Reports

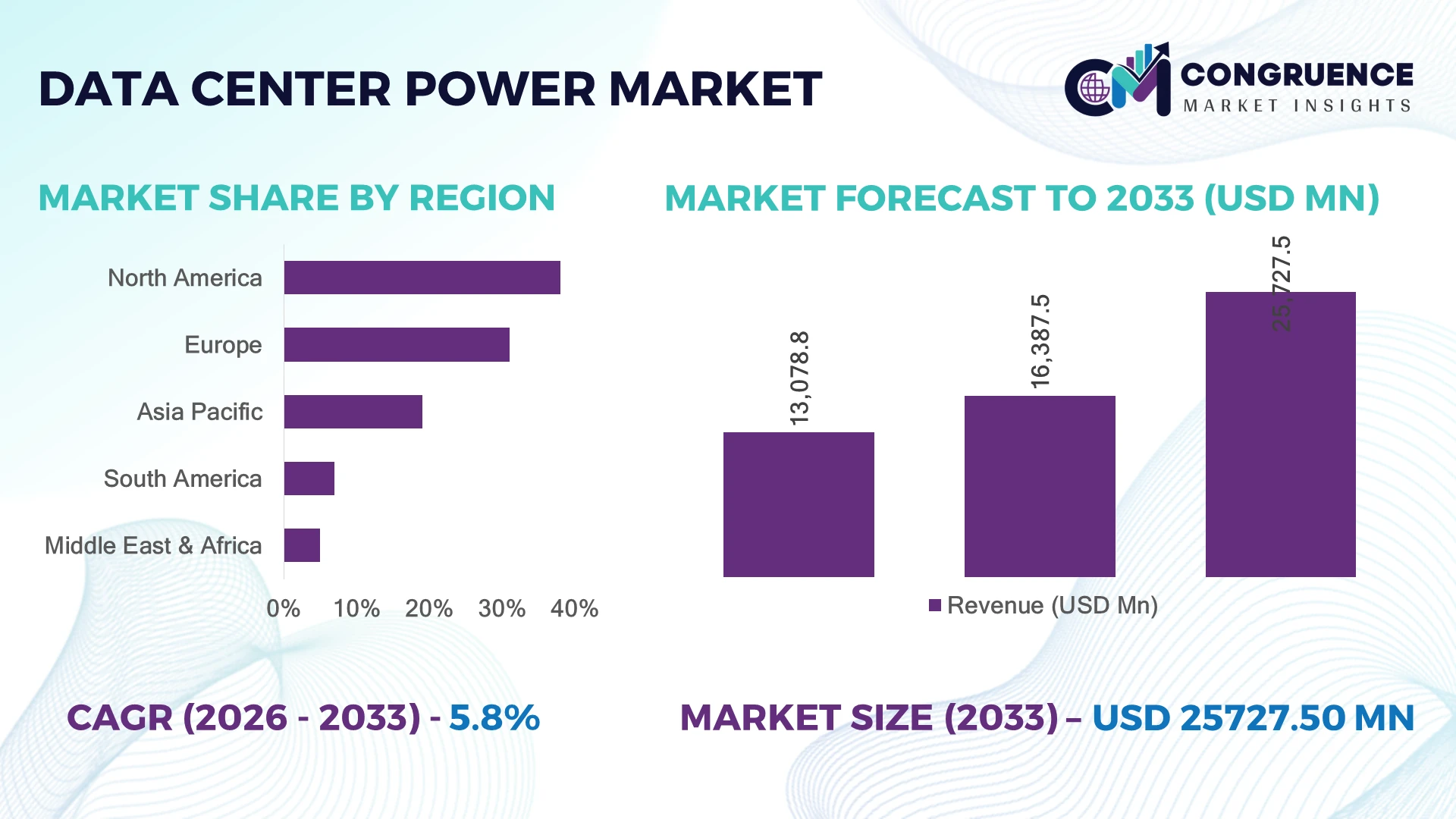

The Global Data Center Power Market was valued at USD 16387.48 Million in 2025 and is anticipated to reach a value of USD 25727.5 Million by 2033 expanding at a CAGR of 5.8% between 2026 and 2033. Rising hyperscale AI deployments, liquid-cooled server clusters, and grid modernization programs are accelerating procurement of advanced UPS systems, intelligent PDUs, lithium-ion backup solutions, and modular power infrastructure across high-density global data center environments.

