Reports

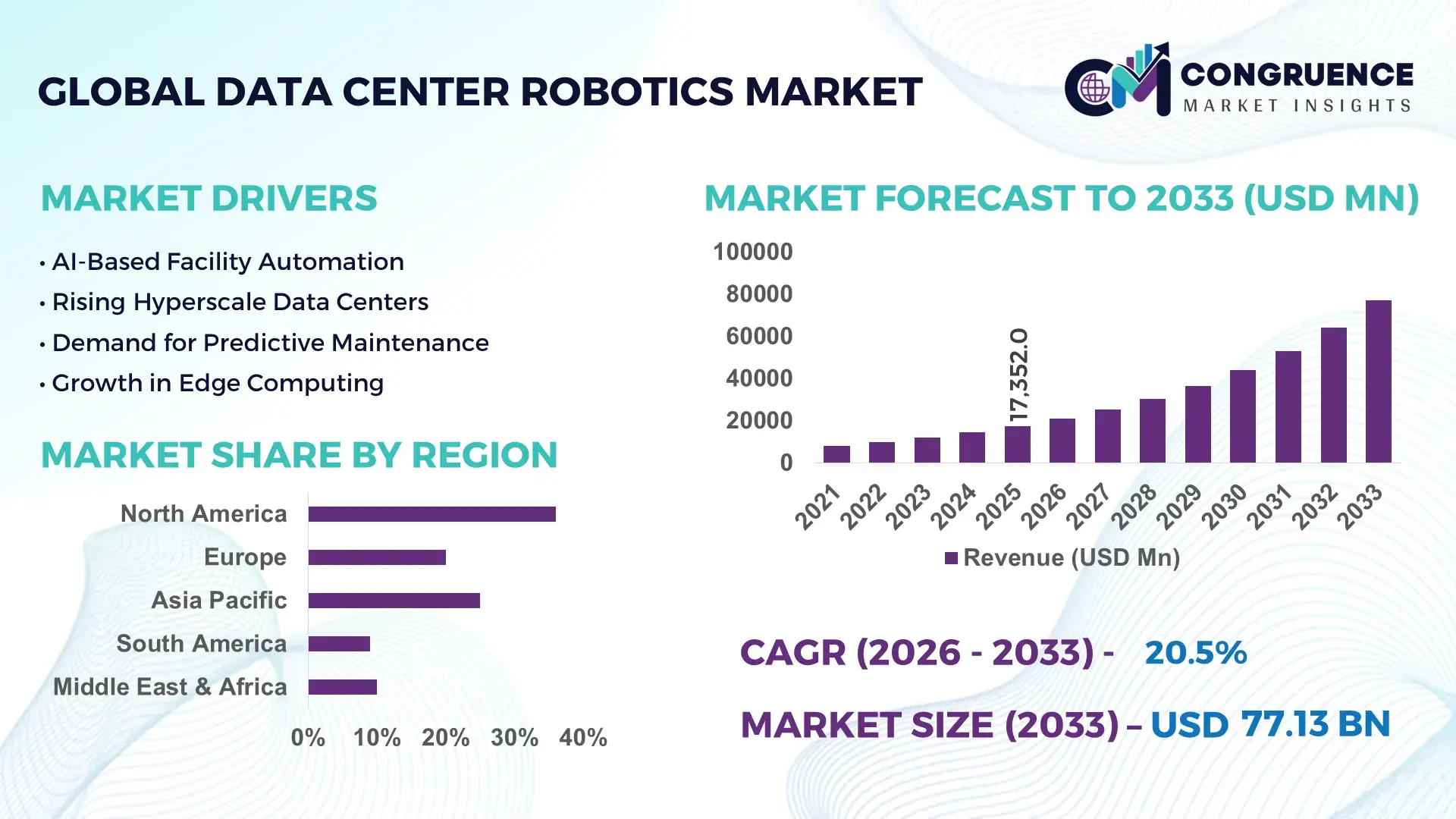

The Global Data Center Robotics Market was valued at USD 17352 Million in 2025 and is anticipated to reach a value of USD 77134.01 Million by 2033 expanding at a CAGR of 20.5% between 2026 and 2033.

