Reports

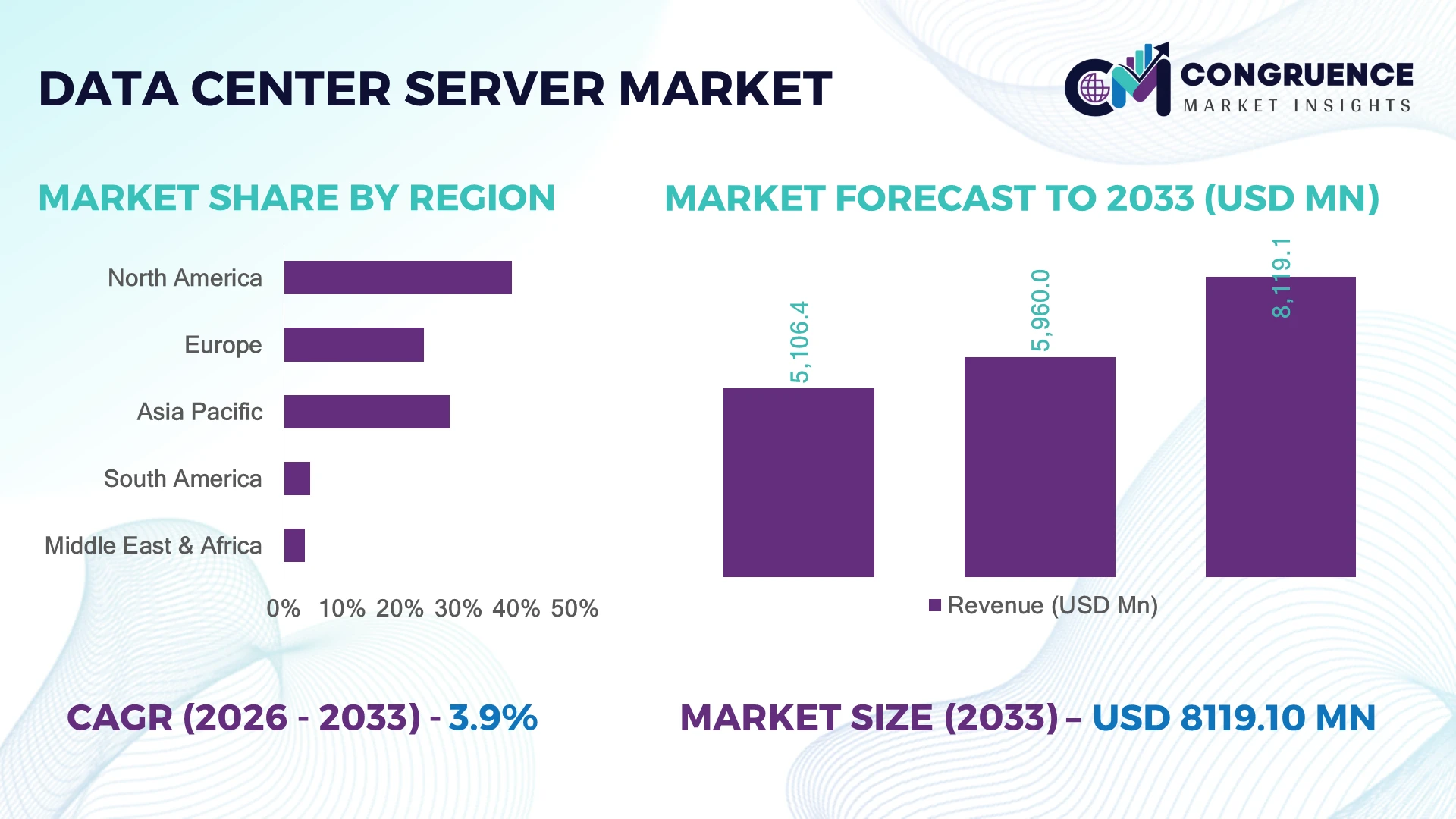

The Global Data Center Server Market was valued at USD 5,960.0 Million in 2025 and is anticipated to reach a value of USD 8,119.1 Million by 2033 expanding at a CAGR of 3.94% between 2026 and 2033. Growth is primarily driven by AI-ready server deployments, hyperscale data center expansion, and accelerated enterprise migration toward high-density computing infrastructure.

The United States dominates the global Data Center Server Market with approximately 38% of installed hyperscale server capacity, supported by over 5,400 operational data centers, multibillion-dollar cloud infrastructure investments, and strong adoption across AI, financial services, healthcare, and digital commerce. Compared with Germany's mature enterprise-focused infrastructure, the U.S. deploys significantly larger hyperscale clusters while benefiting from the CHIPS and Science Act, reinforcing advanced server manufacturing and next-generation computing capabilities.

Organizations that prioritize scalable, energy-efficient server platforms and resilient supply-chain partnerships will secure stronger operational performance and long-term competitive advantage.

Market Size & Growth: USD 5,960.0 Million in 2025 is projected to reach USD 8,119.1 Million by 2033 at 3.94% CAGR, supported by AI infrastructure expansion and hyperscale server modernization.

Top Growth Drivers: AI workload deployment (45%), enterprise cloud migration (39%), and high-density rack adoption (32%) continue accelerating infrastructure investments.

Short-Term Forecast: By 2028, server power efficiency improves by nearly 20%, while automated infrastructure management reduces maintenance downtime by approximately 15%.

Emerging Technologies: AI accelerators, liquid cooling, and composable infrastructure enable advanced, high-performance server environments for enterprise and hyperscale operators.

Regional Leaders: North America (~USD 2,850 Million), Asia Pacific (~USD 1,760 Million), and Europe (~USD 1,340 Million) lead through cloud expansion, sovereign infrastructure, and enterprise modernization amid global digital transformation.

Consumer/End-User Trends: More than 65% of hyperscale operators prioritize GPU-optimized server deployments for AI training and inference workloads.

Pilot/Case Example: In 2025, liquid-cooled AI server deployments reduced cooling energy consumption by nearly 30% in high-density data center environments.

Competitive Landscape: Dell Technologies holds approximately 17% market share alongside Hewlett Packard Enterprise, Lenovo, Supermicro, and Inspur in advanced server deployments.

Regulatory & ESG Impact: Energy-efficiency initiatives reduce facility power consumption by nearly 18%, supporting stricter sustainability and carbon reduction objectives.

Investment & Funding: More than USD 40 Billion in global investments supports hyperscale expansion, semiconductor partnerships, and resilient regional supply-chain development.

Innovation & Future Outlook: AI-native architectures, rack-scale computing, and modular server platforms strengthen operational flexibility and competitive digital infrastructure.

The Data Center Server Market is rapidly evolving as enterprises prioritize AI computing, hyperscale cloud expansion, and edge processing across financial services, healthcare, manufacturing, and telecommunications. Recent innovations include liquid-cooled high-density servers, GPU-accelerated platforms, and composable infrastructure that improve computing efficiency by nearly 25%. Ongoing semiconductor supply-chain diversification and regional manufacturing initiatives are reshaping procurement strategies while strengthening long-term infrastructure resilience, setting the stage for broader strategic transformation.

The Data Center Server Market has become strategically important because digital infrastructure now underpins AI adoption, enterprise cloud services, national digital resilience, and advanced computing capabilities. Organizations are expanding server capacity to support increasingly complex workloads while restructuring supply chains to reduce semiconductor dependency and improve deployment flexibility. Infrastructure modernization and sovereign computing initiatives continue strengthening long-term investment priorities across both public and private sectors.

Modern GPU-enabled servers deliver up to 35% higher workload efficiency than conventional CPU-centric platforms while reducing processing time for AI-intensive applications. North America maintains leadership through hyperscale deployments and cloud innovation, whereas Asia-Pacific records faster infrastructure rollouts driven by manufacturing expansion, digital transformation, and government-backed technology initiatives. Over the next two to three years, automated infrastructure management and intelligent workload orchestration are expected to reduce operational downtime by approximately 15% across large-scale facilities.

A practical example is the deployment of liquid-cooled AI server racks within hyperscale campuses, enabling higher rack density while lowering cooling energy requirements. Leading vendors are expanding manufacturing partnerships, regional assembly capabilities, and integrated hardware-software ecosystems to improve delivery resilience and deployment speed. Companies that combine energy-efficient server platforms with scalable AI-ready architectures will strengthen competitive positioning, improve operational performance, and establish lasting advantages in the global digital infrastructure landscape.

Enterprise AI deployment and hyperscale cloud expansion are fundamentally reshaping server procurement strategies. More than 65% of newly commissioned hyperscale facilities now prioritize GPU-optimized server infrastructure, while high-density rack deployments have increased by nearly 30% to support generative AI and advanced analytics workloads. The United States continues strengthening domestic semiconductor and server manufacturing through the CHIPS and Science Act, improving hardware availability and reducing strategic supply-chain dependence. This structural shift increases demand for modular, liquid-cooled, and energy-efficient server platforms capable of supporting higher computational intensity. In response, leading manufacturers are expanding production capacity, investing in AI-native server architectures, and forming technology partnerships with accelerator and cloud providers. Companies integrating scalable compute platforms with optimized thermal management are securing stronger enterprise contracts and long-term infrastructure leadership.

Persistent dependence on advanced semiconductor manufacturing and specialized server components continues limiting deployment flexibility. Nearly 75% of leading-edge AI processors originate from a limited group of fabrication facilities, while advanced memory and networking components account for over 40% of high-performance server hardware costs. Export controls affecting advanced computing technologies have further complicated procurement for several international markets, extending procurement timelines and inventory planning. These structural constraints increase capital requirements, delay infrastructure expansion, and compress operational margins for system integrators. To reduce exposure, server manufacturers are diversifying supplier networks, expanding localized assembly operations in countries such as Mexico and Vietnam, and negotiating long-term component agreements. Strengthening multi-source procurement strategies has become a critical operational priority for maintaining deployment consistency.

Rapid deployment of edge computing and AI inference workloads is creating new opportunities beyond traditional hyperscale environments. More than 55% of industrial organizations plan to process latency-sensitive workloads closer to operational assets, while intelligent edge deployments can reduce network traffic by approximately 35% through localized data processing. Japan's smart manufacturing initiatives and digital infrastructure investments are accelerating adoption of compact, high-performance server platforms across factories, transportation, and healthcare networks. Vendors are responding by developing modular edge servers, integrated AI accelerators, and remote lifecycle management capabilities that simplify distributed deployments. A less obvious opportunity lies in software-defined infrastructure, enabling enterprises to maximize server utilization while lowering hardware replacement frequency and improving long-term operational efficiency.

Deploying next-generation server infrastructure at enterprise scale requires balancing computing density, thermal performance, cybersecurity, and operational resilience. AI-ready server clusters can consume nearly 2× the power of conventional enterprise racks, while organizations report approximately 28% greater operational complexity when integrating heterogeneous CPU, GPU, and accelerator environments. In Germany, increasingly stringent energy-efficiency and cybersecurity compliance requirements add further complexity to infrastructure planning and lifecycle management. Without standardized orchestration and skilled technical teams, organizations risk inconsistent performance, prolonged deployment cycles, and reduced infrastructure utilization. Leading companies are addressing these challenges through intelligent infrastructure management software, advanced liquid-cooling technologies, workforce development programs, and strategic partnerships that combine hardware, networking, and cloud management into unified deployment ecosystems.

AI-Optimized Server Architectures Expand Enterprise infrastructure is rapidly shifting toward AI-ready server platforms, with more than 65% of new hyperscale deployments incorporating GPU-accelerated configurations and high-density rack designs. Average rack power capacity has increased by nearly 40% to accommodate advanced workloads, while liquid-cooling adoption continues accelerating. In response to growing AI infrastructure requirements and semiconductor transition cycles, vendors are expanding AI server portfolios, strengthening accelerator partnerships, and redesigning thermal management systems to improve deployment efficiency.

Supply Chains Become More Regionalized Global server manufacturers are restructuring production networks as over 45% of enterprise buyers prioritize diversified sourcing strategies following semiconductor disruptions and export-control adjustments. Assembly expansion across Mexico and Vietnam has shortened regional delivery timelines by approximately 18% while reducing logistics exposure. Companies are increasing localized manufacturing, qualifying multiple component suppliers, and adopting digital supply-chain monitoring to improve procurement resilience and inventory visibility.

Automation Reshapes Data Center Operations AI-driven infrastructure management platforms now automate nearly 55% of routine server administration tasks, while predictive maintenance reduces unexpected hardware failures by approximately 22%. Enterprises are integrating software-defined infrastructure, digital twins, and intelligent workload scheduling to optimize utilization. Server vendors are responding through platform integration, lifecycle management services, and automation partnerships that improve operational consistency while lowering manual intervention.

Energy-Efficient Infrastructure Accelerates Sustainability objectives and stricter efficiency requirements are encouraging deployment of advanced power management technologies, reducing server energy consumption by nearly 20% in optimized facilities. More than 35% of newly commissioned enterprise data centers now incorporate liquid cooling or heat-recovery systems. Equipment providers are redesigning server platforms with modular power architectures and intelligent monitoring capabilities, enabling operators to balance performance, compliance, and long-term operating costs.

Rack Servers remain the leading segment because they offer superior scalability, standardized deployment, and efficient integration into hyperscale and enterprise data center environments. They account for approximately 52% of server deployments, supported by high-density configurations and compatibility with AI accelerators, virtualization, and cloud-native workloads. Their modular architecture simplifies maintenance while maximizing rack utilization, making them the preferred choice for cloud providers and colocation operators. Blade Servers represent the fastest-growing segment, with adoption increasing by nearly 16% as organizations seek greater compute density and centralized infrastructure management for AI and high-performance computing applications. Tower Servers continue serving small and medium-sized enterprises requiring standalone computing environments with lower acquisition costs and simplified deployment. Micro Servers are gaining relevance for edge computing and lightweight distributed workloads because they reduce energy consumption by approximately 25% compared with conventional enterprise servers in selected applications. Vendors are expanding AI-compatible Rack Server portfolios, investing in Blade Server innovation, and enhancing modular product ecosystems to address evolving enterprise infrastructure requirements and changing investment priorities.

Cloud Computing remains the dominant application as enterprises continue migrating business-critical workloads to scalable digital infrastructure. Nearly 60% of newly deployed enterprise servers are configured for cloud-native environments supporting virtualization, AI processing, and containerized applications. Its leadership is reinforced by continuous investments from hyperscale cloud providers seeking greater processing efficiency and workload flexibility. Edge Computing represents the fastest-growing application, expanding rapidly as latency-sensitive industrial automation, autonomous systems, and IoT deployments require localized computing resources. Enterprise adoption of edge infrastructure has increased by approximately 30%, driven by real-time analytics and distributed AI workloads. Enterprise Data Centers maintain stable investment as organizations modernize legacy infrastructure to improve cybersecurity, automation, and workload consolidation. Colocation Data Centers continue expanding through enterprise outsourcing strategies that improve operational flexibility while reducing facility management complexity. Vendors are strengthening application-specific server configurations, expanding hybrid deployment capabilities, and integrating intelligent management platforms that support seamless workload mobility across centralized and distributed computing environments.

IT & Telecommunications represents the largest end-user segment because cloud providers, network operators, and digital platform companies require continuous server expansion to support data-intensive services. This segment accounts for approximately 42% of enterprise server deployments, driven by AI applications, 5G infrastructure, and cloud service delivery. Healthcare is emerging as the fastest-growing end-user, with server deployments increasing by nearly 18% as hospitals adopt AI diagnostics, medical imaging platforms, and electronic health record modernization requiring secure high-performance computing infrastructure. BFSI continues investing in resilient server platforms to support digital banking, fraud analytics, and regulatory compliance, while Government agencies modernize digital public services through secure infrastructure upgrades. Manufacturing increasingly deploys industrial edge servers for smart factories and predictive maintenance, whereas Retail strengthens omnichannel operations using AI-driven inventory management and customer analytics. Vendors are tailoring industry-specific server solutions, expanding strategic partnerships, and delivering integrated infrastructure platforms that improve deployment flexibility while strengthening long-term customer relationships.

North America accounted for the largest market share at 39.2%in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a 5.8% CAGRbetween 2026 and 2033.

North America remains the leading Data Center Server Market due to its concentration of hyperscale cloud operators, AI infrastructure investments, and advanced semiconductor ecosystem. The region contributes approximately 39.2% of global demand, supported by extensive deployments across cloud computing, financial services, digital media, and enterprise AI. More than 60% of newly commissioned hyperscale facilities are designed to accommodate high-density server racks and GPU-enabled workloads. Continued investment in liquid-cooled infrastructure, automation platforms, and software-defined data centers strengthens operational efficiency. Strategic collaborations between cloud providers, server manufacturers, and semiconductor companies continue accelerating deployment speed while improving supply-chain resilience for next-generation computing environments.

United States Market Outlook: The United States remains the regional growth engine with over 5,400 operational data centers supporting AI, cloud computing, and enterprise digital transformation. The country's advanced semiconductor ecosystem, large-scale hyperscale campuses, and supportive manufacturing policies encourage continuous server deployment. Major cloud providers continue expanding AI infrastructure while domestic hardware manufacturing investments strengthen supply security. Integration of liquid cooling, GPU clusters, and intelligent infrastructure management further enhances deployment efficiency across commercial and government computing environments.

Europe maintains a strong position through enterprise modernization, sovereign cloud initiatives, and energy-efficient data center investments. The region accounts for approximately 24.1% of global server deployments, supported by strict sustainability standards and expanding digital infrastructure. More than 35% of newly developed facilities incorporate advanced cooling technologies and intelligent power optimization systems to improve operational efficiency. Investments in localized cloud infrastructure and secure enterprise computing continue strengthening deployment activity. Server vendors increasingly align product development with energy-performance standards while expanding partnerships with regional colocation providers and enterprise technology integrators.

Germany Market Outlook: Germany serves as Europe's most strategically important server market because of its industrial digitalization, manufacturing leadership, and enterprise cloud adoption. Large automotive, industrial automation, and engineering companies continue modernizing mission-critical computing infrastructure with AI-ready server platforms. Growing colocation investments and stricter energy-efficiency regulations encourage deployment of advanced cooling technologies and high-performance computing systems, reinforcing Germany's position as a key enterprise infrastructure hub.

Asia-Pacific is emerging as the fastest-expanding market, supported by rapid digital transformation, semiconductor manufacturing, and hyperscale cloud investments. The region represents nearly 28.5% of global demand while recording the strongest deployment momentum. More than 45% of new regional capacity additions are linked to AI computing, cloud expansion, and enterprise digitalization projects. Local manufacturing capabilities and government-backed technology initiatives improve server availability while strengthening regional supply chains. Equipment suppliers are expanding assembly operations, increasing localization strategies, and introducing AI-optimized server platforms tailored to rapidly growing enterprise workloads.

China Market Outlook: China remains the largest market within Asia-Pacific due to extensive cloud infrastructure, domestic server manufacturing, and national digital economy initiatives. Large internet platforms, telecommunications operators, and industrial enterprises continue deploying high-density computing infrastructure to support AI and intelligent manufacturing. Domestic hardware production capabilities, combined with increasing investment in advanced processors and cloud infrastructure, reinforce China's leadership in enterprise-scale server deployment and technology localization.

South America continues expanding its server infrastructure through cloud migration, financial sector modernization, and enterprise digital transformation. The region contributes approximately 4.6% of global deployments, with demand concentrated around major metropolitan data center clusters. Enterprise cloud adoption has increased by nearly 28%, encouraging investments in localized computing infrastructure and colocation capacity. Infrastructure limitations and power availability remain operational constraints, yet international cloud providers continue strengthening regional presence through new facilities and strategic partnerships. Vendors are introducing modular server platforms that simplify deployment while improving operational efficiency for expanding enterprise workloads.

Brazil Market Outlook: Brazil represents the region's largest server market due to its mature financial services sector, expanding cloud ecosystem, and rapidly growing enterprise digitalization initiatives. Major colocation operators continue investing in new facilities supporting banking, telecommunications, retail, and government applications. Increasing fiber connectivity and enterprise cloud migration are strengthening demand for scalable server infrastructure, while partnerships between global technology vendors and domestic service providers improve deployment capabilities across the country's primary digital corridors.

The Middle East & Africa market is strengthening through national digital transformation programs, hyperscale investments, and expanding enterprise cloud infrastructure. The region accounts for approximately 3.6% of global server demand while recording steady deployment growth across government, financial services, and telecommunications sectors. More than 30% of recently announced infrastructure projects incorporate AI-ready computing capabilities and advanced power management technologies. International cloud providers continue partnering with regional operators to expand localized data center capacity, while governments prioritize secure digital infrastructure to support economic diversification and public-sector modernization.

United Arab Emirates Market Outlook: The United Arab Emirates has established itself as the region's leading digital infrastructure hub through aggressive smart city initiatives, cloud investments, and advanced connectivity. Global hyperscale providers continue expanding local availability zones, while enterprise organizations accelerate migration toward AI-enabled computing environments. Strategic investments in modern data centers, renewable-powered facilities, and digital infrastructure create favorable conditions for high-performance server deployments supporting finance, government, healthcare, and emerging AI applications.

The competitive landscape is defined by global OEMs including Dell Technologies, Hewlett Packard Enterprise, Lenovo, Supermicro, and Cisco, competing against regional manufacturers such as Inspur and ODM suppliers serving hyperscale cloud providers. The top five vendors collectively control approximately 58% of the global market, intensifying competition across AI-optimized infrastructure. Competition centers on accelerated computing performance, deployment speed, energy efficiency, and supply-chain resilience rather than price alone. AI-enabled server configurations now command nearly 35% higher average selling prices, while liquid-cooled platforms improve rack efficiency by roughly 20%. Leading vendors are expanding manufacturing capacity, partnering with NVIDIA, AMD, and Intel, and vertically integrating software, networking, and lifecycle services. The market is shifting toward rack-scale AI systems, giving technology innovators an advantage over cost-focused manufacturers. High capital requirements, advanced semiconductor access, and enterprise qualification cycles remain significant entry barriers. Winning requires differentiated AI infrastructure, dependable component supply, rapid customization, and integrated enterprise support capabilities.

Hewlett Packard Enterprise (HPE)

Lenovo

Supermicro

Cisco Systems

Fujitsu

Inspur Electronic Information Industry Co., Ltd.

NEC Corporation

ASUS

GIGABYTE Technology

Intel Corporation

IBM Corporation

AI-native server architectures, GPU acceleration, liquid cooling, and software-defined infrastructure are redefining enterprise computing. More than 65% of newly deployed hyperscale servers are optimized for AI workloads, while direct liquid cooling improves thermal efficiency by approximately 25% compared with conventional air-cooled systems. Enterprises are increasingly integrating intelligent orchestration platforms that automate workload balancing, predictive maintenance, and infrastructure monitoring to improve operational consistency.

Modern rack-scale AI platforms outperform traditional CPU-only environments by nearly 40% for parallel computing applications while reducing processing time for large AI models. Composable infrastructure enables hardware resources to be dynamically allocated, increasing server utilization by approximately 20%. Cloud providers, hyperscale operators, and financial institutions gain the greatest competitive advantage because faster provisioning, higher density, and improved energy efficiency directly lower operational costs while accelerating digital service delivery.

Between 2026 and 2028, widespread adoption of rack-scale computing, CXL-enabled memory architectures, silicon photonics, and AI-driven infrastructure automation will reshape data center design. Server vendors are integrating hardware, networking, and lifecycle software into unified platforms to simplify deployment and strengthen customer retention. Organizations investing now in AI-ready, modular, and energy-efficient server technologies will achieve superior scalability, faster deployment cycles, improved infrastructure resilience, and stronger long-term competitive positioning as enterprise AI adoption continues accelerating.

August 2025 – NVIDIA announced RTX PRO Blackwell Server Edition GPUs for enterprise servers from Dell Technologies, HPE, Lenovo, Cisco, and Supermicro, accelerating AI and graphics workloads through standardized 2U platforms for broad enterprise deployment. Business impact: Faster enterprise AI adoption. Source: www.nvidianews.nvidia.com

September 2025 – Supermicro began volume shipments of NVIDIA Blackwell Ultra systems, introducing 10+ AI infrastructure SKUs with plug-and-play rack-scale deployment capabilities. Business impact: Reduced deployment timelines for hyperscale AI data centers through integrated, validated infrastructure.

May 2026 – Dell Technologies introduced its 18th-generation PowerEdge server portfolio alongside PowerStore Elite, delivering 50% more Intel CPU cores in selected storage platforms while strengthening AI-ready enterprise infrastructure. Business impact: Higher compute density and simplified modernization.

March 2026 – Supermicro unveiled one of the industry's first NVIDIA BlueField-4 STX storage servers supporting Context Memory architecture to accelerate AI inference performance. Business impact: Improved AI storage efficiency and strengthened leadership in next-generation AI infrastructure.

This report provides comprehensive analysis of the Data Center Server Market across Rack Servers, Blade Servers, Tower Servers, Micro Servers, and Others, covering deployments within Cloud Computing, Enterprise Data Centers, Colocation Data Centers, Edge Computing, and additional specialized applications. It evaluates demand across IT & Telecommunications, BFSI, Government, Healthcare, Manufacturing, Retail, and other end-user industries while examining adoption patterns, infrastructure modernization, AI integration, and deployment strategies across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa.

The report assesses competitive positioning of major technology providers, product innovation strategies, AI-ready server adoption, liquid cooling, software-defined infrastructure, and emerging rack-scale computing architectures. It incorporates operational benchmarks, enterprise deployment trends, regional investment activity, and evolving infrastructure priorities to support investment planning, expansion strategy, technology selection, supply-chain decisions, competitive benchmarking, and long-term business planning throughout the 2026–2033 assessment period.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 5,960.0 Million |

| Market Revenue (2033) | USD 8,119.1 Million |

| CAGR (2026–2033) | 3.94% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Dell Technologies; Hewlett Packard Enterprise (HPE); Lenovo; Supermicro; Cisco Systems; Fujitsu; Inspur Electronic Information Industry Co., Ltd.; NEC Corporation; ASUS; GIGABYTE Technology; Intel Corporation; IBM Corporation |

| Customization & Pricing | Available on Request (10% Customization Free) |