Reports

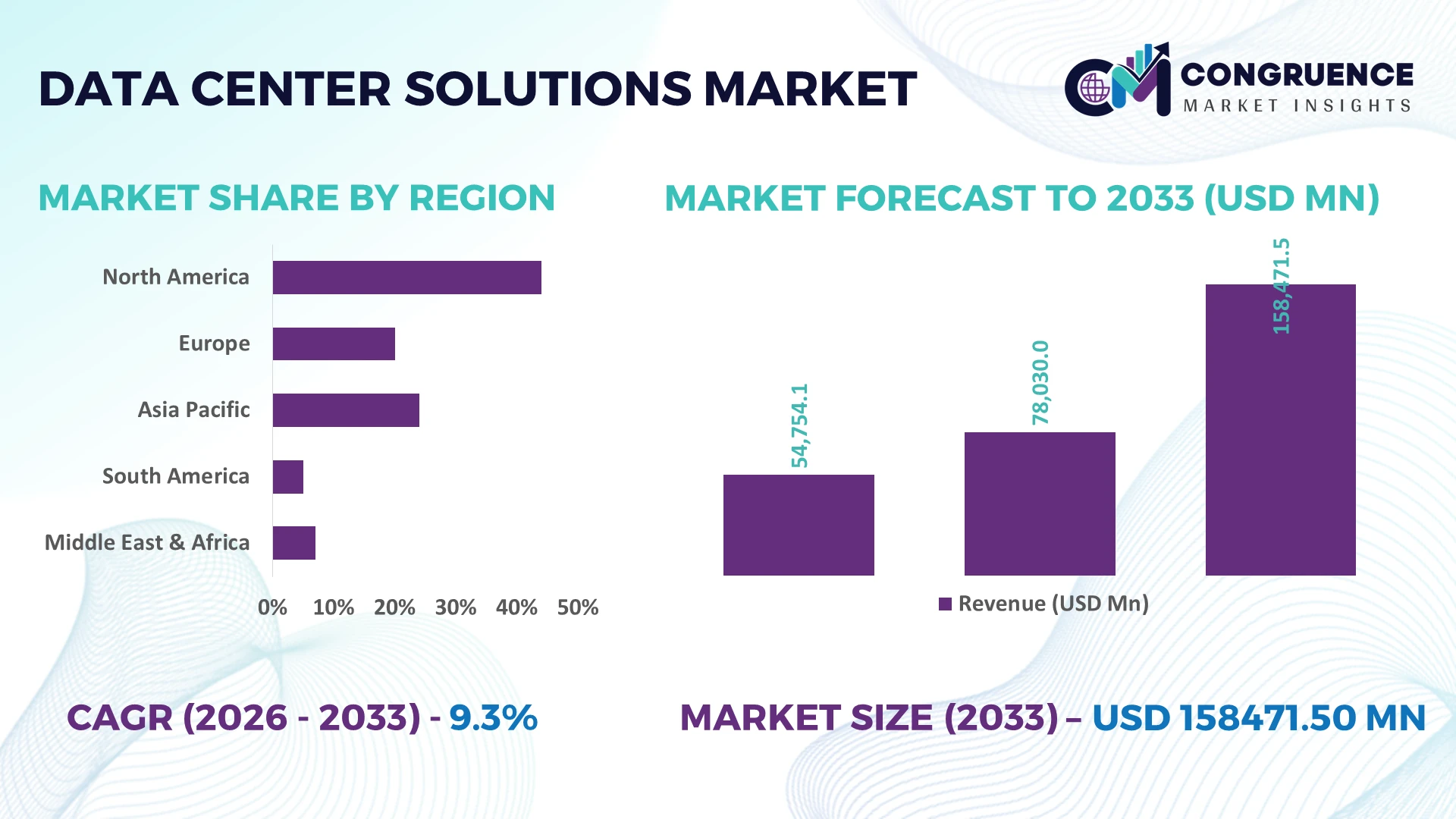

The Global Data Center Solutions Market was valued at USD 78030 Million in 2025 and is anticipated to reach a value of USD 158471.5 Million by 2033 expanding at a CAGR of 9.26% between 2026 and 2033. Enterprise AI deployments, hyperscale infrastructure expansion, liquid cooling adoption, and accelerated edge computing investments are driving sustained growth across advanced data center solutions.

The United States leads the global market with approximately 38% of installed hyperscale data center capacity, supported by multi-billion-dollar digital infrastructure investments, cloud providers, semiconductor manufacturing, and AI workloads. Compared with Germany, where energy-efficiency regulations shape deployment strategies, the U.S. continues faster capacity expansion, while over 65% of new facilities integrate advanced automation and intelligent energy management. Ongoing AI infrastructure competition and semiconductor supply-chain realignment continue influencing deployment priorities across major economies.

Organizations prioritizing scalable, energy-efficient, and AI-ready infrastructure will secure stronger operational resilience and long-term competitive advantage.

Market Size & Growth: USD 78030 Million (2025) to USD 158471.5 Million (2033) at 9.26% CAGR, driven by AI infrastructure expansion and hyperscale deployments.

Top Growth Drivers: AI workloads (+42%), edge computing (+31%), and liquid cooling adoption (+28%) accelerate global infrastructure modernization.

Short-Term Forecast: By 2028, intelligent infrastructure management improves operational efficiency by 25% while reducing energy costs by 18%.

Emerging Technologies: AI orchestration, liquid cooling, and autonomous infrastructure management improve utilization by over 30%.

Regional Leaders: North America leads above USD 60 Billion, Asia-Pacific exceeds USD 48 Billion, Europe surpasses USD 32 Billion with sustainable facility expansion.

Consumer/End-User Trends: More than 70% of enterprises prioritize hybrid cloud-enabled, AI-ready data center environments.

Pilot/Case Example: 2026 AI-enabled facility modernization improved cooling efficiency by 35% and reduced downtime by 22%.

Competitive Landscape: Top providers hold nearly 45% share, supported by Schneider Electric, Vertiv, Siemens, ABB, and Eaton.

Regulatory & ESG Impact: Advanced energy optimization lowers facility emissions by approximately 20% while supporting stricter efficiency compliance.

Investment & Funding: Global investments exceed USD 90 Billion, driven by hyperscale expansion, strategic partnerships, and regional capacity additions.

Innovation & Future Outlook: Modular AI-ready architectures and digital twins strengthen operational resilience amid evolving semiconductor supply-chain diversification.

Demand for Data Center Solutions is expanding across hyperscale cloud platforms, AI training clusters, colocation facilities, and enterprise digital transformation projects. Advanced liquid cooling, software-defined infrastructure, and AI-powered monitoring continue improving operational efficiency, with automated management deployed in over 60% of new facilities. Increasing grid optimization requirements and resilient supply-chain planning are strengthening investment priorities, setting the stage for deeper strategic market evaluation.

Data Center Solutions have become a strategic foundation for enterprise competitiveness as organizations prioritize AI-ready infrastructure, cloud-native operations, and resilient digital ecosystems. Infrastructure modernization, semiconductor supply-chain diversification, and stricter energy-performance requirements are reshaping investment priorities across hyperscale operators and enterprise facilities. More than 60% of newly commissioned data center capacity now incorporates intelligent automation and software-defined management to improve asset utilization while supporting increasingly complex computing workloads.

AI-enabled infrastructure management delivers up to 30% lower energy consumption and nearly 40% faster workload optimization than conventional monitoring platforms, reducing operational overhead while improving system resilience. The United States continues leading hyperscale deployments through advanced AI infrastructure investments, whereas Japan emphasizes high-density, energy-efficient facilities optimized for limited land availability and grid reliability. Over the next two to three years, automated operations are expected to exceed 70% adoption across new enterprise-scale facilities, supported by expanding liquid cooling integration and predictive maintenance technologies.

A recent enterprise deployment integrating AI-driven workload orchestration with liquid cooling reduced unplanned downtime by 25% while improving rack utilization by 20%. Providers are expanding strategic partnerships with semiconductor manufacturers, utility operators, and cloud service providers to accelerate infrastructure deployment and strengthen supply resilience. Organizations that combine scalable digital infrastructure with intelligent energy optimization will establish stronger competitive positioning, lower operating costs, and greater long-term operational flexibility.

Rapid expansion of AI computing, hyperscale cloud infrastructure, and digital enterprise operations continues to reshape investment priorities across the Data Center Solutions Market. More than 68% of enterprise infrastructure projects now incorporate AI-enabled management platforms, while liquid cooling deployments improve thermal efficiency by approximately 30% and reduce energy consumption by nearly 20%. The United States continues expanding domestic semiconductor manufacturing and digital infrastructure, strengthening supply-chain resilience for high-performance computing facilities. Leading vendors are responding through modular facility expansion, AI software integration, and strategic technology partnerships that shorten deployment cycles. An important operational advantage is the convergence of power management and intelligent automation, enabling higher rack density without proportionally increasing facility footprints or energy intensity.

High capital requirements, utility constraints, and component supply concentration continue restricting deployment speed across large-scale facilities. Energy infrastructure accounts for nearly 35% of total project expenditure, while power equipment lead times remain 25–40% longer than historical averages in several industrial markets. Germany and other European countries face stricter grid capacity and environmental compliance requirements, delaying large infrastructure projects despite strong digital demand. Companies are reducing operational exposure by diversifying supplier networks, localizing procurement, and securing long-term equipment agreements. A critical business implication is that power availability increasingly determines project viability, making energy access as important as computing capacity in site selection strategies.

Edge computing, autonomous infrastructure management, and digital twin technologies are creating new commercial opportunities beyond traditional hyperscale deployments. More than 55% of industrial organizations are accelerating edge infrastructure adoption, while AI-driven workload optimization improves server utilization by approximately 28%. India is expanding digital infrastructure through enterprise cloud adoption and localized data processing requirements, encouraging investments in distributed facilities closer to end users. Technology providers are strengthening ecosystems through software partnerships, modular solutions, and advanced cooling innovation to improve deployment flexibility. A notable strategic opportunity lies in integrating AI orchestration with renewable energy optimization, enabling lower operating costs while supporting resilient decentralized computing environments.

Managing high-density AI environments introduces growing operational complexity across cybersecurity, infrastructure integration, and specialized workforce development. AI-enabled facilities generate over 40% higher processing intensity than conventional enterprise environments, increasing demands on cooling, monitoring, and security architecture. Japan and the United States continue strengthening cybersecurity standards for critical digital infrastructure, requiring continuous compliance upgrades and resilient operational frameworks. Companies must expand investments in workforce training, zero-trust security architectures, and intelligent infrastructure management platforms while strengthening technology partnerships. The strongest competitive advantage will belong to operators capable of simultaneously scaling AI capacity, maintaining security resilience, and sustaining consistent operational performance across increasingly distributed infrastructure networks.

AI-Optimized Infrastructure Expansion: Enterprise facilities are redesigning infrastructure for AI-intensive computing, with more than 65% of newly deployed racks supporting high-density workloads and liquid cooling adoption increasing by nearly 30%. Semiconductor supply-chain localization is accelerating procurement flexibility in the United States, while operators expand automation partnerships to shorten deployment timelines, improve rack utilization, and reduce energy intensity across hyperscale and enterprise environments.

Intelligent Energy Management Growth: AI-powered energy optimization platforms are reducing facility power consumption by approximately 18% while predictive maintenance lowers equipment failures by nearly 25%. Stricter energy-efficiency regulations in Germany are encouraging advanced monitoring deployments, prompting providers to integrate digital twins, intelligent power distribution, and automated infrastructure controls that improve operational resilience without expanding physical footprints.

Edge Deployment Standardization: Edge computing deployments now account for over 35% of new distributed infrastructure projects, with deployment times reduced by approximately 22% through modular architectures and preconfigured networking platforms. Manufacturing and telecom enterprises in India are expanding localized processing capacity, while vendors strengthen ecosystem partnerships to deliver standardized deployment models that simplify lifecycle management and improve application responsiveness.

Integrated Security Automation Adoption: Unified physical and cybersecurity management platforms are gaining momentum, with more than 58% of enterprise operators integrating centralized security orchestration and automated compliance monitoring. Increasing regulatory oversight of critical digital infrastructure is accelerating zero-trust implementation, while providers restructure service portfolios around AI-assisted threat detection, enabling faster incident response and lower operational complexity across multi-site environments.

Infrastructure remains the leading segment because scalable computing architecture, storage integration, and workload flexibility form the foundation of every modern data center deployment. Nearly 42% of enterprise infrastructure investments are directed toward integrated infrastructure platforms supporting AI, cloud, and virtualization environments. Cooling Solutions represent the fastest-growing segment as high-density AI workloads increase thermal management requirements, with liquid cooling deployments expanding by approximately 30% annually across newly commissioned facilities. Power Solutions continue strengthening resilience through intelligent power distribution, while Networking Solutions enable low-latency connectivity and Security Solutions protect increasingly distributed digital environments. Vendors continue expanding modular portfolios, strategic partnerships, and integrated management software to improve deployment speed and lifecycle efficiency.

Investment priorities increasingly favor tightly integrated infrastructure ecosystems instead of isolated hardware deployments. Organizations are combining Infrastructure, Cooling, Power, Networking, and Security Solutions into unified operational platforms that reduce maintenance complexity by nearly 20% while improving utilization rates. Technology providers are responding through AI-enabled management software, modular expansion strategies, and interoperability-focused product development to strengthen enterprise adoption.

Cloud Computing remains the dominant application because enterprises continue consolidating digital workloads into scalable hybrid and multi-cloud environments. More than 70% of large organizations now operate hybrid cloud strategies, while automated infrastructure management improves resource utilization by approximately 28%. Edge Computing is the fastest-growing application as manufacturing, telecommunications, and smart city initiatives require localized processing with lower latency. Colocation continues expanding through enterprise outsourcing strategies, Enterprise IT maintains demand for mission-critical operations, and Disaster Recovery gains importance as resilience requirements become more stringent.

Demand is shifting toward flexible deployment models that integrate cloud, edge, and recovery capabilities within unified operating environments. Service providers are expanding automation platforms, AI-enabled orchestration, and regional deployment partnerships to improve operational continuity while reducing provisioning times by nearly 20%. This evolution strengthens long-term infrastructure resilience and supports increasingly distributed enterprise workloads.

IT & Telecom represents the largest end-user segment because cloud platforms, telecommunications networks, AI infrastructure, and digital services require continuous high-capacity computing environments. Nearly 45% of enterprise-scale deployments originate from this sector, while Healthcare is the fastest-growing end-user as digital diagnostics, medical imaging, and AI-assisted clinical systems increase secure computing requirements by more than 25%. BFSI continues investing in resilient infrastructure for transaction processing, Government expands sovereign digital infrastructure, and Retail strengthens omnichannel platforms through intelligent data management and analytics.

Enterprise purchasing behavior increasingly emphasizes integrated solutions rather than standalone infrastructure components. Solution providers are developing industry-specific platforms, expanding managed services, and forming ecosystem partnerships to improve deployment flexibility, cybersecurity, and operational efficiency. Customized offerings for regulated industries are strengthening competitive differentiation while supporting long-term digital transformation strategies across diverse enterprise environments.

North America accounted for the largest market share at 39.2% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a 10.8% between 2026 and 2033.

AI Infrastructure and Hyperscale Expansion Sustain Market Leadership

North America remains the largest regional market due to its concentration of hyperscale cloud providers, advanced semiconductor ecosystems, and enterprise digital infrastructure. The region contributes nearly 40% of global hyperscale capacity, supported by rapid deployment of AI-ready facilities and high-density computing environments. More than 65% of newly commissioned enterprise data centers incorporate liquid cooling or AI-enabled infrastructure management. Utility modernization, long-term power procurement agreements, and collaboration between technology providers and energy companies continue accelerating deployment while improving operational resilience. Companies are prioritizing modular construction, intelligent automation, and integrated infrastructure platforms to reduce implementation timelines and increase computing density without proportionally expanding facility footprints.

United States Market Outlook: The United States leads regional deployment through its extensive hyperscale ecosystem, AI infrastructure investments, and domestic semiconductor manufacturing expansion. Enterprise cloud providers continue developing multi-campus facilities supporting advanced AI workloads, while automation technologies improve infrastructure utilization by approximately 30%. Federal incentives encouraging semiconductor production and digital infrastructure modernization strengthen supply resilience, enabling operators to accelerate facility expansion while maintaining higher energy efficiency and operational reliability across mission-critical environments.

Energy Efficiency and Regulatory Modernization Shape Deployment

Europe continues strengthening its market position through sustainability-focused infrastructure modernization and advanced regulatory frameworks. Approximately 24% of global enterprise data center modernization projects are concentrated across the region, supported by renewable energy integration and intelligent energy management systems. High-efficiency cooling technologies reduce facility power consumption by nearly 18%, while stricter environmental compliance encourages modernization rather than conventional capacity expansion. Operators increasingly deploy AI-powered infrastructure monitoring, modular power systems, and digital twins to optimize performance while meeting evolving operational and environmental standards.

Germany Market Outlook: Germany remains Europe's most influential market through its industrial digitalization strategy, manufacturing leadership, and robust enterprise cloud adoption. The country continues expanding energy-efficient facilities integrated with renewable electricity and advanced automation technologies. More than 60% of newly modernized enterprise facilities incorporate intelligent energy optimization platforms, enabling operators to balance regulatory compliance with operational performance while supporting industrial AI applications and secure enterprise computing environments.

Large-Scale Digital Infrastructure Accelerates Deployment

Asia-Pacific represents the fastest-evolving regional market, driven by digital transformation, cloud adoption, expanding AI investments, and rising enterprise connectivity requirements. The region accounts for approximately 31% of new global data center deployments, while modular infrastructure implementation reduces commissioning time by nearly 22%. Governments continue supporting domestic digital infrastructure through investment incentives and localized data processing initiatives. Providers are expanding edge computing facilities, intelligent networking platforms, and AI-enabled operations to accommodate increasing enterprise demand while improving deployment flexibility and operational efficiency.

China Market Outlook: China maintains a dominant position through extensive cloud infrastructure expansion, large-scale AI deployment, and advanced manufacturing capabilities supporting digital infrastructure equipment. National digital economy initiatives continue strengthening regional computing capacity, while intelligent infrastructure management improves operational efficiency across large enterprise campuses. More than half of newly deployed hyperscale facilities integrate advanced automation, enabling higher infrastructure utilization and stronger support for industrial digital transformation.

Enterprise Cloud Adoption Expands Regional Capacity

South America is experiencing steady market development as enterprise cloud migration, financial services modernization, and digital public services increase infrastructure requirements. The region represents approximately 5% of global deployment activity, while modular facility development shortens project implementation by nearly 20%. Connectivity improvements and strategic investments from international cloud providers continue expanding regional capacity despite power infrastructure limitations in selected markets. Operators increasingly deploy scalable infrastructure and intelligent monitoring solutions to improve reliability while managing operating costs across distributed enterprise environments.

Brazil Market Outlook: Brazil remains the region's leading market because of its large enterprise base, expanding financial technology sector, and increasing cloud adoption. International operators continue investing in colocation and hyperscale facilities serving domestic and multinational organizations. AI-enabled infrastructure management and intelligent energy optimization improve operational performance, while stronger fiber connectivity supports growing enterprise demand for resilient, low-latency digital infrastructure across major metropolitan and industrial centers.

Digital Infrastructure Investment Reshapes Regional Ecosystems

The Middle East & Africa market is advancing through national digital transformation programs, cloud localization initiatives, and strategic infrastructure investment. Approximately 7% of new emerging-market data center projects are concentrated within the region, while intelligent infrastructure deployment improves operational efficiency by nearly 20%. Governments continue promoting sovereign digital infrastructure alongside international technology partnerships that strengthen cloud availability and enterprise computing capacity. Operators increasingly integrate renewable energy, modular infrastructure, and AI-enabled monitoring to support long-term operational sustainability in rapidly expanding digital economies.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional development through proactive digital infrastructure policies, advanced connectivity, and large-scale smart city initiatives. International cloud providers and colocation operators continue expanding local facilities to meet growing enterprise and government demand. Intelligent automation, renewable energy integration, and high-performance networking infrastructure enable faster deployment while strengthening the country's position as a regional hub for advanced digital services and AI-enabled computing.

Competition is led by Schneider Electric, Vertiv, Siemens, ABB, and Eaton, while regional infrastructure integrators and specialized cooling providers compete aggressively for enterprise modernization projects. Global technology leaders challenge regional solution providers through integrated platforms, whereas cost-focused manufacturers compete on deployment speed and localized service capabilities. The top five companies collectively control approximately 46% of the market. Competition centers on AI-ready infrastructure, energy optimization, and lifecycle services, with integrated management platforms improving operational efficiency by nearly 25% and modular deployment reducing installation timelines by approximately 20%. Vendors are expanding manufacturing capacity, forming semiconductor and cloud partnerships, strengthening software portfolios, and increasing vertical integration across power, cooling, and monitoring systems. The competitive landscape is shifting toward software-defined infrastructure and intelligent automation, reducing differentiation based solely on hardware performance. High capital requirements, technical certification, and long-term customer relationships remain significant entry barriers. Sustained success depends on combining AI-enabled operations, resilient supply chains, rapid deployment, and integrated infrastructure ecosystems.

Schneider Electric

Vertiv

Siemens

ABB

Eaton

Cisco Systems

Hewlett Packard Enterprise (HPE)

Dell Technologies

Huawei Technologies

Legrand

Rittal

Johnson Controls

Artificial intelligence, software-defined infrastructure, liquid cooling, and digital twin platforms are redefining modern Data Center Solutions. More than 60% of newly commissioned enterprise facilities deploy AI-enabled infrastructure monitoring, while intelligent workload orchestration improves server utilization by approximately 30%. Compared with conventional rule-based management, AI-driven operations reduce energy consumption by nearly 20% and shorten incident response times by over 35%. Hyperscale operators and cloud providers gain the greatest competitive advantage because these technologies enable higher rack density and improved infrastructure resilience without proportional increases in operating costs.

Emerging technologies are expanding beyond automation into predictive maintenance, smart power distribution, and edge-native infrastructure management. Digital twins improve maintenance planning accuracy by approximately 25%, while liquid cooling supports up to 40% greater compute density than traditional air-cooling environments. Around half of new AI-focused deployments integrate intelligent cooling with software-defined resource allocation, enabling operators to optimize computing performance, reduce downtime, and simplify infrastructure lifecycle management through unified operational platforms.

Between 2026 and 2028, autonomous infrastructure orchestration, AI-assisted cybersecurity, and integrated energy optimization will become standard deployment priorities. Technology vendors combining intelligent software, advanced cooling, and resilient power management will strengthen enterprise adoption and long-term customer retention. Organizations investing early in interoperable, AI-ready architectures will achieve faster infrastructure scaling, stronger operational resilience, and greater competitiveness as enterprise computing environments become increasingly distributed and performance intensive.

October 2025 Vertiv expanded its collaboration with NVIDIA by advancing 800 VDC power platform designs for next-generation AI factories, targeting commercial readiness for 2026 and future NVIDIA Rubin Ultra deployments. The new architecture supports significantly higher rack power densities, strengthening AI infrastructure scalability and deployment readiness. Source: vertiv.com

November 2025 Eaton announced the acquisition of Boyd Corporation's thermal business for USD 9.5 billion, significantly strengthening its liquid cooling portfolio for AI-driven data centers. The acquisition expands end-to-end thermal management capabilities and enhances competitive positioning across high-density digital infrastructure markets. Source: reuters.com

February 2026 Schneider Electric inaugurated its first Motivair liquid cooling manufacturing facility in India, establishing its third global production site for the technology. The expansion localizes advanced cooling production, strengthens supply-chain resilience, and positions India as a strategic manufacturing and export hub for AI-ready data center infrastructure. Source: se.com

March 2026 Vertiv partnered with Generate Capital to introduce Bring Your Own Power & Cooling (BYOP&C) solutions for U.S. data centers, integrating financing with modular infrastructure. The initiative accelerates deployment in power-constrained markets, enabling faster capacity delivery while improving infrastructure flexibility for hyperscale AI facilities. Source: vertiv.com

This report provides a comprehensive assessment of the Data Center Solutions Market between 2026 and 2033, covering infrastructure, power solutions, cooling solutions, networking solutions, and security solutions across diverse deployment environments. The analysis evaluates applications including colocation, cloud computing, enterprise IT, edge computing, and disaster recovery, together with demand trends across IT & Telecom, BFSI, Healthcare, Government, and Retail. Regional performance is assessed across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, supported by operational and technology adoption insights.

The report examines AI-enabled infrastructure, liquid cooling, software-defined management, intelligent power systems, automation, and cybersecurity integration while tracking deployment patterns across enterprise and hyperscale facilities. It profiles leading industry participants, competitive positioning, investment priorities, and technology strategies, helping stakeholders evaluate expansion opportunities, optimize infrastructure planning, benchmark competitive capabilities, and identify high-potential market segments through operational, regional, and end-user intelligence.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 78030 Million |

Market Revenue in 2033 | USD 158471.5 Million |

CAGR (2026 - 2033) | 9.26% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Schneider Electric, Vertiv, Siemens, ABB, Eaton, Cisco Systems, Hewlett Packard Enterprise (HPE), Dell Technologies, Huawei Technologies, Legrand, Rittal, Johnson Controls |

Customization & Pricing | Available on Request (10% Customization is Free) |