Reports

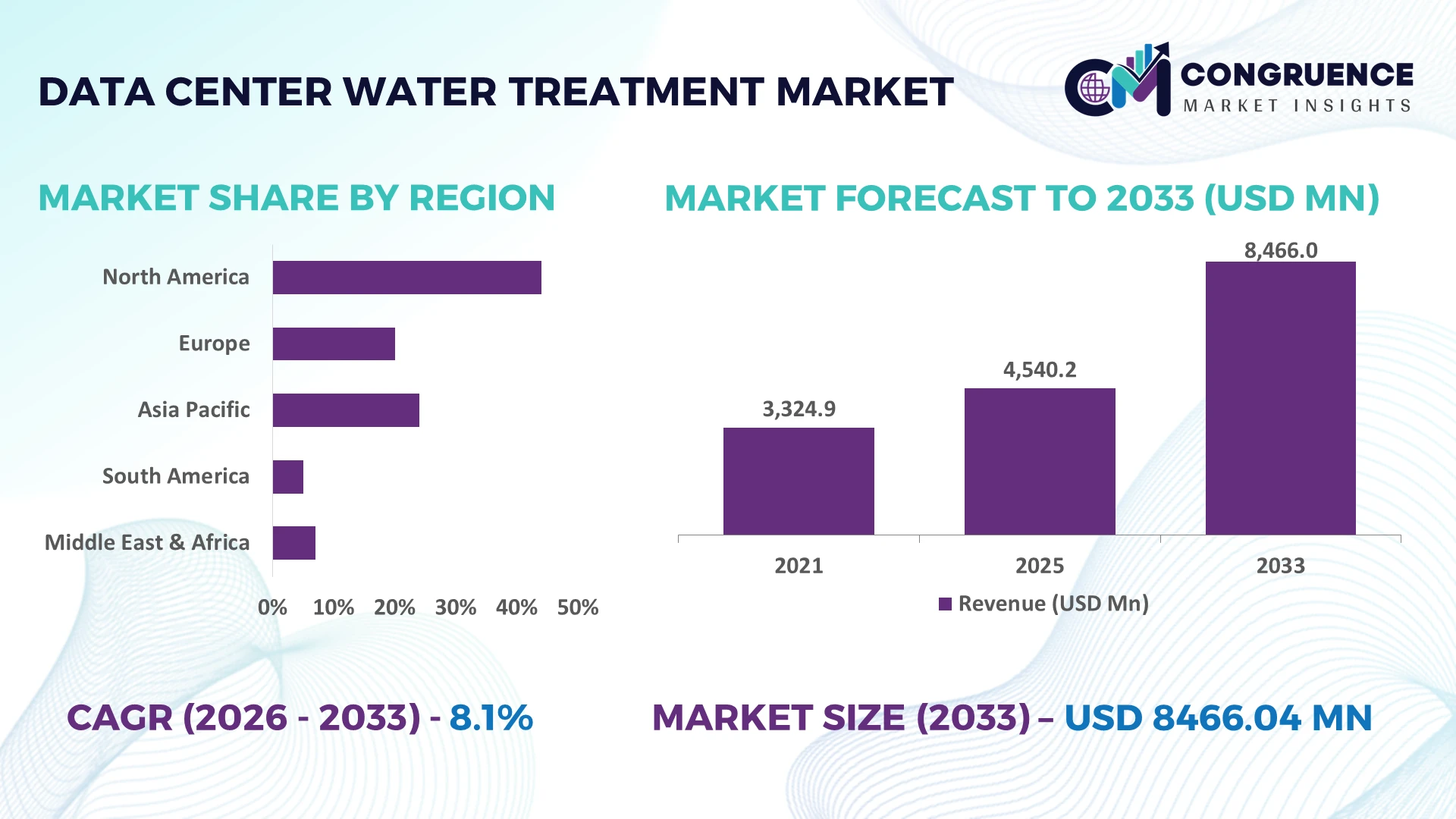

The Global Data Center Water Treatment Market was valued at USD 4540.2 Million in 2025 and is anticipated to reach a value of USD 8466.04 Million by 2033 expanding at a CAGR of 8.1% between 2026 and 2033. Growing AI-driven hyperscale data centers, stricter industrial water conservation standards, and wider deployment of closed-loop cooling systems are accelerating investments in advanced data center water treatment solutions.

The United States accounts for approximately 37% of global hyperscale data center capacity, supported by large-scale cloud infrastructure investments and AI computing expansion, while China holds nearly 24% through government-backed digital infrastructure programs and manufacturing-led digitalization. Following continued semiconductor supply chain realignment across North America and Asia in 2026, operators are prioritizing high-efficiency water treatment systems to improve operational resilience and reduce freshwater consumption.

Strategic investment in intelligent water recycling and high-recovery treatment technologies is becoming a key competitive differentiator for infrastructure developers and solution providers.

Market Size & Growth: USD 4540.2 Million in 2025, projected to reach USD 8466.04 Million by 2033 at a CAGR of 8.1%, driven by AI-enabled data center expansion and advanced cooling infrastructure.

Top Growth Drivers: AI computing workloads (+30%), water reuse adoption (+35%), and hyperscale facility expansion (+22%) continue to accelerate global market growth.

Short-Term Forecast: By 2028, advanced treatment systems are expected to reduce cooling-water consumption by 18% while improving operating efficiency by 15%.

Emerging Technologies: AI-powered monitoring, membrane filtration, and digital water management platforms improve treatment performance by over 25%.

Regional Leaders: North America approaches USD 3.2 Billion, Asia Pacific exceeds USD 2.7 Billion, and Europe reaches nearly USD 1.5 Billion, supported by sustainable infrastructure expansion.

Consumer/End-User Trends: More than 62% of newly developed hyperscale facilities integrate intelligent water recycling systems during project implementation.

Pilot/Case Example: A 2026 hyperscale deployment achieved a 30% reduction in freshwater consumption through automated water treatment and recycling technologies.

Competitive Landscape: Leading suppliers collectively account for approximately 42% of the global market, with Veolia, Xylem, Ecolab, Kurita Water Industries, and SUEZ maintaining strong industry positions.

Regulatory & ESG Impact: Water stewardship initiatives reduce freshwater withdrawal by nearly 20% while supporting compliance with stricter environmental regulations.

Investment & Funding: More than USD 6 Billion has been directed toward sustainable digital infrastructure, emphasizing strategic partnerships, capacity expansion, and resilient supply chains.

Innovation & Future Outlook: High-recovery filtration, predictive automation, and zero-liquid-discharge technologies are strengthening next-generation global data center sustainability strategies.

Advanced Data Center Water Treatment solutions are gaining wider adoption across hyperscale, colocation, and enterprise facilities as operators focus on improving water efficiency and infrastructure reliability. Intelligent monitoring platforms, high-performance membrane systems, and automated chemical dosing enhance treatment effectiveness by nearly 25% while supporting evolving environmental compliance requirements. Continued regional manufacturing expansion and resilient supply-chain strategies are reinforcing long-term technology deployment, setting the stage for deeper strategic market analysis.

The Data Center Water Treatment Market has become strategically important as hyperscale operators, colocation providers, and enterprise data center owners prioritize water resilience alongside computing performance. Infrastructure modernization, AI-driven server deployment, and tightening water-use regulations are reshaping investment priorities, making advanced treatment systems an operational requirement rather than an environmental add-on. This shift is strengthening competition among technology providers offering integrated monitoring, water reuse, and intelligent treatment platforms.

Modern membrane-based treatment and AI-enabled monitoring systems improve water recovery efficiency by nearly 25% while lowering chemical consumption by around 15% compared with conventional filtration methods. The United States continues to lead large-scale hyperscale deployments, whereas Singapore emphasizes high-efficiency water reuse because of limited freshwater availability. Over the next two to three years, more than 60% of newly commissioned hyperscale facilities are expected to integrate digital water management platforms, reflecting a clear transition toward automated infrastructure operations.

A 2026 hyperscale deployment incorporating intelligent water recycling and predictive monitoring reduced freshwater intake by approximately 30% while improving cooling reliability. Technology providers are expanding strategic partnerships with engineering firms and cooling system manufacturers to deliver integrated solutions. Organizations capable of combining water efficiency, operational intelligence, and regulatory compliance will strengthen long-term competitive positioning as sustainable digital infrastructure becomes a critical investment priority.

Rapid deployment of AI computing clusters is increasing cooling intensity and accelerating investment in advanced water treatment systems. Nearly 35% of new hyperscale facilities now incorporate water recycling technologies during project development, while intelligent monitoring platforms improve treatment efficiency by approximately 25%. In the United States, stricter water conservation requirements for large industrial facilities are encouraging adoption of high-recovery treatment technologies. This regulatory and operational shift is reducing dependence on freshwater resources while improving infrastructure resilience. Companies are responding through partnerships with cooling technology providers, expanded manufacturing capacity, and development of automated treatment platforms that optimize water quality, lower operating costs, and support long-term infrastructure sustainability.

Advanced membrane filtration, intelligent monitoring systems, and automated treatment equipment increase initial project costs by nearly 20%, creating financial barriers for mid-sized data center operators. Approximately 30% of existing facilities continue using legacy water management infrastructure that requires costly retrofitting to support modern treatment technologies. Supply-chain concentration for specialized filtration membranes and industrial sensors also extends procurement timelines in several manufacturing hubs. Companies are reducing these risks through localized sourcing strategies, long-term supplier agreements, and modular treatment architectures that simplify phased deployment. Improving interoperability between existing cooling systems and advanced treatment technologies remains essential for maintaining project profitability and deployment consistency.

Digital water management platforms, predictive analytics, and advanced recovery technologies are creating new opportunities for infrastructure optimization. Automated monitoring solutions reduce maintenance interventions by nearly 22%, while high-recovery treatment systems enable water reuse rates exceeding 80% in advanced facilities. Japan and the United Arab Emirates are increasing investment in water-efficient digital infrastructure to support expanding AI and cloud computing capacity. Technology suppliers are accelerating research into low-energy filtration, smart sensors, and automated chemical optimization while strengthening partnerships across the cooling ecosystem. Companies delivering integrated treatment, analytics, and recycling capabilities will secure a stronger position as sustainable infrastructure becomes a competitive procurement criterion.

Deploying advanced water treatment solutions consistently across hyperscale, enterprise, and edge facilities remains a significant execution challenge. More than 40% of existing facilities operate with infrastructure designed before intelligent water optimization became standard, increasing integration complexity and deployment costs. Skilled water management specialists remain in limited supply, while evolving environmental compliance requirements continue raising operational expectations. In countries such as Germany, increasingly rigorous sustainability standards require continuous performance monitoring and reporting across digital infrastructure. Companies must strengthen engineering capabilities, invest in workforce development, and collaborate with automation and cooling technology partners to ensure reliable, scalable, and compliant water treatment operations across expanding data center networks.

AI-Driven Water Optimization AI-enabled monitoring platforms are now being integrated into more than 55% of newly commissioned hyperscale facilities, improving treatment accuracy by nearly 25% and reducing manual intervention by around 30%. Growing AI server density is increasing cooling complexity, prompting operators in the United States to automate water quality management. Solution providers are expanding software partnerships and embedding predictive analytics into treatment systems to improve operational continuity and reduce maintenance costs.

Water Reuse Becomes Standard Closed-loop recycling systems now achieve water recovery rates above 80% in advanced installations, while freshwater consumption declines by approximately 20% following system upgrades. Tightening industrial water-use regulations and local permitting requirements are accelerating deployment across Singapore and other water-constrained markets. Equipment manufacturers are scaling integrated recycling technologies and modular treatment platforms to help operators meet sustainability targets without compromising cooling performance.

Modular Treatment Infrastructure Expands Prefabricated water treatment units reduce on-site installation time by nearly 35% while improving deployment flexibility across hyperscale and edge facilities. Standardized system architecture simplifies maintenance and supports faster infrastructure expansion as semiconductor supply chains stabilize during 2026. Companies are increasing investments in modular manufacturing, localized assembly, and engineering partnerships to shorten delivery cycles and improve project execution.

Digital Compliance and Monitoring More than 60% of enterprise operators are implementing continuous water monitoring to strengthen environmental reporting and operational transparency. Automated compliance platforms reduce reporting workloads by approximately 40% while enabling faster response to changing water quality conditions. As regulatory oversight expands in Germany and the United States, technology providers are integrating intelligent sensors, cloud-based dashboards, and remote diagnostics into complete water treatment ecosystems, creating a competitive advantage through data-driven infrastructure management.

Reverse Osmosis Systems remain the leading segment because of their superior contaminant removal efficiency, scalability, and compatibility with hyperscale cooling infrastructure. More than 45% of large-scale facilities deploy reverse osmosis as the primary treatment process to maintain stable water quality and extend equipment life. Filtration Systems continue to serve as essential pre-treatment solutions, while Water Softening Systems remain widely deployed in locations with high mineral content to minimize scaling and improve cooling performance.

UV Disinfection Systems represent the fastest-growing segment as operators increasingly reduce chemical dependency while improving biological contamination control. Adoption of UV-based treatment has increased by approximately 28% across newly developed facilities because of lower maintenance requirements and stronger environmental performance. Chemical Treatment Systems continue supporting corrosion and microbial control through integrated treatment programs rather than standalone deployment. Companies are expanding membrane innovation, strengthening OEM partnerships, and developing intelligent treatment platforms that combine multiple technologies to improve operational reliability and reduce lifecycle costs.

Cooling Water Treatment accounts for the largest share of market demand because uninterrupted cooling performance directly influences server reliability and energy efficiency. More than 65% of advanced facilities prioritize continuous monitoring and treatment of cooling water to minimize scaling, corrosion, and biological fouling. Cooling Towers remain a critical application in large campuses, while Chilled Water Systems continue expanding with increasing deployment of high-density computing infrastructure requiring tighter thermal management.

Water Recycling is the fastest-growing application as operators target freshwater reduction and regulatory compliance. Advanced recycling technologies now enable water recovery rates exceeding 80% in selected hyperscale installations, while automated monitoring improves treatment consistency by approximately 22%. Boiler Water Treatment maintains strategic importance in facilities supporting combined utility infrastructure. Companies are integrating intelligent automation, digital monitoring, and recycling technologies into unified water management platforms to improve operational efficiency and strengthen long-term sustainability performance.

Cloud Service Providers represent the largest end-user segment because of continuous expansion of hyperscale campuses supporting AI, cloud computing, and enterprise digital services. Approximately 60% of newly commissioned large-scale facilities are operated by cloud providers requiring advanced water treatment for uninterrupted cooling operations and regulatory compliance. Enterprise Data Centers continue upgrading existing infrastructure through phased modernization, while Government Data Centers emphasize resilient and secure utility systems supporting mission-critical operations.

Colocation Providers are the fastest-growing end-user segment as enterprises increasingly outsource digital infrastructure to specialized operators. Adoption of intelligent water management platforms has increased by nearly 27% among major colocation providers seeking operational efficiency and sustainability differentiation. Telecommunications facilities continue deploying advanced treatment systems alongside edge computing expansion to improve infrastructure reliability. Companies are responding through customized treatment solutions, strategic engineering partnerships, flexible service agreements, and integrated digital monitoring platforms tailored to diverse operational requirements.

North America accounted for the largest market share at 39.4% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.4% between 2026 and 2033.

AI Infrastructure Driving Advanced Water Management

North America maintains the leading position due to its high concentration of hyperscale data centers, advanced cloud infrastructure, and rapid AI computing deployment. Large operators are accelerating investments in intelligent water treatment systems to improve cooling reliability while meeting stricter environmental compliance requirements. More than 55% of hyperscale facilities in the region now incorporate automated water quality monitoring, while water recycling integration continues expanding across new developments. Continued investment in liquid cooling infrastructure and digital water management platforms is strengthening demand for high-performance filtration, reverse osmosis, and intelligent treatment technologies. Technology providers are expanding engineering partnerships and localized service capabilities to support increasingly complex digital infrastructure projects.

United States Market Outlook: The United States remains the largest country market, supported by the world's highest concentration of hyperscale facilities and continuous investment in AI infrastructure. Nearly 37% of global hyperscale capacity is located in the country, encouraging rapid deployment of advanced water treatment technologies. Operators continue modernizing cooling infrastructure through intelligent monitoring, water recycling, and predictive maintenance while technology suppliers expand domestic manufacturing, engineering support, and long-term service partnerships.

Sustainability Standards Reshaping Infrastructure Design

Europe continues strengthening its market position through strict environmental regulations, sustainable infrastructure investment, and modernization of digital facilities. Growing emphasis on water conservation has accelerated adoption of advanced treatment technologies, automated monitoring, and water reuse systems across major enterprise and colocation developments. Approximately 48% of newly developed facilities incorporate enhanced water efficiency objectives during design and construction. Companies are deploying integrated treatment platforms to improve regulatory compliance while reducing operational resource consumption. Engineering firms are also increasing collaboration with cooling technology providers to optimize long-term infrastructure performance.

Germany Market Outlook: Germany represents the region's most strategically important market because of its advanced industrial ecosystem, expanding colocation sector, and strong sustainability framework. Enterprise operators continue investing in intelligent cooling infrastructure supported by advanced filtration and recycling technologies. More than 30% of newly commissioned high-capacity facilities emphasize integrated environmental monitoring, encouraging suppliers to strengthen local engineering capabilities and technology partnerships.

Large-Scale Digital Infrastructure Expansion

Asia-Pacific is experiencing the fastest deployment of advanced water treatment systems as cloud computing, AI infrastructure, and industrial digitalization accelerate across major economies. China, India, Japan, and Singapore continue expanding hyperscale and enterprise facilities requiring efficient cooling water management. Nearly 45% of recently announced large-scale projects across the region include intelligent water optimization technologies from the planning stage. Manufacturers are increasing localized production of treatment equipment while engineering firms expand regional deployment capabilities. Continued digital infrastructure investment and improved supply-chain resilience are strengthening long-term demand for integrated water treatment solutions.

China Market Outlook: China leads regional deployment through extensive digital infrastructure development, strong manufacturing capacity, and government-supported technology expansion. Approximately 24% of global hyperscale capacity is located in China, increasing demand for advanced water treatment systems that improve cooling efficiency and environmental performance. Domestic companies continue expanding equipment manufacturing, automation capabilities, and strategic partnerships to support rapidly growing cloud and AI infrastructure projects.

Cloud Expansion Supporting Infrastructure Modernization

South America is steadily strengthening its market position through increasing cloud adoption, enterprise digital transformation, and modernization of regional data center infrastructure. Brazil and neighboring countries are investing in higher-capacity facilities that require efficient cooling water management and improved operational resilience. Nearly 20% of newly planned enterprise facilities incorporate advanced treatment and monitoring technologies to improve long-term efficiency. Infrastructure limitations remain in selected markets, encouraging modular deployment strategies and localized engineering partnerships. Equipment suppliers are expanding regional technical support to improve implementation speed and operational reliability.

Brazil Market Outlook: Brazil remains the leading country market due to its expanding cloud ecosystem, improving digital infrastructure, and concentration of enterprise data centers. Growing investment in colocation capacity is increasing demand for intelligent water treatment technologies capable of supporting reliable cooling operations. International technology providers continue strengthening partnerships with local engineering firms while expanding after-sales service and technical integration capabilities.

Water Security Driving Infrastructure Investment

The Middle East & Africa market is expanding as governments and private investors accelerate digital infrastructure development while prioritizing efficient water utilization. Large hyperscale and enterprise facilities increasingly deploy advanced treatment systems to address water scarcity and improve long-term cooling reliability. More than 35% of recently announced large-scale projects integrate water recycling technologies during infrastructure planning. Digital transformation initiatives, smart city programs, and continued investment in cloud infrastructure are encouraging adoption of intelligent water management platforms. Companies are strengthening regional partnerships and expanding technical support capabilities to improve deployment quality and operational performance.

United Arab Emirates Market Outlook: The United Arab Emirates leads the regional market through sustained investment in hyperscale infrastructure, cloud services, and smart city initiatives. Advanced cooling technologies and water-efficient treatment systems are becoming standard across newly developed facilities as operators target higher sustainability performance. Continued infrastructure modernization and international technology partnerships are strengthening the country's position as a regional hub for advanced digital infrastructure deployment.

The competitive landscape is led by Veolia, Xylem, Ecolab, Kurita Water Industries, and SUEZ, which compete directly with regional engineering firms, specialized membrane suppliers, and industrial water technology providers for hyperscale and enterprise data center projects. The top five players collectively account for approximately 42% of the global market, creating competition between technology-driven global leaders and cost-focused regional integrators. Performance differentiation depends on intelligent automation, water recovery efficiency, deployment speed, and lifecycle service capabilities rather than equipment pricing alone. Advanced treatment platforms improve operational efficiency by nearly 25%, while predictive monitoring reduces maintenance requirements by approximately 30%, making technology integration a decisive purchasing factor. Companies are expanding through strategic partnerships with cooling infrastructure providers, localized manufacturing, digital service platforms, and vertically integrated engineering capabilities. Competition is shifting toward integrated water management ecosystems as AI-driven facilities demand higher operational resilience and regulatory compliance. High technical qualification requirements and long customer validation cycles remain major entry barriers. Success depends on delivering scalable, intelligent, and highly reliable treatment solutions with strong lifecycle support.

Veolia

Xylem Inc.

Ecolab Inc.

Kurita Water Industries Ltd.

SUEZ

Evoqua Water Technologies

Pentair plc

DuPont Water Solutions

Solenis

Thermax Limited

Aquatech International LLC

Pall Corporation

Culligan International

Lenntech B.V.

Advanced membrane filtration, AI-based monitoring, and automated chemical dosing represent the core technologies transforming the Data Center Water Treatment Market. More than 55% of newly commissioned hyperscale facilities deploy intelligent monitoring platforms that improve treatment accuracy by approximately 25% while reducing manual inspection requirements by nearly 30%. Digital water analytics are increasingly integrated with building management and cooling control systems, enabling faster operational decisions and greater infrastructure reliability.

Emerging technologies include high-recovery reverse osmosis, UV disinfection, predictive maintenance platforms, and digital twin-enabled water optimization. Compared with conventional treatment systems, AI-enabled solutions reduce chemical consumption by around 15% and improve water recovery efficiency by nearly 20%. Cloud service providers and hyperscale operators gain the greatest competitive advantage because integrated treatment platforms improve cooling consistency while supporting environmental compliance. Modular treatment systems are also accelerating deployment across edge and colocation facilities through standardized infrastructure design.

Between 2026 and 2028, intelligent automation, real-time sensor networks, and zero-liquid-discharge technologies will reshape infrastructure planning. Deployment of automated water management platforms is expected to exceed 65% across newly developed hyperscale projects. Companies investing early in integrated digital treatment ecosystems, advanced filtration innovation, and predictive operational intelligence will secure stronger competitive differentiation, lower operating costs, and greater resilience against tightening water management requirements.

April 2026 Veolia launched its Data Center Resource 360 platform, integrating water, energy, and waste management into a unified offering for hyperscale facilities. The solution targets up to 75% water footprint reduction and 95% waste recycling, strengthening sustainable infrastructure strategies for AI-driven data centers. Source: Veolia

April 2026 Veolia and Amazon announced a collaboration to deploy reclaimed wastewater for cooling at Amazon's Mississippi data center. The project is designed to reuse more than 83 million gallons of water annually, improving local water resilience while advancing large-scale sustainable cooling operations. Source: Veolia

May 2025 Veolia agreed to acquire the remaining 30% stake in Water Technologies and Solutions, securing full ownership while adding approximately USD 750 million in new industrial contracts. The move strengthens integrated water technology capabilities serving semiconductor and data center customers. Source: Reuters

June 2026 Xylem expanded its long-term partnership with Dow to design, build, and operate advanced industrial water reuse systems supporting the Path2Zero project. The integrated solution improves freshwater efficiency through full-cycle treatment and reinforces Xylem's leadership in large-scale water infrastructure. Source: Xylem

The report provides comprehensive coverage of the Data Center Water Treatment Market across Reverse Osmosis Systems, Filtration Systems, Water Softening Systems, UV Disinfection Systems, and Chemical Treatment Systems. It evaluates Cooling Water Treatment, Chilled Water Systems, Cooling Towers, Boiler Water Treatment, and Water Recycling applications while assessing demand across Cloud Service Providers, Colocation Providers, Enterprise Data Centers, Government Data Centers, and Telecommunications. More than 60% of new hyperscale facilities now integrate intelligent water management, reflecting rapid technology adoption and evolving infrastructure priorities.

The analysis covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting regional deployment patterns, technology adoption, investment priorities, and competitive positioning between 2026 and 2033. It examines automation, AI-enabled monitoring, membrane technologies, digital water management, and sustainability-driven infrastructure modernization while profiling leading industry participants and emerging innovators. The report supports investment evaluation, expansion planning, supplier benchmarking, partnership strategy, risk assessment, and long-term decision-making across the global digital infrastructure ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 4540.2 Million |

Market Revenue in 2033 | USD 8466.04 Million |

CAGR (2026 - 2033) | 8.1% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Veolia, Xylem Inc., Ecolab Inc., Kurita Water Industries Ltd., SUEZ, Evoqua Water Technologies, Pentair plc, DuPont Water Solutions, Solenis, Thermax Limited, Aquatech International LLC, Pall Corporation, Culligan International, Lenntech B.V. |

Customization & Pricing | Available on Request (10% Customization is Free) |