The United States dominates the global data center power market with nearly 38% of installed hyperscale capacity, supported by over 5 GW of active data center construction and aggressive AI infrastructure investment from cloud and semiconductor firms in 2026. China follows with approximately 22% market share, driven by western-region energy optimization mandates and renewable-powered facilities. India recorded over 28% annual growth in colocation capacity additions, supported by digital banking, telecom expansion, and favorable state-level infrastructure incentives despite ongoing semiconductor supply chain realignments linked to US-China technology restrictions.

Strategic investments in resilient, energy-efficient power architectures are becoming essential for operators seeking lower downtime risk, faster scalability, and compliance with tightening global energy efficiency standards.

Market Size & Growth: USD 16387.48 Million in 2025 reaching USD 25727.5 Million by 2033, driven by AI server density growth exceeding 35% across hyperscale facilities.

Top Growth Drivers: AI workload expansion (+41%), modular data center adoption (+29%), and renewable-backed power integration (+33%) accelerate infrastructure upgrades.

Short-Term Forecast: By 2028, advanced power management systems improve facility energy efficiency by 18% while reducing unplanned downtime by 22%.

Emerging Technologies: Lithium-ion UPS, AI-based energy orchestration, and liquid-cooling compatible power systems increase operational efficiency by over 25%.

Regional Leaders: North America exceeds USD 9.4 Billion through hyperscale expansion, Asia-Pacific crosses USD 7 Billion via colocation growth, while Europe surpasses USD 5.1 Billion through green data center adoption.

Consumer/End-User Trends: Over 62% of enterprise operators prioritize high-density rack power systems supporting AI and accelerated computing environments.

Pilot/Case Example: In 2026, a Nordic modular data center deployment reduced cooling-related power losses by 31% using integrated smart-grid optimization.

Competitive Landscape: Top providers control nearly 48% market share, led by Schneider Electric, Eaton, Vertiv, ABB, and Siemens.

Regulatory & ESG Impact: Carbon-neutral infrastructure policies lowered diesel backup dependence by 19% across advanced European facilities.

Investment & Funding: Global investments exceeded USD 24 Billion in advanced data center energy infrastructure, supported by utility partnerships and regional expansion programs.

Innovation & Future Outlook: Next-generation DC power architectures and hydrogen-ready backup systems are reshaping high-growth hyperscale deployment strategies worldwide.

The Data Center Power Market is expanding rapidly across hyperscale cloud campuses, AI training facilities, edge computing hubs, and colocation environments requiring high-efficiency electrical infrastructure. Intelligent battery management systems and lithium-ion UPS deployments improved backup reliability by 27% in 2026, while modular power skids shortened deployment timelines. Increasing pressure on grid stability and energy compliance standards is accelerating investment in resilient, software-defined power ecosystems, setting the foundation for broader strategic transformation.

The Data Center Power Market is becoming strategically critical as hyperscale cloud operators, AI infrastructure providers, and colocation firms compete to secure resilient high-density power capacity amid accelerating digital infrastructure expansion. Grid modernization programs, semiconductor manufacturing incentives, and stricter energy-efficiency regulations are reshaping procurement priorities across the United States, Germany, India, and the Gulf region. In 2026, over 46% of newly commissioned hyperscale facilities integrated intelligent power orchestration platforms to manage rising rack densities exceeding 80 kW per rack in AI-focused deployments.

Advanced lithium-ion UPS systems now deliver nearly 35% lower maintenance requirements and 28% smaller footprint utilization compared to legacy VRLA battery architectures, improving operational continuity in space-constrained facilities. The United States continues leading hyperscale deployments with multi-gigawatt campuses, while Singapore and Japan prioritize compact, energy-efficient modular systems due to land and grid limitations. A leading Nordic colocation operator recently deployed AI-enabled energy balancing software, reducing peak power losses by 18% while improving server uptime consistency.

Over the next three years, operators are expected to accelerate partnerships with utility providers, battery manufacturers, and cooling technology firms to stabilize long-term power availability. Companies securing scalable, low-loss power ecosystems will strengthen competitive positioning, reduce operational exposure, and improve deployment flexibility across next-generation digital infrastructure networks.

Rising AI infrastructure deployment is intensifying demand for advanced data center power systems capable of supporting ultra-high-density computing loads. In 2026, AI-oriented server clusters increased average rack power consumption by 32%, while hyperscale operators expanded liquid-cooled environments by nearly 40% to maintain thermal efficiency. The United States and Saudi Arabia accelerated grid-connected hyperscale projects through power infrastructure modernization and fast-track industrial approvals. This shift is forcing operators to replace legacy UPS and switchgear systems with intelligent, modular architectures supporting predictive energy management. Major providers are expanding battery storage partnerships and investing in prefabricated power modules to shorten deployment timelines by nearly 25%. Companies integrating software-defined power management with renewable energy balancing are gaining operational resilience and lower downtime exposure in increasingly power-constrained digital infrastructure markets.

Transformer shortages, battery raw material volatility, and grid interconnection delays are constraining large-scale data center power deployments across major industrial hubs. In 2026, lead times for high-capacity transformers extended beyond 50 weeks in the United States, while lithium-ion battery pricing volatility remained above 18% due to mineral supply concentration and logistics disruptions. Germany and the United Kingdom faced power availability restrictions in key colocation clusters, limiting rapid hyperscale expansion. These constraints are increasing capital intensity and delaying commissioning schedules for advanced facilities. Operators are responding through localized supplier agreements, dual-sourcing strategies, and long-term procurement contracts for electrical infrastructure components. Several companies are also deploying hybrid backup architectures combining fuel cells and battery systems to reduce dependency on constrained diesel and battery supply chains while improving deployment continuity.

The expansion of edge computing, industrial AI workloads, and autonomous digital systems is creating new opportunities for distributed data center power architectures. In 2026, intelligent energy management platforms improved power utilization efficiency by nearly 21%, while modular edge deployments grew by over 30% across India, South Korea, and the United Arab Emirates. Operators are increasingly investing in direct-current distribution systems and AI-based load forecasting tools to optimize energy balancing in compact facilities. Government-backed renewable integration policies are also accelerating adoption of microgrid-compatible backup systems and advanced battery storage platforms. Companies are strengthening partnerships with utility firms and semiconductor manufacturers to secure long-term energy reliability for edge clusters. A growing strategic advantage is emerging for providers capable of integrating real-time analytics with low-latency power infrastructure across decentralized digital ecosystems.

Sustaining reliable power delivery for next-generation AI facilities is becoming increasingly complex as rack densities and cooling requirements rise sharply. In 2026, nearly 44% of hyperscale operators reported integration challenges between advanced cooling systems and legacy electrical infrastructure, while grid congestion risks increased in major hubs including Northern Virginia and Dublin. Workforce shortages in high-voltage engineering and energy optimization disciplines are also slowing deployment consistency for large campuses. These pressures are increasing operational risk, particularly in facilities requiring uninterrupted power availability above 99.99%. Companies must invest heavily in intelligent monitoring systems, digital twins, and adaptive power routing technologies to maintain scalability without compromising resilience. Strategic collaboration between utilities, infrastructure developers, and technology providers is becoming essential to support long-term high-density computing expansion while maintaining energy stability and sustainability targets.

AI Rack Density Escalation AI-focused hyperscale facilities increased average rack density by 34% in 2026, pushing operators toward high-capacity busway systems and liquid-cooling-compatible power architectures. Facilities in the United States and South Korea are replacing legacy floor-based distribution with overhead intelligent busways, reducing deployment time by nearly 22%. Companies are restructuring procurement contracts around modular electrical assemblies to accelerate AI cluster commissioning and reduce integration bottlenecks caused by transformer shortages.

Battery Storage Transition Accelerates Lithium-ion battery adoption in advanced data center environments exceeded 58% of new UPS-linked deployments during 2026 due to lower maintenance requirements and improved energy density. Germany and Singapore introduced stricter backup efficiency standards, accelerating replacement of VRLA systems across colocation facilities. Operators are forming long-term partnerships with battery manufacturers and deploying predictive battery analytics platforms that reduced backup-related downtime incidents by approximately 19%.

Software-Defined Power Expansion Intelligent energy orchestration platforms gained rapid adoption as operators targeted lower operational losses and dynamic load balancing. Nearly 47% of hyperscale operators integrated AI-driven power monitoring tools in 2026, improving power usage optimization by 16%. A notable operational shift involves integrating electrical infrastructure data directly into digital twin environments, enabling predictive maintenance scheduling and reducing emergency servicing cycles across large campuses.

Localized Modular Deployment Growth Prefabricated modular power infrastructure deployments expanded by 31% as colocation and edge operators sought faster commissioning and reduced labor dependency. India and the United Arab Emirates accelerated deployment of factory-integrated power skids to support banking, telecom, and smart-city expansion programs. Companies are prioritizing localized assembly partnerships and standardized modular designs, shortening deployment timelines by nearly 27% while improving scalability across distributed digital infrastructure networks.

UPS Systems remain the dominant segment within the Data Center Power Market due to their central role in maintaining uninterrupted operations across hyperscale, cloud, and enterprise facilities. In 2026, UPS deployments accounted for nearly 36% of total power infrastructure installations, driven by increased dependence on AI-driven computing clusters and high-density server environments. Lithium-ion integrated UPS solutions reduced maintenance cycles by approximately 30% compared to conventional VRLA configurations, strengthening adoption across North American and Japanese colocation hubs. Companies are prioritizing scalable modular UPS architectures and intelligent battery management integration to improve uptime reliability and operational flexibility.

Battery Systems are emerging as the fastest-growing segment as operators increasingly invest in advanced energy storage for backup optimization and renewable integration. Adoption of intelligent battery analytics platforms increased by over 24% during 2026, particularly across Germany and Singapore where energy efficiency regulations intensified. Power Distribution Units and Busway Systems continue gaining traction through high-density rack deployments, while Generators remain strategically important for long-duration resilience in grid-constrained industrial clusters. Vendors are expanding partnerships with utility providers and cooling technology firms to deliver integrated high-efficiency power ecosystems supporting next-generation AI workloads.

Hyperscale Data Centers represent the leading application segment due to large-scale AI processing, cloud expansion, and accelerated deployment of ultra-high-density compute infrastructure. In 2026, hyperscale environments accounted for approximately 42% of advanced power system demand, with average facility power loads increasing by nearly 28% following AI server expansion. Operators in the United States and Saudi Arabia are deploying integrated power orchestration systems and high-capacity busway networks to support rapidly scaling compute clusters. Companies are also increasing investments in liquid-cooling-compatible electrical infrastructure to improve operational continuity and energy balancing efficiency.

Edge Data Centers are emerging as the fastest-growing application segment, supported by industrial automation, telecom modernization, and low-latency computing requirements. Edge deployments expanded by over 33% in India and South Korea during 2026 as enterprises prioritized decentralized digital infrastructure. Colocation Data Centers continue strengthening through flexible leasing models and energy-efficient retrofits, while Enterprise Data Centers increasingly focus on hybrid modernization strategies. Cloud Data Centers remain operationally critical for large-scale digital workloads, prompting vendors to expand modular power deployment capabilities and automation partnerships across distributed infrastructure environments.

Cloud Service Providers remain the dominant end-user segment due to continuous hyperscale expansion, AI training workloads, and growing multi-tenant digital infrastructure requirements. In 2026, cloud operators represented nearly 39% of high-density power infrastructure procurement, with average facility energy demand increasing by approximately 26% across AI-integrated campuses. Major providers are deploying software-defined energy orchestration platforms and scalable battery-backed UPS systems to improve uptime and operational efficiency. IT and Telecom companies continue expanding edge-ready infrastructure to support 5G traffic growth and distributed application processing environments.

Healthcare is emerging as the fastest-growing end-user segment as digital diagnostics, medical imaging workloads, and connected health systems intensify infrastructure requirements. Healthcare-focused data center deployments increased by nearly 23% in 2026, particularly across the United States and India where hospitals accelerated digital record modernization. BFSI institutions continue investing in resilient backup systems to support real-time transaction processing, while Government Sector deployments prioritize sovereign infrastructure resilience. Manufacturing Industry adoption is also strengthening through industrial IoT and smart factory integration, prompting vendors to develop customized high-efficiency power solutions and long-term infrastructure service partnerships.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.1% between 2026 and 2033.

Hyperscale Expansion Reshaping Power Infrastructure Priorities

North America maintains leadership in the Data Center Power Market through concentrated hyperscale deployments, advanced grid connectivity, and large-scale AI infrastructure expansion. The region represented nearly 38% of global high-density data center power deployments in 2025, driven primarily by the United States and Canada. Northern Virginia, Texas, and Arizona continue attracting large multi-gigawatt projects requiring modular UPS systems, intelligent busway architectures, and grid-integrated backup infrastructure. In 2026, operators accelerated adoption of liquid-cooling-compatible power systems, increasing high-density rack deployment efficiency by approximately 24%. Utility partnerships and long-term transformer procurement agreements are becoming critical as operators address grid congestion and rising AI power loads. Companies are prioritizing vertically integrated energy strategies and prefabricated power module deployment to reduce commissioning timelines and improve operational resilience.

United States Market Outlook: The United States remains the region’s strategic center for hyperscale and AI-focused infrastructure deployment, supported by strong cloud computing demand, semiconductor investment expansion, and advanced utility integration capabilities. More than 5 GW of active data center capacity construction continued across major industrial hubs during 2026. Operators are investing heavily in software-defined energy management and battery-backed modular power systems to support rack densities exceeding 80 kW in AI clusters while reducing operational downtime exposure.

Sustainability Regulations Accelerate Infrastructure Modernization

Europe is strengthening its position through energy-efficient infrastructure modernization, sustainability mandates, and advanced colocation expansion across Germany, the United Kingdom, and the Nordic countries. The region accounted for nearly 24% of advanced data center power deployments in 2025, with operators increasingly prioritizing renewable-backed electrical systems and intelligent power balancing technologies. In 2026, over 52% of newly commissioned facilities integrated lithium-ion UPS platforms to align with stricter carbon reduction targets and lower maintenance requirements. Land constraints and power availability challenges in Dublin and Frankfurt are driving demand for compact modular architectures and AI-driven energy optimization tools. Companies are restructuring procurement around high-efficiency power ecosystems and localized energy partnerships to improve operational continuity under tightening grid regulations.

Germany Market Outlook: Germany remains a critical enterprise and colocation infrastructure hub due to its industrial digitalization strategy, strong manufacturing base, and advanced sustainability standards. Frankfurt continues leading interconnection and colocation density across continental Europe, with operators deploying intelligent load-balancing systems that improved facility energy utilization by nearly 18% in 2026. Enterprises are also accelerating investment in renewable-integrated backup infrastructure and modular switchgear modernization to comply with evolving energy efficiency regulations.

Massive Digital Infrastructure Scaling Drives Deployment Momentum

Asia-Pacific is emerging as the fastest-scaling regional market due to rapid cloud adoption, telecom modernization, semiconductor expansion, and aggressive hyperscale investment activity. The region contributed approximately 31% of global data center power deployments in 2025, supported by large-scale infrastructure expansion across China, India, Japan, Singapore, and South Korea. In 2026, modular edge and hyperscale facility deployments increased by over 33%, intensifying demand for intelligent UPS systems, compact busway architectures, and battery-backed backup platforms. Operators are increasingly adopting prefabricated power infrastructure to reduce labor dependency and accelerate commissioning timelines. Supply-chain localization initiatives and industrial policy incentives are also strengthening regional manufacturing capabilities for electrical infrastructure components and energy storage systems.

China Market Outlook: China continues dominating large-scale infrastructure deployment through aggressive cloud expansion, AI industrialization, and state-backed digital infrastructure modernization programs. Western-region renewable-powered data center projects gained substantial traction in 2026 as operators prioritized energy balancing and grid efficiency optimization. High-density computing deployments increased significantly across Beijing, Shanghai, and Inner Mongolia, prompting accelerated investment in advanced cooling-compatible power architectures and intelligent energy orchestration systems capable of supporting ultra-large compute environments.

Cloud Localization Expands Regional Infrastructure Demand

South America is experiencing steady market expansion through rising cloud localization requirements, digital banking growth, and increasing enterprise modernization initiatives. Brazil, Chile, and Colombia are driving most regional deployment activity as telecom providers and colocation operators expand distributed infrastructure capacity. The region represented nearly 5% of global data center power installations in 2025, with demand concentrated around modular backup systems and intelligent power distribution platforms. In 2026, colocation-driven deployments increased by approximately 21% as enterprises prioritized lower-latency digital services and regional data compliance requirements. However, grid instability and transformer import dependency continue affecting deployment consistency and infrastructure scalability. Companies are responding through localized partnerships, renewable integration projects, and phased infrastructure expansion strategies to improve resilience and reduce operational disruption.

Brazil Market Outlook: Brazil remains the region’s largest operational hub due to strong financial services digitization, expanding telecom infrastructure, and growing hyperscale investment activity around São Paulo. Operators increased deployment of intelligent UPS and battery-backed backup systems by nearly 19% during 2026 to stabilize operations amid periodic grid reliability challenges. Government-backed connectivity expansion programs and enterprise cloud migration initiatives are also supporting stronger long-term demand for resilient data center power ecosystems.

Sovereign Infrastructure Investment Accelerates Market Transformation

The Middle East & Africa market is advancing through sovereign cloud initiatives, smart-city investments, and rapid hyperscale infrastructure development across the Gulf states and South Africa. The region accounted for approximately 7% of global data center power deployments in 2025, supported by growing demand for resilient digital infrastructure and localized data processing capabilities. In 2026, hyperscale and colocation projects across the United Arab Emirates and Saudi Arabia accelerated deployment of modular power skids and intelligent battery-backed systems to support AI-enabled computing facilities. Governments are prioritizing grid modernization and renewable integration to strengthen long-term digital infrastructure resilience. Companies are expanding regional partnerships with utility providers and industrial developers to improve deployment scalability and energy efficiency under harsh climate operating conditions.

Saudi Arabia Market Outlook: Saudi Arabia is rapidly strengthening its position through large-scale smart infrastructure programs, sovereign cloud expansion, and industrial digitalization initiatives linked to long-term economic diversification plans. Data center operators accelerated deployment of renewable-integrated power architectures and modular backup systems across Riyadh and NEOM-linked projects during 2026. AI-focused infrastructure development and utility modernization programs are increasing demand for scalable high-density power systems capable of supporting advanced compute workloads under extreme environmental conditions.

Global leaders including Schneider Electric, Vertiv, Eaton, ABB, Siemens, and Legrand compete aggressively against regional power infrastructure specialists and low-cost Asian manufacturers across hyperscale, colocation, and enterprise deployments. The top five players collectively control nearly 48% of the Data Center Power Market, competing primarily through energy efficiency, deployment speed, intelligent monitoring capability, and integrated infrastructure delivery. Vertically integrated suppliers reduced deployment lead times by approximately 20%, while AI-enabled power optimization platforms improved operational efficiency by nearly 18% in large-scale facilities. Competition increasingly centers on modular UPS systems, lithium-ion battery integration, and software-defined energy orchestration rather than conventional electrical hardware pricing alone. Companies are expanding manufacturing localization, securing transformer supply agreements, and forming utility partnerships to strengthen long-term infrastructure availability. Market consolidation is accelerating as hyperscale operators prioritize end-to-end deployment capability. Winning requires scalable engineering expertise, resilient supply-chain control, rapid customization, and advanced energy optimization aligned with high-density AI infrastructure demands.

Schneider Electric

Vertiv

Eaton

ABB

Siemens

Legrand

Delta Electronics

Huawei Digital Power

Mitsubishi Electric

Cummins

Rittal

Cyber Power Systems

Toshiba Energy Systems

Fuji Electric

AI-driven power orchestration, modular UPS architectures, and lithium-ion battery systems are reshaping modern data center power infrastructure. In 2026, nearly 58% of newly deployed hyperscale facilities integrated intelligent energy management platforms capable of reducing power losses by approximately 16%. Lithium-ion UPS systems improved footprint efficiency by nearly 28% compared to legacy VRLA configurations while lowering maintenance cycles across high-density environments. Operators in the United States and Japan are increasingly deploying software-defined power monitoring to stabilize AI rack densities exceeding 80 kW and improve uptime consistency under fluctuating grid conditions.

Emerging technologies including liquid-cooling-compatible busway systems, direct-current distribution architectures, and digital twin-based power simulation platforms are accelerating infrastructure optimization. Advanced 800VDC systems reduced resistive transmission losses by nearly 20% compared to conventional AC-based distribution in pilot AI facilities during 2026. More than 42% of hyperscale operators are integrating predictive analytics into electrical infrastructure workflows to improve load balancing and reduce emergency maintenance events. Companies adopting modular prefabricated power systems shortened commissioning timelines by approximately 25%, strengthening deployment speed advantages in competitive colocation and cloud markets.

Between 2026 and 2028, grid-integrated energy storage, hydrogen-ready backup systems, and AI-enabled adaptive switching technologies will become critical differentiators. Providers securing scalable, low-loss, automation-driven power ecosystems will gain stronger operational resilience, faster AI infrastructure deployment capability, and improved long-term energy optimization competitiveness.

March 2026 – Eaton introduced the Beam Rubin DSX platform integrated with NVIDIA AI factory reference architecture, enabling modular grid-to-chip power deployment for hyperscale AI facilities. The platform supports infrastructure scaling from megawatts to hundreds of megawatts while accelerating deployment timelines from years to months, strengthening high-density AI infrastructure delivery capabilities. Source: eaton.com

May 2026 – Schneider Electric expanded its India data center infrastructure operations as AI-ready deployments accelerated beyond traditional cloud expansion patterns. The company reported that data center operations now contribute nearly 15–20% of its India business, supported by growing local manufacturing and multi-state hyperscale deployment activity. Source: reuters.com

October 2024 – Schneider Electric acquired a 75% stake in liquid-cooling specialist Motivair to strengthen high-performance computing and AI-focused data center cooling integration capabilities. The transaction, valued at approximately USD 850 million, improved Schneider Electric’s position in advanced thermal and power optimization infrastructure for next-generation compute environments. Source: reuters.com

March 2024 – Schneider Electric and NVIDIA launched AI data center reference designs integrating power, cooling, and digital twin optimization technologies for accelerated computing environments. The collaboration improved infrastructure scalability and operational energy efficiency while enabling standardized deployment frameworks for AI-ready facilities across hyperscale and enterprise infrastructure ecosystems. Source: se.com

The Data Center Power Market report provides detailed analysis across critical infrastructure categories including UPS Systems, Power Distribution Units, Generators, Busway Systems, and Battery Systems, with strategic coverage spanning hyperscale, cloud, edge, enterprise, and colocation deployments. The study evaluates operational trends across IT and Telecom, BFSI, Healthcare, Government Sector, Manufacturing Industry, and Cloud Service Providers, highlighting shifting infrastructure priorities linked to AI workloads, modular deployment models, and high-density computing environments. Nearly 58% of hyperscale operators analyzed within the report are actively integrating intelligent energy orchestration and lithium-ion backup architectures into next-generation facilities.

The report delivers region-wise assessment covering North America, Europe, Asia-Pacific, South America, and Middle East & Africa with emphasis on deployment concentration, infrastructure modernization, localization strategies, and power ecosystem resilience. It also examines emerging technologies including AI-driven power management, 800VDC architectures, predictive maintenance systems, and renewable-integrated backup platforms. Strategic insights support investment planning, supply-chain positioning, infrastructure scaling, partnership evaluation, and long-term competitive readiness between 2026 and 2033.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 16387.48 Million |

|

Market Revenue in 2033 |

USD 25727.5 Million |

|

CAGR (2026 - 2033) |

5.8% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Schneider Electric, Vertiv, Eaton, ABB, Siemens, Legrand, Delta Electronics, Huawei Digital Power, Mitsubishi Electric, Cummins, Rittal, Cyber Power Systems, Toshiba Energy Systems, Fuji Electric |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |