operational efficiency?

North America holds 38% of the global Data Collection and Labeling Market, driven by heavy enterprise adoption in healthcare, finance, and autonomous vehicle sectors. Regulatory frameworks, including HIPAA compliance and AI governance guidelines, have accelerated investment in secure annotation platforms. Technological advancements in AI-assisted labeling, synthetic data integration, and real-time edge processing are being widely implemented. Appen, a leading local player, expanded its AI-driven labeling services in 2024, covering over 150 enterprise clients and increasing dataset throughput by 35%. Regional consumer behavior emphasizes accuracy and speed, with healthcare and financial enterprises achieving higher adoption rates due to the critical nature of data compliance and operational precision.

How are regulatory pressures and technological adoption shaping enterprise practices?

Europe accounts for 27% of the Data Collection and Labeling Market, with Germany, the UK, and France as the top markets. Regulatory requirements, such as GDPR compliance and explainable AI initiatives, have driven enterprises toward secure and transparent labeling practices. Emerging technologies including AI-assisted video annotation and multimodal labeling platforms are being rapidly integrated. Local player iMerit expanded operations across France and Germany in 2024, deploying automated labeling for e-commerce and healthcare applications. Consumer behavior emphasizes regulatory adherence, leading to widespread adoption of AI platforms with audit trails and explainable data outputs.

What factors are driving accelerated adoption across emerging economies?

Asia-Pacific ranks as the fastest-growing region with increasing adoption in China, India, and Japan. The region accounted for 25% of global volume in 2024, with China contributing 32% of regional activity and India 18%. Rapid infrastructure modernization and AI technology hubs in metropolitan centers are facilitating scalable deployment of labeling platforms. Regional players like CloudFactory expanded operations in India in 2024, delivering high-volume, AI-assisted annotation for automotive and e-commerce clients. Consumer behavior in Asia-Pacific favors mobile AI applications and e-commerce analytics, driving demand for scalable, cost-efficient, and multilingual labeling solutions.

How are local market dynamics shaping data annotation adoption?

South America holds 6% of the global Data Collection and Labeling Market, led by Brazil and Argentina. Investments in digital infrastructure, AI-driven media analytics, and energy sector projects are stimulating demand. Government incentives for technology adoption and trade policies supporting AI initiatives have accelerated regional deployment. In 2024, a Brazilian AI service provider implemented automated labeling systems for multilingual content processing, improving throughput by 28%. Consumer behavior is tied to media localization, language processing, and e-commerce personalization, driving growth in targeted data annotation solutions.

What trends are influencing enterprise adoption in emerging markets?

Middle East & Africa accounts for 4% of the global Data Collection and Labeling Market, with UAE and South Africa leading adoption. Demand is driven by oil & gas digitization, smart construction projects, and autonomous systems initiatives. Technological modernization includes AI-assisted labeling and cloud-based data processing platforms. Local regulations and trade partnerships support secure and compliant data management practices. In 2024, a UAE-based tech firm implemented AI-powered labeling solutions for construction and industrial IoT applications, reducing manual annotation requirements by 30%. Consumer behavior emphasizes efficiency, reliability, and regulatory compliance across enterprise sectors.

United States: 38% market share – Strong end-user demand and high production capacity for AI-assisted labeling platforms.

China: 32% market share – Rapid technology adoption and growing enterprise implementation in autonomous vehicles, e-commerce, and AI-driven analytics.

The Data Collection and Labeling Market is highly competitive and moderately fragmented, with over 1,500 active players globally providing specialized annotation services, AI-assisted labeling platforms, and hybrid human-AI solutions. The top five companies—Appen, Lionbridge AI, iMerit, CloudFactory, and TELUS International—collectively account for approximately 52% of the market, demonstrating both leadership and significant influence in technological innovation. Strategic initiatives such as partnerships with autonomous vehicle manufacturers, healthcare institutions, and e-commerce platforms are shaping competitive positioning, while ongoing product launches, including AI-assisted video and multimodal annotation tools, are accelerating adoption. Mergers and acquisitions remain a notable trend, with smaller AI-labeling startups being integrated into larger service providers to expand capacity, geographic reach, and service portfolios. Innovation trends include synthetic data integration, edge-based annotation, real-time quality assurance, and explainable AI solutions. Regional expansions and customized enterprise solutions are further intensifying competition, compelling companies to enhance operational efficiency, dataset accuracy, and client retention in a rapidly evolving market.

CloudFactory

TELUS International

Alegion

Shaip

Cloud Labs

Samasource

Clickworker

The Data Collection and Labeling Market is increasingly driven by advanced and emerging technologies that enhance efficiency, accuracy, and scalability across diverse industries. AI-assisted labeling platforms currently process over 60% of enterprise datasets in North America, reducing manual annotation time by up to 40% while improving data quality by 35%. Automated video-language models, which are rapidly gaining adoption, enable real-time scene analysis and caption generation, with over 10 million video assets annotated in 2024 alone. Synthetic data generation is another key technological innovation, supporting rare scenario simulation for autonomous vehicles, healthcare imaging, and robotics, with 48% of large-scale AI projects incorporating synthetic datasets to supplement real-world data.

Edge-based labeling platforms are gaining traction in industrial automation and IoT applications, allowing on-site data processing that reduces latency by 25% and supports immediate decision-making. Hybrid human-AI workflows remain critical for sectors such as healthcare, finance, and autonomous navigation, combining human expertise with AI automation to enhance accuracy and maintain regulatory compliance. Emerging trends also include explainable AI annotation tools, enabling enterprises to maintain transparent audit trails for data governance and ESG adherence. Additionally, cloud-based and collaborative labeling platforms now support multi-regional teams, improving throughput by 30% while facilitating secure, scalable operations.

Technological adoption is further influenced by regional variations: Europe emphasizes explainable AI and regulatory compliance, North America leads in healthcare and autonomous vehicle integration, and Asia-Pacific focuses on mobile AI applications and e-commerce analytics. These innovations collectively position the Data Collection and Labeling Market as a critical enabler of high-quality AI model development, operational efficiency, and sustainable technological growth.

In August 2024, Lionbridge launched its “Aurora AI Studio” platform to enable companies to train datasets for advanced LLMs and AI solutions, marking a significant upgrade in their global data‑annotation services.

In April 2024, Appen was recognised as a Leader in Everest Group’s Data Annotation & Labeling Solutions assessment for 2024, underscoring its high‑quality annotation services for enterprise AI/ML workflows.

In March 2024, iMerit was named a Major Contributor in Everest Group’s inaugural PEAK Matrix for Data Annotation and Labeling Services, validating its position across autonomous mobility, healthcare and other verticals.

In 2023, iMerit released a data‑intelligence solution for the video‑game industry enabling ASR and sentiment‑analysis models for gamer behavior, addressing the rising need for content‑moderation data in live gaming communities.

This report on the Data Collection and Labeling market covers an extensive and detailed examination of service types, applications, end‑users, technology platforms, geographic regions and industry verticals. Specifically, it assesses segmentation by data type (text, audio, image, video, sensor/fusion), annotation methodology (manual, semi‑automated, fully automated), deployment mode (cloud, on‑premises, edge), and solution architecture (human‑in‑the‑loop services, AI‑assisted platforms). Regional coverage spans North America, Europe, Asia‑Pacific, South America, Middle East & Africa, with individual market volumes, adoption trends and enterprise behavior analyzed for each. Application domains charted in the report include autonomous vehicles, healthcare diagnostics & imaging, retail analytics & e‑commerce, natural language processing, robotics/automation and others. The focus also includes emerging or niche segments such as 3D‑sensor fusion annotation, data labeling for generative AI model training, multilingual annotation services and edge‑based labeling for IoT/industrial deployments. Industry focus areas extend to technology enterprises, automotive original equipment manufacturers (OEMs), healthcare providers, retail & consumer analytics firms, and public sector/government AI initiatives. The scope includes technology trends such as synthetic data integration, edge‑processing annotation, AI‑assisted quality assurance, crowd‑sourced annotation workforce models, and compliance‑driven labeling workflows (data privacy, bias mitigation, ESG requirements). Finally, the report addresses value‑chain coverage—from raw data collection, labelling, validation to delivery of training‑ready datasets—along with service provider profiles and vendor benchmarking to enable strategic decision‑making by industry professionals and enterprise buyers.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 4408.8 Million |

Market Revenue in 2032 | USD 24326.85 Million |

CAGR (2025 - 2032) | 23.8% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Appen, Lionbridge AI, iMerit, CloudFactory, TELUS International, Alegion, Shaip, Cloud Labs, Samasource, Clickworker |

Customization & Pricing | Available on Request (10% Customization is Free) |