Rapid expansion of hyperscale AI infrastructure, rising deployment of autonomous maintenance systems, and increasing operational pressure to reduce downtime are accelerating robotics integration across high-density data center facilities. Advanced robotic inspection and predictive monitoring systems are lowering maintenance response times by nearly 35% while reducing cooling-related energy consumption by approximately 18% in next-generation server environments. Between 2024 and 2026, semiconductor supply chain regionalization and stricter energy-efficiency mandates across North America and Europe accelerated investment in automated infrastructure management. Data center operators managing AI-intensive workloads above 40 MW capacity increasingly shifted toward robotics-enabled thermal diagnostics and autonomous cable management systems as labor shortages and rising uptime costs intensified. Compared with traditional facilities, robotics-enabled sites demonstrate nearly 1.5x higher operational continuity during peak compute demand cycles.

The United States dominates the global market with nearly 38% share in 2026, supported by hyperscale investments exceeding USD 85 billion across cloud computing, generative AI, financial services, and defense infrastructure. More than 42% of newly commissioned Tier IV facilities in the country now integrate robotic predictive maintenance platforms and AI-powered inspection systems. North American operators also report approximately 31% lower unscheduled maintenance interventions compared with conventional manual operations, outperforming European adoption rates due to faster AI infrastructure deployment and stronger automation spending. Large-scale cloud providers are prioritizing robotics integration to optimize power utilization effectiveness and improve infrastructure scalability under growing AI server density requirements.

The market is evolving from basic automation toward fully autonomous infrastructure operations, making robotics investment a strategic requirement for operators seeking scalable, energy-efficient, and resilient data center ecosystems.

Market Size & Growth: USD 17.3 billion in 2025 expanding toward USD 77.1 billion by 2033, driven by hyperscale AI deployment and autonomous infrastructure management adoption.

Top Growth Drivers: Predictive robotics reduce maintenance downtime by 31%, automated cooling systems lower energy usage by 18%, and labor optimization improves operational efficiency by 27%.

Short-Term Forecast: By 2028, autonomous robotic inspection systems are projected to decrease manual maintenance cycles by 40% across advanced Tier III and Tier IV facilities.

Emerging Technologies: AI vision robotics, digital twin-integrated automation, and autonomous mobile monitoring platforms are recording deployment growth above 34% annually.

Regional Leaders: North America exceeds USD 28 billion through hyperscale expansion, Asia-Pacific surpasses USD 21 billion with semiconductor-led growth, and Europe advances beyond USD 14 billion through energy-efficiency automation programs.

Consumer/End-User Trends: Nearly 46% of colocation and cloud operators prioritize robotics-enabled predictive infrastructure management for high-density AI workloads.

Pilot/Case Example: In 2025, a multi-site hyperscale robotics deployment reduced thermal incidents by 29% and improved infrastructure fault response speed by 41%.

Competitive Landscape: Leading vendors collectively control nearly 44% market share, with competition focused on AI-enabled autonomous maintenance and intelligent inspection robotics.

Regulatory & ESG Impact: Energy-efficiency regulations across Europe and North America are supporting robotics systems capable of lowering cooling-related carbon emissions by up to 22%.

Investment & Funding: Global investments exceeded USD 11 billion between 2024 and 2026 as cloud providers expanded automation partnerships amid semiconductor supply chain restructuring.

Innovation & Future Outlook: Autonomous server-handling robots, liquid-cooling compatible robotics, and edge-ready inspection drones are reshaping advanced smart data center operations.

Cloud service providers account for nearly 48% of total market demand, followed by colocation operators at 29% and enterprise facilities at 16%, highlighting strong robotics adoption across AI-driven computing infrastructure. Recent innovations focus on AI-powered thermal inspection robotics and digital twin synchronization systems capable of improving diagnostics accuracy by over 33%. North America maintains leadership in deployment capacity, while Asia-Pacific records the fastest infrastructure expansion due to semiconductor manufacturing growth and hyperscale construction activity. Rising regulatory pressure on energy optimization and ongoing global supply chain realignment are accelerating autonomous infrastructure investment, positioning robotics as a foundational technology for future-ready data center scalability and operational resilience.

Data center robotics is rapidly transforming from an operational enhancement tool into a core competitive infrastructure layer for hyperscale computing, AI cloud expansion, and autonomous facility management. Operators are accelerating robotics deployment to optimize uptime, reduce thermal failures, and manage rising server density linked to generative AI workloads. Between 2024 and 2026, stricter energy-efficiency regulations and semiconductor supply chain restructuring intensified investment in autonomous maintenance platforms capable of reducing manual intervention by nearly 40%. AI-powered robotics systems now outperform legacy maintenance models by improving infrastructure efficiency by 34% while reducing operating costs by approximately 22% compared to traditional human-dependent workflows.

North America leads in deployment volume due to hyperscale cloud expansion, while Asia-Pacific leads in robotics innovation adoption with nearly 37% faster integration of AI-enabled inspection systems across high-density facilities. Within the next two to three years, robotics-enabled predictive infrastructure management is projected to reduce unscheduled downtime incidents by over 30% and improve power utilization optimization by 18%. ESG alignment is also becoming a strategic advantage, as autonomous cooling and inspection robotics lower energy waste and support carbon-reduction compliance targets across advanced data center ecosystems.

In 2025, a robotics-integrated hyperscale facility deployment reduced thermal anomaly response times by 41% and improved maintenance efficiency by 28%, demonstrating measurable operational resilience under AI-driven compute pressure. Leading operators are shifting capital allocation toward autonomous infrastructure ecosystems, digital twin integration, and robotics-compatible liquid cooling environments to strengthen scalability and long-term operational continuity. Companies securing robotics-led infrastructure advantages today are positioning themselves to dominate future AI-ready data center networks through superior efficiency, resilience, and infrastructure intelligence.

Rising AI workloads and hyperscale expansion are forcing operators to deploy autonomous robotics for predictive maintenance, thermal inspection, and infrastructure monitoring. Average rack density increased by nearly 45% between 2024 and 2026, pushing facilities toward robotics systems that reduce manual intervention by approximately 30%. Semiconductor localization programs across North America and Asia accelerated new facility construction, increasing demand for automation-ready infrastructure. In response, cloud providers are expanding robotics partnerships and integrating AI-driven monitoring platforms that improve diagnostics accuracy by over 33%, strengthening operational efficiency and uptime performance.

High retrofitting costs and infrastructure compatibility issues remain major barriers to large-scale robotics adoption. Integrating robotics into legacy facilities increases modernization expenses by nearly 25%, while over 40% of mid-sized operators face deployment delays linked to outdated power and cooling systems. Semiconductor supply concentration is also constraining hardware availability during geopolitical trade disruptions. To reduce operational risk, companies are adopting modular robotics platforms, diversifying component sourcing, and securing long-term supplier agreements that improve deployment flexibility and reduce integration complexity by nearly 18%.

Edge infrastructure expansion and autonomous operations are creating strong long-term opportunities for robotics vendors. Edge facilities are expected to contribute nearly 32% of new robotics deployments by 2028 as enterprises prioritize low-latency AI processing environments. AI-enabled robotic systems are improving predictive fault detection accuracy by more than 35%, reducing emergency maintenance cycles and operational disruptions. Companies are accelerating investment in liquid-cooling compatible robotics, digital twin integration, and self-learning automation platforms to secure future competitive advantage across decentralized computing ecosystems.

Power limitations, cybersecurity exposure, and infrastructure synchronization issues are challenging long-term robotics scalability. High-density AI facilities increased electricity consumption intensity by nearly 38% between 2024 and 2026, creating grid pressure across major hyperscale markets. At the same time, interconnected robotics systems expanded cybersecurity risk exposure by approximately 27%, increasing operational vulnerability. Companies are responding through resilient power investments, AI-based security frameworks, and strategic automation partnerships to maintain operational continuity and infrastructure reliability across large-scale autonomous data center environments.

AI-guided inspection deployments increased by 36% across hyperscale facilities in 2025, reshaping infrastructure monitoring cycles. Operators are replacing manual inspection rounds with autonomous robotics capable of reducing fault-detection time by 31% and improving thermal diagnostics precision by 28%. Companies are integrating digital twin synchronization platforms to optimize predictive maintenance workflows while lowering unplanned intervention frequency during high-density AI server operations.

Automated cooling robotics reduced energy optimization response times by 24%, forcing operational restructuring across large-scale facilities. Rising electricity intensity and stricter energy-efficiency compliance requirements pushed operators toward robotics-enabled airflow balancing and liquid-cooling inspection systems. Facilities deploying autonomous cooling robotics lowered cooling-related power waste by nearly 18%, while major providers accelerated partnerships with thermal management technology firms to improve infrastructure efficiency.

Asia-Pacific robotics adoption expanded by 33% as regional supply chain shifts accelerated localized automation deployment. Semiconductor manufacturing growth and rapid hyperscale expansion increased demand for autonomous maintenance systems across Singapore, India, and Southeast Asia. Unlike North America, which leads in deployment volume, Asia-Pacific operators are prioritizing modular robotics platforms that reduce infrastructure integration complexity by approximately 20%, improving deployment speed across newly commissioned edge facilities.

Robotics-as-a-service adoption climbed by 27%, redefining procurement and infrastructure scaling models. Mid-sized operators increasingly shifted toward subscription-based robotics deployment to avoid high upfront modernization costs and shorten implementation timelines by nearly 22%. Vendors responded by restructuring commercial models around managed automation services, predictive analytics integration, and remote operational support, creating a non-obvious shift where recurring service capability is becoming as strategically important as robotics hardware performance.

The Data Center Robotics Market is segmented by type, application, and end-user, with demand increasingly concentrating around autonomous infrastructure optimization and AI-driven operational efficiency. Maintenance Robots and Facility Monitoring applications currently dominate deployment volumes due to their direct impact on uptime continuity and operational cost reduction. Cloud Providers and IT & Telecom operators collectively account for more than 55% of market demand as hyperscale AI infrastructure expansion accelerates robotics integration across high-density facilities. At the same time, demand is shifting toward predictive automation, cooling management, and modular robotics platforms capable of supporting decentralized edge infrastructure. Security-focused robotics and inspection systems are also gaining strategic relevance as cybersecurity and compliance pressures intensify. Companies are responding through targeted product specialization, AI-enabled automation upgrades, and robotics-compatible infrastructure expansion to capture long-term demand across performance-critical data center ecosystems.

Maintenance Robots currently dominate the market with nearly 34% share due to their strong integration advantage in predictive maintenance, thermal diagnostics, and uptime optimization across hyperscale facilities. Their ability to reduce manual intervention by approximately 30% while improving infrastructure response speed has positioned them as the preferred deployment category for large-scale operators. Inspection Robots represent the fastest-growing segment, expanding at nearly 29% deployment growth as AI-driven visual diagnostics and autonomous monitoring systems become critical for high-density server environments. Compared with Cleaning Robots, which remain concentrated in routine environmental management, Inspection Robots are increasingly prioritized for predictive analytics integration and digital twin synchronization capabilities. Security Robots and Cleaning Robots collectively account for nearly 38% of deployment activity, maintaining strategic relevance through autonomous surveillance, restricted-access monitoring, and contamination control in liquid-cooling environments. Companies are accelerating investment in AI-enabled robotics platforms, modular deployment architecture, and sensor-enhanced navigation systems to capture growing demand for intelligent automation. Market momentum is clearly shifting toward multifunctional robotics ecosystems capable of combining maintenance, diagnostics, and monitoring within a unified infrastructure management framework.

Facility Monitoring leads the market with nearly 32% share as operators prioritize continuous infrastructure visibility, thermal optimization, and real-time operational diagnostics across AI-intensive facilities. Usage concentration remains high because autonomous monitoring systems improve fault-detection speed by approximately 28% while supporting uninterrupted high-density computing operations. Cooling Management is emerging as the fastest-growing application segment with deployment expansion exceeding 30%, driven by rising power-density pressure and stricter energy-efficiency compliance requirements. Compared with Security Surveillance, which remains heavily focused on access control and perimeter automation, Cooling Management is gaining stronger investment momentum due to its direct impact on power utilization optimization and operating cost reduction. Equipment Inspection, Asset Maintenance, and Security Surveillance collectively contribute nearly 49% of total deployment activity, supported by growing demand for predictive analytics and autonomous operational management. Companies are scaling AI-driven robotics integration, expanding liquid-cooling compatible automation systems, and restructuring deployment strategies around real-time infrastructure optimization. Demand is clearly shifting toward applications capable of delivering measurable operational intelligence rather than isolated automation functionality.

Cloud Providers dominate the market with nearly 36% share due to their large-scale hyperscale infrastructure expansion, high automation dependency, and continuous AI workload growth. These operators prioritize robotics deployment to optimize uptime performance, reduce maintenance complexity, and manage increasingly dense server environments. Colocation Providers represent the fastest-growing end-user segment with adoption growth exceeding 28%, fueled by rising enterprise outsourcing demand and accelerated edge infrastructure deployment. Compared with BFSI organizations, which focus heavily on secure infrastructure monitoring and operational continuity, Cloud Providers invest more aggressively in fully autonomous infrastructure ecosystems and robotics-integrated predictive analytics platforms. IT & Telecom, Government, and BFSI sectors collectively account for nearly 47% of total market demand, supported by growing digital infrastructure modernization and cybersecurity compliance requirements. Companies are responding through customized robotics deployment models, subscription-based automation services, and strategic technology partnerships designed to improve scalability and operational flexibility. Future demand is increasingly shifting toward operators capable of integrating robotics into AI-driven infrastructure management and decentralized computing environments.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 23.1% between 2026 and 2033.

North America maintains demand concentration through hyperscale AI infrastructure deployment and advanced robotics integration across cloud and colocation facilities. Europe contributes nearly 24% share, driven by energy-efficiency mandates and robotics-enabled infrastructure optimization programs focused on reducing cooling-related power consumption. Asia-Pacific holds approximately 29% share and is accelerating rapidly due to semiconductor manufacturing expansion, localized automation deployment, and large-scale edge infrastructure construction across India, Singapore, and Southeast Asia. Meanwhile, Middle East investments in digital infrastructure modernization and South American colocation expansion are reshaping regional adoption patterns. Ongoing semiconductor supply chain diversification and AI infrastructure localization are forcing companies to prioritize automation-ready facility expansion, strategic robotics partnerships, and region-specific infrastructure optimization strategies globally.

North America holds nearly 38% of global market demand, supported by aggressive hyperscale expansion and high-density AI infrastructure deployment across the United States and Canada. Cloud providers and colocation operators are accelerating robotics adoption for predictive maintenance, thermal inspection, and autonomous infrastructure monitoring to improve uptime performance by approximately 31%. Rising power-density pressure and stricter operational efficiency targets are forcing facilities toward robotics-enabled cooling optimization and digital twin integration systems. More than 42% of newly commissioned Tier IV facilities now incorporate autonomous monitoring platforms and AI-guided maintenance robotics. Enterprises increasingly prioritize scalable automation ecosystems over labor-intensive operations to reduce downtime risk and improve operational continuity. Companies are expanding robotics-compatible infrastructure capacity and accelerating partnerships with AI automation vendors to secure long-term infrastructure resilience and competitive operational efficiency.

Europe accounts for nearly 24% of global market activity, with Germany, the Netherlands, and the Nordic region leading robotics deployment across energy-efficient hyperscale and colocation facilities. Regulatory pressure linked to carbon reduction and power utilization optimization is accelerating adoption of autonomous cooling inspection and predictive maintenance robotics capable of lowering cooling-related electricity waste by approximately 18%. More than 36% of advanced facilities are integrating robotics-enabled infrastructure monitoring to align with stricter sustainability compliance standards. Enterprises are prioritizing high-efficiency automation systems, liquid-cooling compatible robotics, and low-energy operational frameworks to strengthen long-term compliance positioning. Companies are restructuring deployment models around AI-driven energy optimization and expanding regional partnerships focused on sustainable infrastructure automation. Europe is forcing robotics providers to innovate around efficiency, interoperability, and ESG-focused operational intelligence.

Asia-Pacific represents nearly 29% of global market demand and remains the fastest-expanding regional ecosystem due to hyperscale infrastructure growth across China, India, Singapore, and Southeast Asia. Strong semiconductor manufacturing capacity and localized robotics production are improving deployment speed while reducing infrastructure integration costs by approximately 20%. Regional operators increased autonomous monitoring and inspection robotics deployment by over 33% between 2024 and 2026 as edge infrastructure expansion accelerated. Enterprises are prioritizing scalable, modular robotics platforms capable of supporting rapid facility commissioning and AI-intensive workloads. Large cloud operators are also expanding robotics-integrated facilities exceeding 40 MW capacity to strengthen operational scalability and infrastructure efficiency. Asia-Pacific has become strategically critical for companies targeting large-volume deployment, localized production efficiency, and accelerated infrastructure expansion opportunities.

South America contributes nearly 6% of global market activity, with Brazil and Chile emerging as the leading deployment hubs due to growing colocation demand and enterprise digital infrastructure modernization. Rising cloud adoption and increased financial sector digitization are accelerating demand for predictive maintenance and autonomous security robotics capable of improving operational response efficiency by approximately 22%. However, high infrastructure import dependency and elevated deployment costs continue constraining large-scale robotics integration across mid-sized facilities. Enterprises are increasingly adopting modular automation systems and phased deployment models to balance operational modernization with capital efficiency. Regional colocation providers expanded robotics-enabled monitoring deployments by nearly 19% between 2024 and 2026 to improve uptime performance and reduce labor-intensive maintenance cycles. The region presents strong expansion potential but requires cost-optimized deployment strategies and localized infrastructure adaptation.

Middle East & Africa account for approximately 3% of global market demand, with the United Arab Emirates and Saudi Arabia leading regional deployment through aggressive smart infrastructure and hyperscale digital transformation initiatives. Oil & gas digitization, government-backed AI infrastructure programs, and large-scale smart city investments are accelerating demand for autonomous facility monitoring and predictive maintenance robotics. Robotics-enabled infrastructure deployments improved operational monitoring efficiency by nearly 24% across newly commissioned high-density facilities. Enterprises are prioritizing automation systems capable of optimizing cooling performance and reducing operational dependency in extreme environmental conditions. Regional operators also increased strategic partnerships with global automation providers to strengthen infrastructure scalability and AI readiness. The region is emerging as a strategically important market for companies targeting infrastructure modernization, government-backed digital expansion, and long-term automation deployment opportunities.

United States – 38% market share: The U.S. Data Center Robotics Market dominates through hyperscale AI infrastructure expansion, advanced automation deployment, and strong cloud computing demand concentration.

China – 21% market share: China maintains strong Data Center Robotics Market leadership through large-scale digital infrastructure construction, semiconductor manufacturing strength, and rapid autonomous facility deployment.

The Data Center Robotics Market is characterized by intense competition between global automation leaders, AI-driven robotics innovators, infrastructure technology providers, and specialized autonomous maintenance vendors. Major players including ABB, Siemens, Schneider Electric, Fanuc, and Boston Dynamics compete aggressively with infrastructure-focused robotics developers on automation intelligence, deployment scalability, and predictive maintenance capability. The top five companies collectively control nearly 47% of market influence, with competition increasingly shifting from hardware performance toward AI-enabled operational optimization and infrastructure integration speed. Advanced robotics platforms capable of reducing maintenance intervention time by over 30% and improving thermal diagnostics accuracy by approximately 28% are gaining stronger enterprise preference. Companies are accelerating partnerships with hyperscale cloud operators, expanding robotics-compatible infrastructure ecosystems, and integrating digital twin synchronization technologies to strengthen operational differentiation. The market is also witnessing growing pressure from modular robotics providers offering deployment flexibility and lower infrastructure integration costs. High infrastructure compatibility requirements, semiconductor dependency, and AI software integration complexity remain major entry barriers. Winning in this market increasingly depends on autonomous operational intelligence, infrastructure interoperability, and long-term hyperscale deployment capability.

ABB Ltd.

Siemens AG

Schneider Electric SE

Fanuc Corporation

Boston Dynamics

KUKA AG

Yaskawa Electric Corporation

SoftBank Robotics

Omron Corporation

Zebra Technologies Corporation

Nvidia Corporation

Rockwell Automation Inc.

Huawei Technologies Co., Ltd.

Mitsubishi Electric Corporation

AI-enabled predictive maintenance robotics and autonomous inspection platforms are currently transforming data center operations through real-time diagnostics, thermal imaging, and digital twin integration. Nearly 46% of hyperscale facilities now deploy AI-guided monitoring robotics to reduce infrastructure fault response times by approximately 31% and improve maintenance efficiency by 28%. Compared with legacy manual inspection systems, autonomous robotics platforms improve diagnostics accuracy by over 34% while lowering operational intervention costs by nearly 22%. Operators are increasingly integrating robotics with digital infrastructure management software to optimize uptime continuity and support high-density AI computing environments.

Emerging technologies are centered on liquid-cooling compatible robotics, edge-enabled autonomous monitoring systems, and AI-powered infrastructure orchestration platforms. Robotics-integrated cooling management systems are reducing cooling-related power waste by nearly 18%, while modular robotics deployment architectures lower infrastructure integration complexity by approximately 20%. More than 38% of newly commissioned Tier IV facilities now incorporate AI-driven thermal robotics and automated environmental monitoring systems. Companies focusing on robotics-compatible liquid cooling and predictive analytics platforms are gaining stronger competitive positioning among hyperscale cloud and colocation operators prioritizing operational scalability and energy optimization.

Disruptive innovation between 2026 and 2028 will increasingly focus on physical AI, self-learning robotics ecosystems, and autonomous infrastructure coordination platforms capable of managing multi-site operations with minimal human intervention. Advanced robotics orchestration systems are projected to improve infrastructure utilization efficiency by over 30% while accelerating maintenance cycle automation across decentralized edge environments. Companies investing early in AI-native robotics infrastructure, digital twin synchronization, and modular autonomous operations are positioning themselves to secure long-term operational efficiency advantages as AI-driven compute density continues reshaping global data center infrastructure requirements.

November 2025 Schneider Electric expanded its partnership with Switch through a $1.9 billion infrastructure supply agreement supporting AI-ready data center automation and robotics-compatible cooling systems. The deployment introduced advanced Uniflair cooling platforms capable of improving thermal efficiency by nearly 20% across high-density AI facilities, strengthening hyperscale operational scalability. [AI Cooling Scale-Up]

January 2026 Siemens and NVIDIA expanded their industrial AI partnership to accelerate autonomous infrastructure management and digital twin integration for advanced data center environments. Siemens reported more than 33% growth in AI-related infrastructure demand as operators increased deployment of AI-native operational automation systems. [Industrial AI Integration]

June 2025 Schneider Electric and NVIDIA launched next-generation AI-factory infrastructure architectures integrating robotics-enabled cooling, power optimization, and autonomous monitoring systems. The deployment framework reduced infrastructure development timelines by approximately 30% while supporting server rack environments operating above 130 kilowatts capacity. [High-Density Infrastructure Push]

April 2026 Siemens introduced its AI-ready Industrial Automation DataCenter platform integrating NVIDIA accelerated computing and AI-driven cybersecurity infrastructure for autonomous operations. The pre-configured architecture reduced infrastructure integration complexity while improving real-time automation scalability across advanced industrial and hyperscale digital environments. [AI-Ready Automation Stack]

The report provides comprehensive analysis of the Data Center Robotics Market across core technology segments, operational applications, end-user industries, and regional deployment ecosystems. Coverage includes key robot types such as Inspection Robots, Cleaning Robots, Security Robots, and Maintenance Robots, alongside critical applications including Facility Monitoring, Equipment Inspection, Cooling Management, Security Surveillance, and Asset Maintenance. The study evaluates demand trends across Cloud Providers, IT and Telecom operators, BFSI institutions, Government facilities, and Colocation Providers. Geographic assessment spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, capturing region-specific infrastructure shifts, automation deployment patterns, and AI-driven operational transformation trends.

The report delivers detailed strategic analysis across more than 15 market-level indicators including deployment concentration, adoption intensity, operational efficiency impact, and infrastructure modernization patterns. Maintenance robotics currently account for nearly 34% of deployment concentration, while autonomous cooling management systems are expanding adoption above 30% due to rising power-density pressures. The study also evaluates emerging technologies including digital twin synchronization, liquid-cooling compatible robotics, AI-native infrastructure automation, and robotics-as-a-service deployment models shaping operational strategies between 2026 and 2033.

The report supports investment planning, regional expansion decisions, competitive benchmarking, and infrastructure automation strategy development by identifying where deployment demand is accelerating, which technologies are reshaping operational efficiency, and how leading companies are positioning for long-term AI infrastructure scalability.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 17352 Million |

|

Market Revenue in 2033 |

USD 77134.01 Million |

|

CAGR (2026 - 2033) |

20.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

ABB Ltd., Siemens AG, Schneider Electric SE, Fanuc Corporation, Boston Dynamics, KUKA AG, Yaskawa Electric Corporation, SoftBank Robotics, Omron Corporation, Zebra Technologies Corporation, Nvidia Corporation, Rockwell Automation Inc., Huawei Technologies Co., Ltd., Mitsubishi Electric Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |